With a non-stop flow of propaganda from Western mainstream media outlets, today Michael Pento sent King World News a fantastic piece which puts aside the propaganda and lays out what is really taking place. Pento also discusses what to expect in the future.

With a non-stop flow of propaganda from Western mainstream media outlets, today Michael Pento sent King World News a fantastic piece which puts aside the propaganda and lays out what is really taking place. Pento also discusses what to expect in the future.

Personal Finance

Looking over a 2007 report on Irish real estate last week, I got a chill when I ran across this line: “Most available evidence would now appear to suggest that the housing market appears to be on the way to achieving a soft landing.”

Looking over a 2007 report on Irish real estate last week, I got a chill when I ran across this line: “Most available evidence would now appear to suggest that the housing market appears to be on the way to achieving a soft landing.”

Sound familiar? It’s a line Canadians have been hearing for years, recently from Finance Minister Joe Oliver and the Bank of Canada. ….continue reading HERE

Hat Tip To- Investor Relations Vancouver

Smart, Courageous, Industrious & Successful….

{mp3}/mikesdailycomment/mc072914{/mp3}

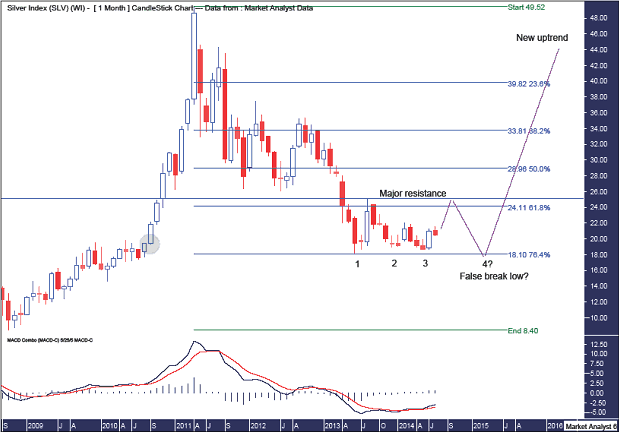

With silver recently putting in a nice 10% plus rally, I thought it was time to follow up my last article on silver, Silver Set To Stun. It’s been two months since that article so there is some new information to process. Let’s get straight into it with the monthly chart.

I showed this chart in my previous article but I thought it would be good to refresh our minds and provide a good overview.

I have added Fibonacci retracement levels of the upleg from the 2008 low to 2011 high. Price is finding support at the 76.4% level of US$18.10 after having had three cracks at it. A triple bottom.

Price has bounced strongly off this last bottom and with the Moving Average Convergence Divergence (MACD) indicator currently looking bullish, the blue line being above the red line, perhaps we can expect price to continue higher over the next couple of months.

However, triple bottoms (and double bottoms) are actually not a common trend ending pattern so it is unlikely that price will rise above the previous major swing high set in August 2013. This is denoted by the horizontal line labelled Major resistance and stands at US$25.13.

So, if that analysis is correct, we could expect price to turn back down and bust the triple bottom low of US$18.17. However, I don’t believe this will be a clean break. On the contrary, I think it will only be a marginal break before reversing and putting in a false break low. Why?

Well, firstly, Gann noted that price normally busts support (and resistance) on the fourth attempt. But if a clean break lower isn’t made then that is a very bullish sign. And combine that with a common false break low pattern that runs all the stops that will have built up under the triple bottom low. A nice combo in itself!

So we have three pieces of evidence suggesting the triple bottom price level is a good candidate for the final low price. First, the 76.4% Fibonacci level. Second, an unsuccessful fourth attempt at support which is very bullish. And third, a common false break low pattern.

But let’s add another piece of evidence. If three’s a crowd, then four’s a party! We can see in the green highlighted circle is where price really started to streak away. That is the level whereby price went parabolic. And when correcting, price often pulls back to the level where the explosion higher began. And the current triple bottom is smack bang right in this zone. Woohoo.

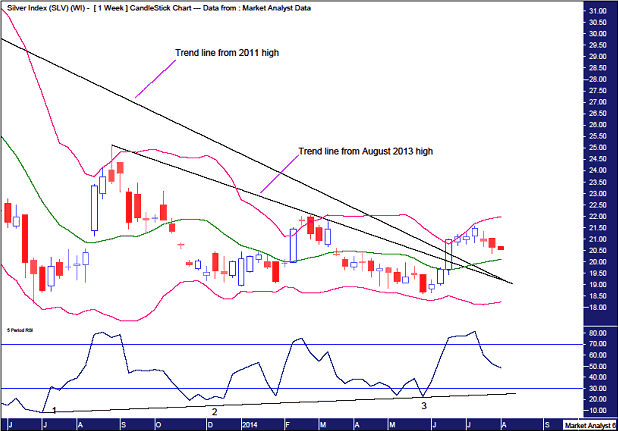

Before we crack open the champers, let’s calm down and move onto the weekly chart.

I have drawn two black down trending lines. One from the 2011 high and one from the August 2013 high. This recent rally has busted above both of these trend lines. The silver bulls are getting all giddy over this. And fair enough. It’s the first glimmer of hope they’ve had in yonks.

But price looks to be retreating in the very near term. I have added Bollinger Bands and while price has retreated from the upper band it may find support around the middle band. And the Relative Strength Indicator (RSI) looks to be building strength as demonstrated by the up trending line I have drawn along bottoms. So once price finds support shortly, perhaps we could expect a nice push higher. The bulls are certainly pawing the ground ready to charge!

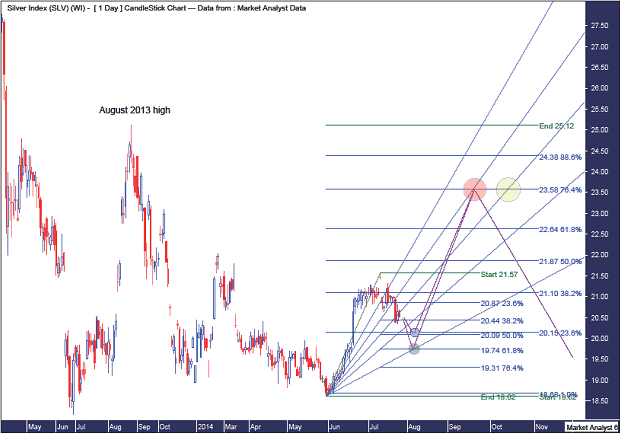

Let’s wrap it up by looing in close with the daily chart.

Ok, this looks a bit daunting but let’s break it all down. We’ll begin with the small picture. Price recently rallied from its May low to recent July high. Price now appears to be correcting that rally. I have drawn Fibonacci retracement levels of this rally to help determine where this little correction may end. The two levels that stand out to me are the 50% and 61.8% levels at US$20.09 and US$19.74 respectively. The little blue circle is at the 50% level while the 61.8% level is shown in the little green circle.

I have also drawn a Fibonacci Fan and interestingly the 76.4% angle looks to intersect with the 61.8% level towards the end of the first week of August. From the weekly analysis, we could surmise that this time period for a pullback low fits in quite nicely. Let’s see.

Once the low is in, I’m expecting a strong rally that will put that of gold’s to shame The break above the two down trending lines, as shown on the weekly chart, should provide a good springboard for the next rally. The permabulls are already salivating in anticipation. But more disappointment awaits if my analysis is correct. Knowing that triple bottoms generally don’t end trends, the probability is that the August 2013 high won’t be broken. So, where will the rally end?

I have drawn Fibonacci retracement levels of the down leg from the August 2013 high to recent May 2014 low. I favour a deep retracement, at least up to the 76.4% level and possibly higher. I have drawn two highlighted circles where the 76.4% level intersects with a couple of Fibonacci Fan angles – the 38.2% angle as shown in the orange circle and the 50% angle as shown in the yellow circle. The orange circle occurs in mid September while the yellow circle occurs in mid October. So they are potential timing periods to look for a high. Personally, I favour the orange circle scenario. Let’s see.

Now price may rise even higher so I have added the rarely used 88.6% Fibonacci level. If the 76.4% level is broken then watching this level and where it may connect with any fan angle may reveal the final rally ending point.

I’m not currently involved here, still expecting the final false break low, most likely in 2015, to provide my main entry point. But I’m certainly tempted to get a sliver!

By Michael Pento of Pento Portfolio Strategies

July 27 (King World News) – Forget The Propaganda, This Is What’s really Happening

Baseball great Yogi Berra had a saying “It’s déjà vu all over again,” and every year around this time, I am reminded of those words. As we have once again happened upon that magical time of year I call, recovery summer déjà vu. It’s the time of year when Wall Street and Washington apologists trot out their dog and pony narrative, in an attempt to spin the actual data, proving we have finally embarked on the summer that will launch sustainable economic growth….

….continue reading HERE

While we are busy arguing whether the Fed’s exit will consist of rising rates, reverse repos or the trimming of its massive portfolio, the Fed may well be fooling all of us. Investors must have been swallowing lots of blue pills not to see the illusion hiding in plain sight.

Let’s assume that we will indeed get a rate hike next year, and that the Fed will have figured out how to implement it. We may get our exit all right, but it’s not the sort of exit most appear to be expecting. That’s because in our humble view, an “exit” ought to reflect a path towards normalization, away from financial repression, back to an environment where pensioners might once again be able to live off income generated from their savings.

If anyone dares to take a red pill, you will learn that interest rates net of inflation, i.e. real interest rates, have not only continued to be negative, but become more negative of late, meaning inflation has started to inch upward. For normalization to occur, interest rates must move higher faster than the pace of inflation; and not only do real interest rates need to move higher, they ought to move into positive territory to suggest we might be exiting financial repression.

The chart above shows real interest rates in the U.S. versus the Eurozone. While pundits focus on the fact that the European Central Bank (ECB) now has a negative rate on deposits, most forget the inconvenient truth that real interest rates are higher in the Eurozone than the U.S. Not only are rates higher in the Eurozone, but the gap has also been widening. Yet, investors appear to be embracing the storyline that rates will be lower for longer in the Eurozone, as we have the Fed about to raise rates.

The above chart shows headline consumer price inflation (headline CPI). Given that the Fed (unlike the ECB) focuses more on core inflation, below is a comparison of core CPI in the U.S. versus Eurozone:

Critics of the Fed suggest that U.S. inflation is higher than reported, further increasing the threshold to get us away from financial repression.

In the meantime, ECB head Draghi is trying to convince investors that rates in the Eurozone will stay lower for longer; Draghi has even said that real interest rates are negative and are likely to become more negative over time. The relevance to this discussion is simply that there’s a central banker being frank. And the reason he is so frank may well be that it is far more difficult to induce inflation in the Eurozone than in the U.S.

In the U.S., we see inflationary pressures come up in pockets. Full-time employees, for example, appear to have pricing power, even as the Fed’s preferred gauge of all employees remains fairly stable. In our assessment, we have a bifurcated recovery where those with assets, those with jobs, do well, but the have-nots are left behind. And because Fed Chair Yellen cares about Main Street, she wants to keep rates low until the have-nots have recovered from the Great Recession.

Are economically disadvantaged Americans really so different from Portuguese workers? At the risk of grossly oversimplifying the respective challenges, keeping rates low to help out those left behind might allow inflation to creep up elsewhere. Conversely, consider the prosperous end of the spectrum? Clearly there are differences between wealthy Americans and the German economy, but inflation has been creeping up in their respective domains.

What is different between the Eurozone and the U.S. is that the U.S. economy is far more sensitive to the markets, whereas the Eurozone economy is dependent on the health of banks. And given the ongoing balance sheet challenges faced by Eurozone banks, I don’t think one needs to be a rocket scientist to determine that inflationary pressures more easily build in the U.S.

In the U.S., much of the economic recovery is based on asset price inflation: when homeowners are no longer ‘upside down’ in their mortgage, they might be better consumers. As asset prices have floated higher the wealth effect might get consumers to spend more. Aside from the problem that lots of folks have been left behind in this so-called recovery, it may be at least as much of a challenge that such a recovery is rather unstable, as the “progress” may be lost if asset prices come back down. Positive real interest rates could create immense headwinds.

The other big challenge is that we might not be able to afford positive real interest rates. When Yellen was asked about the impact of higher rates on the federal deficit, she dodged the question. However, if indeed we went back to historical levels in interest rates then, based on Congressional Budget Office (CBO) projections on deficits, we might be spending $1 trillion more a year simply to pay interest on our debt. Given the gridlock in Congress may make it impossible to achieve the necessary reforms to either raise the revenue or cut taxes sufficiently to make U.S. deficits sustainable, the Fed has a tremendous incentive to keep rates low…

As we discussed in more depth in our recent Merk Insight ‘Instability the New Normal?’, one of the Fed’s biggest achievements is to compress risk premia, to make risky assets appear less risky (as evidenced, for example, by low volatility in the stock market or low yields available in the junk bond market). If the Fed indeed were to pursue an ‘exit,’ odds are that risk premia would go back up – a more fearful environment may cause substantial headwinds to the economy (as well as asset prices). Again, a major incentive for the Fed to keep rates low.

Yellen appears to be aware of at least some of these forces as she recently testified that headwinds to the economy may well persist even as the Fed raises rates.

To make a long story short, yes, nominal rates may be rising. But don’t count on real rates moving up, let alone into positive territory, anytime soon. Indeed, I fear inflation may be picking up much faster than interest rates. In that environment, Draghi’s predictions of rates becoming more negative over time will very much apply to the greenback as well.

And before people lash out at me for downplaying the challenges in Europe, don’t read me wrong: I very much agree that Europe is a mess; it has always been a mess and is likely going to remain a mess. But that’s not the question I’m addressing here. All I’m arguing is that real interest rates in the Eurozone are likely to remain higher than in the U.S.

It shouldn’t come as a surprise that we like gold in this environment: a) because real interest rates are negative; and b) because we expect real interest rates to remain negative for a long time. In fact, if you look at how incentives are aligned, they point towards inflation, as both the U.S. government and consumers – given their high debt loads – might want inflation to debase the value of their debt. It’s foreigners holding U.S. debt that suffer the most from U.S. inflation as they have an interest in preserving the purchasing power of the debt. As foreigners are not voting, it speaks volumes about the path of least resistance – or at least the path of greatest temptation.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair