We’ve now seen the last day for a Fed POMO.

If you’re unfamiliar with this term, it stands for Permanent Open Market Operation. This is the mechanism through which the Fed pumps money from QE into the financial system. It’s also the single most important item as far as stock market rallies are concerned.

Indeed, the stock market has closely correlated the Fed’s balance sheet expansion since 2009. As the below chart shows, they are almost identical in growth.

When QE ends today, the Fed balance sheet will stop expanding. Which means stocks will be standing on their own two legs for the first time in the last two years.

Unfortunately, those two legs: economic growth and earnings are both weak.

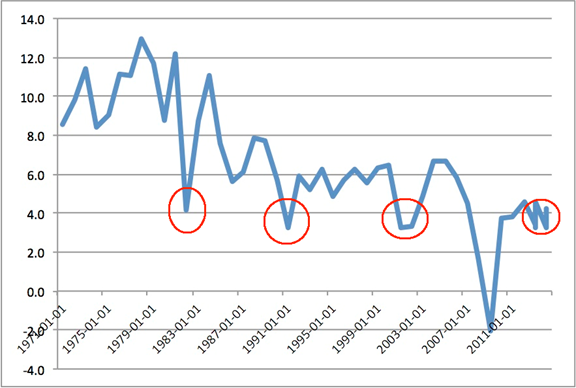

As far as economic growth goes, if you want a clear picture, you need to look at nominal GDP growth. The reason for this is that because the Fed greatly understates inflation, the official GDP numbers are horribly inaccurate.

By using nominal GDP measures, you remove the Feds’ phony deflator metric. With that in mind, consider the year over year change in nominal GDP that has occurred.

As you can see, we’ve broken below four, the reading that has been triggered at every recession in the last 30 years. At best, we’re flat-lining. At worst we’re already in recession again.

So economic growth is weak.

What about earnings?

The media is trumpeting how great earnings are… but the reality is that most of the earnings growth is coming from buybacks, NOT organic growth.

Here’s how it works. A company uses cash to buy back its shares. As a result the number of shares falls. Thus, its earnings are spread out over a small number of shares… so that Earnings Per Share is in fact much higher.

This game has been going on for some time. According to JP Morgan, roughly HALF of all earnings growth since 2011 has come from BUYBACKs, not organic growth. Indeed, in this last quarter, companies used up 95% of all earnings BUYING BACK SHARES or issuing dividends.

So earnings are not nearly as great as they appear.

So… no more QE from the Fed… a US economy teetering on the brink of recession… and earnings that are far lower than the headline numbers imply.

This is a recipe for a MAJOR market correction.