Gold & Precious Metals

Mario Draghi and the European Central Bank (ECB) shocked financial markets this week when they yet again revealed they were prepared to further combat a stagnating European economy. They announced they were lowering three key policy rates to their ‘lower bound’ and unveiled an unconventional QE style stimulus program to purchase non-financial private sector debt. Unfortunately, the implicit message delivered was that their policy options are becoming exhausted, and consequently further accommodative policy saw the euro fall over 2 cents on Thursday against the US dollar.

Mario Draghi and the European Central Bank (ECB) shocked financial markets this week when they yet again revealed they were prepared to further combat a stagnating European economy. They announced they were lowering three key policy rates to their ‘lower bound’ and unveiled an unconventional QE style stimulus program to purchase non-financial private sector debt. Unfortunately, the implicit message delivered was that their policy options are becoming exhausted, and consequently further accommodative policy saw the euro fall over 2 cents on Thursday against the US dollar.

The trimming of the key policy rates is only somewhat significant as they have taken their deposit rate, the rate of interest charged to financial institutions, further into negative territory. Ideally, no financial institution is going to take a loss or pay the ECB interest to hold their cash overnight, and ultimately it’s a facility that will not be used. In theory, it’s to create the disincentive to deposit funds with the ECB, and instead incentivise them to make money available to the business sector.

The other key lending rate to focus on is the refinancing rate, which the ECB cut to 0.05 percent. This is similar to where the Federal Funds Rate in the US sits between 0 and 0.25 per cent, and at 1 per cent in Canada. And again, a marginal 10 basis point cut does not make a huge material difference to incentivize banks to now borrow more and make loans, but it almost acts as part of a last resort move for the ECB attempting to stave off a deflationary environment.

These further rate cuts seem like a last resort tool for the ECB in terms of utilizing their conventional policy tools, which clearly are not providing the incentives with the liquidity to spur economic activity in the respective economies. With powerhouses like Germany actually seeing GDP growth contract in the latest quarter, and Italy now entering a triple dip recession, this crisis still very much drags on in Europe. But the question is, as monetary policy sees a diminishing impact, can further accommodation prolong the structural reforms so desperately needed?

Mario Draghi said at his press conference that these measures will only work if they come with the structural reforms on the fiscal policy side, and that is left up to the individual European governments. But as the ECB looks to protect its mandate of price stability in the euro, similar to that of the US Fed, policies in the last week have entered the experimental phase as they begin their targeted bond purchases.

The biggest shortfall of monetary policy in Europe was that it was not filtering through to the businesses that hire workers and advance the economy. As was seen by continuously lowering policy rates, credit has largely remained unavailable to the small and medium size enterprises. The announcement of purchasing asset backed securities is the first step in how the ECB plans to combatthis.

As Draghi dictated and the market reacted, this is a policy that ultimately weakens their currency, where on Thursday the euro reacted and fell to its lowest level since July of last year. Many are drawing comparisons to this and the Fed’s Quantitative Easing, or Abenomic’s and its three arrow approach in Japan. Moreover, the ECB is really the last major central bank to join the experimental policy party, and whether they will be successful is not the question, as six years into recovery, investors have learnt the hard lessons of not betting against central banks. Instead, what is the cost of experimental policy and ongoing government malaise?

A question we are still awaiting an answer to here in North America.

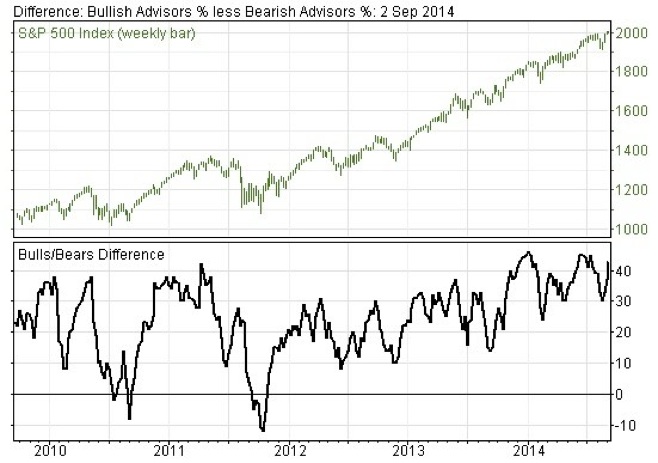

Today a 42-year market veteran warned King World News that great danger now looms as investors say goodbye to summer and global trading enters the final few months of this year. Below is what Egon von Greyerz, who is founder of Matterhorn Asset Management out of Switzerland, had to say in this fascinating interview.

Greyerz: “Looking around the world it is astounding how investors are ignoring risk in their investment strategy. Global stock markets are in bubble territory, but the massive liquidity and the lemming mentality of investors have led to a total disregard of the risks that stocks represent today….continue reading the Egon von Greyerz HERE

…also another article titled: The Remarkable Chart The Big Money Is Watching Right Now – Below is the chart it focuses on:

‘I’ve been waiting for this day for more than a year now when I first created this long term US dollar chart” – Rambus

Full article at this site where all 6 charts are in full size without having to click on each one. – Money Talks Editor

Click chart for LARGE image & Analysis

Here is one interpretation of when we’ll run out of each metal or energy source. While the technicalities of some of this information can be debated, I think the general theme runs the same. There is a limited supply of these commodities – and if there are no discoveries, no price changes, and no changes in consumption, we are running out relatively soon. In my opinion, there are two caveats that are always worth considering when looking at something like this.

1. “Reserves” are an engineering number that are based on economic viability. Technically speaking, there are small concentrations of gold everywhere. It is just not usually viable to mine 0.1 g/t gold. When we will “run out” of each mineral in this chart is based on current reserves and prices. If the gold price doubles, then suddenly it is economic to mine more.

2. This chart is a reminder that something has to give. Either prices are going to have to go up, or new amazing discoveries have to be made to keep prices down. It’s basic economics, and either way it seems that there are many opportunities in the mining industry for investors and speculators on both fronts.

In recent weeks we wrote about the ongoing consolidation in precious metals miners. We touched on the history of September, not as a bullish month but as an important inflection point. With the miners holding up well and Gold still holding its lows we thought a breakout could be coming. Yet we’ve been whipsawed before. Several times over the past year (and as recently as late July) we’ve written about the possibility of a final low in Gold to precede the next impulsive advance in the miners. These scenarios came to a major head this week and the nasty decline across the entire sector suggests the bears are back for one last time.

Below is our chart for Gold’s bear markets which are scaled to the 2011 peak. We exclude the two extreme bears (one lasted six years while the other was the post bubble crash). Longer bears tend to be less severe in price whereas the most severe bears in price tend to be short in time. Examples of that include the 1975-1976 and 1983-1985 bears. The 1987-1993 bear (the longest) only shed 35% while the 1996-1999 bear, which lasted three and a half years bottomed well above $1100 on the current scale. History makes a strong argument that while a new low is likely, anything much below $1100 appears unlikely.

The next chart shows all of the bear markets in Silver sans the 1980-1982 bubble crash. A close below $18.82 would mark a new weekly low. This analog makes a very strong case that Silver’s bear is likely to end in the coming weeks or months.

Staying with Silver, we note that while Silver could make a new low it would soon find 11-year trendline support. This is another reason we will be very bullish on Silver if it breaks to a new low.

So how does affect the miners?

Until days ago the miners looked very strong and on the cusp of a breakout. That possibility has gone out the window. The chart below shows a nasty reversal in our top 40 index which is down 7% on the week and officially broke its consolidation low on Thursday. The index closed Thursday at 382 and the next strong confluence of support is near 350.

GDXJ is down 9% this week and sliced through support on big volume. The next strong support is the previous low around $33. There is nearly 15% downside to that strong support.

Going forward, $1240 Gold and $1200 Gold on a weekly basis are key levels to watch. The miners are very oversold in the short-term and should bounce along with Gold (from $1240). However, the bears have regained control. The bear analogs are quite clear and the miners have suffered major damage which implies more downside. I don’t envision a buying opportunity for the miners until Gold and Silver make new lows. This week could mark the start of that final plunge that has eluded us several times over the past year. We invite you to learn more about our premium service in which we highlight the best junior companies and manage a real portfolio for subscribers benefit.

Good Luck!

Jordan Roy-Byrne, CMT

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair