Personal Finance

- Total worldwide debt is estimated to be $158.8 trillion. The US represents 11% of the total.

- In 2014 emerging markets issued $276 billion in US denominated debt. The total emerging market debt issued in US dollars is $1 Trillion.

- The Russian ruble has fallen 70% against the US dollar since the end of June. Russian corporations have $98 billion in US denominated bonds coming due in 2015.

- Greek government debt totals $479 billion US. Annual interest payments are $35 billion US. On January 25, Greece will vote in what amounts to a referendum on being in the EU. (Here will go again.)

- Japan’s total debt is $1.1 trillion US. Debt servicing consumes 43% of government revenues. Japan population is projected to fall from 127 million to 87 million by the year 2060.

Let me start by saying, pay attention to these numbers. There is a high probability that 2015 will see a return of the debt crisis that gripped the world in 2008 and then again in 2011. Of course it never really ended. Central banks led by the Federal Reserve expended trillions of dollars to paper over the problems but that was always just a stopgap – never a solution.

Let me start by saying, pay attention to these numbers. There is a high probability that 2015 will see a return of the debt crisis that gripped the world in 2008 and then again in 2011. Of course it never really ended. Central banks led by the Federal Reserve expended trillions of dollars to paper over the problems but that was always just a stopgap – never a solution.As the world’s biggest bond fun manager, Bill Gross stated, “Solving a debt crisis by creating more debt cannot cure the disease.”

I have no doubt that central banks will do whatever it takes to avoid another debt liquidation panic but the question is – will it be enough. Enough to rescue Russia, Greece, Venezuela and many other emerging market countries.

No one can afford to ignore the rising probability that the next round of consequences of the sovereign debt crisis will occur in 2015 – but what does it mean for interest rates, the dollar, the stock market, real estate and gold?

This is where we can help

Every year at this time I invite you to come to the World Outlook Financial Conference – and why not? The track record of recommendations has been incredible. We have consistently featured some of the best analysts in the English speaking world who are chosen because of their exceptional track records.

Last year three major macro-economic predictions were made: 1) sell oil and oil stocks; 2) interest rates would fall and 3) have a good chunk of your assets in US dollars. Specifically it was recommended to stay away from gold and other metals, sell the euro, and buy quality dividend paying stocks on dips. Our bonus small cap pick, which was sent to attendees immediately after the conference, was up over 100% by the end of the year.

Arguably the most impressive prediction was presented by Martin Armstrong who reiterated his prediction made at the 2013 Outlook Conference for the date of the Russian invasion of Ukraine and the resulting investment repercussions.

But the terrific track record is not the reason I think you should attend this year. As I outlined above, 2015 is different. The period since the initial credit crisis in 2008 is over and we are about to enter the next phase. It will be marked by higher levels of volatility and by desperate moves by governments including tax grabs and civil seizures.

The Easiest Bet

There is going to be big money made and lost in 2015. The recent decline in oil is a reminder how fast things can change. As oil investors have found out – failing to recognize those changes is very costly. I suspect that people who hold euros and yen will get that message drilled home in 2015 and beyond.

Paying For Your Ticket Many Times Over

While past performance is no guarantee of future success this year’s analysts have displayed an uncanny ability to read the various investment markets while employing proven risk management techniques which raised their probability of success dramatically. And it’s why our analysts like the incredible Martin Armstrong, Timer’s Digest Timer of the Year Mark Leibovit, Canada’s best known independent real estate analyst Ozzie Jurock, and Keystone Financial’s Ryan Irvine charge in excess of $1,700 for personal consultations. Yet at the World Outlook Financial Conference you can get access to them and get your individual questions answered for as little as $129.

Our Special VIP Bonuses

If you go to the MoneyTalks store you will see a number of tremendous bonuses – but today I want to tell you about just one. Keystone Financial is about to release their 2015 Cash Rich/Debt Free, Profitable Canadian Micro to Mid-Cap Report ($599 value). This report is included in your VIP ticket purchase. Plus Ryan and his team create our World Outlook Small Cap portfolio that has never failed to deliver significant double digit returns.

There’s nothing more I can say. 2015 is going to be pivotal to our country, companies and individual financial well being. I hope you take advantage of the opportunity.

Sincerely,

Mike,

Host of MoneyTalks

P.S. As you may know I am hugely interested in educating our younger generation and to that end we have a special offer – if you buy a ticket – you can bring a student absolutely free. The only thing is that we ask you add the free student ticket to your online cart when you purchase your ticket because we have a limited number of tickets set aside. And I might add that the students have really enjoyed the conference but it is also a great way to share/create a common interest with your children – no matter what their age.

P.P.S If you have already purchased your tickets and would like to add a student now, please have them CLICK HERE to register and print out their ticket.

Conference Details

- Where: Westin Bayshore Hotel, Downtown Vancouver

- When: Friday January 30th 1:00pm to 8:00pm and Saturday January 31st 9:00am to 4:00pm

- To Order: www.moneytalks.net/events/world-outlook-financial-conference.html

- Cost: General Admission = $129 for a two day pass

Strengths

- Gold traders surveyed by Bloomberg are bullish for next week. Rising concerns surrounding the political uncertainty in Greece are increasing the precious metal’s appeal as a haven.

- Goldman Sachs set its long-term forecast for gold prices at $1,200 an ounce for the next three years. This price is estimated by the investment bank to be the majority of gold producers’ breakeven price. If gold prices fall below $1,200 an ounce, losses would result in a supply reduction, which should prop prices back up.

- China’s net gold imports from Hong Kong reached a nine-month high in November, most likely due to inventory build-ups for the Lunar New Year. Furthermore, the Shanghai Gold Exchange saw strong withdrawals last week at 57.7 tons, bringing the year to date total to 2,073 tons.

Weaknesses

- Gold ended 2014 slightly down, declining 1.72 percent. This is the second-straight year that gold has declined.

- The drop in gold prices this year is affecting coin sales. The U.S. Mint is heading for its biggest annual decline in sales since 2006.

- Gold-backed ETFs are seeing the negative effects of lower gold prices as well. Holdings in gold-backed ETFs dropped to the lowest level since 2009, as roughly $6.7 billion was removed this year.

Opportunities

- Gold prices responded positively to news last Friday that China’s central bank was considering loosening liquidity requirements for the country’s banks. With many seeing this speculation becoming reality, news of further stimulus in China should cause a further rise in gold prices.

- The New York Federal Reserve recently saw a 42 ton withdrawal of gold. The recent rise in gold repatriation from countries like the Netherlands and Germany is a sign that global market and political uncertainty is on the rise and gold is becoming increasingly valued as a haven asset.

- German five-year yields on government bonds dropped below zero this week for the first time. The difficulties facing Europe are captured in this event, as investors are now willing to pay to hold German debt with no returns. With falling rates and growing uncertainty, gold becomes an increasingly valuable alternative asset.

Threats

- Chilean President Michelle Bachelet presented a bill this week that would make union leaders the only authorized negotiators in wage bargaining, while outlawing mining companies’ rights to replace workers on strike. The proposal will risk further investment delays according to the mining companies affected.

- The Zambia Mines Minister is refusing to undo the hike on mining royalties that came into effect on January 1. The policy raises royalties for open pit mines from six percent to 20 percent.

- The Chilean Supreme Court declined to hear Barrick Gold Corp.’s appeal regarding fines imposed on its Pascua-Lama project. The fines, imposed by the country’s environmental regulator, could make it more difficult to move the project forward.

In the sound-money community there is universal skepticism about the Fed’s plan to stop monetizing the world’s debt. Hardly anyone thinks they’ll go through with it and absolutely no one thinks they’ll succeed if they do.

But the Fed is acting like it’s serious. Take a look at the monetary base, which is the amount of new currency that’s been created and pumped into the banking system. The trajectory since the 2008 crash tells you all you need to know about the “recovery,” which turned out to be just the Fed printing money and a few mostly rich people spending some of it. But check out the far right edge where the line turns negative. Not wildly negative, but still, the Fed does appear to have stopped adding and started subtracting. The money supply is falling.

This kind of tightening would normally coincide with — or cause — rising interest rates. But that’s not yet part of the plan, so even in the face of manifestly tighter money, interest rates have been allowed (or forced) to decline.

But the pressure of tighter money has to be released somewhere, and in this case it’s been the foreign exchange market. The euro, for instance, has tanked since mid-year.

Every other major currency is down as well, which is the same thing as saying that the dollar is up big. And a rising currency is functionally the same thing as higher interest rates. Consider: If you borrow money you have to pay back the principal plus interest. A higher interest rate obviously makes the loan harder to repay. But so does a rising currency because in order to pay dollars to a creditor you have to get those dollars, and if they’ve become more valuable in the meantime you have to pay up.

So the US is experiencing two of the three symptoms of tighter money: a falling money supply and rising currency. Will we eventually get the third, rising interest rates? That would be interesting to say the least. To understand why, let’s revisit the monetary base chart, with the addition of arrows showing what the stock market did during the previous two attempts at tapering. It tanked — or at least started to tank — and the government relented.

Note that during those other two taper attempts the monetary base didn’t fall much if at all, and the dollar didn’t rise to anything like its current level. In other words, the Fed didn’t actually tighten, it just stopped loosening. This latest iteration is already more serious than the two that came before.

So either another stock market scare is coming, and soon, or the economy has finally achieved the fabled escape velocity in which it can grow under its own power without help from performance-enhancing monetary drugs. We should know the answer soon.

Spoiler alert: The sound-money crowd is right. This ends very badly.

Low oil prices today may be setting the world up for an oil shortage as early as 2016. Today we have just 2% more crude oil supply than demand and the price of gasoline is under $2.00/gallon in Texas. If oil supply falls too far, we could see gasoline prices doubling within 18 months. For a commodity as critical to our standard of living as oil is, it only takes a small shortage to drive up the price.

On Thanksgiving Day, 2014 Saudi Arabia decided to maintain their crude oil output of approximately 9.5 million barrels per day. They’ve taken this action despite the fact that they know the world’s oil markets are currently over-supplied by an estimated 1.5 million barrels per day and the severe financial pain it is causing many of the other OPEC nations. By now you are all aware this has caused a sharp drop in global crude oil prices and has a dark cloud hanging over the energy sector. I believe this will be a short-lived dip in the long history of crude oil price cycles. Oil prices have always bounced back and this is not going to be an exception.

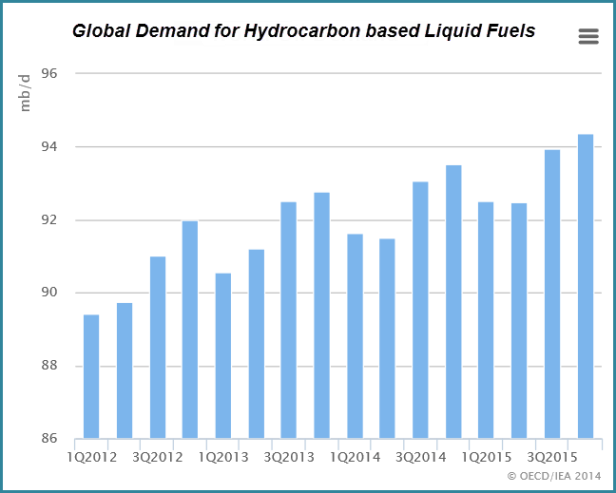

To put this in prospective, the world currently consumes about 93.5 million barrels per day of liquid fuels, not all of which are made from crude oil. About 17% of the world’s total fuel supply comes from natural gas liquids (“NGLs”) and biofuels.

One thing that drives the Bears opinion that oil prices will go lower during the first half of 2015 is that demand does decline during the first half of each year. Since most humans live in the northern hemisphere, weather does have an impact on demand. I agree that this fact will play a part in keeping oil prices depressed for the next few months. However, low gasoline prices in the U.S. are certain to play a part in the fuel demand outlook for this year’s vacation driving season.

Related: Ten Reasons Why A Sustained Drop In Oil Prices Could Be Catastrophic

Brent oil prices are now hovering around $60 a barrel. In my opinion, this is quite a bit lower than Saudi Arabia thought the price would go and may lead to an “Emergency” OPEC meeting during the first quarter. But for now, I am assuming that Saudi Arabia is willing to let the other OPEC members suffer until the next scheduled OPEC meeting in June.

The commonly held belief is that Saudi Arabia is doing this to put a stop to the rapid growth of production from the U.S. shale oil plays. Others believe it is their goal to crush the Russian and Iranian economies. If the oil price remains at the current level for a few months longer it will do all of the above.

My forecast models for 2015 assume that crude oil prices will remain depressed during the first quarter, then slowly ramp up and accelerate as next winter approaches. I believe that by December we will see a much tighter oil market and significantly higher prices. In a December 24, 2014 article in The National, Steven Kopits managing director of Princeton Energy Advisors states that, “In permitting low oil prices, the Saudis seek to bring the market back into equilibrium. At present, our calculation of break-even system-wide is in the $85–$100 a barrel range on a Brent basis.”

Mark Mobius, an economist and regular guest on Bloomberg TV recently said he sees Brent rebounding to $90/bbl by the end of 2015.

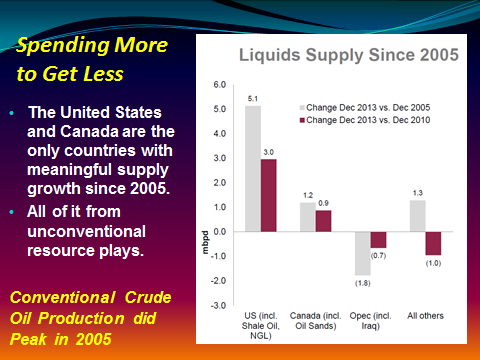

Since 2005, only North America has been able to add meaningful crude oil supply. Outside of Canada and the United States (including the Gulf of Mexico), the rest of the world’s crude oil production netted to a decline of a million barrels per day from December, 2010 to December, 2013. More than half of the OPEC nations are now in decline. We’ve been able to supplement our fuel supply during the last ten years with biofuels, but that is limited since we need the farmland for food supply.

I believe the current low crude oil price could be overkill and result in the next “Energy Crisis” by early 2016. Enjoy these low gasoline prices while they last.

The upstream U.S. oil companies we follow closely are all announcing 20% to 50% cuts in capital spending for 2015. We will start seeing the impact on supply at the same time the annual increase in demand kicks in. Our model portfolio companies are all expected to report year-over-year increases in production, but at a much slower pace than the last few years.

A study released by Credit Suisse two weeks ago shows that U.S. independents expect capital-expenditure (Capex) cuts of one-third against production gains of 10 per cent next year. This would imply production growth of 600,000 bpd of shale liquids, and perhaps another 200,000 bpd from Gulf of Mexico deepwater projects. At the same time, U.S. conventional onshore production continues to fall. I have seen estimates of 500,000 to 700,000 bpd declines within twelve months. If these forecasts are accurate, U.S. oil production growth would be barely positive next year and headed for a material downturn in 2016.

North American unconventionals (oil sands, shale and other tight formations) have been almost all of net global supply growth since 2005. If unconventional growth grinds to zero and conventional growth is falling outright, the supply side heading into 2016 looks highly compromised. At today’s oil price, only the “Sweet Spots” in the North American Shale Plays and the Canadian Oil Sands generate decent financial returns to justify the massive capital requirements needed to continue development. Global deepwater exploration is rapidly coming to a halt.

Were demand growth muted, this might not matter. Demand for liquid fuels goes up year-after-year. It even increased in 2008 during the “Great Recession” and ramped up sharply during 2009 and 2010 despite a sluggish global economy. Low fuel prices are increasing demand today and my guess is that, with U.S. GDP growth now forecast at 5% in 2015, we could see demand for fuels increase by close to 1.5 million barrels per day this year. The current IEA forecast is for oil demand to increase by 900,000 bpd in 2015.

If this plays out, the oil markets will be heading into a significant squeeze in the first half of 2016.

The last extended period of low oil prices was 1985 to 1990. In 1985, when oil prices collapsed similar to what’s happening now, the world had 13 million bpd of spare capacity, with 7 million bpd in Saudi Arabia alone. OPEC was well-positioned to comfortably meet any increase in demand.

Today, just about all of the world’s discretionary spare capacity resides in Saudi Arabia and amounts to an estimate 2 million bpd. Lou Powers, an EPG member and author of “The World Energy Dilemma,” has said that Saudi Arabia will have difficulty maintaining production at over 10 million bpd for an extended period. If we do swing to a supply shortage, Saudi Arabia may find itself in the position of needing to run the taps full out for much of 2016. In such an event, the world will be headed right back into an oil shock and we will see much higher oil prices than $100/bbl.

Related: The Hidden Costs Of Cheap Oil

Low oil prices will hurt the unhedged upstream companies, but they will hurt the oilfield services sector the most. I’m expecting the onshore active rig count to drop by 30% by mid-2015. Oil price will need to firm up for several months before the upstream companies commit to higher spending levels. That said, the high quality drillers like Helmerich & Payne (HP), Patterson-UTI Energy (PTEN) and Precision Drilling Corp. (PDS) will be fine since a lot of their high end rigs will keep working on long-term contracts. By 2016, they will have gained market share.

Remember, North America and deepwater are the only places with meaningful production upside. If crude oil prices move below $60/bbl and stay there for even six months it could prove catastrophic to non-OPEC supply. At some point, OPEC action may become necessary.

“But perhaps not by the Saudis. Russia’s position is comparable to Saudi Arabia’s. Either could cut production by meaningful quantity, but the Russians need the incremental revenue more. Saudi Arabia would be right to argue that any calls for production cuts should be directed to Moscow. OPEC could cut production to prop up prices and increase revenues. But for now, a better strategy (for Saudi Arabia) would be to hang back, deflect criticism, and let events play out. If the Russians are thinking clearly, Moscow will cut first.” – Steven Kopits the managing director of Princeton Energy Advisors.

The best news for all of us is that Iran may be quite willing to put an end to their nuclear enrichment program a few months from now. I believe this is the real reason for what Saudi Arabia is doing.

By Dan Steffens for Oilprice.com

More Top Reads From Oilprice.com:

- Could Libyan Militants Spark An Oil Price Rebound?

- How Broken Are The Energy Markets?

- Follow The Trends For Oil Price Rebound

KeyStone’s 2015 Cash Rich Report Released

KeyStone’s 2015 Cash Rich Report Released

In the wake of the 2008 credit crisis that froze capital, cash in hand became king. With Western economies awash in debt, both public and private, the great deleveraging continues. Companies with strong balance sheets including zero or manageable debt, solid cash positions, good working capital, and good cash generation can withstand downturns and prosper in market upturns. As such, these Cash Rich stocks continue to garner strong market attention.

With that in mind, KeyStone recently released our 2015 cash Rich, Profitable Canadian Small-Cap Stock Report. Research for the 40+ page report begins with over 3,500 Canadian stocks, our research uncovers over 60 Small to-Micro Cap stocks – all profitable, cash rich (no debt) companies, many with between 10-100% of their market caps in cash. We drill down on each providing fundamental statistics and research notes from our management interviews and provide a select number of NEW BUY Reports. We provide Flash Updates with current BUYS|SELL|HOLD ratings on all Cash Rich Stocks currently in coverage. This year, our three New BUY recommendations include 2 high growth software Small-Caps, one low-priced Micro-Cap and bonus notes on our recent Specialty Pharmaceutical selection which trades at a significant discount to its peers.

The report has become an annual must read for growth and value investors. With 16 stocks highlighted in the annual report over the last 3 years receiving premium takeover bids, it serves as an excellent source of potential takeover targets. Unique research you can find nowhere else. Last year’s Top Cash Rich recommendation, Cipher Pharmaceuticals (CPH:TSX), has gained over 140% – do not miss out on this year’s recommendations.

Again, the theme with these companies has been strong balance sheets and strong cash flow. This type of pristine balance sheet can withstand and even profit from a downturn (via strategic expansion through purchase of distressed assets). We believe companies that hold this profile will continue to attract more attention from individual investors and as potential acquisition targets in 2015.

Having said this, readers must be careful to remember that not all companies included in the report meet our full criteria. In fact, a large cash balance in itself does not make a great investment. If not employed effectively, the return on investment can be low and the opportunity to create excellent long-term returns can be wasted.

To compile this report, we included micro, small, and mid-cap stocks with an eye towards the lower end. Within this report, we strove to include companies with cash balances that exceeded (in most cases) 10-20% of their total market cap as a minimum. We also looked for current profitability or profitability within the last 12-months. Our bias was also towards debt free companies or those with cash balances that significantly exceeded long-term debt. Finally, we have also included our brief research notes on each company from MD&A and management interviews. We advise clients pay close attention to these. The report can be used as a tool to put together your own watch list of companies that appeal to you at certain prices and make strategic purchases. While 9 companies in the survey are already in active coverage, we are monitoring the remainder for potential entry points – we encourage clients to reference the notes on each company for further individual details.

While our Top Pick from last year’s Cash Rich Report, Cipher Pharmaceuticals Inc. (CPH:TSX), has performed tremendously well already, the company’s strong free cash flow and cash balance provide management the fuel necessary for accretive acquisitions in 2015. We maintain our current long-term rating on the stock.

In a low oil environment and over the long term, our 2015 report highlights two energy related stock with excellent free cash flow that trade at depressed prices with very strong balance sheet. The first recently employed its cash rich balance sheet and is well positioned to benefit from the fruits of that cash deployment over the course of the next 1-3 years. The company remains a BUY in both the near term and long term even in the current energy environment based on what we expect to be solid growth in the second half of 2015 with its new drill rigs hitting active operation under 2-year contracts. The second energy service stock trades at low relative valuations with a strong balance sheet. In the near term, the company may face growth challenges in its core market if New Tanker builds decline. Having said this, the company is entering new markets in the second half of 2015 and management is focused on deploying its cash on hand towards accretive acquisitions over the next year. The stock is suitable for long-term investors with a 2-3 year time horizon.

Enghouse Systems Limited (ESL:TSX) is a long-term star on our Focus BUY list and considered a core holding for many long-term clients. The stock is an excellent example of how to generate consistent cash flow and growth via that cash flow long term. We maintain our HOLD rating on the stock near term.

Cash Rich Company Notes

This year we beefed up our individual note section providing full company summaries and written analysis with our thoughts on valuations and whether individual companies may be attractive to certain clients. We are monitoring a number of the 60+ companies for potential entry points.

Primary recommendations include our BUY (Focus BUY) on a software and hardware based technology company, which offers a good mix of both growth and an excellent balance sheet at reasonable valuations. We also initiated coverage on a unique on demand TV-based software company which also boasts a strong balance sheet, current growth and the potential for further dramatic growth via new contract wins. Finally, we initiated coverage on a semiconductor monitoring and measuring equipment manufacturer, which offers a strong balance sheet with good current valuations for long-term patient investors.

Outside of our 3 new recommendations included, we continue to closely monitor a number of stocks which we see as excellent businesses from the report that would make excellent long-term businesses if we can find opportune entry points in 2015.

Overall, 2015 is shaping up to be a very interesting year for North American markets. We see select value in information and technology-based businesses and have recently recommended a number of these including an undervalued Specialty Pharmaceutical Small-Cap which is poised to post significant cash flow growth in 2015. There will be select value in energy, but those investing here will likely have to take a long-term view as the industry adjusts to lower energy prices.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair