Currency

Trying to pick a profitable trade in the foreign exchange market is similar to judging a “reverse beauty” contest, that is to say, the winner is the least ugly currency at any given moment in time. All paper currencies are ugly, because central bankers print vast quantities of fiat currency, to varying degrees, at the behest of the ruling political elite that appointed them to run the printing presses. “By this means, government may secretly and unobserved, confiscate the wealth of the people, and not one man in a million will detect the theft,” – the late British economist John Maynard Keynes, used to say.

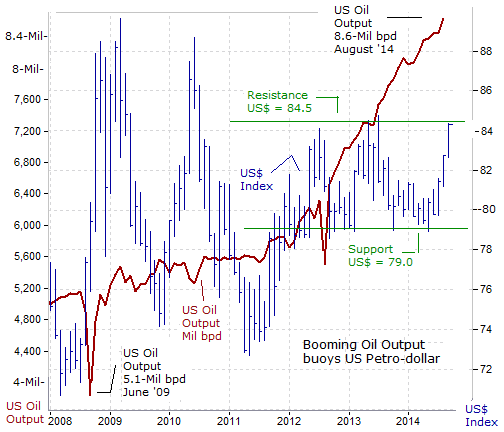

In the arcane world of foreign exchange, the axiom, – “the trend is your friend,” – is a reliable piece of advice, since trends in currency pairs can extend for many months, or even years, and often lead to double-digit returns. As such, the US-Dollar Index, which measures the US$’s value against a basket of six major currencies, has suddenly risen +5% higher over the past nine weeks, to above the 84-level, marking its longest streak of weekly gains in 17-years. Many traders are beginning to wager that the US$’s recent bout of volatility is harbinger of a longer term rally that can extend into 2015.

If the US$ index can manage to break through key horizontal resistance at the 84.50-level in the days or weeks ahead, it would signal a technical breakout to higher ground. Already, the US$ has rolled up its biggest gains against Japan’s yen, climbing +40% higher from above its all-time lows around ¥76, to a six year high above ¥107 last week. The other currencies in the pack, the Euro, British pound, Australian dollar, Swedish krona, and Swiss franc are also looking uglier these days, but are still hanging around within their trading ranges of the past 2-years.

Many analysts and traders were caught off guard by the US$’s recent bout of strength, and as George Orwell used to say; “To see what is in front of one’s nose requires a constant struggle.” The most obvious explanation for the US$’s resiliency is the Federal Reserve’s gradual withdrawal from its Quantitative Easing (QE) scheme. Last year, the Fed pumped $1-trillion of excess US$ liquidity into the money markets, through its QE-3 scheme. However, at its Dec ’13 meeting, – the Fed switched gears, saying it would gradually reduce its injection of monetary heroin to the QE addicted markets. The Fed has reduced its QE-injections by $10-billion /month at each scheduled board meeting this year, to a pace of $25-billion in Sept ’14. The Fed is now entering the homestretch of “Tapering” QE, and will turn-off the money spigot at the end of October, and thereby removing a major headwind for the US$.

Economists are now trying to pinpoint when the Fed would begin to hike the federal funds rate from its current range of zero to 0.25%. Expectations of a series of baby-step Fed rate hikes to begin sometime in 2015, were heightened on Sept 11th, with the appointment of the Fed’s #2 chief, Stanley Fischer to oversee the central bank’s all-important “financial stability panel” – otherwise known as the “Plunge Protection Team” (PPT). Fischer’s crisis management skills will be utilized in guiding the clandestine activities of the PPT – as it tries to cushion the US T-bond and stock markets from the fallout of the Fed’s exit from QE-3. A series of baby-step rate hikes to 1% could tip the US-economy back into a recession, or worse yet, trigger a -10% correction in the US-stock market.

Even if the Fed gets cold feet and decides to delay the series of baby-step rate hikes, the US$ could still win the reverse beauty contest, because the Bank of Japan (BoJ) and the European Central Bank (ECB) are also expected to keep their lending rates locked near zero percent for years to come. Better yet for the US$, – the BoJ is on a set course to weaken the yen by injecting around ¥5-trillion per month into the Tokyo money markets, through the end of March ’15, and the ECB is preparing to print anywhere from €500-billion to €1-trillion over the next few years, under its “Targeted” QE scheme, which is designed to boost bank lending in the Euro zone economy. Thus, the US$ has the winning edge in the arena of competitive currency devaluations with its trading partners.

The Emergence of the US Petro-dollar, – Yet there’s another less cited reason behind the recent strength of the US$ index and what could auger the beginning of a multi-year advance for the greenback, – the US’s output of crude oil and natural gas continues to surge to new record highs. The US’s production of crude oil has reversed years of decline thanks to the development of shale resources, which have boosted output by +65% over the past six years. The US’s shale boom has allowed producers to unlock thousands of barrels of reserves, putting the US on course to become the largest producer of oil globally, which would dramatically reduce its dependence on imports.

US oil output averaged 8.6-million bpd in August, the highest level since July 1986. “US-crude oil production will approach 10-million barrels a day (bpd) in late 2015, and will help cut US imports of fuel next year to just 21% of domestic demand, the lowest level since 1968,” the EIA says. In Q’1 of 2014, the US passed Saudi Arabia to become the world’s largest producer of petroleum liquids, with daily output exceeding 11-million bpd, including crude oil, hydrocarbon gas liquids, and biofuels. In fact, the US would account for 91% of the 1.3-million bpd increase in global oil output next year.

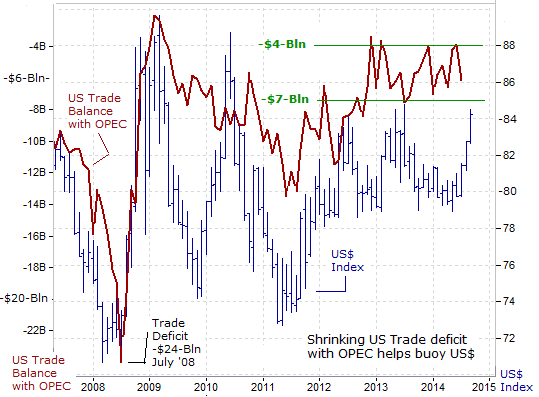

The shale revolution has enabled the US to reduce its imports of crude oil to 7.2-million bpd, or roughly -34% less from its peak in June 2005. Over the past decade, the US has reduced its imports of crude oil from Saudi Arabia, Mexico, and Venezuela, by a combined 2.9-milln bpd, while increasing imports from Canada to 2.6-million bpd. With OPEC as a whole, the US’s oil import bill has dropped dramatically, to $5.5-billion per month, on average, compared with its peak outlay of $24-billion in July 2008.

Until recently, the Saudi oil kingdom was able to maintain a steady flow of 1.3-million bpd to the US, even as total US oil imports fell by a third. However, Saudi Arabia is now losing market share as the shale boom leaves US-refiners with ample supplies of inexpensive domestic oil. Saudi exports of Arab light have fallen by 452,000 bpd since April to 878,000-bpd in August, the least since 2009.

Since hitting a record of almost 21-million bpd in 2005, US-oil demand fell to 18.5-million bpd in 2013, – the EIA says. Fuel efficiency continues to slice away at demand, and an aging population is expected to drive less in the long run. Gasoline demand had been steadily declining since 2007 as motorists drove less and car fuel efficiency improved.New US vehicles available in showrooms are +20% more fuel-efficient on average, than vehicles introduced five years ago, according to AutoNation.

The US’s shale oil revolution has helped to narrow the overall US trade deficit to -$42-billion per month, on average. That’s far less than the average deficit of -$62-billion /month from 2005 thru mid-2008, when the US trade balance was at its worst. The narrowing of the US trade deficit is adding an estimated +0.6% to the US’s annual economic growth rate, compared with a few years ago. And looking towards the future, with the growth in world energy demand expected to increase around +35% by 2030, the US-economy could find itself at close to self-sufficiency in energy.

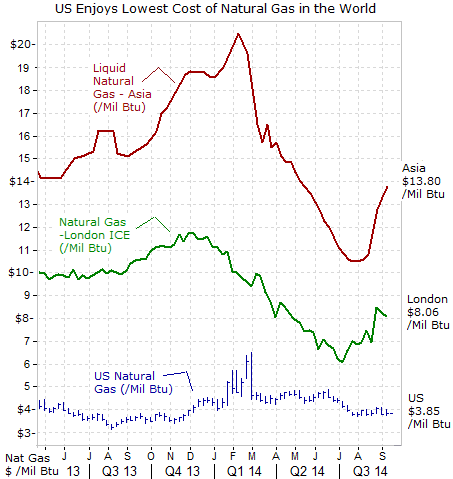

The story line for the US Petro dollar is bound to get better in the years ahead.The US has more recoverable natural gas than any other country. This represents a century’s worth of output and can support peak production at more than twice the 2013 level. As such, the EIA forecasts natural gas prices will average below $5 through 2023 and less than $6 until 2030.

A Renaissance in the factory sector – The US-economy isthe lowest-cost producer of natural gas, and thus, making products such as chemicals, fertilizer, aluminum, steel and glass are more profitable in the US, and will attract manufacturers from around the world, (or to Mexico’s side of the US-border). This creates a stronger base of economic growth than the rest of the industrialized world. Economists estimate that increases in US- oil and natural gas production will create as many as 3.6-million new US-jobs by 2020 and increase economic output by +2% to +3.3-percent.

Unlike crude oil, natural gas cannot be easily transported overseas. German and French companies pay almost three times as much for liquid natural gas, and Japanese importers pay even more. Currently, US natural gas is priced at $3.85 per million British thermal units (mmBtu), while Asian importers pay almost $14 per mmBtu for LNG imports. Europe, which relies on pipeline imports from Russia, Norway and North Africa, is priced in between at around $11 per mmBtu. Benchmark UK spot gas prices traded in London are around $8 per million Btu, while Russian pipeline supplies, which are linked to the price of North Sea Brent crude oil, are around $12/mmBtu.

Europe’s dwindling supplies of natural gas are increasing its import dependency and its exposure to a global liquefied natural gas (LNG) market where prices are high because of demand in Asia and Latin America. The cheapest pending new major gas source will be the US, which could begin exports of LNG, in 2015. But even this gas, once fees and shipping costs are added, would arrive in Europe at current spot prices of around $9-10 per mmBtu. New supplies expected from Australia, the East Mediterranean and East Africa will also be priced well above $10 per mmBtu.

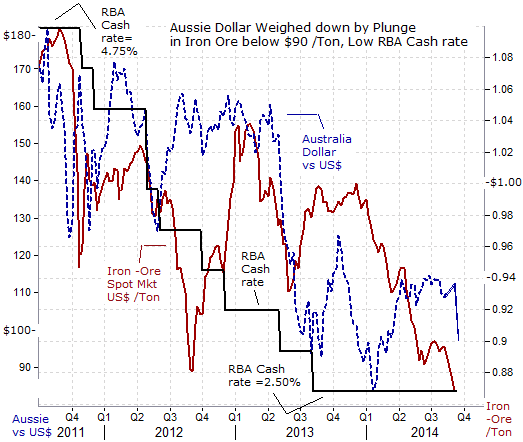

Aussie dollar Plunges alongside Meltdown of Iron ore market, – While the US-dollar is enjoying a renaissance as a “Petro” currency, – the Australian dollar finds itself on the slippery slope of a Bear market. For the week ended Sept 11th, the Aussie dollar fell -3.5%, skidding to the psychological 90-US-cent level. The price of iron ore, used to make steel, – and by far Australia’s most important export, – tumbled to five-year lows on Sept 11th, – settling around $82 per ton, and less than half its all-time high of $185 /ton. The Aussie dollar’s fortunes are influenced by gyrations in the world’s most heavily shipped mineral, which accounts for more than $1 in every $5 of Australia’s export income.

While demand from China’s steel mills continued to climb to record highs, Australia’s miners pumped billions of dollars into expanding the size of their iron ore mines and increased their export capacity, in order to capitalize on China’s high-speed urbanization. Demand for coking coal, which is used to fire the steel mills, and thermal coal used to generate electricity also played to Australia’s advantage as a large-scale coal exporter. Like all booms however, Australia’s mining bonanza has reached its zenith. China’s factory sector sputtered in August as its industrial output slowed to +6.9% in August, year -over-year, from +9% in July, – and the weakest since Dec ’08. Housing sales in China have fallen -11% in the first eight months of 2014 leaving developers burdened with bulging inventori

Softening iron ore prices, combined with the Fed’s tapering of QE-3, have weighed heavily on the Aussie dollar – the world’s fifth most actively traded currency. Ironically, it’s been Australia’s mining giants, – Rio Tinto <RIO.N> and BHP Billiton <BHP.N> that are contributing the most to the supply-side pressure that is bearing down on the price of iron ore. They are the lowest-cost iron ore miners (break-even at $45 /ton) and are flooding the market, in order to push higher-cost miners out of business. With its spending reined in, RIO has lifted annual production at its mines from 240-million tons to 290-million tons in a year. It is aiming at 360-million tons, and a supply-side squeeze is under way.

If the price of iron ore falls below $80 /ton for “an extended period,” higher-cost miners, could close down quickly. Rio, BHP and Brazil’s Vale are cash positive even if the iron ore price falls to $50 /ton. It is why they are boosting production. According to RIO, about 85-million tons of iron ore production has already been shut down in China, – where the average cost of iron-ore production is around $120 /ton. China used to source 50% of its iron ore domestically. Now it sources 20% domestically: it’s not hard to guess which miners are filling the gap. Smaller miners in Australia are on the edge at $80 /ton, if their lower-grade ore sells for less than the high-grade ore that Rio and BHP dig up.

The RBA is banking on a tighter Fed policy to weaken the Aussie dollar over the longer term, perhaps into the 85-cents to 90-cent range. In the meantime, Aussie$ traders will track the wild gyrations in iron ore, coking coal, copper, gold export prices. In the wild and whacky world of commodity trading, sentiment can often turn on a dime. For example, on Sept 15th, the spot price of iron ore suddenly jumped +4% higher to $85.20, /ton, and helped to brake the Aussie’s fall at 90-cents.

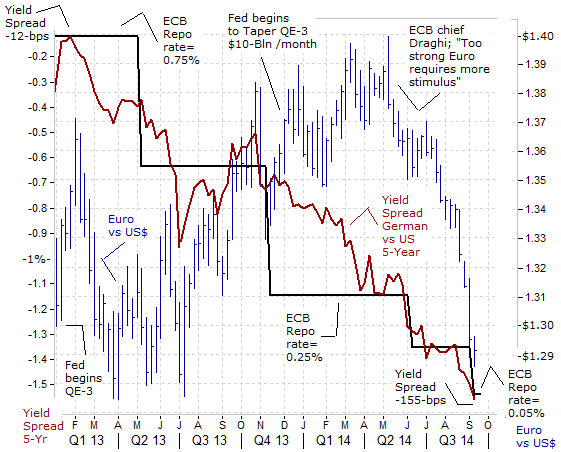

ECB knocks the Euro below psychological $1.300, While the US$ appears to be benefiting, either directly or indirectly, from its evolving status as a “Petro” currency, and psychology behind the Australian dollar has long focused on its status as a “Commodity” currency, it would be short sighted to omit that the vast majority of foreign currency transactions are earmarked for buying and selling bonds and stocks listed in the world’s capital markets. Nowadays, the movement of capital across borders happens with the click of a mouse, from a legion of traders ranging from such diverse groups, such as of lower-tier banks, carry traders, pension funds and mutual funds, hedge funds, central banks, sovereign wealth funds, and high-frequency traders, to the private retail investor.

In the foreign-exchange market, roughly $5.6-trillion changes hands each trading day, between the spot, forward, and derivatives markets. The Euro is used in 33% of these transactions, or about $1.85-trillion per day. However, the use of the Euro in the settlement of commercial transactions is just a fraction of the overall amount of trading in the common currency, compared to what’s earmarked for investment in financial markets, or what’s utilized by speculators, such as carry traders.

As such, the Euro’s exchange rate has been mostly influenced by the actions of the major central banks. For example, the Euro was climbing higher in an erratic fashion from the $1.300 area to as high as $1.400 during the 15-months ending in May ’14. The Euro was deemed to be the least ugly currency because the Fed was injecting $85-billion per month of freshly printed greenbacks into the US-money markets, and the BoJ was simultaneously injecting ¥7-trillion per month into the Tokyo money markets, under the respective QE schemes. Although the ECB was lowering its repo rate to undermine the Euro’s advance, the central bank was still resisting the nuclear option of QE.

However, that perception began to change, when in late August, ECB chief Mario Draghi suggested the ECB would start to unleash “Targeted” QE – aimed at the asset backed markets, rather than the sovereign bond markets, but with the same net results, – a massive increase in the supply of Euros. In a battered regional economy further shaken by a mini trade war with Russia, the Euro began to tumble more steeply towards $1.300, and surrendered its gains of the previous year, as the yield on France’s 2-year government notes turned negative to as low as minus -3-basis points (bps). Yields on Germany’s 2-year schatz fell to minus -7-bps, and have been below zero percent since August 25th.

In this upside-down world, lenders pay borrowers to take their money. It’s a result of the ECB’s move to impose a penalty of -20-bps on banks that park money in the central bank’s vaults. The radical move is an attempt to force banks to lend excess Euros on hand, to businesses and consumers, and end a long drought of credit in crisis countries like Greece, Italy and Portugal. However, in many cases, commercial banks, would rather lend Euros to Paris or Berlin at zero percent or less.

The ECB says it will provide as much as €1-trillion of cheap 0.15% loans to banks, on the condition that they lend the money to businesses or to individuals, – “Targeted” QE. The ECB will begin dispensing that money on Sept 18th. These loans would be bundled together into packages called “asset backed securities’ (ABS’s), and the ECB has offered to buy the ABS’s with freshly printed Euros. It’s a more intelligent way of trying to jump start an economy, rather than the QE policies in England, Japan, and the US, which are mainly designed to inflate the wealth of shareholders in the local stock markets. And targeted QE increases the supply of Euros floating in the banking system, which has the side effect of weakening the Euro’s exchange rate, in order to help boost the fortunes of exporters.

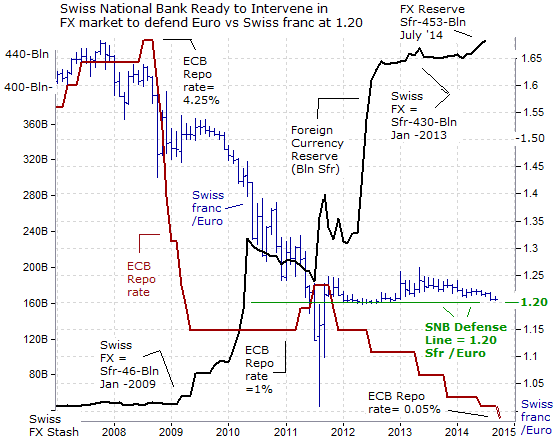

SNB says ready to act in wake of ECB easing, While the Bank of Japan, the Bank of England, and the Fed have resorted to purchasing Treasury notes, as the key mechanism of increasing liquidity in the banking system, the Swiss National Bank (SNB) has taken a different route, but producing the same results. The SNB is limited from purchasing government bonds, because the local bond market is illiquid – at just $90-billion worth. The SNB could quickly end up owning the entire Swiss government bond market if it tried to match the ECB’s printing spree. Instead, the SNB has relied upon foreign currency intervention, – printing Swiss francs in order to purchase foreign currency. Thus, the size of the SNB’s FX stash is the barometer of the scope of the central bank’s liquidity injection operations.

Since Jan ’09, the SNB’s stash of foreign currencies has mushroomed by roughly 400-billion francs, or a 10-fold increase. The SNB has enforced a floor under the Euro at 1.20- Swiss franc since Sept ’11, through a combination of verbal jawboning and outright intervention in the FX market. The SNB hasn’t been forced to intervene in the foreign currency markets for the past 2-years, as traders have shown the utmost of respect for the resolve of the SNB in defending the Euro’s floor at 1.20-francs. However, the Euro has been weakening against the franc in recent weeks, to as low as 1.205- francs. SNB chief Thomas Jordan has dropped broad hints that the bank is ready to push short-term Swiss deposit rates deeper into negative territory to make the currency less attractive. Given the sizeable amount of bank deposits held with the SNB, such a policy step could have a particularly strong impact. Negative deposit rates would make it expensive to hold Swiss francs. As a result, the US$ is looking less ugly than the Swiss franc these days, whose fate is largely tied to that of the Euro.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Global Money Trends filters important news and information into (1) bullet-point, easy to understand reports, (2) featuring “Inter-Market Technical Analysis,” with lots of charts displaying the dynamic inter-relationships between foreign currencies, commodities, interest rates, and the stock markets from a dozen key countries around the world, (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, posted Monday and Wednesday evenings, with the latest news and analysis on global markets. To order a subscription to Global Money Trends, click on the hyperlink, http://www.sirchartsalot.com/newsletters or call 561-391-8008, to order, Sunday thru Friday, 9-am to 9-pm EST.

1. Job Growth – we look for trends in job creation, type of employment, and unemployment trends

1. Job Growth – we look for trends in job creation, type of employment, and unemployment trends

2. Population Growth – we look for trends in growth, demographics, and forecasts that mitigate growth

3. Economic Growth – we look at what is driving the economy, is it diversified and economic trends

4. Healthy Real Estate Fundamentals – are we too late or early? Is the market stable with positive growth trends? Is the market affordable?

5. Business Friendly Government – understanding municipal and provincial / state attitudes towards development (taxation, levies, growth plans)

What Real Estate Markets do we like and what particular sectors in that market?

Canada

Calgary – arguably not only the best market in Canada but in the world to invest. According to the June 2013 IPD Global Cities Report puts Calgary as the leader in overall performance as to real estate returns in the world for the last 2 years.

What we like: concrete tower apartment buildings, inner city development in residential, retail and commercial.

Edmonton – Alberta continues to add over 100,000 new people a year driven by the energy sector and Edmonton as the capital and the “blue collar” side of the energy will continue to grow.

What we like: apartment buildings, medical, light industrial, and raw land development.

United States

Texas – Texas leads the nation in job growth, low unemployment, affordable, projected to double in size by 2040 (over 50 million people), low taxes, pro-business government, energy, etc.

What we like: we love the Texas Triangle (Houston, San Antonio, Dallas). We like raw land for residential and retail.

Arizona – real estate trends around the Greater Phoenix area show growth trends of 30% over the next 3 years that are still well below the peak of 2008. Phoenix is in the Top 10 of fastest growing cities in the US, Top 5 in Job Growth, and #1 in real estate recovery.

What we like: we like apartment buildings in and around the Phoenix area

Craig Burows is the President of TriView Capital, an Exempt Market Dealer specializing in private equity offerings

Michael interviewed US Health Care Reform expert Sibyl Bogardus of HUB International on the impending deadline and significant fines looming for Canadian companies, sno-birds and expats working and residing in the US. CLICK BELOW to listen to the full interview.

{mp3}grant/sibylinterview{/mp3}

And if this issue impacts you or your company – we recommend you make time to learn more when Sibyl puts on a series of seminars this month. Seminar Dates:

- Calgary – Monday, September 29th, 3-6 pm – Hotel Arts, 119 12th Avenue SW

- Edmonton – Tuesday, September 30th, 3-6 pm – Fairmont Hotel Macdonald, 10065 100th Street

- Winnipeg – Wednesday, October 1st, 3-6 pm – Manitoba Club, 194 Broadway

- Vancouver – Thursday, October 2nd, 3-6 pm – Ter minal City Club, 837 West Hastings Street

*RSVP at www.hubhcr.ca

Seminar Will Include Information Regarding:

- How US health care reform rules apply when a US company or companies have a foreign parent or owner

- Penalties for non-compliance

- Obligations, strategies and solutions for compliance

- Maintaining effective benefit plans while holding costs in check

- Creating a 3-5 year strategic plan

N.B. By attending this seminar, both Accounting and HR Professionals are eligible for 2 hours of continuing education credits

Updates and changes to US Health Care Reform can be found at:

www.hubinternational.com/employee-benefits/healthcare-reform/enewsletter/

Sibyl is a nationally recognized speaker on health care reform, medical plan design trends, state and federal laws and human resources issues. She has presented at numerous national conferences. She is a widely published author on health care reform, employee benefits, tax and labor law issues.

In December 2013, the House of Representatives invited Sibyl to testify on health reform impacts to their Small Business Committee in Washington, D.C. She currently serves on an IRS Advisory Council for the Gulf Coast.

In this week’s issue:

- Weekly Commentary

- Strategy of the Week

- Stocks That Meet The Featured Strategy

– Stockscores’ Market Minutes Video – The Importance of Abnormal Volume

– Stockscores Trader Training – Stockscores Video Party

– Stock Features of the Week – Catalysts

Stockscores Market Minutes Video – The Importance of Abnormal Volume

Beating the market requires finding stocks that are trading on their own story, these stocks are called Alpha stocks. One of the important keys to finding Alpha is a focus on stocks trading abnormal volume. This week, Tyler explains this concept before providing his regular weekly market analysis.

Click here to watch this week’s Market Minutes, The Importance of Abnormal Activity

Stockscores Trader Training – Video Party

This week I focus on videos of some of my recent webinars. Grab some popcorn and watch the videos below:

First, I take you on a tour of the tools offered at Stockscores.com. See the Market Scan, learn how to adjust chart settings and much more.

Click here to view “The Stockscores Tour”

Active trading with the Stockscores Approach can be day trading with the exit before the close or less active swing trading with stocks that are held for a few days. In this webinar, I highlight the similarities and differences between my approach to day and swing trading.

Click here to view “Day Trading vs. Swing Trading”

The Stockscores Market Scan tool and strategies are efficient and effective ways to find stocks for your investment portfolio. In this webinar, I show how this tool works and the daily and weekly processes I use to find promising stocks.

Click here to view “The Stockscores Approach to Investing”

Finally, this webinar video highlights the tools and processes used to actively trade the stock market using the Stockscores strategies. If you have ever thought about making trading a full or part time occupation, this webinar should not be missed. I show what I do each trading day to find and execute my short term trades.

Click here to watch “The Stockscores Approach to Active Trading”

When I find a stock that is trading abnormally and has a decent chart pattern, I look in to the company story to see if there are catalysts for speculation. I want to know if the company has something happening that will make people want to buy it for future news. An oil company that is drilling, a software company with a new release, a biotech company in FDA testing – these are catalysts that will make investors buy for the dream of big news in the future.

I don’t have to be around for the news because the market is very good at moving up before the news comes out, giving a good trade without the company ever proving it has the goods.

This week, I share with you two stocks that I featured to the readers of my daily newsletter last week which have good charts and catalysts for speculation:

1. V.GPH

The company says it has the largest graphite deposit in the US which could be very valuable since graphite is an important component in the kind of batteries that Tesla will produce in their new Gigafactory being constructed in Nevada. Company is doing a drilling program to prove up the resource right now. Stock traded very abnormal volume last week and has been moving higher. Support at $0.14.

2. VOXX

this maker of audio systems has invested in a competitor to GoPro’s personal camera called 360fly which will be launching their new 360 degree view camera very soon. Stock broke out of an optimistic chart pattern and has been moving higher since. Support at $9.95.

References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

The resounding story for the markets these last few weeks has been the unequivocal strength of the US dollar. The dollar closed higher Friday for the ninth straight week as it continues on its best run in 17 years. This has been the move in the dollar that many investment professionals were looking for as they anticipated the US Fed to end their Quantitative Easing program and begin to raise the Federal Funds rate, but the move in the dollar really did not come to fruition until the latter half of this year. That, however, is not the only story that has been supporting the strong dollar trade as a number of both domestic and international factors are weighing in on the foreign exchange markets.

The resounding story for the markets these last few weeks has been the unequivocal strength of the US dollar. The dollar closed higher Friday for the ninth straight week as it continues on its best run in 17 years. This has been the move in the dollar that many investment professionals were looking for as they anticipated the US Fed to end their Quantitative Easing program and begin to raise the Federal Funds rate, but the move in the dollar really did not come to fruition until the latter half of this year. That, however, is not the only story that has been supporting the strong dollar trade as a number of both domestic and international factors are weighing in on the foreign exchange markets.

The international story is based on the action of western central banks. As the US has passed their inflection point from making policy more to less accommodative, the question through the end of the summer has been what future measures will be taken by the European Central Bank and Bank of Japan? And unfortunately for the Bank of England, despite efforts by Governor Mark Carney to talk up the pound, a referendum on Scottish Independence on the 18th of this month has substantially weakened the pound translating to a stronger greenback.

On the domestic side it’s perhaps investor’s lax expectations that shifted this market. The San Francisco Fed put out a paper this week looking at how investors and futures markets were anticipating when the Fed might begin to tighten policy and at what pace versus what members of the Federal Open Market Committee (FOMC) were actually saying in their most recent June meeting. What the San Francisco Fed found was that the market and investors are behind the curve in anticipating when the Fed will begin to raise rates. This is inherent in an expectation that the accommodative policy will be around longer than the Fed currently plans on delivering.

This all leads into what will be a very important week for the markets. The FOMC meets Tuesday and Wednesday, and following that on Thursday Scotland votes. No question, volatility which has been vacant from currency markets for so long is finding its way back. Accommodative policy from the world’s most influential central bank had dampened volatility from the FX markets. As we’ve learnt, this had an effect of suppressing and stabilizing interest rates at record low levels. But as the Fed shifts back to a less discernible role in the markets, volatility in currencies will begin to rise.

The unknown going forward is what it means for the US dollar, and commodity prices, along with equities and the outlook for earnings of US companies, with a foreign income stream. The same questions holds true for most other financial markets. A stronger dollar provides headwinds and at this stage the dollar looks like it will continue to dominate.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair