Asset protection

This week’s Outside the Box continues with a theme that I and my colleague Worth Wray have been hammering on for some time: the very real potential for a rising dollar to trigger the next global financial crisis.

We are concerned about the consequences of multi-speed economic growth around the world and the growing divergence between major central banks. In our opinion, if these trends persist, they likely mean (1) a major US dollar rally, (2) a rapid unwind of QE-induced capital flows to emerging markets, (3) a hard slide in fragile emerging-market and commodity-exporter currencies, and (4) financial shocks capable of ushering in a new global financial crisis.

Alongside true macro legends like Kyle Bass, Raoul Pal, Luigi Buttiglione, and Raghuram Rajan, Worth and I have written about this theme extensively in 2014 (“Central Banker Throwdown,” “Every Central Bank for Itself,” “The Cost of Code Red,” “Sea Change,” “A Scary Story for Emerging Markets”). Now it’s quickly becoming a mainstream macro theme on almost everyone’s radar. Virtually every economist and investment strategist on Wall Street has a view on the US dollar and the QE-induced carry trade into emerging markets… and anyone who doesn’t should start looking for a different job.

Policy divergence is really the only macro theme that matters right now. And on that note, the Bank for International Settlements just released its predictably must-read quarterly review, with an urgent warning:

The appreciation of the dollar against the backdrop of divergent monetary policies may, if persistent, have a profound impact on EMEs [emerging-market economies]. For example, it may expose financial vulnerabilities as many firms in emerging markets have large US dollar-denominated liabilities. A continued depreciation of the domestic currency against the dollar could reduce the credit worthiness of many firms, potentially inducing a tightening of financial conditions.

Echoing those comments on Twitter, the “bank for central banks” reiterated how this trend affects all of us (feel free to follow us at @JohnFMauldin and @WorthWray):

@BIS_org: US dollar as global unit of account in debt contracts means a stronger dollar constitutes tightening of global financial conditions.

This is in spite of continued efforts by central banks to ease monetary conditions. Calling attention to that very risk in our Halloween edition of Thoughts from the Frontline, Worth explained that the catalysts are already in position to spark a collapse in a number of fragile emerging markets if the dollar moves even modestly higher (into the low 90s on the DXY Index); but we have struggled to quantify the actual size of the nebulous USD-backed carry trade that could now come unwound at any moment.

Reasonable estimates range from $2 trillion to $5 trillion. The true number could be even larger if more speculative money has slipped through the cracks than has been officially reported in places like China; or it could be smaller if a significant portion of recent inflows represents a more permanent deepening of emerging-market financial systems rather than an attempt to escape financial repression in the developed world. It’s hard to know for sure, and that’s why this week’s Outside the Box is so important.

In a recent presentation at the Brookings Institution, BIS Head of Research and Princeton University Professor Hyun Song Shin shared his research revealing that dollar-denominated credit to non-bank offshore borrowers is now more than $9 TRILLION and at serious risk in the event of continued policy divergence.

I’d encourage you to listen to or download an audio recording of Dr. Shin’s presentation, and take some time to flip through his slides; but David Wessel’s cogent summary, which follows in today’s Outside the Box, will give you an idea of what may happen as the US dollar rallies. It’s short, sweet, and REQUIRED READING for anyone who wants to understand where the global financial system is heading in the coming quarters.

Then we wrap up with an essay on the same theme by my friend Mohamed El-Erian, who is typically not as strident in his wording; but for those of us who know Mohamed, this is the equivalent of him pounding the table:

Avoiding the disruptive potential of divergence is not a question of policy design; there is already broad, albeit not universal, agreement among economists about the measures that are needed at the national, regional, and global levels. Rather, it a question of implementation – and getting that right requires significant and sustained political will.

The pressure on policymakers to address the risks of divergence will increase next year. The consequences of inaction will extend well beyond 2015.

For readers interested in this theme, let me also offer a link to some on-the-record remarks from Claudio Borio, the head of the Monetary and Economic Department at the BIS, and Dr. Shin, preceding the release of the BIS quarterly report. For a representative of such a staid and sober organization, Mr. Borio uses a lot of rather disconcerting terms. He is clearly very concerned. Again, you can read the full BIS quarterly review here.

I’ve spent some time this week working with Jack Rivkin and our respective teams at Altegris and Mauldin Economics, putting together the lineup for our 2015 Strategic Investment Conference. I think it will be our best conference ever. You should definitely save the dates April 29 through May 2, as this will be a can’t-miss conference. We will get you more details soon.

I trust your week is going well. We are planning for the holidays and looking forward to some great family time. We’ll see if a new grandchild shows up in time for Christmas or decides to become a New Year’s baby.

Your thinking about 2015 analyst,

John Mauldin, Editor

Outside the Boxsubscribers@mauldineconomics.com

How the Rising Dollar Could Trigger the Next Global Financial Crisis

By David Wessel

Wall Street Journal, Dec. 7, 2014

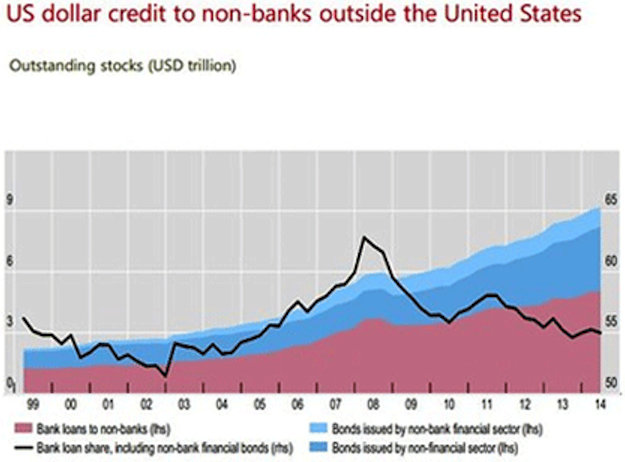

A slide from Hyun Song Shin’s presentation to the Brookings Institution on financial stability risks shows the Bank for International Settlement’s analysis of dollar lending to non-banks outside of the United States.

Bank for International Settlements

Hyun Song Shin, who is on leave from Princeton while chief economist at the Bank for International Settlements in Basel, spends a lot of time wondering what could cause the next financial crisis. He suspects it will be something different from the leveraged bets on housing that were at the root of the last crisis.

So, what might it be? Perhaps the steady rise of the U.S. dollar on global currency markets.

In recent presentations at the Brookings Institution, Mr. Shin documented the growing use of the U.S. dollar by borrowers and lenders outside of this country. U.S. banks and bond investors have lent $2.3 trillion outside the U.S. Foreign banks and foreign bond investors have lent much more: $6.5 trillion.

(Mr. Shin and colleagues at the Bank for International Settlements elaborated on his latest analysis in the bank’s new Quarterly Review posted Sunday.)

Here’s how Mr. Shin sees the world: A manufacturer in an emerging market borrows in dollars, perhaps because it sells a lot of goods in dollars and sees borrowing in dollars as a hedge. A local bank lends the dollars, borrowing from some big global bank. When the emerging-market currency is strong and the dollar is weak, that manufacturer’s balance sheet looks sturdier–and the local bank sees that and lends more readily. Thus a weak dollar can lead to a global credit boom.

When the dollar rises, though, all this runs in reverse, effectively tightening global financial conditions, particularly in emerging markets. The emerging-market currency falls. The manufacturer has trouble making payments on its dollar loans; so do its peers. Banks lend less readily. Capital investment stalls. Global money managers–the ones with lots of short-term wholesale deposits that search the world for the best yields–see a falling local currency and a weakening economy and pull money from the emerging-market banks.

Then, global asset managers who had been lured by a high-growth story see that it is now over and do the same thing, selling emerging-market corporate bonds. That pushes up interest rates that businesses in emerging markets have to pay, and weakens them further in a vicious cycle.

“Even if you have long-term investors and you don’t have [leveraged investors], if events in the financial markets translate into events in the real economy, you can get a feedback loop,” Mr. Shin says. And this, he adds, is a very different mechanism than the insolvency of highly leveraged financial institutions that was at the heart of the recent global financial crisis.

All this is a timely reminder that all the important steps taken to strengthen the foundations of the world’s banks in response to the last crisis aren’t a cause for complacency.

David Wessel is director of the Brookings Institution’s Hutchins Center on Fiscal & Monetary Policy and a contributing correspondent to The Wall Street Journal. He is on Twitter: @davidmwessel.

An investor’s first instinct is to prefer successful companies. The boss is revered, the stock is a rocket. General Electric was, in Jack Welch’s heyday, a prime example.

An investor’s first instinct is to prefer successful companies. The boss is revered, the stock is a rocket. General Electric was, in Jack Welch’s heyday, a prime example.

I have a contrary strategy: Buy shares of crappy companies. Look for a business whose stock has gone nowhere and whose corner office is covered with a thick layer of dust.

If you buy cheaply and patiently, you could get a nice windfall via a takeover. Even without such a rescue you could see a decent return. Perhaps the third-rate management gets replaced with second-rate management.

Canadian Pacific was a mediocre railroad when a fund run by William Ackman acquired a position. Ackman is a hands-on investor–perhaps we should say, hands-on-throat. He got the chief executive axed. In the three years since Ackman started making a stink, the stock has tripled.

I have a little list of companies that could benefit from some cage-rattling. Over the past decade their stocks have, according to Morningstar’s calculation of total return, lagged both the market and the average for industry peers. They have underexploited assets and complacent managers.

SCHOLASTIC (SCHL, 35) has a commanding presence in publishing for young readers, both in and out of schoolrooms. When you look at its bottom line, though, what you see is what could have been. As publisher of the Harry Potter and Hunger Games novels, it could have had a nice piece of the movies. Somehow those opportunities slipped between its fingers. Instead it sank money into a movie based on another children’s fantasy series. The Golden Compass came out in 2007, and we’re still waiting for the sequel.

Scholastic Chief Executive Richard Robinson has been with the company (which his father founded) since 1962. He has a good grip on his job, what with supervoting shares that give Robinson heirs control of the board. But maybe his relatives, or an outside investor, could persuade him that everyone would be enriched if he moved on.

TOOTSIE ROLL INDUSTRIES (TR, 29) is sitting on valuable candy brands, including Junior Mints and Charms. For the past half-century Melvin Gordon has been firmly in control. Someone might delicately suggest that it’s not too soon for him to retire (age in last proxy: 94).

….continue reading stocks 3-6 HERE

Today’s videos:

Silver Volume Bar Of Respect Charts Analysis

Gold Downtrend Breakout Charts Analysis

US Dollar Fib Line In The Sand Charts Analysis

GDX Two Day Close Charts Analysis

GDXJ Two Day Close Charts Analysis

Thanks,

Morris

Friday, Dec 12, 2014 Super Force Signals special offer for 321Gold Readers:

Send an email to trading@superforcesignals.com and I’ll send you 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you!

The SuperForce Proprietary SURGE index SIGNALS:

25 Surge Index Buy or 25 Surge Index Sell: Solid Power.

50 Surge Index Buy or 50 Surge Index Sell: Stronger Power.

75 Surge Index Buy or 75 Surge Index Sell: Maximum Power.

100 Surge Index Buy or 100 Surge Index Sell: “Over The Top” Power.

Stay alert for our surge signals, sent by email to subscribers, for both the daily charts on Super Force Signals at www.superforcesignals.com and for the 60 minute charts at www.superforce60.com

About Super Force Signals:

Our Surge Index Signals are created thru our proprietary blend of the highest quality technical analysis and many years of successful business building. We are two business owners with excellent synergy. We understand risk and reward. Our subscribers are generally successfully business owners, people like yourself with speculative funds, looking for serious management of your risk and reward in the market.

Frank Johnson: Executive Editor, Macro Risk Manager.

Morris Hubbartt: Chief Market Analyst, Trading Risk Specialist.

website: www.superforcesignals.com

email: trading@superforcesignals.com

email: trading@superforce60.com

SFS Web Services

1170 Bay Street, Suite #143

Toronto, Ontario, M5S 2B4

Canada

###

Dec 12, 2014

Morris Hubbartt

Silver’s Investment & Industrial Demand Colliding with Problematic Supply

Investors in future decades will look back on this period’s history and marvel at some extraordinary events. They will remark on parabolic debt charts and King Dollar’s dethroning. And they will see the great opportunities, unnoticed and passed over by most, as obvious in hindsight. Silver may well be one of these great opportunities.

Gold prices stand to benefit from a worldwiden exodus from fiat currency and paper assets. Demand for platinum and palladium mirrors growth in manufacturing around the world – particularly in developing economies. But silver is uniquely positioned to benefit from both of these macro trends… in spades.

Profligate governments, central banks, and various crises are fueling safe-haven investment demand for silver coins, rounds, and bars from people around the globe.

While there is lots of coverage of events driving investment demand, readers may not be as familiar with developments relating to the industrial use of silver. Silver enjoyed steady demand growth as worldwide manufacturing boomed leading up to the 2008 financial crisis. Silver prices fell when manufacturing powerhouse economies including the U.S., Japan, and Europe slumped.

Going forward, silver’s industrial demand is likely to fare better than manufacturing generally. The metal is widely used in faster growing sectors such as electronics and solar power. Most of the drag created by the transition to digital photography and away from conventional film processing is behind us. And new applications such as LED light bulbs, flexible displays, RFID tags, cellular technology, and even medical equipment and compounds promise to increase the world’s appetite for silver in the coming years.

Why Do Manufacturers Choose Silver?

Jewelers appreciate silver because they can attain a higher polish than with any other metal.

Engineers specify silver because nothing else offers as much electrical or thermal conductivity or as much reflectivity. They find silver indispensable given the inexorable drive to make more efficient electronics and photo-voltaic panels for solar power generation. Manufacturers of medical equipment and supplies employ silver as a biocide. And silver catalysts facilitate the reactions needed to produce ethylene oxide and formaldehyde – major industrial compounds with myriad applications.

Silver’s unique properties, along with the relatively small quantities of silver needed in many applications will make silver hard to replace – even as prices rise.

Key Applications Devour Silver

Solar Panels

The Silver Institute’s Outlook for New Electrical & Electronic Uses of Silver (released July 2014) reports 4% year-over-year growth in overall industrial demand for silver in 2013. Modest, but what isn’t apparent in the headline numbers is that most of that growth came in the second half of the year.

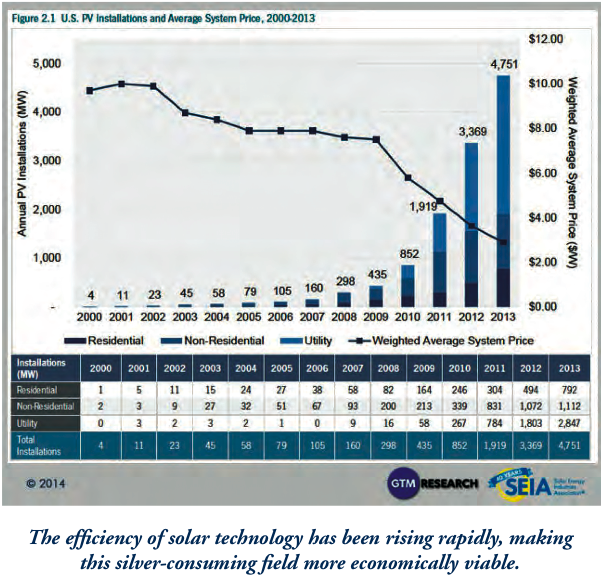

And the recovery was driven in large part by a resurgence in solar panel manufacturing. The solar industry wound up with significant overcapacity, and underwent about 18 months of retrenching as demand caught up.

The surge in silver prices to nearly $50/ounce in 2011 also prompted significant “thrifting.” Manufacturers found ways to do more using less silver – a tough dynamic for short-term demand but likely good for demand longer term, because manufacturers now have less incentive to find alternatives.

Imports of silver powder, particularly in China, for use in new panels are once again on the rise.

The market research firm IHS forecasts 22% growth in solar this year versus 2013. Much of this growth is expected in China and Japan where governments recently shifted policy even more in favor of solar power. But significant growth is expected virtually everywhere as manufacturing costs fall and efficiency rises.

The chart below, showing solar installations and average cost in the U.S., provides a good idea of what is happening globally.

Silver demand in photovoltaic panels represented approximately 40 million ounces in 2013. Investors can expect rapid growth in that number in the coming years.

Flexible Displays

New consumer electronics, including smart watches and wearable medical sensors are just now coming to market, and silver has an important role to play. Currently most touch screens use indium tin oxide as conductive transparent layer. However, the layer is brittle and fragile. More flexible and resilient silver nanowire appears set to gain widespread use as an alternative. Demand for silver in this brand new application is forecast for a modest 500,000 ounces by 2017, but growth beyond that may prove exponential.

LED Lighting

TVs and computer displays already feature LED technology, but light emitting diodes are also transforming the way consumers light their homes and businesses. Anyone visiting their local home- improvement center will encounter an aisle of the new LED light bulbs featuring dramatically longer life and much greater efficiency. In 2013, LED bulbs represented 20% of demand and as prices fall, adoption of the new technology will accelerate.

Silver has three applications in LED: a reflective layer, an adhesive layer, and a bonding wire. Cumulatively, demand for these applications is expected to reach 8 million ounces over the next 5 years. And once again, growth in demand beyond that is expected to be enormous.

Ethylene Oxides & Formaldehyde

Ethylene oxide is a key component in the production of detergents, solvents, plastics, and other organic chemicals. Roughly 25% of the ethylene oxide produced is used to make antifreeze coolant for vehicles. The production of polyester and other common plastics also requires these compounds.

Silver enters the equation, not as a component, but as a catalyst to facilitate necessary chemical reactions. Current annual demand in these applications is roughly 150 million ounces according to the Silver Institute. Thomson Reuters GFMS expects this demand to increase by 8 million ounces in 2014.

Silver’s Positive Outlook

The Silver Institute in their Outlook for New Electronic and Electrical Uses of Silver estimates demand growth in these applications will be 6% for 2014 with similar growth for the next two years. That represents approximately 14 million ounces of additional demand annually. Growth in other industrial applications – including ethylene oxides – should add nearly as many additional ounces. Overall growth in industrial demand looks set to significantly outpace GDP growth.

Silver is clearly good for a lot more than hedging against inflation. And focusing entirely on silver’s role as a monetary metal means overlooking half of the complete picture. Precious metals investors should also factor in silver’s utility in a growing number of manufacturing applications.

….related: Precious Metals Buyers Should Be Wary of Long Delivery Delays

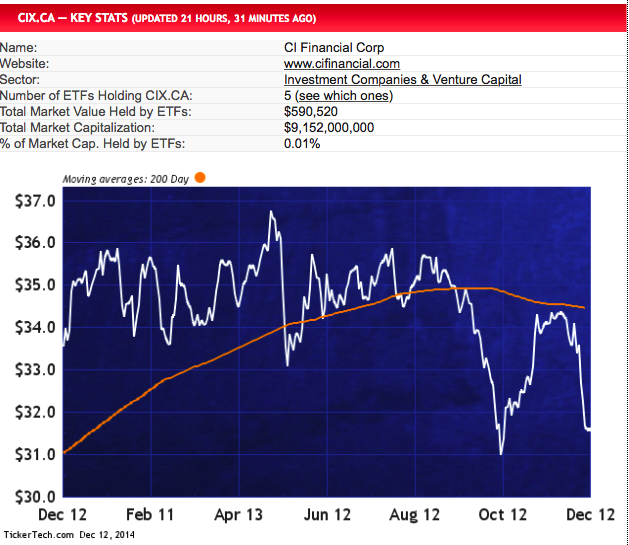

#10. CI Financial Corp (TSE:CIX.CA) — 4.0% YIELD

At #10, CI Financial is engaged in the management, marketing, distribution and administration of mutual funds, segregated funds, structured products and other fee-earning investment products for Canadian investors. Co. operates two reportable segments: Asset Management and Asset Administration. The asset management segment provides the management of mutual, segregated, pooled and closed-end funds, structured products and discretionary accounts. The asset administration segment involves the sale of mutual funds and other financial products, and ongoing service to clients and capital market activities.

![]()

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair