Personal Finance

“I’m no genius. I’m smart in spots – but I stay around those spots.”

“I’m no genius. I’m smart in spots – but I stay around those spots.”

Tom Watson Sr., Founder of IBM

“What an investor needs is the ability to correctly evaluate selected businesses. Note that word ‘selected’: You don’t have to be an expert on every company, or even many. You only have to be able to evaluate companies within your circle of competence. The size of that circle is not very important; knowing its boundaries, however, is vital.”

– Warren Buffett (Trades, Portfolio) 1996 Letter to Shareholders

In the world of value investing, one of the most important concepts is the concept of “Circle of Competence,” which came from and has been used over the years by Warren Buffett(Trades, Portfolio) as a way to focus investors on only operating in areas they know the best. In one of my previous articles, I wrote that, by understanding the business, Buffett means understanding the business model, not necessarily the products or services provided by the business. You can drink Coca-Cola (KO) every day yet not have the faintest idea why it is such a great business. On the other hand, you may have no idea of Valeant’s pipeline of drugs, but you can understand the business model without understanding most of its drugs.

There are a lot of discussion points on this important topic of “Circle of Competence.” In this article, I want to discuss what I call the “Circle of Competence Trap,” and especially three sectors that investors are especially subject to this trap. These three sectors are retails, energy and metals. I intentionally exclude the technology sector because it is well known that value investors tend to shun this sector anyway.

Let’s talk about the retail sector first. When I first started investing, I naively thought retail was one of the most understandable business because it is so closely related to our daily lives be it general retailers or specialty retailers. They are everywhere in our lives. Because I could see and visit those retailers in person, I assumed that I could understand how they make money and observe the trend in the retail business. Boy, was I wrong. It didn’t take that many mistakes and observations for me to realize that retail is one of the toughest businesses out there and as value investors, we have to be very careful with this sector. Look at what happened to Borders, JC Penney (JCP), Aeropostale (ARO) and Tesco (TSCO). Borders and JC Penney were high-profile mistakes made by Bill Ackman (Trades, Portfolio), who has a fabulous batting average and Tesco was a mistake made by great Warren Buffett (Trades, Portfolio). Let’s not forget about Buffett’s early investment in this department store called Hochschild, Kohn and Co. The reality is, the business model of retailing is inherently tough. It is a challenging business because shopping habits and sales channels are constantly changing, making it difficult for businesses to build and maintain competitive advantages. Moreover, your competitors can copy your best practices in no time, making it even harder for everybody to compete in this business. Some retailers are also subject to rapid technology changes, which make their business models deteriorate very rapidly (RadioShack [RSH], Borders etc.). It is just very tough to assess the business model in the next 5-10 years in retail.

Energy and metals are another two sectors where many value investors claim false “Circle of Competence.” If you ask a typical analyst what the business model of an energy E&P company is, he or she will probably tell you that you make all these capital investments in machines and equipment so you can drill oil or gas wells, then you extract them out of the ground and sell them to somebody else, hopefully at a price that not only covers your extraction and development cost but also makes you nice little profit. Similarly, for metal miners, they invest in the mines, extract the metals and sell them to someone else. Of course there are many other sub-industries in this sector such as oilfield services, offshore drillers, steel mills, etc. But if you ask me what is the most important factor that affects almost all businesses in this sector, I would say it is the price of the commodity, be it the price of oil or gas or gold, the future price of which I would argue very few of us can forecast with a reasonable amount of confidence. I was looking at some onshore rig services companies recently and stumbled onto the 2001 and 2002 annual report of this one company. I was shocked to find out that, at one time during that period, oil was below $20 a barrel. That was merely 12-13 years ago and just recently, many people were freaking out because oil dipped below $80 a barrel. Incidentally, during the same period, gold was trading below $300 per ounce, which is about one-fourth of where it is today and one-sixth of what it was two years ago. If we were in the middle of 2002, instead of 2014, could any of us imagine the price of oil and gold would quadruple within the next 12 years? I doubt many of us could. And if we couldn’t, we should think twice if we think energy and metal businesses are within our “Circle of Competence.”

In the end, I want to clarify that I am not discouraging the readers. My intention is barely to remind us that these three sectors are very tough for us to come up with reasonable forecast on what is going to happen to the business in the next 5 to 10 years. Therefore, we should be more careful if we claim these businesses within our “Circle of Competence.” Although it might seem obvious that investors should stick to what they know, the temptation to step outside one’s circle of competence can be strong. By reminding ourselves of the perils in investing in retail, energy and metals, we are better guarded against the folly that may come from an incomplete understanding of the business model.

….related:

- Seth Klarman Buys Big Stakes in 3 Companies by Holly LaFon

- A Complete List of Books Written By the Gurus by Sheila Dang

- Multiple and Customizable Investment Checklist: New and Much Improved Feature by GuruFocus

Perspective

At 89.4, the US consumer has clocked the biggest number since July 2007. The cyclical low was 55 set in November 2009.

On the other side, commodity or producer prices remain weak. Over time this will feed pricing pressures into commerce and industry. This impairs cash flow and makes it difficult to service debt.

More specifically, Deutsche Bank calculates that if crude drops to $60 some 30 percent of B and CCC bonds would default.

Charts showing the decline in Iron Ore Prices and South African Coal Prices follow. Since the summer both have taken out key lows, extending the downtrend that started in 2011.

Last week we reviewed that the business cycle turns with commodity prices, which has been the case for a couple of thousand years anyway. Included were charts of crude oil and producer prices.

Throughout business history rising prices have indicated prosperity and falling prices have indicated hard times. Our era of chronic and deliberate inflation has obscured this.

For too many decades the policymakers and too many Wall Street pundits really believed that rising oil prices were a tax on the system and too high would force a recession. Then of course, low gasoline prices, such as now, will prompt a recovery.

There is scholarly evidence that the 3 to 5-year business cycle prevailed as far back as the 1500s. Crude oil was not a commercial product then.

In any century falling commodity prices signaled a contraction.

Gasoline prices fell from the peak of 3.29 in June 2008 to 0.96 (no typo) in that December. The plunge did not prevent the contraction but was part of it.

It is worth repeating that the consumer is the most ebullient and carefree since 2007.

Stock Markets

Stock markets are enjoying ebullience as well, which has pushed the AAII Sentiment up to 57.9 Percent Bulls. The following chart shows that it can get higher in the early stages of a bull market. It also shows that at a potential peak this is the highest reading since 2000.

For the senior indexes the decline was a “correction” and for such as the Small Caps (RUT) and the STOXX it was a hit. As with October 2013, the S&P recorded a Springboard Buy. Last year’s target was a rally to around February. This year’s correction was greater and the rebound has been outstanding. Perhaps even impetuous. The S&P has been above its 5-Day ma for 20 trading days without a break. This has happened only three times in the past twenty years.

Of interest is that the “big” market, the NYSE comp (NYA) has not made it to new highs. It is working on a big test.

Last year’s “Rotation” theme worked well and seasonal forces seem to be setting up another opportunity. We have been looking for a low for copper in November. So far the low has been 2.96 earlier in the month with some stability last week at 2.98. However, rally attempts since September have been turned back by the 50-Day ma. So it has to get through that.

Base metal miners (SPTMN) declined from 954 reached on the last “Rotation” to 654 on Monday. The latest decline was sharp, driving the Weekly RSI down to 25. This seems oversold enough to pop a brief rally.

The Oil Patch (XLE) set a magnificent high at 101 in June and slumped to 77 in the middle of October. The Weekly RSI got down to 30, which was big change from the overbought at RSI 83. The rebound made it to 89 a couple of weeks ago. This was turned back by the 50-Day ma and the index has slumped to 84.

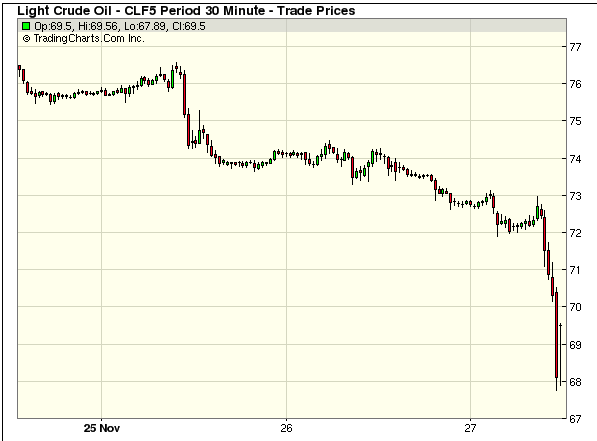

Crude oil was likely to set an important low in December. Oil stocks still seem vulnerable.

Bank stocks (BKX) could become interesting. The action is describing a big rounded top with highs at 73.90 in March and at 74.49 in early September. Since late 2012 the “dips” found support at the 50-Week ma. That ended in October when the slide from 74.49 to 65 took out the 50-Day. The 12 percent hit was tied to a sharp turn in the yield curve to steepening and credit spreads to widening.

The curve bounced and is testing the highs with quite a swing in momentum. Another run at steepening seems likely. As reviewed below, spreads have continued to widen. The alert on the banks would be the BKX taking out the 50-Day. This is at 71.25 and the index is at 72.50.

Since the beginning of the month, the spread from BBB to treasuries has widened from 167 bps to 179 bps. This is becoming impressive.

Our overall theme has been some distinctive action from Exuberance (back again) to Divergence (late summer) to Volatility (September, October and into this month). The remaining phase “Resolution” has yet to complete.

Credit Markets

We keep looking back to the extraordinary spike up in the bond future. The instruction was that at the opening on October 14th there was no liquidity and the price shot up 5 points in an instant.

Weird, but perhaps an indication of what might happen when the world loses confidence in the arbitrary aspirations of central bankers. The October event was up, which implies there could be a down event.

The US bond future needs to test the high at 147.75. It is at 141.25 now.

On JNK, the big overbought was set at 41.81 in June and the decline to the 39 level in mid-October was severe enough to register a Springboard Buy. The bounce to 40.56 was fast enough to register the opposite signal.

JNK has been following the 50-Day average down, but this week the decline steepened. Taking out the 39 level would be an important step on the way to credit dislocation.

This shows clearly in the following chart on spreads (mentioned above). This week we have added the chart of spreads on the key reversal in 2007.

Over in Europe, this week the Russian bond yield broke to new highs at 10.42%. The previous high was 10.29% set earlier in the month. In May 2013 the yield declined to 6.46%.

The Spanish yield declined to 5.56% in early in September. With somewhat of a local panic it jumped to 8.88% on October 16. The subsequent low was 7.20% and it has methodically increased to 8.32%.

Other country yields are no longer declining and are building a bottom.

Commodities

Agriculturals (GKX) became very oversold at the end of September. Enough to suggest a sector that could rally. The low was 290 and with some stair-steps the index made it to 327 last week. Corrections have found support at the 50-Day which is at 308 and gently turning up.

Base metals and energy items were covered above, but merit additional comment.

Copper seems to be working on a double bottom. One low was at 2.96 in the turmoil of mid-October with the other at 2.97 on November 4th. Getting above the 50-Day would be constructive.

Crude oil’s plunge has driven the Weekly RSI down to 18.5, which is very oversold. A brief rally is possible. But we remain concerned about a “political failure” similar to the one from late 1985 to early 1986. That failure bankrupted the Soviet Union and this time around it would be very constructive to bankrupt the Neo-Soviet Union as well as terrorist movements in the Middle East.

Precious Metals

Will this sector become “precious” again?

Under the old paradigm of what happens in a post-bubble contraction – Yes!

Gold’s real price, as tracked by our Gold/Commodities Index, completed a cyclical bear in June and has set a cyclical bull market. Threats to the stocks would be diminishing liquidity in the big stock market and the even bigger credit markets. Going back a few years, the other threat was that in bull markets for orthodox investments, precious metals under-perform or head down.

Our November 6th Pivot noted that the bottom in the sector would be determined by gold shares starting to outperform the bullion price.

The plunge in HUI/Gold was the worst since the crash into late 2000. The numbers say it was more severe. In 2000, the ratio fell to .133 with the Weekly RSI down to 24. This time around, it plunged to .124 (November 4th) with the RSI down to 19.5.

Quite likely this took out the last of the “inflationists” playing the “hate-the-Fed” game that started very quietly in the mid-1960s. It became exceedingly popular in 2011.

HUI/Gold rallied to .141 and tested the low at .130 last week. The rise since has been very constructive and getting though the 50-Day at .152 would set the uptrend.

We think that crude oil is a reasonable proxy for the cost of energy when mining. Gold/Crude set its bottom at 11.71 in June and with a couple of corrections has made it to 16.20.

It seems that what was needed to determine the cyclical bottom for the precious metals has been accomplished. Gold shares could become outstanding performers and one should buy the dips. The main setbacks to golds will be liquidity concerns in the orthodox markets.

*****

Roy Spencer has an interesting blog on the snow storm that hit Buffalo, N.Y.:

Link to November 22nd Bob Hoye interview on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2014/11/central-banks-admit-their-actions-are-reckless/

….if the referendum passes next Monday doubling prices.

….if the referendum passes next Monday doubling prices.

“Switzerland was the last country in the world to leave the gold standard in 1999 and may be the first to take a major step to becoming a gold-backed currency next week.”

The Swiss National Bank would be forced to buy the equivalent of around 70 per cent of total global gold production for the next three years if the referendum being held in Switzerland next Monday is passed. Gold prices could easily double within a matter of weeks.

Recent polls have suggested an early surge in the ‘yes’ vote to 42 per cent has declined in recent days. But the large number of voters declaring themselves undecided will make the result on Monday a cliffhanger for gold and silver investors.

Gold standard

Switzerland was the last country in the world to leave the gold standard in 1999 and may be the first to take a major step to becoming a gold-backed currency next week. Many Swiss citizens are scared by the rise of paper money and money printing around the world and now regret having ditched the gold standard.

Experts say that if the Swiss vote ‘yes’ on Monday, the SNB will have to buy 1,500 tonnes of gold over the next five years, the equivalent of almost 70 per cent of the annual global output from gold mines.

Five million Swiss citizens are able to vote on a proposal that would force the central bank to triple its gold reserves from seven to 20 per cent of total foreign currency reserves. The vote is being keenly observed by financial markets and governments all over the world.

Under the ‘Save Our Swiss Gold’ initiative the SNB will have to hold at least a fifth of its assets in gold within five years. The bank will also be required to repatriate all Swiss gold held abroad and be banned from selling any of its holdings in future. A fifth of Switzerland’s 1,040 tonnes of gold reserves are in the vaults of The Bank of England while a third are deposited in the Canadian Central Bank.

Gold-backed Swisse

Opponents see this as fatally tying the hands of the SNB. The Swiss franc is already at a two-year high thanks to the referendum. The SNB has been forced to track the euro lower in recent years to avoid making Swiss industry hopelessly uncompetitive against the eurozone countries. This will be far more difficult to achieve with a gold-backed Swisse.

Still securing the position of the Swiss franc buy buying gold is far from being as mad as trying to do so by printing paper money as other central banks around the world are doing with their currencies. Somebody has to be the first to move towards sound money.

If Everything Is Just Fine, Why Are So Many Really Smart People Forecasting Economic Disaster?

Could they be wrong?

It’s certainly possible.

But I wouldn’t bet against them.

….read more HERE

The Vienna meeting is the most crucial since the financial crisis, with the price of oil having slumped by more than 30 per cent since mid-June.

….continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair