Personal Finance

Argentina, Hungary, France, Portugal, & Ireland, have confiscated some or all Retirement Accounts – Editor Money Talks

Don’t Let Obama Redistribute Your Money

Don’t Let Obama Redistribute Your MoneyNOTE: This is a message from our friends at Personal Liberty Digest that we think you’ll enjoy. – Bill Bonner

“Bail-Ins”… Coming to a Federal Government Near You… Does Obama’s MyRa Signal the Beginning of Wealth Confiscation?

According to USDebtClock.org, our total obligations are a stunning $126 trillion dollars… not the $17 trillion the feds would like you to believe.

That’s more than $400,000 of debt for every man, woman and child in America today.

I’m assuming you don’t have the extra cash to spare, so Obama has just revealed exactly how he plans to get it out of you… MyRA!

Right now, I believe we are on the brink of the greatest money grab in human history.

And they won’t come knocking on your door to get it from you… they don’t have to. They’ll take it with a few keystrokes on a computer.

It’s the Great American Confiscation of 2014-2015 and insiders reveal the Federal Government is seriously considering “nationalizing” your privately held IRA or 401(k). Right now, there’s $21 trillion in CASH sitting in private retirement accounts.

And to politicians your money is a veritable “pot of gold.”

Think it sounds far-fetched? Well, it’s already happening. Retirement accounts have been confiscated in Argentina, Hungary and Portugal… and a dozen other countries—including the European Union—have similar plans in place.

Think it can’t happen in the U.S.? Well, think again!

Now more than ever, it’s time to take drastic measures to keep your hard-earned savings out of the government’s grubby hands.

Good luck—my friend,

Bob Livingston

Editor, The Bob Livingston Letter™

My name is Bob Livingston and I’ve published The Bob Livingston Letter™ since 1969.

Claim my FREE urgent report that can show you how to:

• Bank in secret to avoid becoming a prime target!

• Use your life insurance and special “trusts” to protect your assets!

• Make your transactions and online communications invisible!

• Avoid IRS red flags!

• And much, much more to protect yourself from this grievous Government overreach!

Don’t wait till it’s too late to protect your money, your privacy and your life from the Government or any money-grubbing opportunist spying on you! I urge you—Read my FREE Report NOW!

Good luck—my friend,

Bob Livingston

Editor, The Bob Livingston Letter™

{kind=link}

{kind=link}

{kind=link}

{kind=link}

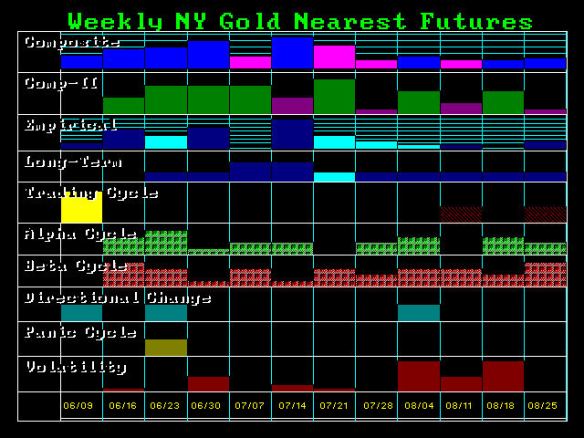

Gold began the bounce on target but we need a daily closing ABOVE 1295 to suggest any further upside pressure. The low was on June 2nd so technically we have fulfilled the first target in time for a June seasonal low. We would need a weekly closing above 1355 to really suggest a brief sustained rally is possible while resistance is starting at 1307 on our weekly models.

The current bounce is due to the shift in currencies. Keep in mind that for a real bull market to form long-term gold must rise WITH THE DOLLAR. Only when it rises in all currencies will we see a bull market. We can see in Euros, the December low is the major low while in dollars we have a double bottom.

We can see the broader pattern in gold expressed in euros. The flat top is a warning that we will see new highs in gold in euros, It appears that our timing models in euros is highlighting an important shift in trend in September 2016.

We can see the broader pattern in gold expressed in euros. The flat top is a warning that we will see new highs in gold in euros, It appears that our timing models in euros is highlighting an important shift in trend in September 2016.

also from Martin today:

The Debt Bubble & Big Money

Canadian home prices hit record in May – A double whammy. Below 2 articles, one on a Calgararian contractor’s view land prices are & the problems that will bring. Also an article on Housing prices hitting a record – Editor Money Talks

Land prices in Calgary are rising so quickly that an affordability crisis could emerge if the city doesn’t make building in the suburbs easier, a local home builder is arguing.

Jay Westman, the chief executive of Jayman MasterBuilt, says there’s a serious shortage of land that can be developed quickly, and it’s causing prices to escalate by the month.

Calgary land prices nearing crisis point, builder argues

The growth in national home prices was not driven by Vancouver this time, with that city’s prices remaining flat after 12 months in a row of increases.

Canadian home prices hit record in May

The FT reports “a cluster of central banking investors has become major players on world equity markets.” – Editor Money Talks

Of all the questions that need answers, I can think of none as universally pertinent as this:

Who is watching the watchers?

The question can be universally applied to just about every controversy and issue in the last several years.

The Patriot Act, rise of the police state, and big data retention with the subsequent rise of hacking certainly could use an answer to the question.

The NSA’s litany of issues need answering too, from wholesale mass surveillance, to lying to Congress while clandestinely monitoring congress members, to claiming that it cannot possibly provide court-mandated records because the systems are too complex to stop deleting evidence.

Here is one to add to the list — central banks and their new and increasingly dangerous addiction to the asset bubble and rising global systemic risk.

Positive Feedback Loop

Today, an organization called the Official Monetary and Financial Institutions Forum is releasing a report called Global Public Investor 2014.

This is the first comprehensive survey of investments held by 400 public sector institutions in 162 countries. These institutions now have $29.1 trillion in market investments, equivalent to about 40% of the global gross domestic product.

The dominant group in this report is made up of central banks, and they account for $13.2 trillion of the assets.

The dominant group in this report is made up of central banks, and they account for $13.2 trillion of the assets.

“A cluster of central banking investors has become major players on world equity markets,” says the report. In a diplomatically worded warning, it also stated that the trend “could potentially contribute to overheated asset prices.”

It appears that the unprecedented economic interventions and policies designed to force investors and businesses into swallowing risk to pursue any meaningful returns have created a positive feedback loop.

Here is how it works:

1. Central banks offer incredibly low interest rates to spur investment by investors and businesses.

2. Investors are forced to accept higher risk to see any gains. Companies with reasonable valuations become increasingly rare.

3. Thanks to incredibly cheap debt from the low interest rates, businesses take the easy path to entice these investors by using share buybacks. They use rotating debt to boost earnings per share, instead of capital expenditures to create meaningful long-term growth.

Corporations capitalized on these low interest rates by issuing $18.2 trillion worth of bonds worldwide since 2008. Currently outstanding corporate debt has risen over 50% to $9.6 trillion over the same period.

4. The policies enacted by the central banks reduce their own revenue. To make up for the shortfall, the central banks invest in the very equities that they are forcing everyone else to buy.

5. Valuations creep up more as fundamentals are abandoned. More businesses and investors chase artificially inflated stock market gains.

6. Central bank policies become increasingly hard to change because any correction would be more severe. Investors, businesses and the central banks themselves would take greater losses. Interest rates stay abnormally low, and the behavior reinforces itself and repeats.

The “Minsky Moment”

At a certain point, this runaway positive feedback loop makes a “Minsky Moment” inevitable.

Paul McCulley of PIMCO coined this term back in 1998, naming it after the late economist Hyman Minsky.

Minsky’s work focused on understanding and explaining the characteristics of financial crises. In particular, he looked at credit cycles.

He argued that during prosperous times, when corporate cash flow rises beyond what is needed to pay off debt, a speculative euphoria develops. Debts eventually start to exceed what borrowers can pay off from their incoming revenue.

Banks and lenders are forced to tighten credit, even to companies that can afford loans. Unsustainable debt causes the forced sale of some assets.

This causes others to sell assets, which causes asset values to drop further and more forced sales to occur.

In the end, far more investors and businesses take greater losses than were actually required to correct the unstable bubble.

Interest rates will have to go up. There is no way around it in the long run. This could easily trigger the Minsky moment for us.

Since many corporations chose to forgo meaningful capital growth and focus on share buybacks, there is little room for revenue growth, making the increasingly expensive debt harder to maintain when rates rise.

If corporations start to fall, a shock would spread through the web of interconnected business to business spending and creditors.

The longer the positive feedback loop created by central banks persists without correction, the wider the gulf between reasonable equity prices and current prices becomes, the greater the damage.

Drinking the Kool-Aid

Perhaps a more reasonable scenario would be panning out right now if there wasn’t an unquestioned belief that central bankers know what they are doing and are in control.

Congress is technically in charge of central bank oversight, but is poorly equipped to question the Fed, let alone understand the implications of complex macroeconomic consequences.

As such, it is much like the NSA. Unless a question is perfectly worded, the same canned general responses are used.

For actual verification of what Congress is told, it takes specific legislation. Case in point: the amendment Sen. Bernie Sanders added to the Wall Street reform law in late 2011.

The amendment directed the GAO to do a comprehensive audit of the Fed. When the report was released, it detailed $16 trillion of transactions in bailouts to domestic and international corporations and banks, there was nothing that could be done about it.

Sen. Bernie Sanders stated, “No agency of the United States government should be allowed to bailout a foreign bank or corporation without the direct approval of Congress and the president.”

Yet there were no consequences for their actions and the implications were under-reported. The same will happen with the fallout from the feedback loop the Fed created. We’ll be reading about it in a postmortem report.

There is no oversight on how central banks are investing in equities. There are no 13F forms to publish holdings and keep tabs on the portfolio. The only option is to trust that they know what they’re doing.

Don’t question the Fed’s actions or the two starkly different classes it is creating in America. Keep buying overvalued equities. Keep making the inevitable “Minsky moment” worse and worse.

If this trend keeps up, central banks will implode with the blind faithful because they bought into their own manipulative scheme.

For your own sake, be very careful and have a contingency plan in place. Don’t drink the Kool-Aid with them.

Take Care,

Adam English

About Adam English

Adam’s editorial talents and analysis drew the attention of senior editors at Outsider Club, which he joined in mid-2012. While he has acquired years of hands-on experience in the editorial room by working side by side with ex-brokers, options floor traders, and financial advisors, he is acutely aware of the challenges faced by retail investors after starting at the ground floor in the financial publishing field. For more on Adam, check out his editor’s page.

*Follow Outsider Club on Facebook and Twitter.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair