Gold & Precious Metals

Here are today’s videos and charts:

Gold Slow Stokes Calls A Turn Video Analysis

FXI (China Stock Market ETF) Breakout Of Champions Video Analysis

Silver Potential Bull Flag Video Analysis

GDX Bulls Charge Towards $20 Video Analysis

GDXJ Slow Stokes Calls A Turn Video Analysis

Junior Gold Stock Trade Tactics Video Analysis

Thanks,

Morris

Friday, Apr 3, 2015 Super Force Signals special offer for Money Talks Readers:

Send an email to trading@superforcesignals.com and I’ll send you 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you!

The SuperForce Proprietary SURGE index SIGNALS:

25 Surge Index Buy or 25 Surge Index Sell: Solid Power.

50 Surge Index Buy or 50 Surge Index Sell: Stronger Power.

75 Surge Index Buy or 75 Surge Index Sell: Maximum Power.

100 Surge Index Buy or 100 Surge Index Sell: “Over The Top” Power.

Stay alert for our surge signals, sent by email to subscribers, for both the daily charts on Super Force Signals at www.superforcesignals.com and for the 60 minute charts at www.superforce60.com

About Super Force Signals:

Our Surge Index Signals are created thru our proprietary blend of the highest quality technical analysis and many years of successful business building. We are two business owners with excellent synergy. We understand risk and reward. Our subscribers are generally successfully business owners, people like yourself with speculative funds, looking for serious management of your risk and reward in the market.

Frank Johnson: Executive Editor, Macro Risk Manager.

Morris Hubbartt: Chief Market Analyst, Trading Risk Specialist.

website: www.superforcesignals.com

email: trading@superforcesignals.com

email: trading@superforce60.com

SFS Web Services

1170 Bay Street, Suite #143

Toronto, Ontario, M5S 2B4

Canada

Apr 3, 2015

Morris Hubbartt

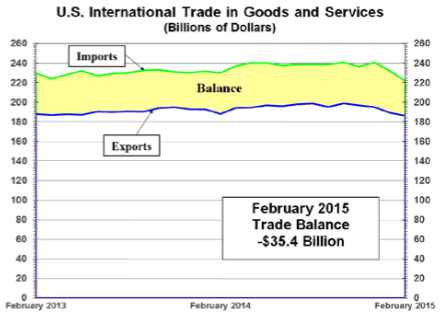

Trade Deficit Shrinks

Inquiring minds are investigating the Commerce Department report on International Trade in Goods and Services for February 2015, for clues about first quarter GDP.

Highlights

- Exports were $186.2 billion, down $3.0 billion from January.

- Imports were $221.7 billion, down $10.2 billion from January.

- Year-to-date, the goods and services deficit decreased $ 2.6 billion, or 3.2 percent, from the same period in 2014.

- Year-to-date exports decreased $5.3 billion or 1.4 percent.

- Year-to-date imports decreased $7.9 billion or 1.7 percent.

Balance of Trade

GDP Analysis

Recall that exports add to GDP and imports subtract from GDP. Thus my first reaction to the report was that

GDP estimates would go up. They did, but very slightly.

Atlanta Fed GDPNow Model

Yesterday, following an Unexpected Decline in Construction activity, the Atlanta Fed GDPNowforecast dipped to 0.0%.

Today following the shrinkage in the trade deficit, the forecast is back in positive territory at 0.1%.

“The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2015 was 0.1 percent on April 2, up from 0.0 percent on April 1. Following this morning’s international trade release from the U.S. Census Bureau, the nowcast for the change in real net exports in 2009 dollars increased from -40 billion to -33 billion. The nowcast for real equipment investment growth declined from 7.5 percent to 6.1 percent following the international trade report and the Census Bureau’s M3 manufacturing report.“

GDPNow Estimate for 1st Quarter

Another Sign of Slowing Global Economy

The declining trade deficit is a good thing. However, the shrinking trade deficit is not as positive as it may look at first glance.

It would have been far better had the trade deficit shrinkage been on rising exports. Instead, imports and exports are both down. That is yet another sign of the slowing global economy.

Back in January, I forecast declining exports on the strength of the US dollar. Here we are. If oil ticks back up for any reason, so will imports.

There is not a lot to cheer about in today’s reports (Also see Factory Orders Unexpectedly Rise Snapping String of 6 Straight Declines.)

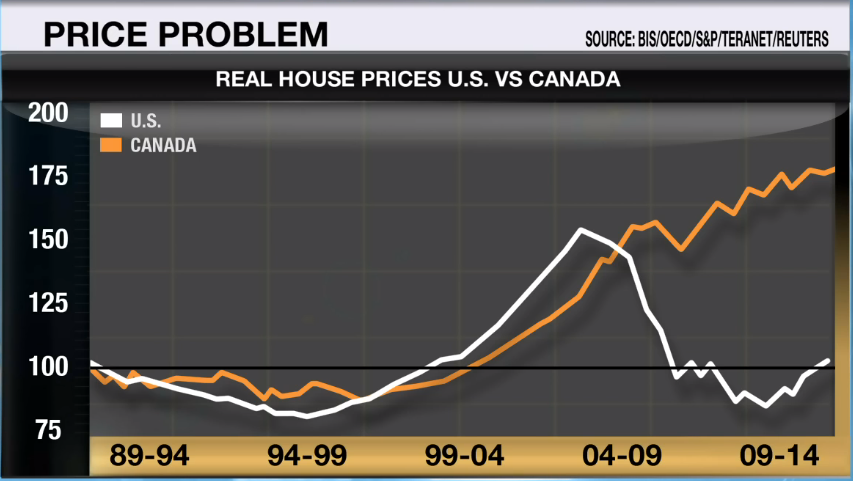

The author of BoomBustOlogy “Spotting Financial Bubbles Before They Burst”, explains why he’s shortselling Canadian Real Estate. Below are some bullet poiints from the compelling 9 minute BNN interview, worth listening to – Editor Money Talks

Canadians have extremely higher debt to income ratios than Greeks do.

Canadian housing prices have diverged extremely upward from the U.S. experience without a corresponding correction.

The Canadian economy is at risk from the oil sell off.

Canadian sub-prime loans could be as high as 25% of new loan creation.

Canadian hubris, over confidence and fear:

1) Canada is different,

2) foreign buyers want Canadian real estate,

3) real estate prices will continue to rise (the inflation argument),

4) have to buy now before being priced out.

Click on image to listen to the 9 minute interview (begins after commercial)

The action in a number of markets reached some stressed out levels. This showed up in the Downside Capitulation in The Canadian dollar. At the end of January that was on the daily, weekly and monthly readings. The low then was 78.13. The rise was to 80.88 and last week’s low was 77.92, which looks like a good test. Now it is up to the 50-Day ma and getting above would be constructive.

Crude oil has been trading with the $C, or the other way around, and seemed have concluded a test last week.

Our March 19th Memo noted that the “Ides of March” target of a tradable low on gold seems to have worked out and the rally can continue on what could be an intermediate move. What is again needed in this department is gold shares to be outperforming the bullion price and silver to be outperforming gold.

Both seem underway as the gold/silver ratio has jumped from .132 to .143, which is fast.

Base metals (GKX) have also completed the test last week and have jumped. Much the same holds for the grains (GKX). The overall index, the DBC has been working on the same pattern.

Our last Pivot was dated March 12th and it was looking for a “pause” in the hot dollar action. The decline and associated rallies on commodities makes sense to us and could be another “Rotation”. The hot stuff gets tired and the boring, perhaps terrifying items come back from the dead.

Getting through some moving averages will help and with that the action could run into May.

It is uncertain how the senior stock indexes will perform, but the ChartWorks has noted that the Biotechs (IBB) which have been super-flyers have clocked a rare Trifecta Sell.

BOB HOYE, INSTITUTIONAL ADVISORS – WEBSITE: www.institutionaladvisors.com

Several months ago, the government of Australia proposed to tax bank deposits up to $250,000 at a rate of 0.05% (5 basis points).

Several months ago, the government of Australia proposed to tax bank deposits up to $250,000 at a rate of 0.05% (5 basis points).

Their idea was for the money to be invested in a rainy day Financial Stabilization Fund to insure against in the unlikely event of a banking crisis… or all-out collapse.

And as of this morning, it looks like the levy might just pass and become law in Australia. All parties support the idea. Which means that Australia might just have a tax on bank deposits starting January 1, 2016.

….continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair