Asset protection

An Austrian economist’s take on the financial markets & economy

An Austrian economist’s take on the financial markets & economy

The Federal Reserve is “normalizing” its monetary policies. QE3, the latest installment of its multi-year $3.7 billion asset purchase program is ending this month. And although its zero interest rate policy(ZIRP) is still fully in force, the Federal Reserve is signaling that as long as the economy continues to improve, interest rates are going up. Though these easy money policies are acknowledged by most investors as the driving force behind the strengthening U.S. economy and, as a derivative, the five-plus year bull run in the equity market, equity investors seem to be taking the Federal Reserve’s normalization plans in stride. So too the Federal Reserve. As we posited here, the reason is because equity investors and FOMC members alike believe the Federal Reserve’s easy money policies have worked; that they have finally put the economy on a sustainable, longer-run growth path. In fact, the economy is doing so well that it’s time to normalize monetary policy.

As we wrote here, here and here, in the end this story will prove to be pure fantasy. The lion’s share of the supposed economic strength we see today is both artificial and unsustainable because it is built on malinvestments born out of the monetary largesse underwritten by the Federal Reserve’s policies. Normalize those policies; i.e., end QE and raise interest rates, and sooner or later those malinvestments will be liquidated. The supposed economic boom will turn to economic bust, and with that, a bust in the publicly traded equities that lay claim to those malinvestments. As Austrian Business Cycle Theory (ABCT) theorists teach, such is the course of every boom-bust cycle. Easy money – whether that originates directly from the central bank or from the central bank supported, fractional reserve banking system – gooses the money supply creating an artificial, unsustainable boom. The boom will bust when that easy money abates.

…..continue reading HERE

We’ve now seen the last day for a Fed POMO.

If you’re unfamiliar with this term, it stands for Permanent Open Market Operation. This is the mechanism through which the Fed pumps money from QE into the financial system. It’s also the single most important item as far as stock market rallies are concerned.

Indeed, the stock market has closely correlated the Fed’s balance sheet expansion since 2009. As the below chart shows, they are almost identical in growth.

When QE ends today, the Fed balance sheet will stop expanding. Which means stocks will be standing on their own two legs for the first time in the last two years.

Unfortunately, those two legs: economic growth and earnings are both weak.

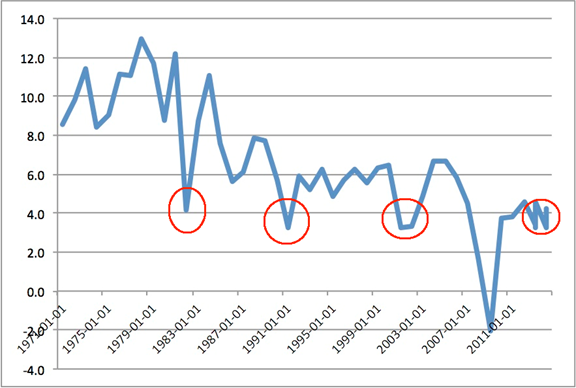

As far as economic growth goes, if you want a clear picture, you need to look at nominal GDP growth. The reason for this is that because the Fed greatly understates inflation, the official GDP numbers are horribly inaccurate.

By using nominal GDP measures, you remove the Feds’ phony deflator metric. With that in mind, consider the year over year change in nominal GDP that has occurred.

As you can see, we’ve broken below four, the reading that has been triggered at every recession in the last 30 years. At best, we’re flat-lining. At worst we’re already in recession again.

So economic growth is weak.

What about earnings?

The media is trumpeting how great earnings are… but the reality is that most of the earnings growth is coming from buybacks, NOT organic growth.

Here’s how it works. A company uses cash to buy back its shares. As a result the number of shares falls. Thus, its earnings are spread out over a small number of shares… so that Earnings Per Share is in fact much higher.

This game has been going on for some time. According to JP Morgan, roughly HALF of all earnings growth since 2011 has come from BUYBACKs, not organic growth. Indeed, in this last quarter, companies used up 95% of all earnings BUYING BACK SHARES or issuing dividends.

So earnings are not nearly as great as they appear.

So… no more QE from the Fed… a US economy teetering on the brink of recession… and earnings that are far lower than the headline numbers imply.

This is a recipe for a MAJOR market correction.

Today the Federal Open Market Committee wraps up its latest monetary policy meeting.

Today the Federal Open Market Committee wraps up its latest monetary policy meeting.

Traders are desperately searching for an answer to this question: Will the FOMC alter their interest rate language if they terminate their bond buying program?

Will they keep words that keep interest rates low for a “considerable time”?

Heavy sigh.

Every FOMC meeting comes down to these potential tweaks. The changes are subtle, and they seem innocuous. But, if I may speculate, the impact too often damages your trading account …

Surprise: The Federal Reserve doesn’t care if their comments cause you to lose money.

They want the consensus to stay tied up, confused and guessing about the future for interest rates, markets and the economy. This buys them time while they themselves guess about the impact of market forces.

It’s the same tired game. So forgive me for being indifferent.

Besides, indifference is the best way to insulate your trading account (and profit too) from FOMC word games and the market forces that confound them.

Forget About Federal Reserve Futility

Yesterday, the US durable goods report missed by a lot.

The US dollar took a hit.

Why?

Because if the US economy isn’t on solid footing, the consensus thinks Janet Yellen and the FOMC will lean dovish and keep from hiking interest rates for a “considerable time.”

Long live the liquidity champions.

The reality, of course, is that no one knows what the Fed is going to say or do with its monetary policy statement today … or when they will or won’t be hiking rates in the future.

The consensus can only guess. And hope the market won’t inflict too much pain on them if they guess wrong (which is likely). It’s an exercise in futility.

This is why I don’t trade the FOMC announcement. Rather, I trade the traders trading around the announcement.

What does that mean?

It means I don’t care what the Fed does. I only care what price action does.

Price action represents the shifting emotions of traders. I essentially profit by harnessing those emotions.

I’ve been around a long time, through many economic and market cycles, and I don’t recall a time when the bull/bear debate had such strong arguments on both sides.

The bullish case:

- The economic recovery from the Great Recession continues.

- The Fed promises to keep rates low until the economy strengthens more.

- Earnings continue to meet or beat Wall Street estimates.

- Corporations are buying back their stock, decreasing the supply.

- With interest rates so low, there’s no place for investors other than in stocks.

- Oil and energy costs are plunging, leaving consumers with more disposable income.

- The market has finally experienced the overdue 10% correction.

- Favorable seasonality has arrived.

- The S&P 500 breaking below its long-term 200-day m.a. was a false alarm.

The bearish case:

- The recovery remains as anemic as it has been for the last five years. The Fed is ending QE stimulus on which the economy has been dependent. Every time the Fed let QE stimulus expire, the market and economy stumbled until they re-instated it.

- The economies of America’s largest global trading partners are in trouble. The 18-nation euro-zone is potentially even sliding back into recession. Global slowdowns will drag the U.S. economy down.

- That earnings are beating Wall Street’s estimates is only a measure of Wall Street’s ability to obtain guidance from companies. Actual earnings growth is slowing.

- That corporations are using their cash to buy back their stock, artificially manipulating the P/E ratio, rather than investing in growth, is not a positive for the economy. It’s an activity usually seen near the end of bull markets.

- The U.S. stock market is at high valuation levels even for times when the economy was already super strong and growing.

- On the 200-day m.a. being a false alarm, not so far on the broad NYSE Composite.

- After four straight down weeks, the market rallied back this week. So far, the rally looks as much like a normal brief bounce-back from an oversold condition beneath key moving averages, as the beginning of a new leg up.

- Investor sentiment has already spiked back up to levels of bullishness usually seen at market and rally tops. This week’s AAII poll showed the bullish percentage jumped to 49.7%, while the bearish percentage plunged to 22.5%. By the time a correction ends, fear has usually taken over, with bulls under 20% and bears over 50%, just the opposite of this week’s readings. For instance, in early September, just before the mid-September market peak, bulls were at 51.9%, bears at 19.2%.

- Meanwhile, in the midst of investor optimism this week, bellwether companies in important economic sectors released disappointing 3rd quarter financial reports and warnings, the likes of American Express, IBM, Samsung Electronics, Walmart, Family Dollar Stores, Coca-Cola, McDonald’s, eBay, Netflix, Amazon.

Strong arguments on both sides.

Unfortunately, at this point the charts do not settle the debate for either side.

My technical indicators have improved, but have not yet issued an all-clear signal, suggesting this still may be just a deserved bounce, after an unusual four straight down weeks that had the market short-term oversold, but may not be the end of the correction.

The answer one way or the other should not be many days away.

Related:

Rick Santelli: When the Music Is Playing, You Have to Get Up and Dance

Get used to the headlines like the one below. You’re going to hear hundreds of US multinational companies blame their profit shortfalls on the strong dollar.

Revenue Miss #1: Lockheed Martin rose sharply after reporting better-than-expected quarterly profits. However, their $11.11 billion of sales for the quarter missed the $11.28 billion forecast and was a 2% year-over-year decline from Q3 2013.

Revenue Miss #2: eBay earned one penny more than expected, but its revenues of $4.35 billion missed expectations for $4.37 billion.

Revenue Miss #3: SanDisk reported better-than-expected profits, but its revenue of $1.75 billion was a little short of the $1.76 billion forecast. More importantly, SanDisk told Wall Street to lower its Q4 revenue expectation to between $1.8 billion to $1.85 billion, below estimates of $1.88 billion.

Revenue Miss #4: IBM, which I lambasted a couple weeks ago, delivered $22.4 billion of sales, a pathetic 3% year- over-year decline and below the $23.37 billion consensus forecast.

Revenue Miss #5: Wall Street liked a better-than-expected profit report from General Motors. GM beat profit expectation by two cents, but revenues did not fare as well; GM had $39.3 billion of quarterly revenues, but Wall Street analysts had forecasted sales of $39.5 billion.

Revenue Miss #6: Coca-Cola, the world’s largest beverage maker, said that net income for its Q3 ended September 26 was $2.1 billion, or 48 cents a share—down from $2.4 billion, or 54 cents a share, a year earlier.

Coca-Cola reported quarterly revenue of $12 billion, a flat performance from the previous quarter. Year to date, the company’s reported revenue is down 1.9% from 2013.

COKE also expects fluctuations in foreign currency exchange rates to have an unfavorable impact on its 2015 results.

Those currency losses are tucked away in the “Other Income (loss)” line of the income statement. The currency effect on operating income will equal 7% in the fourth quarter, and 6% for the full year.

COKE estimates that the strong dollar will reduce its profits by 6% over the next year!

And to make sure that COKE paints itself in the best possible light going forward, it will start using “profit before tax” rather than “operating income” as a primary metric to track profitability.

I could go on, but I think the above examples show there’s a lot of financial engineering going on behind the scenes to meet profit expectations. A serious underlying revenue slowdown is running through corporate America.

The common theme for all these revenue-challenged companies is a heavy dose of foreign sales. Those foreign sales are being negatively affected by a strong US dollar.

The US dollar has been on fire, but instead of helping corporate America, it hurts US multinational companies in two painful ways:

Top Line Pain: A strong dollar raises prices for foreign customers and those higher prices can negatively affect demand.

Bottom Line Pain: The value of overseas sales declines when translated back into US dollars.

The result is a double-whammy of profit pressure. How much of a whammy? Experts say a 1% move in the dollar can have a 2% impact on the earnings of the S&P 500 companies.

When I connect the dots, I see an explosion in the number of companies that will soon report worse-than-expected results, which they will blame on the strong dollar.

You’d be wise to take a close look at the stocks in your portfolio and jettison any that look vulnerable.

Better yet, if you have some speculative capital, there are big profits to be made by betting against—through short sales, inverse ETFs, and/or put options—those ticking time bombs.

30-year market expert Tony Sagami leads the Yield Shark and Rational Bear advisories at Mauldin Economics. To learn more about Yield Shark and how it helps you maximize dividend income, click here. To learn more about Rational Bear and how you can use it to benefit from falling stocks and sectors, click here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair