Personal Finance

It is with a troubled heart that I look at the continued fighting in eastern Ukraine. I worry about my friends and students in the country who may well be in physical danger soon, if the conflict escalates. As an investment analyst, it’s the financial war the Russians seem quite willing to wage that has my attention.

It should have yours as well.

In our just-released documentary, Meltdown America, one of the experts noted that the Kremlin had already made moves to dethrone the US dollar as the world’s reserve currency before the renewed East-West tensions of this year. Putin has openly threatened what amounts to economic warfare as a response to sanctions placed on Russia after its Crimea grab.

Now bullets are flying—can Putin’s financial ICBM be far behind?

Mind you, the US and global economies are on such shaky ground, they could come crashing down without any help from Gospodin Putin.

One of the things that really struck me while watching Meltdown America was the way the writing was clearly visible on the wall in past cases of financial collapse and hyperinflation—but no one wanted to believe it.

That’s the way I see the US today. Life seems so normal and there’s so much wealth even in poorer regions, it’s hard to believe the cracks in the foundation could really bring down everything built on it. And that’s exactly why the cracks never get fixed; people don’t want to see them, and politicians do everything possible to deny they exist. So they widen and deepen until the collapse becomes inevitable—and I believe we have already passed the point of no return.

It’s just a matter of time now.

Gloomy thoughts indeed, but I’m not here to depress anyone. Hopefully, I can help deliver a wake-up call. Perhaps even more useful, I can tell you what I’m doing about it.

Of course, precious metals and the associated stocks are a key part of my strategy. As Doug Casey likes to say, I buy gold for prudence and gold stocks for profit. If I’m right about the economic trouble ahead, gold will protect me, and my gold stock picks will make me a fortune.

But Doug also says that our biggest risk today is not market risk; it’s political risk. He has moved to rural Argentina to get out of harm’s way. I’ve moved to Puerto Rico, a US territory that is rapidly becoming the only tax haven that matters for US taxpayers.

Million-Dollar Condos for Half Price

As I type here in my new home office, I glance up and see waves of Caribbean blue crashing on the palm-lined beach. Surfers are out in force. Scattered clouds add to the already amazing variety of colors in the ocean. I wonder if I will have time to go for a swim before dinner—and I’m amazed yet again to think that it was a shot at lower taxes that brought me here to Puerto Rico.

It seems almost unnatural for me to be able to enjoy so much beauty while saving money, but that’s exactly what I’m doing.

The view from my new home office.

You see, the economy here never really recovered from the crash of 2008. This is very bad news for long-suffering Puerto Ricans trying to make ends meet. When I first came here with my wife to check the place out, locals kept asking us why we were thinking of moving here; jobs are scarce, and something of an exodus is taking place in the opposite direction (Puerto Ricans are US citizens and can travel and work freely anywhere in the US).

But I wasn’t coming to Puerto Rico to sell hot dogs. My income doesn’t depend on the local economy, so its woes are an obvious opportunity for a contrarian speculator like me.

Take the most simple and basic asset class one can invest in as a Puerto Rico play: real estate. The market has been so devastated that million-dollar condos are selling for half price. When we closed on our new place, the seller came up short, and we had other options, so we weren’t willing to pay more. The real estate agents involved were so eager to keep the deal from falling through, they kicked in with their own money to help the seller out.

Personally, I’m not a big fan of gated communities, but for people who are concerned about possible social unrest in the future, it’s good to know that you can buy properties in some of the most posh and secure communities on the island with no money down.

Now, as much as I like a contrarian bargain, and as much as my wife loves the tropical weather, what really brought us here were the new tax incentives the government of Puerto Rico enacted to make the island more attractive to investors and employers.

The critical point here is that Puerto Ricans are exempt from US federal income taxes, even though they are US citizens. They pay Puerto Rican taxes, of course, and those have generally been similar to US taxes, so the island has never been seen as a tax haven before. That all changed in 2012, when Puerto Rico passed Acts 20 and 22.

Act 22

Act 22 is basically a 100% capital-gains tax holiday designed to attract investors to come live in Puerto Rico. Exactly what is included or excluded is beyond the scope of this article, but for me, the important thing is that it covers the stocks I already owned when I moved here on January 1, 2014. Given that the market bottomed at almost the same time, I have no gains to be taxed on for 2013, and will not be taxed for the gains I make going forward—all the way to 2036.

This alone was worth the move to Puerto Rico, in my opinion.

Happily, the application process was simple. My wife downloaded the form and filled it out. I signed it, and a couple weeks later, we got an official tax holiday decree in the mail—no questions asked. I had to accept the conditions of the decree in front of a notary and send in an acceptance form with a $50 filing fee, and that was it. Didn’t even have to hire a lawyer.

This tax break is not available to current residents of Puerto Rico—it’s designed to attract wealthy people to come live on the island, after all—but it’s available to all others who move here, including but not limited to US taxpayers.

Act 20

Act 20 is a tax break on corporate earnings designed to incent job creation in Puerto Rico. The idea is to persuade US employers who might set up call centers in India, or create other similar jobs abroad, to do so closer to home, by offering them a 4% corporate earnings tax rate.

My fellow Casey Research editor Alex Daley has moved to Puerto Rico as well, and we’ve formed a company here that exports writing and analytical services to Casey Research in Vermont. This is the basis of our application for Act 20 tax benefits, which has not been approved yet, but which we understand is close.

If we get our Act 20 decree approved, we’ll still have to pay regular income taxes on our base salaries, but the lower tax rate applied to our corporate income will result in a drastically lower total income tax rate for us as individuals.

I’ll be sure to let readers know when we get our Act 20 decree approved.

All 100% Legal

The beauty of this is that Puerto Rico’s tax breaks are not shady tax dodges set up by entities of questionable legality or trustworthiness, but perfectly legal tax incentives within the US.

Act 20 and Act 22 benefits are available to non-US persons, but they are especially important to US taxpayers because, unlike almost every other country in the world, the US taxes its serfs citizens whether they live in the US or abroad.

In other words, while a Canadian can get out of paying Canadian income taxes by moving out of Canada, a US person cannot escape US taxes by moving to Argentina, or anywhere else—anywhere besides Puerto Rico.

It’s like expatriation without having to leave the US, truly a unique situation.

And it’s a win-win situation; people like us bring much-needed money, ideas, and energy to the island, while getting to keep more of what our crisis-investing strategy nets us. We create jobs, rather than take them. We are part of the solution here, and we’ve been made very welcome.

Is It Safe?

So that’s why I’m here. Whether or not my Act 20 status gets approved, I’m so happy about my Act 22 decree that I’m convinced we did the right thing moving here.

When I tell people what I’ve done and why, most get immediately excited by the idea—and then they balk. The first question they ask is usually: What about crime?

Puerto Rico isn’t a large island, and a good chunk of its three million inhabitants are clustered in and around the capital city of San Juan. Of course there is crime here, as there is in any large city. There are places I would not walk alone at night—just as there are in New York City.

Mexico City, Buenos Aires, La Paz… the capital of any other Latin American country or Caribbean country I’ve been to is much larger, more polluted, and more dangerous than San Juan. In my subjective view, San Juan, with its old Spanish fortifications and amazing beaches, is more beautiful. And you can drink the water here.

Sure, it might be cleaner and safer in Palm Beach, Florida—but it’s a lot more expensive there, it has less charm, and there’s no Act 20 nor 22. It’s a matter of priorities.

When I say this, most people remain skeptical; they read about the economic problems Puerto Rico has and the financial trouble the government is in, and they wonder if things could get worse.

Of course they can—but if Doug is right about The Greater Depression about to envelop the whole world, things are going to get worse everywhere.

Here at least, people are already used to massive unemployment. It won’t come as a shock; it’s never left since 2008.

Another way of looking at it is that since tropical storms hit the island from time to time (southern Florida is much more prone to major hurricanes than Puerto Rico, but they do happen), people here are more prepared for disasters than in many other parts of the US. The better apartment buildings and hotels have their own electricity generators. Nobody can freeze to death here, anyway, and fruit trees grow all over the island.

There’s a lot more I could say, but the bottom line is that I think Puerto Rico is a much better place to ride out a global financial storm than Miami, or Anchorage, or almost any city in between. A self-sustaining farm in rural Alabama might be better, but that’s not the sort of place I want to live.

I Like It Here

That last is an important point: if I have to hunker down to ride out an economic storm, it should be in a place where I like being.

Puerto Rico is beautiful and bountiful year-round. I speak Spanish, but most people in San Juan are bilingual, so that’s not really an issue. Our new flat is blocks from the best schools, shops, and restaurants in town—and even the hospital.

I open the window and the fresh air coming off the ocean carries the sound of waves, sometimes laughing children. There’s more noise pollution during the day, but at night, the city calms down, and we can hear the famous Puerto Rican coquí frogs, which my daughter calls “happy frogs.” Ten floors up, the ocean breeze is cool enough that we have yet to turn on the air conditioning.

The beaches are fantastic, and the clear water makes for great diving. I’ve never been a surfer, but the waves here are famous too, so I’m thinking of trying it out. There’s no end of other things to try out, and the neighboring islands have their own charms to offer as well.

Granted, my wife and I try to be smart about what we do and where we go, but we’ve never felt unsafe here—well, apart from the crazy drivers.

We like it here. We’re happy. For tax reasons, for quality of life, and with the potential meltdown of America in mind, we’re glad we made the move.

Find Out More

Doug Casey’s International Man Editor Nick Giambruno, Alex Daley, and I have coauthored a special report on Puerto Rico’s stunning new tax advantages. The report gets into all the details I didn’t have time or space for here. We cover all the specifics of what, why, and how. The report includes links to the forms you need, as well as recommended resources, from lawyers to realtors.

Whether you’re thinking about expatriating or you’re just tired of paying high taxes, I think Puerto Rico is a place you should consider. I know of no better resource to help you get started than our special report.

For your own health, wealth, and enjoyment, I encourage you to get your copy today.

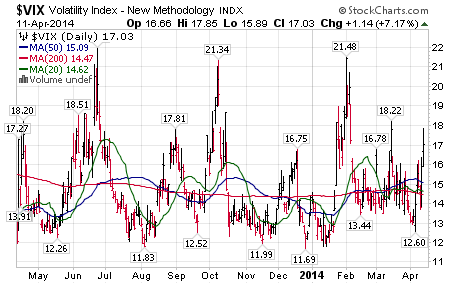

Strength in mid-week last week is expected to prove to be the last chance to take profits in a variety of seasonal trades that were approaching their average exit dates. Intermediate downside risk remains. Any short term strength will provide an opportunity to reduce positions.

The VIX Index spiked 3.07 (21.99%) last week. The Index moved above its 20, 50 and 200 day moving averages.

Technical action by individual equities in the S&P 500 was bearish last week. On Friday, 48 S&P 500 stocks broke intermediate support levels. Look for more stocks breaking support than stocks breaking resistance this week.

Technical action by individual equities in the TSX Composite Index was neutral. Energy stocks dominated the list of stocks breaking resistance. Seasonal influences in the sector remain positive until early May.

Major breakdowns by broadly based U.S. equity indices last week imply that an intermediate correction has started. Short and intermediate technical indicators for U.S. indices and sectors generally are trending down from overbought levels.

Economic news this week is expected to confirm a rebound in the U.S. economy from depressed December/early March weather-depressed levels.

First quarter reports start to pour in this week. Main focus is on the Financial Services sector. Technology also is in focus. The market is anticipating a “difficult” comparison for earnings and revenues on a year-over-year basis. Consensus for S&P 500 companies on average is no change from last year. However, most first quarter reports are released at annual meetings where stock splits, dividend increases and share buy backs frequently are announced.

Historically during U.S. Midterm Presidential Election years, U.S. equity indices have reached an intermediate high near the middle of April followed by a correction that lasts until early October. Technical action last week suggests that the correction this year already has started. We are not alone with this call. Following is a link to a MarketWatch.com call published on Friday with a headline reading, “A bigger 10%-15% correction is coming this autumn: Bank of America/Merrill Lynch”.

http://blogs.marketwatch.com/thetell/2014/04/11/a-bigger-10-15-correction-is-coming-this-autumn-bank-of-america-merrill-lynch/

International focus this week is on China’s first quarter GDP to be released on Wednesday. Consensus is for a slowdown to 7.3% from 7.7% in the fourth quarter. Other international focuses include developments in Ukraine, Venezuela and Iran.

Trading activity is expected to diminish during the week as the Good Friday holiday approaches.

Weakness in the U.S. Dollar continues to impact equity markets, particularly the Materials and Energy sectors.

Equity markets outside of the U.S. continue to show positive returns on a real and relative basis.

Equity Trends

The S&P 500 Index plunged 49.40 points (2.65%) last week. Trend changed from up to neutral when the Index fell below the 1,839.57. The Index remains below its 20 day moving average and fell below its 50 day moving average. Short term momentum indicators are trending down.

The TSX Composite Index fell 135.41 points (0.94%) last week. Intermediate trend remains up (Score: 1.0). The Index fell below its 20 day moving average (Score: 0.0). Strength relative to the S&P 500 Index changed to positive from neutral (Score: 1.0). Technical score based on the above technical indicators slipped to 2.0 from 2.5 out of 3.0. Short term momentum indicators are trending down.

To view 45 more charts & comments go HERE

Special Free Services available through www.equityclock.com

Equityclock.com is offering free access to a data base showing seasonal studies on individual stocks and sectors. The data base holds seasonality studies on over 1000 big and moderate cap securities and indices. To login, simply go tohttp://www.equityclock.com/charts/

What Will The Stock Market and Gold, Do For the Balance of 2014?

What Will The Stock Market and Gold, Do For the Balance of 2014?

If you knew the answer to that question, how would your investment or trading results be different?

Over the past twenty plus years Mark Leibovit’s Annual Forecast Model has provided Wall Street industry professionals with an accurate blueprint of major swing patterns during the course of the year months in advance. This report is sold by Mark for US$450.

For the next 48 hours, to celebrate Mark joining Michael’s Inside Edge team, you can get the 2014 version for only C$29.95. That’s right – only $29.95.

This is your opportunity to view the AFM forecasts for 2014 for the Dow Industrials, Gold, Palladium, U.S. Dollar, 30 Year Treasury Bond and Natural Gas. Just imagine how a road map to the stock market’s future performance would help your investment strategy.

“Inflation is taxation without legislation.” – Milton Friedman

The stock market has recovered a good deal from last week’s momentum-induced slide. The S&P 500 rallied all four days this week, and the exchanges are closed today for Good Friday. All told, this was the best week for the S&P 500 since July.

This is an exciting time for the market. We’re moving into the heart of earnings season. Already about one-fifth of the S&P 500 has reported earnings; 52% of the reports have beaten on revenues, and 63% have beaten on earnings. Both numbers are about average. (That’s right, on Wall Street, beating expectations is to be expected.)

Despite this resurgence, I think the market’s shift to value, which I discussed in last week’s issue, still has some room to play out. I expect to see growth names, especially the pricey ones, lag the overall market. Investors should continue to be conservative and not tempted to chase after bad names.

In this week’s CWS Market Review, I want to address an important topic—the threat of inflation. In the eyes of the stock market, inflation is Public Enemy #1. I want to emphasize that I don’t believe the threat is serious, for now, but there’s already some evidence that inflation’s years-long decline could be over. I’ll have more to say about that in a bit.

I’ll also talk about recent earnings reports from Wells Fargo (pretty good) and IBM (rather blah). Plus, I’ll preview a slew of Buy List earnings coming our way next week, including Ford, Microsoft and Qualcomm. But first, let’s look at where we stand with regard to inflation.

Is More Inflation Headed Our Way?

Those of you old enough to remember the 70s certainly remember inflation. It was the worst thing about that decade. Well…that and disco. Every week, it seemed, prices climbed higher, and the prime rate went up, up, up.

There’s no way to sugarcoat it. Inflation is devastating for investors. It eats away at savings, and it knocks stock prices for a loop. On December 31, 1964, right before inflation became a problem, the Dow closed at 874.13. Exactly seventeen years later, the index stood at 875.00. Stock prices had barely budged, yet the Consumer Price Index had tripled. Then, once inflation got under control, stock prices soared. So much of the 1980s bull market was really making up for lost ground.

Inflation also has an unusual impact on earnings. Not all earnings are the same, and inflation exacts a heavy toll on asset-heavy businesses. Companies with high assets relative to their profits tend to report ersatz earnings.

Let’s look at some recent figures. Last Friday, the Labor Department reported that the Producer Price Index rose by 0.5% last month. That was the biggest increase in nine months. Economists like to track prices at the wholesale level because it’s often an early warning sign of price increases at the consumer level. Digging into the details, the rise in the PPI was driven by a 0.7% increase in wholesale services and a 1.1% rise in food prices. The core rate, which excludes food and energy, rose by 0.6%.

Then on Monday, the Consumer Price Index report showed that consumer prices rose 0.2% last month. That’s still not much, but it was more than the 0.1% economists were expecting. The core consumer rate also rose by 0.2% for its biggest monthly increase in 14 months.

Of course, some of the bad news about inflation could really be good news about the economy. Consumers are buying more stuff, and workers are harder to come by. We had another good initial claims report this week. The price of shrimp, of all things, is at a 14-year high. There have been a lot of silly predictions of about the imminent return of hyper-inflation. Don’t be fooled: every single one of these predictions has failed. The truth is that inflation has been remarkably low—and not just low, but low and stable. The year-over-year core inflation rate has stayed between 1.5% and 2.3% for the last 35 months.

I’m not going to try to predict if inflation will come back, but we have to be realistic and watch the data. One important indicator is the spread between the 5-year Treasury yield and the 5-year TIPs. This is the market’s view of what the CPI will be over the next five years. The “breakeven” spread increased this week to 2.24%, which is up 0.13% since Monday. Also, the back end of the yield curve is starting to flatten. The spread between the 5- and 30-year Treasuries just narrowed to its smallest point in five years.

A few years ago, I ran the numbers on how the stock market reacts to inflation. Here’s what I found:

Now let’s look at some numbers. I took all of the monthly returns from 1925 to 2012 and broke them into three groups. There were 75 months of severe deflation (greater than -5% annualized deflation), 335 months of severe inflation (greater than 5% annualized), and 634 months of stable prices (between -5% and +5%).

The 75 months of deflation produced a combined real return of -46.77%, or -9.60% annualized. The 335 months of high inflation produced a total return of -70.84%, or -4.32% annualized. The 634 months of stable prices produced a stunning return of more than 177,000%. Annualized, that works out to 15.21%, which is more than double the long-term average.

Here’s an interesting stat: The entire stock market’s real return has come during months when annualized inflation has been between 0% and 5.1%. The rest of the time, the stock market has been a net loser.

The Fed’s target for inflation is currently 2%, and we’ve been below that for some time. Fed Chair Janet Yellen said that’s probably due to lower energy prices and lower import prices. I want to make it clear that I don’t think inflation is a problem or will soon be a problem, but the era of rock-bottom inflation may be over. To some extent, a small increase of inflation could be beneficial. American firms are currently sitting on more than $1.6 trillion in cash, and a small boost to inflation might cause them to spend more.

The bottom line is to ignore the doom and gloom crowd. There’s no danger of hyper-inflation but it’s very likely that inflation will creep up to the Fed’s target zone. That will be another reason for the Fed to raise rates. As long as the yield curve is steep, the math is in the stock market’s favor. But the steep curve won’t last forever. Now let’s look at some recent earnings.

Good Earnings from Wells Fargo, Blah Earnings from IBM

Last Wednesday, Wells Fargo (WFC) reported Q1 earnings of $1.05 per share, which beat estimates of 97 cents per share. This was the 17th quarter in a row in which Wells has reported earnings growth.

Wells continues to be the strongest large bank in the country. As expected, their mortgage business got hit hard last quarter, but we saw that coming. Still, Wells was able to grow its loan portfolio by more than $4 billion. Their total loan portfolio now stands at $826.4 billion.

The results were particularly welcome for two reasons. One is that the earnings from competitor and former Buy List member JPMorgan Chase were pretty ugly. The other reason is that shares of WFC were sliding going into the report. Clearly, some traders were nervous, and the results quelled that. Wells Fargo remains a very good buy up to $54 per share.

IBM’s (IBM) earnings were a different story. First, I have to remind investors that many cheap stocks are cheap for a reason. The question to ask is how serious are those reasons. IBM is in a rough patch right now. In many ways, I think the company is in a place similar to where Microsoft was a few years ago.

For Q1, IBM reported earnings of $2.54 per share, which matched Wall Street’s estimate. Big Blue had revenues of $22.48 billion, which missed estimates by $320 million. This is the eighth sales decline in a row. The details weren’t pretty. Hardware sales dropped 23%. System-storage sales also dropped 23%. Software sales rose by just 1.6%. The market was not pleased, and IBM got knocked for a 3.4% loss on Thursday.

Perhaps the most impressive part of the earnings report was that IBM reiterated its forecast of earning $18 per share for this year. Wall Street doesn’t buy it, but it’s noteworthy that IBM hasn’t backed away from that forecast. I like IBM here, but it’s a longer-term story. The stock is going for less than 11 times this year’s earnings. IBM is a good buy up to $197 per share.

Seven Buy List Earnings Reports Next Week

Get ready for a lot of earnings news next week. On Tuesday, CR Bard and McDonald’s are scheduled to report Q1 earnings. CR Bard (BCR) was one of the surprising winners in the early part of this year until the shares pulled back this month. On the last earnings call, Bard said to expect Q1 earnings to range between $1.83 and $1.87 per share. For the whole year, they see earnings between $8.20 and $8.30 per share. I like this stock. Bard has increased its dividend every year since 1972. Expect another increase in a few months. CR Bard is a good buy up to $152 per share.

McDonald’s (MCD) has beaten earnings for the last two quarters, which ended a period in which they missed earnings four times in five quarters. The fast-food joint is working to turn itself around, and some of the early results look promising. Wall Street currently expects Q1 earnings of $1.24 per share. I also like MCD’s dividend, which is currently over 3.2%. MCD remains a buy up to $102 per share. I’m keeping a tight range, so don’t chase it. Let’s wait until we see strong results.

On Wednesday, April 23, Stryker and Qualcomm are due to report earnings. Three months ago,Stryker (SYK) not only beat expectations but also guided higher for the year. Interestingly, the stock initially dropped after the good news. After that, the stock rallied until the middle of February and has bounced along ever since then. The Street sees Q1 earnings of $1.08 per share, which is probably a penny or two too low. I’m curious to hear what they have to say for guidance. For now, I’m keeping my Buy Below at $90, which may have to come down soon. But Stryker is a fine buy.

Qualcomm (QCOM) may be one of my favorite stocks on the Buy List right now. Next to DirecTV, it’s our second-best performer this year. The stock is inches away from another multi-year high. Last month, Qualcomm gave us a nice 20% dividend increase, and three months ago, they sang our favorite tune—the beat-and-raise chorus. A lot of tech heads will be watching this report for clues about Smartphone sales. QCOM is a buy up to $87 per share.

On Thursday, Microsoft (MSFT) will report its fiscal Q3 earnings. It’s odd to see MSFT and its new CEO get so much good press lately. It wasn’t that long ago that MSFT was written off as a dinosaur that was desperately behind the times. Thanks to the hate, we jumped in and made a cool 40% last year with Microsoft. The Street expects 63 cents per share, and I think we’re going to see a nice beat. MSFT is a very good buy up to $43 per share.

On Friday, April 25, Moog and Ford Motor are due to report. Moog (MOG-A) was a big disappointment last earnings season. They missed by a penny and lowered guidance. The stock got crushed—although by the early part of April, it had made back a lot of what it had lost. That’s one plus to owning high-quality stocks. They often bend but rarely break. In this earnings report, I want to hear if business has improved. Moog remains a good buy up to $66 per share.

Ford (F) is also one of my favorite stocks, and I think the shares are very much undervalued. This is a crucial time for Ford, as they’re rolling out several new models this year. Business is improving in Europe, and they may break even this year. The consensus on Wall Street is for earnings of 31 cents per share. I’ll tell you right now, Ford will beat that. Ford is a solid buy up to $18 per share.

That’s all for now. Stay turned for lots more earnings next week. You can see our complete Buy Listearnings calendar here. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Over the last month the energy sector has outperformed the market, and as you can see in the chart below, has done so by 6.5 percent. Year-to-date the sector is beating the S&P 500 Index by over 3 percent.

In a spectacularly performing market during 2013, energy lacked some of the incredible performance seen throughout the other sectors, but recently it has turned up, catching the attention of the market yet again.

What’s causing this sudden shift in relative strength?

As our Director of Research John Derrick describes in our recent video on the Periodic Table of Sector Returns, it is not unusual to see sectors move from top to bottom from one year to the next. For example, energy ranked as one of the top-performing sectors from 2004 through 2007, but quickly lost momentum in 2008 when it was hit the hardest after the financial crisis. In 2012 and 2013 energy turned in some solid numbers, but lagged in comparison to the other sectors.

Click imgage for larger view

In looking at an overview of market performance, it’s important to recognize what caused the moves. For example, one reason the energy sector is climbing back up, could be due to the broader market rotation that we’ve noticed recently, from growth stocks to value stocks.

Growth stocks are generally successful companies that are expected to continue growing their earnings, usually at a rate that outpaces the market, causing investors to pay more for them. Value stocks rarely outpace the market as much as growth stocks do. Investors see potential in buying these cheaper names, ones that trade at lower price-to-earnings (P/E) ratios than the S&P average, because they still have the potential to significantly outperform over time.

As I mentioned, in the past few weeks high-growth names have pulled back, while value names are steadily gaining momentum. One of the main reasons for this rotation is that some investors view the valuations of growth names as too high, especially in comparison to the value companies.

As I mentioned, in the past few weeks high-growth names have pulled back, while value names are steadily gaining momentum. One of the main reasons for this rotation is that some investors view the valuations of growth names as too high, especially in comparison to the value companies.

What’s significant is that many of these value names happen to be in the energy sector. We’ve taken advantage of this shift to value in our Global Resources Fund (PSPFX) through names like Pacific Rubiales and Valero Energy.

Although this rotation is important to the recent moves in energy, it is not the only factor driving the sector up. Take a look at the price of oil and natural gas.

Currently natural gas prices are starting to stabilize while the price of West Texas Intermediate (WTI) crude oil is up by 4 percent year-to-date, reaching $104 a barrel just this week. This price increase in WTI is linked to concerns over future supply, but nevertheless higher oil prices bode well for stocks within the energy sector.

According to the Energy Information Administration (EIA), short-term projections for the price of WTI remain relatively high. Additionally, the group commented that, “Aside from seasonal issues, the EIA expects strong crude oil production growth, primarily concentrated in the Bakken, Eagle Ford, and Permian regions, continuing through 2015. Forecast production increases from an estimated 7.4 million barrels per day in 2013 to 8.4 million barrels per day in 2014 and 9.1 million barrels per day in 2015.” This projection is good for North American producers and service companies.

So how can you gain entry into this energy opportunity?

The portfolio managers and I continue to stay focused on companies that show robust fundamentals and are located in sectors showing strength. Currently, within ourGlobal Resources Fund (PSPFX), we are seeking to capture the latest takeoff in the energy sector through our exposure to companies that appear reasonably valued. In addition to the two I mentioned previously, if you look at the fund’s top 10 holdings you will also see our investments in large-cap names like Schlumberger, EOG Resources and Halliburton.

Are you ready to energize your portfolio? I believe a well-diversified portfolio includes exposure to natural resources. In fact, I am in Tirana, the capital city of Albania, where I have had the opportunity to expand my tacit knowledge by visiting several resource companies.

I am excited to share my journey with you next week when I return home!

Index Summary

- Major market indices finished higher this week. The Dow Jones Industrial Average rose 2.38 percent. The S&P 500 Stock Index gained 2.71 percent, while the Nasdaq Composite advanced 2.39 percent. The Russell 2000 small capitalization index rose 2.38 percent this week.

- The Hang Seng Composite fell 1.16 percent; Taiwan gained 0.41 percent while the KOSPI declined 0.27 percent.

- The 10-year Treasury bond yield rose 9 basis points to finish the week at 2.72 percent.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair