Currency

Mario Draghi did not disappoint today when the ECB announced a QE programme to buy 60 Billion Euro in assets per month until September 2016 . The asset purchases will cover both private and public sector bonds and will begin in March 2015. European focus will now turn to the Greek election on Sunday.

After the surprise move by the Bank of Canada to cut its overnight benchmark interest rate yesterday the Canadian dollar is still trading near 6 year lows and given the outlook for energy prices and the likely path of monetary policy in the US , further weakness can be expected.

USD/CAD currently 1.2360 (H) 1.2389 (L) 1.2314

![]()

In today’s Outside the Box, good friend Ben Hunt informs us that we have entered the cult phase of the Golden Age of the Central Banker:

We pray for extraordinary monetary policy accommodation as a sign of our Central Bankers’ love, not because we think the policy will do much of anything to solve our real-world economic problems, but because their favor gives us confidence to stay in the market. I mean, does anyone really think that the problem with the Italian economy is that interest rates aren’t low enough? Gosh, if only ECB intervention could get the Italian 10-yr bond down to 1.75% from the current 1.85%, why then we’d be off to the races! Really? But God forbid that Mario Draghi doesn’t (finally) put his money where his mouth is and announce a trillion euro sovereign debt purchase plan. That would be a disaster, says Mr. Market. Why? Not because the absence of a debt purchase plan would be terrible for the real economy. That’s not a big deal one way or another. It would be a disaster because it would mean that the Central Bank gods are no longer responding to our prayers.

But, he points out, the cult phase of any human society is a stable phase in the sense that, while change may happen, it will not happen from within:

There is such an unwavering faith in Central Bank control over market outcomes, such a universal assumption of god-like omnipotence within this realm, that any internal market shock is going to be willed away.

However, there is a minor catch: external market risk factors are all screaming red.

I’ve been doing this for a long time, and I can’t remember a time when there was such a gulf between the environmental or exogenous risks to the market and the internal or behavioral dynamics of the market. The market today is Wile E. Coyote wearing his latest purchase from the Acme Company – a miraculous bat-wing costume that prevents the usual plunge into the canyon below by sheer dint of will.

Ben identifies the three most pressing exogenous risks as the “supply shock” of collapsing oil prices, a realigning Greek election, and the realpolitik dynamics of the West vs. Islam and the West vs. Russia. (You or I might want to expand Ben’s list with one or two of our own favorites; but the point is, it’s a big, bad, volatile world out there right now.) Ben admits that it feels a bit weird to have written on all three of his chosen topics a few weeks before each of them appeared on investors’ radar screens. “Call me Cassandra,” says Ben. (Naw, I’ll stay with Ben.)

Ben identifies the three most pressing exogenous risks as the “supply shock” of collapsing oil prices, a realigning Greek election, and the realpolitik dynamics of the West vs. Islam and the West vs. Russia. (You or I might want to expand Ben’s list with one or two of our own favorites; but the point is, it’s a big, bad, volatile world out there right now.) Ben admits that it feels a bit weird to have written on all three of his chosen topics a few weeks before each of them appeared on investors’ radar screens. “Call me Cassandra,” says Ben. (Naw, I’ll stay with Ben.)

I wouldn’t want to steal too much of Ben’s thunder here, but I just can’t help sharing with you the punch line to his piece: “The gods always end up disappointing us mere mortals.” This is one of Ben’s better pieces, and I really commend it to you as something you need to think about.

Before we examine our collective religious delusions (or at least our central banking delusions), let’s have a little fun. My friend Dennis Gartman (who could be the hardest-working writer in the business) found this gem and shared it with his readers this morning. It is about the supposed lack of environmental concern of the Boomer generation has. And some of you will read it that way.

But I want those of you who are of a certain age (ahem) to realize just how much your world has changed in the last 50 years. If you are young, yes, we really did all the stuff listed below. I personally experienced every one of the rather long list of activities mentioned by the “little old lady.” Major changes in lifestyle since then? No, not really. But I’ll grand you that things are a good deal more convenient and time-saving today. Now sit back and enjoy.

Checking out at the store, the young cashier suggested to the much older lady that she should bring her own grocery bags, because plastic bags are not good for the environment. The woman apologized to the young girl and explained, “We didn’t have this ‘green thing’ back in my earlier days.” The young clerk responded, “That’s our problem today. Your generation did not care enough to save our environment for future generations.” The older lady said that she was right – her generation didn’t have the “green thing” in its day. The older lady went on to explain: “Back then, we returned milk bottles, soda bottles and beer bottles to the store. The store sent them back to the plant to be washed and sterilized and refilled, so it could use the same bottles over and over. So they really were recycled. But we didn’t have the ‘green thing’ back in our day. Grocery stores bagged our groceries in brown paper bags that we reused for numerous things. Most memorable besides household garbage bags was the use of brown paper bags as book covers for our school books. This was to ensure that public property (the books provided for our use by the school) was not defaced by our scribblings. Then we were able to personalize our books on the brown paper bags. But, too bad we didn’t do the ‘green thing’ back then. We walked up stairs because we didn’t have an escalator in every store and office building. We walked to the grocery store and didn’t climb into a 300-horsepower machine every time we had to go two blocks. But you’re right, we didn’t have the ‘green thing’ in our day. Back then we washed the baby’s diapers because we didn’t have the throwaway kind. We dried clothes on a line, not in an energy-gobbling machine burning up 220volts. Wind and solar power really did dry our clothes back in the early days. Kids got hand-me-down clothes from their brothers or sisters (and cousins), not always brand-new clothing. But you’re right, young lady; we didn’t have the ‘green thing’ back in our day. Back then we had one TV, or radio, in the house – not a TV in every room. And the TV had a screen the size of a handkerchief [remember them?], not a screen the size of the state of Montana. In the kitchen we blended and stirred by hand because we didn’t have electric machines to do everything for us. When we packaged a fragile item to send in the mail, we used wadded up old newspapers to cushion it, not Styrofoam or plastic bubble wrap. Back then, we didn’t fire up an engine and burn gasoline just to cut the lawn. We used a push mower that ran on human power. We exercised by working, so we didn’t need to go to a health club to run on treadmills that operate on electricity.” But you’re right; we didn’t have the ‘green thing’ back then. We drank from a fountain when we were thirsty instead of using a cup or a plastic bottle every time we had a drink of water. We refilled writing pens with ink instead of buying a new pen, and we replaced the razor blade in a razor instead of throwing away the whole razor just because the blade got dull. But we didn’t have the ‘green thing back then. Back then, people took the streetcar or the bus, and kids rode their bikes to school or walked instead of turning their moms into a 24-hour taxi service in the family’s $45,000 SUV or van, which cost what a whole house did before the ‘green thing.’ We had one electrical outlet in a room, not an entire bank of sockets to power a dozen appliances. And we didn’t need a computerized gadget to receive a signal beamed from satellites 23,000 miles out in space in order to find the nearest burger joint. But, isn’t it sad, how the current generation laments how wasteful we old folks were just because we didn’t have the ‘green thing’ back then?”

I wonder what our grandchildren will be telling their grandchildren in 50 years… “I remember a time when we actually used combustion engines to drive our cars that belched out dirty gases. We actually had massive electricity-generating power plants and wires everywhere to deliver the electricity, rather than the small, efficient home units that produce free electricity for us now. We used something called glasses to help us see. People actually had to carry their communications devices around, and computers were measured in pounds not ounces. We had to do something called “typing” to write; and while we didn’t have to actually go to places called libraries like our grandparents did, we could and did spend all day searching through a disorganized Internet for what we needed. You weren’t connected biologically to your computer, so getting information in and out of it was a drag.

“People actually got sick and died; and though the situation was getting better, billions of people didn’t have enough food at night. People went to big stores to buy what was needed rather than just ordering it or producing it on the spot. We actually threw garbage away in huge resource-consuming “dumps” rather than completely recycling it into new products at the back of the house. It took like forever to get from one point to another. People actually had to “drive” their car rather than just getting in it and telling it where to go. And people died all the time in those cars – they were so dangerous and uncomfortable. In those days you couldn’t even instantly communicate with anybody by just thinking. You had to push buttons on that clumsy communication device you hauled around, and then talk into it; and if you lost it you were out of touch and out of luck. We didn’t even have intelligent personal robots in those days. It was so Stone Age.”

I could go on and on, but you get the drift. The changes in the last 50 years are simply a down payment on the change we’ll see and live in the next 50.

When I think about central banks and markets and try to figure out how to get preserve and grow assets from where we are today to where we will be in 10 years, it can be a rather daunting and sometimes even a depressing task. But then I think about what the world will be like and how much fun my grandkids are going to have, and I get all optimistic and smiling again.

Have a great week. The future is going to turn out just fine.

Your wondering if we will have flying cars analyst,

John Mauldin, Editor

Outside the Boxsubscribers@mauldineconomics.com

Although many energy stocks are starting to stabilize, oil has yet to find a bottom and base. Most analysts agree that, in the short run, oil prices may go lower.

However, longer-term demand increases and cuts in capital spending and production will eventually cut supplies. After all, companies just can’t spend and produce like they did when prices were $100 per barrel — now, those are below $50, and their costs remain above $50.

This means that, ultimately, production will decline, especially from the U.S. and Canada. We are already hearing about big layoffs in this space.

Just yesterday, Baker Hughes (BHI) announced it would cut 7,000 jobs. Halliburton (HAL), which is acquiring BHI in a $35 billion deal, managed to beat earnings estimates this week after cutting 1,000 jobs last quarter.

It’s not the first time we’ve seen this boom-bust story before, and it won’t be the last. Yet, this certainly creates opportunities for investors.

We’re Not There Yet. But

Are We Getting Closer?

As I have mentioned before, price discovery for oil is made in the futures market, and the futures market is dominated by speculators due to the significant leverage (about 8-to-1).

I have my commodity brokerage license, and used to work at a famous, managed futures firm. So, I can tell you firsthand that futures managers and speculators think and act very differently than investors.

Here’s a simple difference: Individual investors generally focus on fundamentals, while technicals are more important to futures participants than fundamentals.

So today let’s take a look at …

What Futures Traders See for Oil

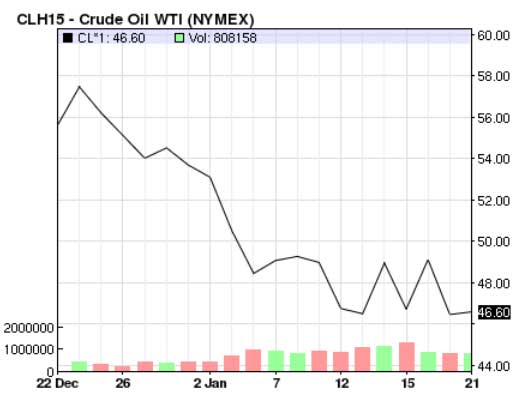

Fundamentally, there is a global surplus of about 3%, but prices are down over 50%. With this relatively small surplus, on a fundamental basis, prices should be at $70 to $80, and not below $50.

Yet, as evidenced by the acceleration in the price decline, the technicals are bearish, which means the futures traders are in control.

On a technical basis, we can look at round numbers for the next support. Prices did not hold at $70, $65 … even $50. Let’s see if prices hold at $45. If they don’t, the next round number would be $40.

If prices held at the $40 area for a sustained period, then oil production would have a high probability of being shut down.

Then, supply and demand would be in equilibrium, with a chance of having shortages.

Now, notice the surge in trading volume on the chart — and most of it selling. Longs were probably forced out due to margin calls as well as shorts being added.

We also saw two big days of buying which may be short-covering. But, we can see most of the volume is selling, and some of that are probably the shorts. When prices reverse eventually, these shorts will have to cover to take profits to avoid losses.

What Earnings Season Will Tell Us About Oil Prices

Oil prices at the end of 2014 are important, as companies that can’t produce economically at those prices or below will have to write down those reserves.

will write more about this after earnings season when we can see the impact on income statements and balance sheets.

Earnings for energy companies normally come late in the earnings season, late February to March.

Also, we still have to be concerned about the Saudis and OPEC, as they can still talk down prices and produce more oil (not much more).

I will write more about this once we understand what will be the production cuts in the U.S. and Canada. Most capital spending and production cuts will be announced during earnings seasons.

Some companies are announcing capital spending cuts before earnings season. At $50 oil, there is sure to be more cuts.

Currently, the Saudis are reducing discounts to certain customers and raising prices for others.

Fortunately, many energy companies are finding bottoms and are basing. Here, we have investors similar to ourselves who realize the bargains with energy companies and the upside these companies have.

Energy Company Outlook

One of the good things about this bear market in energy is that now we can own higher-quality companies with better management, reserves and fundamentals — especially balance sheets.

Previously, these companies were more expensive and would probably not be bought out. I prefer investing in companies that have the potential to be acquired.

I recently recommended such a company, EOG Resources (EOG).

Below is a current chart:

As you know, I have been writing about how energy stocks need to find a bottom and base, but EOG found a bottom in October and has been basing ever since, despite the continued fall in prices.

This is a bullish sign for EOG. Most basing periods last about seven months.

Remember, bases are like diving boards: The longer the board, the greater the next move.

I will probably trade the basing range several times (support $84, resistance $97.50) for the next few months until oil prices find a bottom.

It is normal during a basing period for prices to test support, or even make a new low. This could happen to EOG if oil prices fall to $45 and especially if prices fell to $40.

Unfortunately, most energy stocks don’t look like EOG. Most energy stocks look like the SPDR S&P Oil & Gas Exploration & Production ETF (XOP).

In October through November, XOP was starting to base and had a bullish ascending triangle as participants were buying the pullbacks.

But, once OPEC announced that it would not support prices, most energy stocks took another leg down.

Prices are starting to base again, but with oil prices still bearish, energy stocks could possibly get another leg down — creating even better bargains.

There is still downside risk with energy stocks, but the upside is much greater.

We have to be patient and let oil prices find a bottom.

I have listed many catalysts for oil and energy stocks to move higher. These are worth listing again. Take a look:

- Lower prices could increase oil and gas demand.

- Lower prices will cause cuts in capital spending and production.

- Oil supply disruptions from wars, terrorist attacks, oil spills, weather, and maintenance could occur at any time.

- Normally, oil prices have a risk premium. At this point there is none. Eventually, there should be.

- Most analysts see equilibrium between supply and demand by summer or by the latest the end of the year. Remember, the market is forward-looking, so we need to be invested before equilibrium occurs.

- The best bargains in the markets are among energy stocks and this will attract investors. This is one of the reasons why energy stocks prices are reacting better than oil.

- Most analysts are anticipating more mergers and acquisitions. As you recall, we did see this happen with Talisman Energy (TLM) and with Baker Hughes.

Once oil has found a bottom and starts to base, it will be time to add to existing positions to bring down the cost-per-share basis, or to initiate new ones.

Remember, a base is like a diving board: the longer the diving board, the better and bigger the bounce. So, when prices start to settle and gain some traction, get your shopping list ready because that’s when it will be time to buy again.

Good Gold and Energy Investing,

Dan Hassey

While the financial media is absolutely infatuated with stocks hitting new highs everyday, we would do well to pay attention to some ongoing bear markets:

1) Japanese stocks continue to languish under the effects of deflation following a well over 26 year old bear market, down over 50% from the highs set in 1989.

2) Despite some great innovation out of the U.S from the likes of Apple, Google, Facebook e.t.c the NASDAQ continues to remain in a 15 year bear market down over 10% from the highs in 2000.

3) Despite going parabolic yet again, Chinese stocks continue to remain in a 7 year bear market down well over 50% from the highs set in 2008.

4) US bank stocks are entering a 7 year bear market despite all the QE money and super low interest rates down over 40% from their highs set in 2008.

5) The Euro is also in a 7 year bear market down over 25% against the dollar from it’s highs set in 2008.

6) Gold and gold ETF’s continue to be in bear markets down well over 35% from their highs set in 2008.

7) The more recent casualty oil and oil ETF’s are down well over 60% from their highs set in 2008.

It is well worth noting that it is no strange coincidence that there are major bear markets in several key asset classes and despite recent bear market rallies caused by the FED’s QE for ever policies the hibernating bear is all set to emerge with a vengeance.

There are no two identical business cycles. Their courses depend on the many independent actions of market participants. Also, each time money flows and spreads out differently in the economy, affecting distinct prices in various ways. However, according to a general pattern, business cycles can be broken down into four stages, during which distinct assets classes, including gold, behave differently. To understand what may happen in the gold market during a possible recession, we have to examine how changes in the business cycle affect the performance of different asset classes.

So, according to the literature, stock prices mimic rises and falls in the business cycle, while bonds are anti-cyclical instruments. How does it look in detail? Let’s start from recovery. In that phase (or even at trough) stocks – the leading indicator of economic improvement – begin to grow. In the expansion stage, commodities are the best investment. Commodity prices rise because of the increased demand of entrepreneurs and inflation concerns. It is a good moment to sell bonds, because in the next phase interest rates are increased due to higher demand for credits and a rise in inflation expectations. The hike of interest rates and a credit crunch eventually worry equity market investors, who start selling stocks in anticipation of contraction. During recessions, cash is king, while commodity prices fall due to reduction in demand. In the last stage, i.e., depression, bonds perform the best, as the Fed lowers interest rates. Surely, this is a very simplified picture of the business cycle, not taking into account differences among countries (think about commodity exporting countries like Australia) or within asset classes (e.g., dividends stocks vs. growth stocks), however most of the economists agree that, in short, stocks lead commodities, commodities leads bonds and bonds lead stocks.

But where is gold in that picture? Gold generally doesn’t sync with stocks or bonds over the long run. This is why gold is the best asset class during slowdowns. It is a very interesting result, because commodities in general perform best during downturns. This confirms that gold is something more than just a commodity and is considered by investors as a hedge against currency weakness or financial turmoil. This also means that gold is neither pro-cyclical nor anti-cyclical. Therefore, gold investors should neither be afraid of recession nor assume that gold automatically gains if stock market collapses. It is true, as we pointed out in the last Market Overview, that in the last few years gold was negatively correlated with U.S. stocks (see chart 3). However, historically, gold moves independently. In other words, the relationship between gold and stocks has been anything but static. Changes in the correlation between these two asset classes depend mostly on two factors.

Graph 3: Gold price (PM Fixing, green line) and S&P 500 (red line) from 2005 to 2014

First, this relationship depends on how capital flows between asset classes. For example, after the real-estate market went bust in 2007/2008, hot money went into both stock and gold markets, significantly increasing the correlation coefficient between them. So the question is where the outflows from equities or commodities will go. We have to remember that markets are strongly interconnected today. Therefore, a sharp downturn in one asset class can actually pull down another, as investors are forced to raise cash. This is why gold fell immediately after Lehman’s bankruptcy and the stock market collapse.

Second, the relationship between stocks and gold can be affected by the changes in the greenback’s value. Generally, stocks are negatively correlated with the U.S. dollar. However, during the last few years the greenback often declined in tandem with equities selloffs, e.g., between May 21, 2013 and June 5, 2013. Therefore, gold can gain in the case of stocks falling, but a lot depends, as we thoroughly explained in one of the previous editions of the Market Overview, on the behavior of the U.S. dollar. We are not saying that we are already entering a recession; however this is what just happened to Japan. And stock market investors were clearly nervous in December because of the low oil prices. Gold investors should be simply aware that, according to the business cycle approach to the asset allocation, falling commodity prices often signal the recession. Therefore, they should also know what entering into recession implies for gold market, and understand that equity selloffs do not guarantee gains in gold. A lot of depends on Fed’s monetary policy and the behavior of the U.S. dollar.

Would you like what are the prospects of greenback? We analyze this issue in our last Market Overview report. We provide also Gold & Silver Trading Alerts for traders interested more in the short-term correlations between gold and other asset classes. Sign up for our gold newsletter and stay up-to-date. It’s free and you can unsubscribe anytime.

********

Courtesy of Sunshine Profits‘ Market Overview Editor

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair