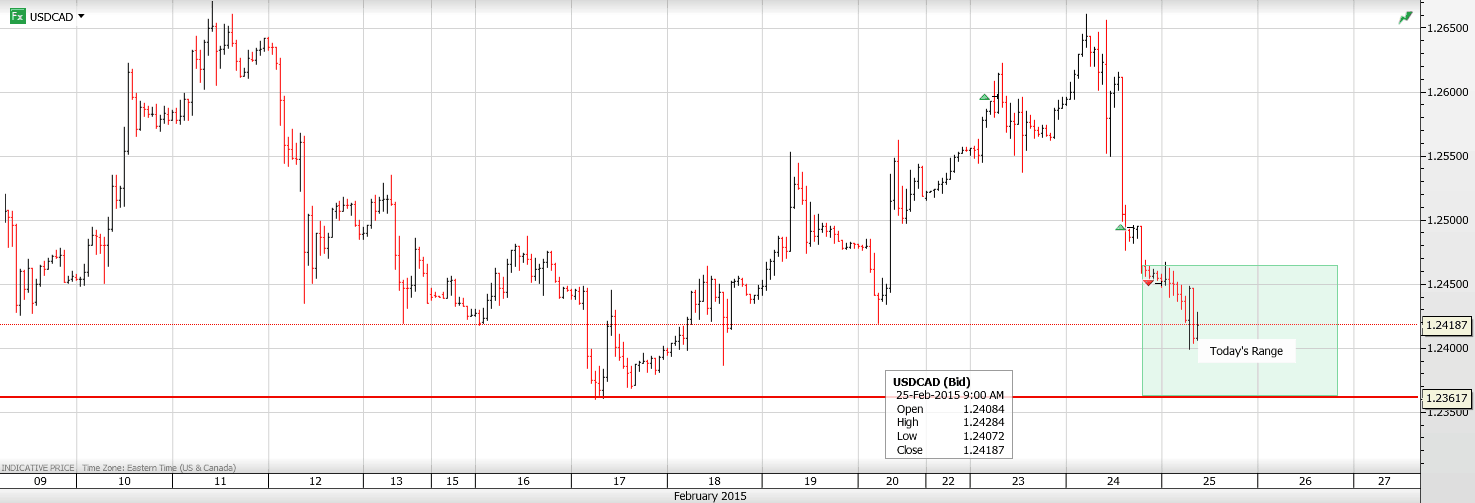

Currency

USDCAD Overnight Range 1.2405-1.2496

It appears that Mr. Poloz has taken the 1980 Devo song to heart and decided to whip the FX markets and whip’em good. After whipping the Loonie to Fifty Shades of Down last month, he used yesterday’s speech and lashed the Loonie Fifty Shades of Up. Last month’s rate cut was blamed on “falling oil prices being unambiguously negative for Canada”.Yesterday,not so much. The rate cut was just insurance. March rate cuts predictions were tossed out the window while Mr. Poloz gleefully clapped “it’s an exciting time to be a Central Banker.” Expectations for another rate cut on Tuesday were tossed out the window along with USDCAD bulls and the Loonie gained over 2 cents.

Meanwhile, the debate rages as to whether Ms. Yellen’s speech was hawkish or doveish. Her comments were fairly upbeat leaving scope for a June hike on the table.Unfortunately,it seems that FX markets expected her to declare June, FOMC Rate Hike month and were disappointed.

Tomorrow’s US economic data releases will be important signposts as to whether a June rate hike is still on the table.

USDCAD technical Outlook

The intraday USDCAD technicals are bearish following the break of 1.2490 and 1.2440 which targets the 1.2340-60 area. A break here risks further losses to 1.2050. For today, USD support is at 1.2405 and 1.2380. Resistance is at 1.2450 and 1.2470

Today’s Range 1.2380-1.2450

![]()

Please remember this warning when you go to the ATM to get cash… and there is none!

Please remember this warning when you go to the ATM to get cash… and there is none!

While we were thinking about what was really going on with today’s strange new money system, a startling thought occurred to us.

Our financial system could take a surprising and catastrophic twist that almost nobody imagines, let alone anticipates.

Do you remember when a lethal tsunami hit the beaches of Southeast Asia, killing thousands of people and causing billions of dollars of damage?

Well, just before the 80-foot wall of water slammed into the coast an odd thing happened: The water disappeared.

The tide went out farther than anyone had ever seen before. Local fishermen headed for high ground immediately. They knew what it meant. But the tourists went out onto the beach looking for shells!

The same thing could happen to the money supply: Cash could evaporate suddenly and disastrously – just before we drown in it.

Credit Money

Here’s how… and why:

If you look at M2 money supply – which measures coins and notes in circulation as well as bank deposits and money market accounts – America’s money stock amounted to $11.7 trillion as of last month.

But there was just $1.3 trillion of physical currency in circulation – about only half of which is in the US. (Nobody knows for sure.)

What we use as money today is mostly credit. It exists as zeros and ones in electronic bank accounts. We never see it. Touch it. Feel it. Count it out. Or lose it behind seat cushions.

Banks profit – handsomely – by creating this credit. And as long as banks have sufficient capital, they are happy to create as much credit as we are willing to pay for.

After all, it costs the banks almost nothing to create new credit. That’s why we have so much of it.

A monetary system like this has never before existed. And this one has existed only during a time when credit was undergoing an epic expansion.

So our monetary system has never been thoroughly tested. How will it hold up in a deep or prolonged credit contraction? Can it survive an extended bear market in bonds or stocks? What would happen if consumer prices were out of control?

Less Than Zero

Our current money system began in 1971.

It survived consumer price inflation of almost 14% a year in 1980. But Paul Volcker was already on the job, raising interest rates to bring inflation under control.

And it survived the “credit crunch” of 2008-09. Ben Bernanke dropped the price of credit to almost zero, by slashing short-term interest rates and buying trillions of dollars of government bonds.

But the next crisis could be very different…

Short-term interest rates are already close to zero in the US (and less than zero in Switzerland, Denmark and Sweden). And according to a recent study by McKinsey, the world’s total debt (at least as officially recorded) now stands at $200 trillion – up $57 trillion since 2007. That’s 286% of global GDP… and far in excess of what the real economy can support.

At some point, a debt correction is inevitable. Debt expansions are always – always– followed by debt contractions. There is no other way. Debt cannot increase forever.

And when it happens, ZIRP and QE will not be enough to reverse the process, because they are already running at open throttle.

What then?

The value of debt drops sharply and fast. Creditors look to their borrowers… traders look at their counterparties… bankers look at each other…

…and suddenly, no one wants to part with a penny, for fear he may never see it again. Credit stops.

It’s not just that no one wants to lend, no one wants to borrow either – except for desperate people with no choice, usually those who have no hope of paying their debts.

Just like we saw after the 2008 crisis, we can expect a quick response from the feds.

The Fed will announce unlimited new borrowing facilities. But it won’t matter….

House prices will be crashing. (Who will lend against the value of a house?) Stock prices will be crashing. (Who will be able to borrow against his stocks?) Art, collectibles and resources – all will be in free fall.

The NEXT Crisis

In the last crisis, every major bank and investment firm on Wall Street would have gone broke had the feds not intervened. Next time it may not be so easy to save them.

The next crisis is likely to be across ALL asset classes. And with $57 trillion more in global debt than in 2007, it is likely to be much harder to stop.

Are you with us so far?

Because here is where it gets interesting…

In a gold-backed monetary system prices fall. But the money is still there. Money becomes more valuable. It doesn’t disappear. It is more valuable because you can use it to buy more stuff.

Naturally, people hold on to it. Of course, the velocity of money – the frequency at which each unit of currency is used to buy something – falls. And this makes it appear that the supply of money is falling too.

But imagine what happens to credit money. The money doesn’t just stop circulating. It vanishes.

A bank that had an “asset” (in the form of a loan to a customer) of $100,000 in June may have zilch by July. A corporation that splurged on share buybacks one week could find those shares cut in half two weeks later. A person with a $100,000 stock market portfolio one day, could find his portfolio has no value at all a few days later.

All of this is standard fare for a credit crisis. The new wrinkle – a devastating one – is that people now do what they always do, but they are forced to do it in a radically different way.

They stop spending. They hoard cash. But what cash do you hoard when most transactions are done on credit? Do you hoard a line of credit? Do you put your credit card in your vault?

No. People will hoard the kind of cash they understand… something they can put their hands on… something that is gaining value – rapidly. They’ll want dollar bills.

Also, following a well-known pattern, these paper dollars will quickly disappear. People drain cash machines. They drain credit facilities. They ask for “cash back” when they use their credit cards. They want real money – old-fashioned money that they can put in their pockets and their home safes…

Dollar Panic

Let us stop here and remind readers that we’re talking about a short timeframe – days… maybe weeks… a couple of months at most. That’s all. It’s the period after the credit crisis has sucked the cash out of the system… and before the government’s inflation tsunami has hit.

As Ben Bernanke put it, “a determined central bank can always create positive consumer price inflation.” But it takes time!

And during that interval, panic will set in. A dollar panic – with people desperate to put their hands on dollars… to pay for food… for fuel…and for everything else they need.

Credit may still be available. But it will be useless. No one will want it. ATMs and banks will run out of cash. Credit facilities will be drained of real cash. Banks will put up signs, first: “Cash withdrawals limited to $500.” And then: “No Cash Withdrawals.”

You will have a credit card with a $10,000 line of credit. You have $5,000 in your debit account. But all financial institutions are staggering. And in the news you will read that your bank has defaulted and been placed in receivership. What would you rather have? Your $10,000 line of credit or a stack of $50 bills?

You will go to buy gasoline. You will take out your credit card to pay.

“Cash Only,” the sign will say. Because the machinery of the credit economy will be breaking down. The gas station… its suppliers… and its financiers do not want to get stuck with a “credit” from your bankrupt lender!

Whose lines of credit are still valuable? Whose bank is ready to fail? Who can pay his mortgage? Who will honor his credit card debt? In a crisis, those questions will be as common as “Who will win an Oscar?” is today.

But no one will know the answers. Quickly, they will stop guessing… and turn to cash.

Our advice: Keep some on hand. You may need it.

Regards,

Bill

Business Insider’s Myles Udland just posted a chart, drawn from research by the Bank of England, showing interest rates for the past 3,000 years. And for all those who’ve been feeling like today’s “new normal” is actually profoundly abnormal, here’s your proof. It turns out that interest rates, both long and short-term, are lower than they’ve ever been. Not lower than in this cycle, or post-war or in the past century, but ever, going back to the earliest days of markets.

And they’re still falling in most of the world. Central banks are cutting rates on a daily basis (Turkey was today’s announcement), in some cases to less than zero. Something like $2 trillion of sovereign and corporate debt now trades with negative yields.

Virtually the only major entity considering raising rates is the US, and the incongruity of this threat has traders balking. See Bloomberg’s Traders still don’t believe the Fed is ready to raise rates.

If this is indeed uncharted territory and we’re going further in before we’re done, what are the implications for markets and, well, everything? A couple of thoughts:

The insurance industry, pension funds and money market funds all depend on positive yields to operate. A life insurance company, for instance, can keep premiums low because it can invest that cash for years before having to pay out on the policy. What happens if the bonds it buys start yielding nothing (or less than nothing)? What about a money market fund that can no longer find investment grade corporate paper yielding much more than zero? Pension funds, meanwhile, have generally promised 7%-8% returns to their members, but now have to get all of those profits from the equity and real estate sides of their portfolios.

For any of these entities to stay in business they now have to act like hedge funds, taking on extra risk, rolling the dice and hoping that the good years outweigh the bad ones. In other words, these formerly safest-of-the-safe investment vehicles become just as risky as the typical eTrade account.

Then there’s the impact of negative rates on the market’s price signaling mechanism for the rest of us. Interest rates are the price of money, and as such they tell investors, entrepreneurs and consumers what to do. Low interest rates generally say “buy, build, consume, take risks” while high rates say “save, sell, conserve, wait.” But zero or negative rates? Are they just an extreme version of low rates or is there a qualitative difference? Everyone has a theory about this but in the absence of historical precedent, we’ll have to wait and see.

Anyhow, the coming negative interest rate world will provide plenty of thrills, chills and blog post material. For now it’s enough to note that we’ve never, through depressions, world wars, bubbles and famines, seen anything like today’s economy.

There are many opposing views as to what will drive the price of gold this year and in which direction. We will discuss these views and the major factors that have contributed to their formation. Gold is a function of monetary policy just as currencies are, so we will cover on the actions and current stance of major central banks with a heavy focus on the Fed and the US economy. We currently hold the view that the Fed will hike this year and that this will drive gold to new lows before the end of 2015.

There are many opposing views as to what will drive the price of gold this year and in which direction. We will discuss these views and the major factors that have contributed to their formation. Gold is a function of monetary policy just as currencies are, so we will cover on the actions and current stance of major central banks with a heavy focus on the Fed and the US economy. We currently hold the view that the Fed will hike this year and that this will drive gold to new lows before the end of 2015.

US Economy

Since the global financial crisis in 2008 the US economy has appeared to be on the road to recovery, only for its health to decline further. These false starts show that the current growth and apparent economic health in the US may not be the beginning of another boom. If this is the case the Fed will have to delay the first rate hike, which will be extremely bullish for gold.

However, the signs are particularly strong at present. The employment sector has shown consistent growth with considerable gains in nonfarm payrolls. The average gain of 268,000 jobs a month over the last twelve prints has led to unemployment declining towards the Fed’s target, and has thus resulted in many holding the view that 2015 will see the beginning of a new tightening cycle

From a trading perspective we believe the current situation is one of “the trend is your friend”. This means that we would rather react to a change in data or waning of economic momentum than to call that the economy is heading south prematurely. Moving against the tide of the US economy has been a losing battle for gold bulls in recent years.

The Fed

Gold bears and the majority of investors in the markets both believe that the Fed will hike this year. We are among these, with the June meeting being the most likely candidate for a hike being our view. Just as massive quantitative easing and accommodative monetary policy was highly bullish for gold, a rate hike and an overall tightening of policy will drive gold lower. This means that if data continues to show improvement in the economy, then the Fed will hike this year and gold will be driven to new lows.

Although if recent strength is simply another false start and the data takes a turn for the worse, then the Fed will delay the start of a new tightening cycle. In fact, if the situation becomes severe there is the possibility that the Fed may introduce new easing measures. A dovish change in stance from the Fed, by way of at least a delay in tightening, would be highly bullish for gold.

The Fed has been building towards a rate hike ever since tapering was first discussed, which means that they have now been on this course for years. The situation in the economy also appears strong enough to support higher interest rates and is likely to continue to show improvement. We therefore believe it is near certain that the Fed will hike rates before the year is out.

Monetary Policy Globally

Gold is a function of monetary policy, which is why we cover actions of central banks closely in our research. However, the Fed is not the only central bank, even if it is the most influential to the gold price. This means that we must also consider the actions of central banks globally.

Outside of the US monetary policy is still highly accommodative. The BOJ and ECB have both embarked upon new, major quantitative easing programs in the last six months while other countries are cutting rates or at least holding back in increasing them. This provides a positive back drop for the gold as an alternative monetary asset that cannot be simply “printed” to ease economic conditions.

Yet in spite of this accommodative policy, the fact of the matter is that gold still remains very close to the lows made last November.

The argument that we as gold bears hold as to why ECB QE has failed to drive gold higher is based on the nature of the QE, which targets credit rather than simply being broad based. This means that it will stimulate growth in a similar way to QE3 in the US, which history shows was highly bearish for gold.

The action from the BOJ has not sparked any major movement higher either, but for a different reason. This is that markets and come to expect accommodative policy from Japan after years of deflation and the efforts to combat it. This has lessened the impact on the gold price to effectively nil, which means that future action is unlikely to spark a rally either.

This means that although the actions of central banks globally may provide a positive back drop for gold, it does not make sense to be holding the metal. There are other strategies, such as selling downside equity protection and being long stocks, that are much better suited to taking advantage of accommodative monetary policy.

Currency

Monetary easing across most of the world means that the currencies of these economies, such as the Euro and the Yen, are likely to weaken. This is bullish for gold since the metal makes a good investment as an alternate currency for those in the Eurozone and countries with an accommodative stance.

However, there are also bearish currency implications that arise from the Fed moving towards a tightening cycle while policy is still dovish across the rest of the world. The US dollar has strengthened significantly with a rate hike has been priced in while other currencies are being weakened.

This strength has slowed upward movement in the gold price and is likely to continue to do so. A strengthening US dollar also means that even if gold stays at its current level in other currencies, it has the potential to decline in US dollars.

We believe that the currency implications are on the whole bearish for gold. It is unlikely that increased demand for gold as an alternative monetary asset will counteract the strengthening of the US dollar and the bearish effects of the Fed moving towards a tightening cycle.

Oil

Oil has more than halved since June last year and has lost a third of its value in the last three months alone. This decline and the resultant low energy costs are arguably yet to flow through to effect inflation in full. This means that disinflationary risks are still present with the potential to delay a rate hike and push gold higher.

There is also the risk that oil breaks lower again and declines significantly form here. This leads to the possibility of disinflation and new QE programs in the US to combat it. The effect of which would be massively bullish for gold.

Oil prices have stabilised somewhat around the $50 level, which means that there is the potential for an increase from here. Given that this is the case, we believe the Fed will look through the drop in energy costs as “transitory”, just as they did when oil prices rose post GFC. Policy is about much more than the price of oil and as such linking Fed policy with such high leverage to energy costs is a misconception.

Inflation

The key risk to a bearish stance on gold is a change in the trend of economic data in the US. At present this data is showing improvement in the US economy, particularly in the employment sector as we have covered, but there should be at least some concern around prices. There has been a lack of wage push inflation and the overall inflation rate has slowed since reaching 2.1% in June last year, with the last print showing only a 0.8% rise in prices. If this continues, then the Fed will be under less pressure to increase rates and therefore may delay the first rate hike and lead to a rally in gold.

Although lower inflation does pose a risk to gold shorts, it is unlikely that this risk will become a reality. We are beginning to see wage inflation that is likely to increase as the unemployment rate declines further. Oil prices have also begun to stabilise and have the potential to rebound from here. This means that the current situation in inflation is likely to be transitory and not indicative of the overall economic health in the US. Therefore, it is likely that inflation will provide sufficient pressure for the Fed to hike this year.

Conclusion

Considering the factors and dynamics discussed we are bearish on gold. We respect the risks in play and believe that the extent of the Fed’s hiking cycle will be less than the market currently anticipates, but that ultimately the effect will be bearish. We hold the view that the Fed will hike in June and that ahead of this gold will suffer significantly. Specifically, we believe that gold will make a new low and trade beneath the $1130.40 level seen last November and are offering a money back special to new subscribers until March if we are wrong. To find out how exactly we will take advantage of the decline in gold, please subscribe below.

Go gently.

Bob Kirtley

Email:bob@gold-prices.biz

To stay updated on our market commentary, which gold stocks we are buying and why, please subscribe to The Gold Prices Newsletter, completely FREE of charge. Simply click here and enter your email address. Winners of the GoldDrivers Stock Picking Competition 200

DISCLAIMER : Gold Prices makes no guarantee or warranty on the accuracy or completeness of the data provided on this site. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This website represents our views and nothing more than that. Always consult your registered advisor to assist you with your investments. We accept no liability for any loss arising from the use of the data contained on this website. We may or may not hold a position in these securities at any given time and reserve the right to buy and sell as we think fit.

We have talked a lot in recent months about the panorama of technology innovation, but in our lifetimes there have been very few truly revolutionary technology developments.

The standard is high. One of the first great technology innovations for mankind was the wheel. Beat that, Apple! The harnessing of fire was another big one.

The invention of sailing ships was huge, the cotton gin, the internal-combustion engine, the light bulb, the telephone, the automobile, the train and the jet airplane — all major steps in the development of civilization and commerce.

In the past 50 years, the list narrows quite a bit. Certainly the eradication of certain serious diseases such as polio and smallpox via vaccines has to be listed among the great technologies.

And you will get a debate on this subject, but I would put the development of the Internet — or the networking of computers — among the great innovations of the past 50 years. The Internet has revolutionized the way we learn, communicate, entertain, shop and govern. Add mobility from the development of cellular networks, and the value of fast information dissemination rises dramatically.

Yet to be fair, most of the major developments of the Internet and networking were accomplished in the 1960s and 1970s, and then only refined in the 1980s, 1990s and 2000s. A modern laptop computer is light years faster and can store far more than the original IBM PC that was introduced in 1980, but those are evolutionary, not revolutionary, developments. If you were to transport an office worker from 1982 and put them in front of a modern Dell desktop computer they would be delighted by the speed, color monitor and graphic interface, but they would know their way around.

Yet to be fair, most of the major developments of the Internet and networking were accomplished in the 1960s and 1970s, and then only refined in the 1980s, 1990s and 2000s. A modern laptop computer is light years faster and can store far more than the original IBM PC that was introduced in 1980, but those are evolutionary, not revolutionary, developments. If you were to transport an office worker from 1982 and put them in front of a modern Dell desktop computer they would be delighted by the speed, color monitor and graphic interface, but they would know their way around.

This begs the question of what all those Silicon Alley engineers have been doing the past two decades. From the standpoint of the timeline of science, it seems like a complete waste to put all those Stanford and MIT computer engineers to work coming up with better online advertising algorithms, or new ways of displaying videos in Facebook, or writing code that prevents hackers from breaking into an electronic vault of medical records.

Where’s a breakthrough on the order of the cotton gin or internal combustion engine today? I want to see some truly amazing, not just an iPhone 6 that has a screen that’s a smidge bigger than its predecessors and sports an improved voice command module that can make lunch reservations.

Looking out on the horizon, the most dynamic new technology developments that I see coming are in power and transportation: First, cheap, accessible, grid-level solar energy coming down to a price that is more than competitive with fossil and nuclear fuels; and second, a move toward “autonomous” vehicles for personal and commercial travel — i.e. drone cars in neighborhoods, at the docks and on freeways.

Both of these developments are coming much faster than the public realizes. I sense there may virtually be a “phase change,” in the words of one researcher, which describes a moment when everything transforms quickly rather than slowly. An example would be if you were to apply a match to an ice cube. The molecules undergo a phase change from solid to vapor without stopping first at the intervening state of liquid.

In our recent lifetimes we have seen real but less significant changes in our habits by fast-moving technology. Three years ago you might have spent $300 on the latest Blu-Ray DVD player for movie watching. Now that player sits on its shelf unused as the shift to streaming everything — movies, TV shows and music — has progressed at what feels like lightning speed. You might also have a laptop gathering dust somewhere that you have abandoned in favor of a tablet, such as an iPad. Or indeed you may have an iPad gathering dust now that your smartphone has a comfortably viewable, bright, fast 5.5-inch screen.

All of these developments will be absolutely pale compared to changes coming down the road, so to speak, in the electrical grid and autonomous cars. Big energy companies not too long from now are likely to be looking at their thousands of drilling rigs much like you look at that Blu-Ray player.

Only thousands of times worse. If solar energy becomes as price-competitive at the grid level as soon as I suspect, then not just those rigs but trillions of dollars’ worth of “stranded” oil and gas assets will have to be written down by all the energy companies.

That will cause a major dislocation in markets as investors absorb the losses, but it will be temporary as it will give way to an era of plentiful solar energy that is not just much cleaner but also much cheaper. The money that manufacturers, governments and consumers will save on fossil fuels will be put to new and potentially much better uses, fueling a new boom.

And likewise, as you can learn about in Martin’s column yesterday, autonomous cars, trucks and ships are no longer science fiction. They are rolling down the track at incredible speed, as companies as diverse as Uber, Apple, Audi, General Motors and Tesla are already running neck and neck in attempting to create and lock up as much intellectual property as possible.

I will have much more for you on this subject as 2015 unfolds. Stay tuned.

Best wishes,

Jon Markman

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair