Bonds & Interest Rates

Bank Runs in Bulgaria

Bank Runs in Bulgaria

The financial system is simply imploding because those running the affairs of government are more concerned about retaining power than providing economic stability. There are people who are so polarized on each side of many issues from hyperinflation, global elites, socialists hating the rich, communists who see capitalism as evil, and politicians who blame tax avoiders. There is so much polarization within society that there cannot be any solution for everyone has a fixed opinion and only they are right. This is then exemplified in government. They too only see their point of view and it is simply that they lack 100% control of everything (communism) and this is why it is failing.

Now we have bank runs in Bulgaria. The entire fabric is coming undone and this is part of the fuel that sends everything into chaos and the risk of war as tensions rise and people blame someone else be it rich, foreigners, bankers, or corporations. This is the time where clear reasonable thinking and solutions become impossible.

The IMF is now urging the ECB to start buying government bonds of the member states. They have no solutions but the same old bad of tricks. There is nobody even capable of thinking out of the box in a position of power. We are plagued by lawyer-politicians in the total absence of anyone with experience in international money management – the void of experience and statesmanship.

…also from Martin:

Argentina Fights Back

Capital Has Always Invested on Net Return for Millennia

The gold and silver miners have cooled off in recent days after a red-hot start to the summer. Could this cool off be the start of another move lower or a pause before another leg higher? We continue to be bullish and a new reason is the sudden strength in the monthly and even quarterly charts. For larger or developing trends, monthly charts supersede weekly charts, which supersede daily charts. With only two days left, the gold and silver miners are poised to end the month and quarter with their strength intact.

If GDXJ, (shown below) can close June above $41.34 then it will achieve its highest monthly close in 10 months. At the least, GDXJ is set to close at a four month high in monthly terms while engulfing nearly the last three months of trading. Compare that to the monthly advances in July and August of last year and January and February of this year. Those gains were weaker in comparison. Moreover, the strong gains in June are confirmed by the explosion in the volume.

The monthly chart for GDXJ clearly shows long-term support and resistance. The May and June lows (~$33) are support while the next major resistance figures to be $50. In our last missive we mentioned that GDXJ’s next weekly resistance was $44. GDXJ’s June high is $43.52. Recent weakness and consolidation could continue in the short-term. I see support for GDXJ at $39 (and GDX at $24.75). Nevertheless, GDXJ has material upside from here to its next resistance at $50.

GDXJ is a proxy for the junior gold mining sector but I am not a fan for several reasons. It contains too many silver stocks, too many Australian based companies and some companies I would never consider buying. Stockcharts.com now allows subscribers to upload their own data and essentially create their own charts. Below is a daily chart of my top 15 index, which hit a 16-month high last week. Note how the 200-day moving average was resistance in 2013 and is now support. The index could be forming the handle on a small cup and handle pattern that has potentially 27% upside from here. (That upside coincides with GDXJ’s upside to resistance at $50)

There are two takeaways from this article. First, the strength in the monthly (and quarterly charts) should confirm or at least strengthen the argument that the miners are in a new bull market. We have not seen this kind of strength (with volume confirming) to close a month or a quarter since this bottoming process began a year ago. It’s a signal that buyers are more comfortable holding their positions indefinitely.

Second, there continues to be strong upside potential for the sector in the months ahead.

Our top 15 index shows the strongest companies are leading the way for the rest of the sector. Other than monthly resistance at $50, GDXJ has no major resistance until $70. Most of the upside potential remains ahead of us. With the big declines likely behind us, we think it’s wise to take advantage of dips in the short-term as we see potential for roughly 25% upside to Labor Day. We invite you to learn more about our premium service in which we highlight the best junior companies and trade and invest a real portfolio for subscribers benefit.

Good Luck!

Jordan Roy-Byrne, CMT

-

During the second quarter of 2014, many share prices of energy metals companies struggled for direction after the dust settled from the Tesla (TSLA: NYSE) Gigafactory announcement.

During the second quarter of 2014, many share prices of energy metals companies struggled for direction after the dust settled from the Tesla (TSLA: NYSE) Gigafactory announcement. -

Our theme of viewing the supply and demand dynamics of each energy metal individually continues to be the best course of action as the trajectories of each metal may differ. For example, lithium carbonate prices remained healthy while uranium prices fell by 8% in Q2 and are down 21% YTD.

-

The recent precious metals price spike did not transfer over into the industrial or base metals sector.

-

Though economic data continues to improve selectively, there are still too many economic headwinds in place. Therefore only those resource investments that demonstrate the ability to produce at lowest-cost quartile costs or those that have a disruptive competitive advantage should be considered at this time.

-

Despite nascent inflationary pressures, we are still inclined to believe that deflation (or disinflation) is the predominant threat to growth. The recent US Q1 GDP print of a 2.9% decline has many concerned that this was due to more than “the weather”.

- We think that the second half of 2014 will be just as challenging as the first half for reasons we outline below.

….read more HERE

Although markets have been a bit skittish so far this year and despite concerns about growing debt and slower growth, there are plenty of great value opportunities out there for alert investors.

Although markets have been a bit skittish so far this year and despite concerns about growing debt and slower growth, there are plenty of great value opportunities out there for alert investors.

Still, it makes sense to play some defense by hedging your stock picks with what I call “shock absorbers.” Cash, gold, silver, and high-quality bonds come to mind, but there are also some better options out there — namely stable markets and their currencies.

But first, let’s take a look at three qualities that make a country a good hedge and safe haven:

1. Strong, stable currency with ample liquidity

The country’s currency should demonstrate deep liquidity so that investors can move in and out of it without sharp movements in price. It needs to be widely recognized as a reserve currency.

2. Financial and political stability

The fiscal discipline and political stability of the country needs to be unquestioned. Countries with large fiscal deficits are unable to be dependable safe havens since the path of least resistance is to devalue the currency to make debt loads more manageable.

3. Market-based, rules-driven, open economy

Investors and trading partners thrive best in a market-oriented economy where the rules are clear and transparent. Faith in the fairness of the judicial system and institutions is vitally important.

Switzerland and the Swiss franc fit the bill nicely.

For starters, relatively small Switzerland is home to four of the five largest firms in Europe in terms of market value: UBS (NYSE: UBS), Nestlé (OTC: NSRGY), Novartis (NYSE: NVS) and Roche. These companies are increasingly tapping into emerging market growth.

Switzerland also has a number of other factors on its side:

-

It has the highest per-capita income in the world.

-

While it’s only 137 miles by 216 miles in size with a population of 7.2 million, Switzerland packs a punch and is a financial and multinational powerhouse.

-

The Swiss franc is backed by ample gold reserves, fiscal discipline, a trade surplus, and very little foreign debt.

-

Outward looking, Switzerland has 40% of its gross domestic product attributed to exports.

-

Switzerland represents the third-largest financial center in the world after New York and London. It is also home to world-class pharmaceutical, engineering, and food companies.

-

Switzerland enjoys a stable government, vibrant democracy, and a reputation as an asset haven in times of stress. The Swiss have had a functioning democracy for 500 years and actually have a fairly weak central government, with a legislature that meets for only two weeks, four times a year. (Good idea for U.S. Congress?) Voters actually defeated a referendum that would have implemented a shorter workweek and longer vacations.

-

All men between the ages of 20 and 42 are required to engage in military training each summer, resulting in an army of 625,000. Swiss Guards have protected the Vatican since 1506.

Switzerland is on Sale

That all sounds pretty good, especially since the Swiss stock market is trading at a discount to the S&P 500. Now, how should Switzerland become part of your portfolio?

Large, global blue chip companies are almost always favorable due to attractive price-to-book valuations, entrenched brand names, dominant market shares, proven management teams, solid free cash flows, and double-digit growth potential.

What better way to play this trend than with Swiss quality, value, and global growth?

The iShares Switzerland Index (NYSE: EWL) is a smart way to gain exposure to a basket of Switzerland’s leading multinationals and has an expense ratio of only 0.59%. In addition, while a rising Swiss franc puts pricing pressure on Swiss exporters, a strong Swiss franc supercharges returns for investors in EWL.

My go-to stock pick in Switzerland is Nestlé (OTC: NSRGY). This consumer giant has a share-buyback program, a focus on growth in emerging consumer markets, and a rising dividend.

ABB (NYSE: ABB) is a terrific infrastructure play and has been on a tear, winning power and automation-technology contracts all over the world.

You may also wish to pair EWL with iShares Singapore (NYSE: EWS). Singapore is the “Switzerland of Asia,” with $40,000 of foreign exchange reserves for every citizen.

And if you only want exposure to the Swiss franc, take a look at the CurrencyShares Swiss Franc Trust (NYSE: FXF).

You can’t go wrong buying Swiss quality — and it’s even better if the country is on sale.

Until next time,

Carl Delfeld for Wealth Daily

You May Also Enjoy…

What Is An IRM(72) Retirement Plan?

Your Own Private Island for $50k

Crime is far more common than logic. This is the refuge of bankers.

In capitalism’s end game, leveraged debt fatally destabilizes the supply and demand dynamic necessary for stable economic activity. Understanding this is critical to understanding why capitalism today is failing.

In the banker’s ponzi-scheme of credit and debt, debt-based money is created through central bank credit. Usually, the central banks’ constant expansion of the money supply results in rising prices, i.e. inflation. In the end game, however, this is no longer true.

In the end game, when demand slows, excess supply forces prices lower resulting in a deflationary trend called low inflation. In the end game, low inflation continues until demand falls so low the velocity of money is no longer sufficient to support aggregate economic activity; a monetary phenomena that ends in a catastrophic deflationary depression similar to hypotension, a medical condition where blood pressure falls until fatal.

In June 2009 I wrote in my article, Bull Markets, Bullsh*t and Bubbles:

Deflation arises in the wake of extraordinary speculative bubbles and is caused by a collapse in demand which happens after such bubbles pop, when producers/sellers chase buyers hoping to turn inventories and soon-to-be illiquid assets into cash in order to pay down ever-compounding debts.

Deflation happened in the 1930s in the Great Depression, in the 1990s [through today] in Japan and is now again spreading in the US, the UK, [the EU] and other overly mature late-stage capitalist economies; and akin to a deadly economic cancer, deflation, once metastasized, is exceedingly difficult to eliminate.

…The serial dot.com and US real estate bubbles so distorted the global demand and supply dynamic that memories of the 1930s depression have now been re-awakened, memories that will soon become reality as deflation spreads around the world.

…Bubbles and busts have now replaced the expansions and contractions common to early stage capitalism. We are now in late-stage capitalism, where debt instead of credit is the critical factor and the bond markets, not equity markets, determine the economic future.

CONFUSION IN TODAY’S MARKETS

Today, when it looks like a bull, walks like a bull and acts like a bull, it’s probably a bubble. –Bull Markets, Bullsh*t and Bubbles, DRS, 2009

In late-stage capitalism, stock market highs are like a tan on a dying man. Investors formerly seduced by higher stock prices abandon equities as chances of a bubble bursting increase. When this happens, investors move into bonds—capital’s safe haven of choice. In the end game, however, bond markets are where the final bloodbath of capitalism’s debt-based money will take place.

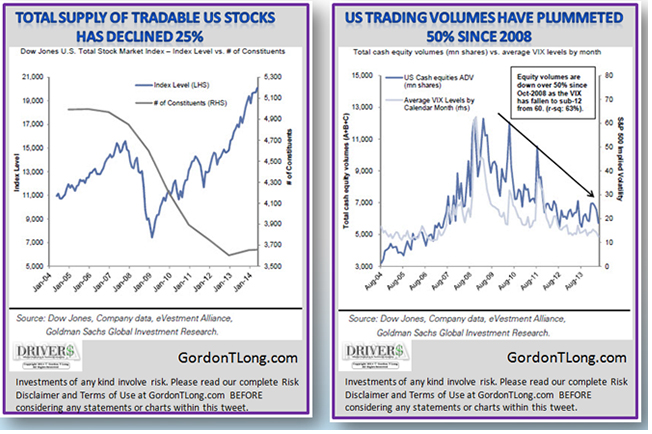

The current stock market bubble is like no other. Even though stock prices are reaching nominal highs, trading volumes are falling. This is the first time in history this has happened.

Two charts from über analyst Gordon T Long provide further evidence that stock markets today are radically different from previous markets.

Today, the Fed and other central banks are so desperate for economic growth they have exacerbated systemic instability by underwriting directly or indirectly the rise in today’s asset markets. On June 15th, the Official Monetary and Financial Institutions Forum, a central bank research and advisory group, noted that central banks and other public sector institutions have, to date, invested $29 trillion in global markets.

Regarding today’s unprecedented market conditions, on June 16th, Citigroup strategists led by Matt King in London wrote: We blame the wave of central-bank liquidity, which has pushed up asset prices irrespective of fundamentals…This creates a vicious circle: ever-higher prices, ever-less trading and liquidity.

Not only has the Fed’s unprecedented and artificial insemination of liquidity distorted equities, bonds, too, are grossly at variance with traditional metrics. On June 2nd, Bloomberg News reported: After unprecedented stimulus by the Fed and other central banks made many traditional models useless, investors and analysts alike are having to reshape their understanding of cheap and expensive as the global market for bonds balloons to $100 trillion.

On June 18th, Mohamed El-Erian, chief economic advisor to Allianz and former co-CEO of PIMCO, the world’s largest bond fund, warned investors of dangers regarding continued central bank support of markets. El-Erian advised: …rather than continuously increasing exposure to ever-rising markets, it is time for highly exposed investors to gradually take some chips off the table.

Instead of betting vast sums on an uncertain future in uncertain markets, smart money institutional investors are now, as El-Erian advised, taking some chips off the table. The dumb money, i.e. private/retail investors, however, are still, literally, buying the bull.

As the odds of systemic collapse rise, safety becomes paramount, even when such safety offers little or no returns. Since peaking in the 1980s, US Treasury interest rates have fallen to almost zero as central banks made credit increasingly cheaper, futilely hoping that with more and cheaper credit, markets can achieve exit speed. In the end game, they can’t.

Despite today’s unprecedented lack of yield, growing distrust of liquidity-driven equity markets, investors are finding refuge in the perceived ‘safety’ of bonds.

Since 2000, investments in bonds are triple the amount invested in equities.

In the end game, the safety of bonds is as illusory as it is fatal.

THE END GAME: PANIC IN THE BOND MARKETS

In 2012, David Stockman, Ronald Reagan’s former budget director, was asked by the editors ofThe Gold Report what catalyst could bring the end game to a final resolution. Today, Stockman’s answer is even more relevant as the end game is even deeper into its final stage.

The Gold Report: If we are in the final innings of a debt super-cycle, what is the catalyst that willend the game?

David Stockman: I think the likely catalyst is a breakdown of the U.S. government bond market. It is the heart of the fixed income market and, therefore, the world’s financial market.

Because of Fed management and interest-rate pegging, the market is artificially medicated. All of the rates and spreads are unreal. The yield curve is not market driven. Supply and demand for savings and investment, future inflation risk discounts by investors – none of these free market forces matter. The price of money is dictated by the Fed, and Wall Street merely attempts to front-run its next move.

As long as the hedge fund traders and fast-money boys believe the Fed can keep everything pegged, we may limp along. The minute they lose confidence, they will unwind their trades.

On the margin, nobody owns the Treasury bond; you rent it. Trillions of treasury paper is funded on repo: You buy $100 million (M) in Treasuries and immediately put them up as collateral for overnight borrowings of $98M. Traders can capture the spread as long as the price of the bond is stable or rising, as it has been for the last year or two. If the bond drops 2%, the spread has been wiped out.

If that happens, the massive repo structures – that is, debt owned by still more debt – will start to unwind and create a panic in the Treasury market. People will realize the emperor is naked.

TRAPPED IN THE HELL OF BOND MARKET ILLIQUIDITY

An illiquid asset is an asset which is not readily salable (without a drastic price reduction, and sometimes not at any price) due to uncertainty about its value or the lack of a market in which it is regularly traded.

http://en.wikipedia.org/wiki/Market_liquidity

The recent and spectacular growth of bond markets has brought with it an equally recent and dangerous downside, i.e. the inability of bond markets to sell what investors have bought. Should bond prices drop 2% as per David Stockman, a panic in the Treasury market will ensue as illiquid markets will prevent investors from selling their bonds as prices fall.

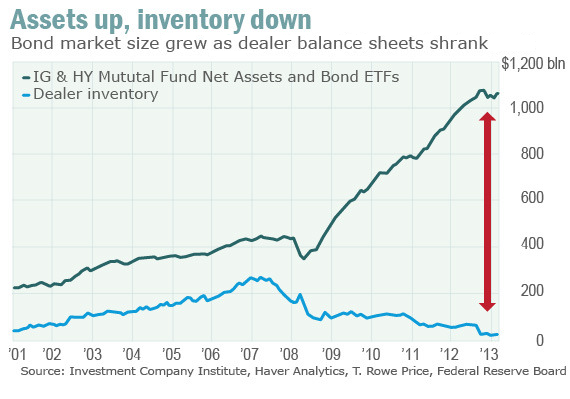

Traditionally, bond dealers provided the liquidity bond markets need to function. After the 2008 financial crisis, however, the ability of bond dealers to do so precipitously declined as the volume of bond purchases inversely grew.

In Mile wide, inch deep – bond market liquidity dries up, a MarketWatch commentary, Ben Eisen wrote: The combination of smaller holdings by dealers and a surge in the amount of outstanding corporate debt suggest that there’s more inventory to change hands with fewer institutions willing to facilitate those transactions. Whereas dealers once held about 4% of all corporate debt on their balance sheets, they now hold closer to 0.5%…

The increasing mismatch between rapidly growing markets and disappearing liquidity will end in a crisis of unprecedented proportions should interest rates rise, driving the value of previously issued bonds lower; resulting in a financial bloodbath where investors are trapped in markets unable to liquidate declining assets.

On June 24, a MoneyNews article, Bond Market Has $900 Billion Mom and Pop Problem When Rates Rise noted that …Investors have piled more than $900 billion into taxable bond funds since the 2008 financial crisis, buying stock-like shares of mutual and exchange traded funds to gain access to infrequently-traded [i.e. illiquid] markets…

If and when the Fed raises interest rates, the concern is that the price of bonds will plunge and mom and pop investors will exit bond funds, leading to an exodus that’ll cause credit markets to freeze up…and a free fall in prices.

On June 16th, the Financial Times reported: Federal Reserve officials have discussed whether regulators should impose exit fees on bond funds to avert a potential run by investors, underlining concern about the vulnerability of the $10 trillion corporate bond market…Officials are concerned that bond funds are becoming ‘shadow banks’, because investors can withdraw their money on demand, even though the assets held by the funds can be hard to sell in a crisis.

Today, credit and debt-based markets have reached their limits and no markets are safe from their coming collapse. Stocks, bonds and commodities will all fall, either serially or as one. This is the bankers’ end game.

GOLD AND SILVER AND THE COLLAPSE OF THE PRESENT PARADIGM

The banker’s house of cards is built on a foundation of paper money. In the beginning, gold and silver provided the stability that paper cannot offer. In 1971, gold was removed from the international monetary system and the cotter pin holding the bankers’ ever-towering edifice of credit and debt was no more.

We are in the end game, where paper promises have replaced the stability of gold and silver. The consequences are there for everyone to see. Equity markets, bond markets, commodity markets have all been poisoned by today’s excessive levels of credit and debt.

Gold and silver are the barometers of systemic financial distress. The bankers’ have done their utmost to disable the most telling indicators of their present disarray and imminent demise. Don’t be fooled, however. In the end game, gold and silver are not investments. They are life insurance policies and when the present system dies—and it will—the payout will justify your faith.

My present youtube video is the 3rd in my current series, Freedom and the Matrix. Once again, central banking is discussed, albeit from another angle. See http://youtu.be/sh5ljkCB5CE.

Take care of you and yours

Take care of others

Buy gold, buy silver, have faith.

Darryl Robert Schoon

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair