Stocks & Equities

The alarm bells went off on Wall Street last week as Federal Reserve Chair Janet Yellen warned of a bubble in social media and biotech stocks. Indeed, in her public comments last week, Yellen stated that biotechnology valuations are “stretched, with ratios of prices to forward earnings remaining high relative to historical norms.”

Since her comments, the iShares Nasdaq Biotechnology ETF (IBB) has declined about 4 percent.

To me, Yellen’s comments were a bit behind the curve. That’s because in a Money and Markets column that was released about two weeks before Yellen’s comments, I warned everyday investors to steer clear of the biotech IPO mania.

But with the S&P 500 health sector having gained a bit over 12 percent so far this year and about 25 percent over the past year, I think it’s worth looking at some of the more established and high-quality companies in the industry for investors looking to participate in the health-care boom without taking on a lot of the risk associated with the high flyers.

If biotech companies are too risky, what’s the everyday investor supposed to do?

If biotech companies are too risky, what’s the everyday investor supposed to do?

In last week’s Money and Markets column, I suggested Becton Dickenson (BDX) as a high-quality core portfolio holding. Becton Dickinson is the world’s largest manufacturer and distributor of medical surgical products, such as needles and syringes. The company also manufactures a wide array of diagnostic instruments and reagents. International revenue accounts for 58 percent of the company’s business.

Another one of my favorite companies in the health-care sector is Medtronic (MDT), whose stock has gained about 16 percent over the past year. Medtronic historically has focused on designing and manufacturing devices to address cardiac care, neurological and spinal conditions, and diabetes.

Medtronic has slightly shifted its strategy to focus on partnering more closely with its hospital clients by offering greater breadth of products and services to help hospitals operate more efficiently. The recently announced $42.9 billion acquisition of Dublin-based Covidien, which pairs Medtronic’s diversified product portfolio aimed at a wide range of chronic diseases with Covidien’s breadth of products for acute care in hospitals, will position Medtronic’s as a key partner for hospitals around the world.

The addition of Covidien ramps up the competition between Medtronic and the No. 1 player in medical technology business, Johnson & Johnson (JNJ), putting Medtronic in prime position to challenge Johnson & Johnson at a time when consolidation and leverage over cost-conscious hospitals is a priority.

Medtronic’s stock has pulled back a bit because the Obama administration wants to stop corporate deals like the proposed Medtronic acquisition that could enable the company to save millions in U.S. taxes by shifting its headquarters to Ireland. But I believe the decline in Medtronic’s stock price represents a buying opportunity for price conscious investors.

As with Becton Dickenson, Medtronic’s strong cash position supports its commitment to consistent dividend growth. With a current yield of 1.84 percent and a dividend payout that’s likely to grow in the future, shareholders can expect a solid cash-on-cash return while they wait for the stock to appreciate.

In today’s risky investment environment, my aim is to focus on high quality and Medtronic and Becton Dickenson are two of the best.

Best wishes,

Bill Hall

P.S. I’ve teamed up with Dr. Weiss to bring you the expertise and guidance the wealthy take for granted, even if you have a small portfolio and can’t afford fat management fees. And I have a proprietary report in which I reveal what the super-rich do right that the average investor does wrong — or doesn’t do at all. You can get your copy, FREE, right here.

One of the hallmarks of the rally in the stock market over the past year and a half has been driven by multiple expansion and not by earnings growth. The market has rallied some 40%, including dividends, over the past 18 months while earnings have only improved approximately 10% over that same time frame.

In addition, a good portion of this growth is from stock buyback activity rather than from organic increases in revenues or earnings. S&P companies bought back more stock in the first quarter of this year than they did in all of 2009 when valuations were much lower. This level of activity is now nearing the peak in 2007 just before markets started their epic decline.

One of the core reasons earnings are hard pressed to advance is due to tepid demand and revenue growth. Revenues for the S&P 500 are projected to only increase 3% to 4% year-over-year in 2014. Wage growth is running at just two percent domestically, just keeping up with inflation and overseas demand is hardly robust right now. Given that the operating margins of the companies in the S&P 500 are at record highs, there are very few operational costs left to cut.

This is why I concentrate on stocks and sectors that are seeing solid organic revenue growth to plumb for possible investment plays. One of these promising areas is energy services. Credit Suisse just raised their growth estimate for global drilling activity in 2014 to 6% to 8% from 5% to 6% previously. In addition, domestic energy service demand remains robust as oil and gas production continues to increase at an impressive rate. Some of these firms should also benefit as this fracking technology migrates to be utilized overseas; China just started the fracking process at a large commercial field. Finally, valuations in the sector are also very reasonable given the overall market multiple.

There are myriad ways to play the solid demand currently happening in energy services. Here are a few I find attractive at current levels.

Halliburton (NYSE: HAL) andBaker Hughes (NYSE: BHI)have the most exposure to North America among the major energy services firms. Both just recently reported quarterly results that beat expectations and showed strong demand coming from the domestic drilling market. Both firms are also seeing even faster international growth.

Both companies are priced right in line with the overall market multiple even as their earning trajectories are much steeper than the S&P 500 driven by revenue increasing at a 10% clip annually. I like Halliburton a bit better here due to the market share leadership in domestic pressure pumping. Over 50% of these contracts should be renegotiated at higher prices by the end of the year. The company is also doing a solid job of providing “value add” services that are improving margins.

For a backdoor play on the growth of energy services some of the railcar manufacturers are benefiting from the huge explosion of oil production over the past half-decade. Not only do they provide the oil tankcars that are transporting a significant and growing amount of the oil being produced domestically, they also build the railcars that haul the “frac” sand needed to get oil and gas from shale formations.

Many of my readers from late 2012 followed me into American Railcar (NASDAQ: ARII) until I sold the shares due to valuation earlier in the year made a tidy fortune. However, my favorite play in this space right now is Trinity Industries (NYSE: TRN).

The company continues to benefit from increasing demand for its railcars and consistently beats quarterly earnings estimates. Trinity Industries has a market capitalization of around $7 billion and the backlog just in its railcar division is over $5 billion. Trinity should also benefit as demand in its construction and industrial segments picks up as the economy accelerates in the second half of the year.

The company continues to benefit from increasing demand for its railcars and consistently beats quarterly earnings estimates. Trinity Industries has a market capitalization of around $7 billion and the backlog just in its railcar division is over $5 billion. Trinity should also benefit as demand in its construction and industrial segments picks up as the economy accelerates in the second half of the year.

Trinity is tracking to better than 50% earnings gain on back of an over 25% increase in revenues year-over-year in 2014. Despite its growth drivers, the shares go for right at 12 times forward earnings; a significant discount to the overall market multiple.

For those investors willing to move out on the risk curve and looking for higher risk/reward play, small cap Key Energy Services (NYSE: KEG) might be worth a look here. The company has been dogged by poor guidance and an investigation into corruption at its smaller Mexican operation. The company also has a high degree of debt.

For those investors willing to move out on the risk curve and looking for higher risk/reward play, small cap Key Energy Services (NYSE: KEG) might be worth a look here. The company has been dogged by poor guidance and an investigation into corruption at its smaller Mexican operation. The company also has a high degree of debt.

Key operates as an onshore, rig-based well servicing contractor. It is in the process of moving approximately 60% of its 40 rigs in Mexico to the United States where it is seeing solid growth especially in the Permian shale region. The company posted a small loss in 2013 and is on track to do so again in 2014.

However, the consensus calls for Key to post 35 to 40 cents a share in earnings in 2015 as revenue growth returns. Insiders bought a good slug of stock at these price levels last year and stock sells for just nine times the earnings it made in 2011 and 2012. Given its small size and slowly improving business fundamentals, I would not be surprised to find the company as a takeout target if M&A activity continues to be robust in the energy sector.

One of the few consistent job and economic drivers over the past half-decade domestically has been the oil and gas sector. In addition to providing high paying jobs and the benefits of increasing energy independence, the recent energy boom has rewarded investors and should continue to do so.

With the market looking as it does there are fewer and fewer places for the individual investor to find real profit potential from fast growing stocks. One of the few remaining is the small cap space, one that’s brought double and triple digit winners to my own portfolio and those of my readers. I’ve just launched a new small cap service called Small Cap Gems, and we’re offering a Charter Member discount. If you’d like to get in on this ground breaking new service or just want more information CLICK HERE.

Positons: Long HAL & TRN

About Bret Jensen

Bret Jensen is the small cap stock lead analyst with Investors Alley. Bret’s small cap newsletter will focus on firms whose growth and value prospects are misunderstood by the overall markets, leading to double and triple digit gains potential. Previously Bret was Co-Founder and Chief Investment Strategist for Simplified Assessment Management, a fund in the top 5% for total returns its inaugural year, and a technology manager in the financial services industry.

We see markets “priced for perfection”…vulnerable to a correction…from a geopolitical shock or from a growing perception that the Fed will raise interest rates more and faster than people think. We think it’s time for investors to get defensive…we see signs that the smart money is already taking money off the table.

We see markets “priced for perfection” as yield-hungry investors pour billions of dollars into the sovereign bonds of obscure countries at tiny premiums over US Treasuries…as option volatility falls to all-time lows…as leverage ramps up to all-time highs. Our good friend BOB HOYE describes the recent market condition as, “Euphoria in the credit markets!”

David Rosenberg reminds us that it’s been 8 years since the Fed raised rates…that we’ve gone 33 months (double the norm) without so much as a 10% correction in the stock market…but last week the DJIA registered a new All Time High Weekly Close…despite geo-political shocks in the Ukraine and Gaza.

BUT…we see signs that the smart money may be quietly slipping out the back door…or at least getting much more defensive. We think capital is moving from the periphery to the center.

For instance, so far in July:

1) Treasury bonds have rallied while “weaker credits” have fallen…credit spreads are widening.

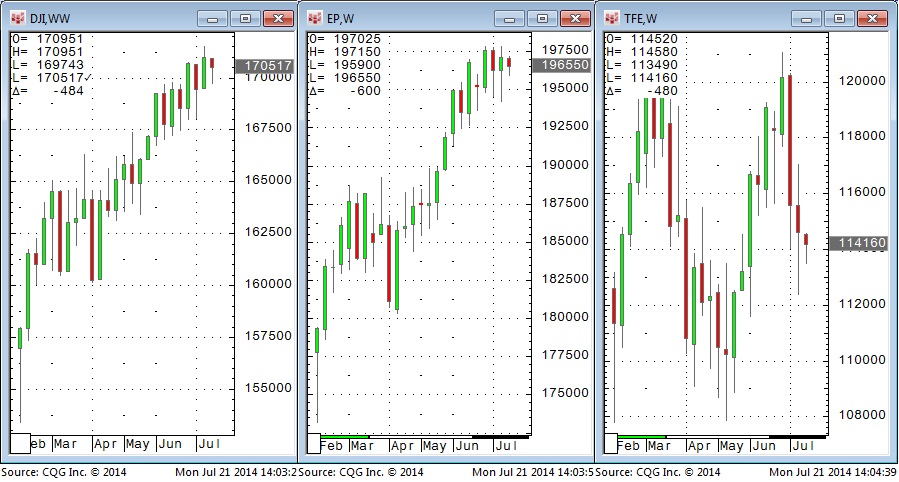

2) The DJIA has made new highs but the broader S+P 500 has gone sideways…while the much broader Russell 2000 is down…the major European stocks markets are down…(L to R: DJI,S&P,Russell)

3)The US Dollar has been rising against most currencies and if it rises another 1.5 to 2% (trading above 8100/8150 ) it will register a significant breakout.

We’ve been anticipating a reversal in bullish Market Psychology to cause:

A sharp widening in credit spreads

A break in the stock market

A higher USD

We think the reversal in Market Psychology has begun…that the key market to watch is the US Dollar…because if the US Dollar starts to rally then EVERYTHING changes. (See: Ambrose Evans-Prichard’s prediction of a “BLISTERING US DOLLAR RALLY” on www.VictorAdair.com)

We think that over the next few years the US Dollar could rally like in did during President Reagan’s first term (it DOUBLED in just over 4 years) or during President Clinton’s 2nd term ( it rose more than 50% in 6 years) as global capital flows to the relative safety of the USA…to the much freer and more innovative American markets…here’s a quote from our July 2nd blog:

“Longer term we expect inflation to erode the purchasing power of the dollar….but capital flowing from the rest of the world to the relative safety of America would see the dollar rise against most currencies. We can imagine a rising USD, rising interest rates and rising stock markets all happening at the same time…a “virtuous circle” based on a relatively stronger and safer America drawing capital from the rest of the world…with that capital flow pushing stocks higher and those gains drawing more capital to America…thus continuing to boost the USD Vs. other currencies. Something similar happened during the 1995 to 2001 period (Clinton’s 2nd term) when capital flows created a virtuous circle of rising interest rates/rising USD/rising stocks which caused the US Dollar Index to rally ~50% and the S+P 500 to gain more than 200% (while the US$ price of gold fell from around $400 to less than $300.)”A US Dollar Bull Market is not typically good for gold, commodities or commodity currencies.

Short term trading:

We remain long the US Dollar Index…and short CAD. We’re looking for other opportunities to make “USD bullish” trades…waiting for markets to “set up” for short positions…possibly in NZD, GBP and EUR. We may buy the Yen Vs. USD and/or EUR. We have taken very short term short positions in the S+P…waiting for “set ups” (for instance, a break of 1940) to confirm that it’s time to take longer term positions.

This week, Bank of Canada Governor Stephen Poloz took the opportunity once again to talk down the Canadian dollar, as he has at almost every opportunity since he took the helm of the central bank.

His plan has been working for the most part as the Canadian dollar has been on a downward trajectory since Mr. Poloz took over. It eroded in the first quarter of the year, and rebounded in the second, most recently trading in a range of about US$0.93 to US$0.94.

The central bank has for some time now held what is known as a neutral bias, which means it’s sending no signal to the markets of whether the next move in its benchmark rate could be up or down. Governor Poloz, however, has left the door open to a rate cut, which has had helped hold the currency down. And the weak jobs report from Statistics Canada last week helped feed into that.

“While there’s no disputing the Canadian manufacturing sector has been in secular decline for more than 30 years, the Loonie has been a pivotal factor in driving activity,” senior economist Benjamin Reitzes of BMO Nesbitt Burns said in a research note this week.

“Clearly the run to parity had a devastating impact on the sector,” he added, referring to his research – posted in chart from below – that shows how the movement in the currency has affected factory jobs, with a lagging impact.

“The only good news here is that the chart suggests we may be nearing a bottom on manufacturing employment. Indeed, if the Loonie weakens as we expect, that could mean some improvement in a year or two.”

This past Wednesday, shrugging off a recent surge in inflation as temporary, the Bank of Canada warned the country’s economy does not yet have enough steam to grow without the bank’s help and said it could just as easily cut interest rates as raise them.

The central bank, as expected, kept its key overnight rate at a low 1%, the stimulative level at which it has been for 46 months. But Governor Stephen Poloz made clear he is worried about downside risks to the economy after “serial disappointment” with global growth in recent years.

“Monetary conditions today are highly stimulative and it’s evident that we don’t have a process of natural growth in the economy yet,” he told a news conference.

The central bank said it would keep its policy stance “neutral,” meaning its next move could be either a tightening or easing.

Small-Cap Opportunities in Exports?

While we see the potential for opportunities to present themselves in the Canadian export sector in a lower dollar environment, we are careful not to base our analysis strictly on this one factor. While the current bias appears to be for a lower Loonie, this is far from a fait accompli.

At this stage, we prefer to invest in quality companies, be they Canadian exporters or Canadian energy producers for example that are already profitable and well run and would benefit further from a lower Loonie, but do not require that type of environment to be profitable and ultimately successful.

KeyStone’s Latest Reports Section

Here We Go Again….

{mp3}/mikesdailycomment/mc07221422{/mp3}

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair