Stocks & Equities

Although China’s economy has been leading the world in annualized growth since the days that mobile phones had retractable antennas, there have always been some aspects of the country’s commercial and financial system that loudly broadcast the underlying illogic of a Communist Party’s firm control of burgeoning capitalism. China’s stock markets were one such venue where things just didn’t add up…literally.

Although China’s economy has been leading the world in annualized growth since the days that mobile phones had retractable antennas, there have always been some aspects of the country’s commercial and financial system that loudly broadcast the underlying illogic of a Communist Party’s firm control of burgeoning capitalism. China’s stock markets were one such venue where things just didn’t add up…literally.

In recent days, the stock market in Hong Kong has rocketed upward, notching the kinds of gains that have inspired many market observers to warn of a dangerous bubble forming. But as we see it, the rise is not the result of an unfounded mania gone wild, but the logical outcome of a deliberate regulatory push from Beijing to allow Chinese markets to function the way markets do in the developed world. In other words, this is not a bubble rally but a move towards normalization.

Until late last year China’s stock markets have been regulated with two very different customer bases in mind, creating two very different price structures. Foreign buyers have been allowed to buy shares on the Hong Kong stock exchange but have been prohibited from buying on the Shanghai exchange. On the other hand, domestic Chinese buyers were prohibited from buying in Hong Kong, but could buy in Shanghai. This meant that the two markets were subject to very different supply and demand dynamics, and very different price trajectories.

Foreign interest was subject to a variety of inputs that did not concern local investors: The strength of overseas markets and economies, the global interest rate environment, opinions about the strength of the Chinese economy, the foreign exchange market, and countless other factors. Chinese buyers were more influenced by the domestic economy, financial regulatory incentives, the local real estate market (which for many years was the investment of choice for the growing middle class), and the movements in gold (another popular investment alternative for rank and file Chinese). This created a tale of two markets, with performance of the Shanghai and Hong Kong markets diverging wildly over the years. The dynamic was most easily observed in the relative valuations of companies that listed themselves in both markets. These dual-listed companies were often assigned one valuation in Shanghai and a very different valuation in Hong Kong. Normally such gaps would create an “arbitrage” opportunity for investors to close the gap. But the strict financial regulations in China prevented such normalization. That is until recently.

For much of the early years of the last decade, when the Chinese economy was in the midst of a spectacular wave of growth, and many Chinese citizens began to buy stocks for the first time, much of the outsized appreciation occurred in Shanghai. By 2007, dual-listed stocks traded at a premium in Shanghai over Hong Kong. But the market crash of 2008 hit Shanghai shares far harder. Perhaps disillusioned by the losses, or perhaps attracted to opportunities in the property market, Chinese investors pulled out, sending Shanghai into a seven-year bear market. Over that time, Hong Kong largely held steady, and so by 2014 dual-listed companies traded at a significant premium there.

However, even with the relative strength of Hong Kong, Chinese market performance over the last seven years has been dismal in comparison to the West, even though Chinese economic growth continues at a rate that far surpasses the developed world. For example, the United States has seen its stock market double in the years since the depths of 2009, while delivering average annual GDP growth of just under 1.2%.

In many ways the performance of financial markets has seemed to eclipse the health of the underlying economy as the true test of global leadership. With this sore spot in mind, the new regime of Chinese leaders that took position in 2013 and 2014, led by General Secretary Xi Jinping and Premiere Li Keqiang, seemed determined to take energetic action to level the financial playing field between East and West.

The most significant change they have implemented thus far has been the Shanghai-Hong Kong Stock Connect, which takes major steps to open up the barriers that have segregated China’s market structure. The provisions will greatly increase the ability for Chinese to buy in Hong Kong and for foreigners to buy in Shanghai. The reforms also change banking regulations and interest rate structures in a way that should incentivize Chinese citizens to take savings out of the bank and invest in shares. It is hoped that these moves will finally give China a stock market that mirrors its economy.

The reforms seemed to have had their intended effect. Beginning late last year, China’s investor class finally began embracing shares, pulling the Shanghai market out of its seven-year dive. The exchange powered up 90% in just six months. Clearly, the action is getting a little frothy. It has been reported that in March alone, Chinese investors opened more than 4.8 million stock trading accounts, a boom of historic proportions. The pace has kept up, with an additional 1.5 million accounts opened in the first week of April (the Chinese government now allows citizens to hold up to 20 separate accounts).

It is assumed that the new interest in shares has been helped by a slowdown in Chinese residential real estate, which had come to be the single greatest focus of the typical Chinese investment portfolio. Having cashed out of property (and to a lesser extent gold), many Chinese turned their attention to the beaten down Shanghai exchange.

At the end of the recent rally, Shanghai shares traded over 16 times earnings, a premium to the Hong Kong Index, which traded at just over 13 times earnings. When the Connect program finally allowed the Chinese into Hong Kong late last month, many Chinese finally jumped in to close this arbitrage, sending Hong Kong up to a seven-year high, finally eclipsing the pre-crash high. (In contrast, the S&P 500 is currently 35% higher than its pre-crash high.) The Hang Seng in Hong Kong rose a blistering 15% in the month between mid-March and mid-April. In this sense, it should be clear that Main Street Chinese investors are finally holding the whip, not the hot foreign money that had been the primary river of Hong Kong performance in years past.

Many have speculated that this current mania is a dangerous flash in the pan that will burn investors who arrive late to what they believe will be a short-lived party. But it’s important to realize two things that should give the rally legs. One is regulatory and the other fundamental.

While the Connect laws have greatly liberalized the ability to buy stocks anywhere in China (which by law must now be settled in RMB), a quota system remains in place to keep the lid on purchases. At present, evidence suggests that the bottleneck has kept the pace below where it would be in an unrestricted market. So far, the maximum quota has been hit every day since the Connect regulations went into effect that allow the Chinese to buy in Hong Kong. This suggests that the demand from Chinese investors has only just begun to be realized. Hong Kong should stay strong as long as it’s being pulled upward by a surging Shanghai.

While Western news outlets loudly proclaim the “death rattle” of the Chinese economy (which appears set to slip below 7% – my God how awful!), it is important to realize just how superior that growth rate remains above the moribund West. In China, 7% is described as anemic, whereas in the U.S. 3% is described as booming (although 3% growth in America is looking to be increasingly unlikely). Even if the Chinese markets, which still have plenty of catch-up to do with the West, can capture a portion of this strength, investors could be rewarded for years to come.

The moves also show how the markets in China have been hindered by regulation. The removal of these barriers has revealed hidden strengths. In contrast, U.S. markets have been helped by robust Fed policies designed to keep money flowing into stocks at all costs. Remove these pro-stock monetary incentives, and the possible crash here in the U.S. could become the opposite of the current rally in China.

Falling oil prices might have been last year’s big story. But 2015 is all about the greenback.

After all, the U.S. dollar’s reach is bigger than just the commodity markets. (But we will look at its impact on gold and oil in just a few moments.)

The thing is, you can’t talk about global growth, inflation, interest rates or corporate earnings without taking the buck into account.

And with the U.S. Dollar Index up 25% since last summer, we have about 9 trillion reasons why the “almighty dollar” affects everything we do … and how we invest.

Since 2009, roughly $9 trillion in dollar-denominated debt has been issued in foreign branches of U.S. banks or in foreign banks.

With a dollar that is worth about 25% more, those loans and interest rates have also increased by 25%.

Think about this …

A $1 million loan at 10% has increased to about $1.25 million. And the interest rate has essentially increased to about 12.5%.

These loans have to be paid back in full. But if slow economic growth around the world would result in a global recession, we could see a rise in defaults.

After all, other currencies haven’t risen in tandem with the dollar. Nor has the dollar increased 25% against these currencies.

The dollar has risen relative to most of them.

The U.S. Dollar Index reflects the dollar’s exchange value against a basket of our trading partners’ currencies — the euro, British pound, Canadian dollar, Mexican peso, Chinese yuan, Australian dollar and others.

It’s important to note that the dollar has appreciated against some currencies more than others.

For example, according to the map above, the greenback is up 31% against the euro, but down 0.08% against the Chinese yuan.

Why the Greenback Has Gained

The dollar has rallied more than 40% off its low of 70 made in 2008.

The greenback was range-bound between 2008 and 2014. The rally picked up speed last December.

It consolidated the move in February before accelerating again.

Take a look at the PowerShares DB U.S. Dollar Bullish ETF (UUP):

There are plenty of reasons for the dollar’s rise: QE ending, stronger economic growth and speculation about rising interest rates.

On top of that, we are attracting foreign capital because of better economic growth than many other countries. This adds to the safety and liquidity of the dollar.

However, there is one other factor.

As we saw when oil was falling, it looks like the futures market is driving prices.

Only in the greenback’s case, it appears to be driving them higher.

Big Bets on the Buck

Keep in mind that the $9 trillion in dollar-denominated debt is held by borrowers outside the United States.

Dollar-denominated deposits at banks outside the U.S. are known as Eurodollars. That’s because many are held in Europe, where they are generally free of regulation.

Below is a table from Barron’s that shows the activity of the Eurodollar futures market.

The Eurodollar saw the most contracts traded during the last week of March, compared to gold and oil.

I’ve circled where large speculators were long 1.7 million contracts. At the same time, small traderswere short nearly 1.3 million.

But that’s not where the biggest action is.

Before we get to it, keep in mind that the futures market has a couple of key functions:

• To shift the risk from producers to risk-takers

• To set asset prices for buyers and sellers

If you look at the above table, most of the contracts belong to commercial hedgers, as they try to reduce their price and currency risk.

Here, we can see 6 million long and 6 million short contracts.

How Much Higher Could the Dollar Go?

Here’s a quick lesson on dollar futures. If the price of the U.S. Dollar Index is at 100, then the futures contract is worth about $100,000.

The Dollar Index traded at 98.7 yesterday. So that would put it at roughly $98,700. (Simply multiply $1,000 times the index value.)

The margin requirement is only about $1,950. So, this tremendous leverage attracts speculators.

Large speculators, deemed as the “smart money,” have more long contracts. Also long contracts have increased, and the shorts decreased.

Speculators and traders dominate the rest of the futures markets due to significant leverage in that area.

So, these aren’t investors driving the prices. Rather, traders are taking advantage of the large leverage that the futures market offers.

On the charts, there is overhead resistance at 100.

If the dollar can break above it, we could see it rally to 105. This would match its highs in the 1990s.

It’s possible that speculators could drive the dollar above 105, but my research tells me that the dollar would be overvalued if this happens.

The Benefits of a Strong U.S. Dollar

A strong dollar is a good thing for consumers as it makes foreign goods and services cheaper.

For example, if you want to take a vacation to Europe, now might be a good time. That’s because it’s about 30% cheaper to do now than it was in 2013.

However, you probably don’t have to rush to book that trip.

That’s because domestic producers and service providers will have to keep prices lower to compete against cheaper foreign goods and services.

This should keep a lid on U.S. inflation and, therefore, interest rates.

In fact, studying the Fed’s every word isn’t the only way to determine its direction on raising interest rates.

In their last news conference, Federal Open Market Committee members said they would be cautious about raising rates.

They understand the potential disruptions the strong dollar could have on the global economy, including dollar-denominated loans.

Why a Strong Buck is Bad for Blue-Chips

However, a strong dollar can be bad news for U.S. blue-chips that do big business overseas.

After all, foreign buyers will need more of their home currency to buy U.S. goods and services.

The stronger dollar and higher-priced U.S. goods and services should lead to weaker sales.

What’s more, U.S.-international companies face a currency conversion loss that happens when a weaker foreign currency sale needs to be converted into a stronger dollar.

With Q1 earnings season starting to pick up momentum, we will soon start to see the effects of the stronger dollar on U.S. multinationals.

What a Strong Dollar Does to Gold

Last but not least, a strong dollar could hurt gold and oil recovery in the short run.

In the Yahoo! Finance chart above, year-to-date UUP (the top pink line) has gained 8.45%. Meanwhile the SPDR Gold Trust (GLD), center blue line, has only added 0.78%. And the U.S. Oil Fund (USO), the bottom red line, is down 7.39%.

When it comes to the dollar-oil relationship, it is an overstated one. Even though the dollar is stronger than the euro by about 30%, oil prices are down about 50%.

In other words, the drop in oil prices is greater than the appreciation of the dollar. So, the dollar shouldn’t affect demand.

As for gold, if the dollar moves above 105, gold could make new lows.

Remember, the all-in cost for gold is about $1,100. Below that price, producers will probably cut production and supply and demand can eventually achieve equilibrium and price stability.

As for the dollar, the futures market and many others suggest it can head higher from here.

My take is that the latest rally has been almost parabolic. This type of move is generally not sustainable when the U.S. doesn’t have a major economic trend like the Internet boom to boost growth and wealth.

However, I’m going to keep a close eye on the futures markets. If the “smart money” is going long the dollar here in the short term, it may be a good bet that other money is going to follow.

Good Investing,

Dan Hassey

#10. IGM Financial Inc (TSE:IGM.CA) — 4.9% YIELD

At #10, IGM Financial is engaged in the provision of financial services. Co.’s Investors Group segment provides financial and investment planning services to Canadians through its network of consultants across the country. Co.’s Mackenzie segment is engaged in the provision of investment advice and related services offered through investment applications, distributed through channels focused on independent financial advice. Co.’s Corporate and Other segment includes net investment income earned on unallocated investments and other income, operating results for Investment Planning Counsel as well as inter-segment eliminations. As of Dec 31 2010, Co. had total assets of C$8,892,563.

![]()

When oil prices fell out of bed last winter there was much hand-wringing over the fate of the former beneficiaries of high-priced crude. Trillions of dollars of junk bonds issued by frackers, for instance, might default, oil field services companies could fail, and layoffs in the oil patch might swamp the nascent employment recovery.

When oil prices fell out of bed last winter there was much hand-wringing over the fate of the former beneficiaries of high-priced crude. Trillions of dollars of junk bonds issued by frackers, for instance, might default, oil field services companies could fail, and layoffs in the oil patch might swamp the nascent employment recovery.

Some of this has happened, though not on the apocalyptic scale the worst-case scenarios suggested. More might be coming, but right now it’s not headline news in North America.

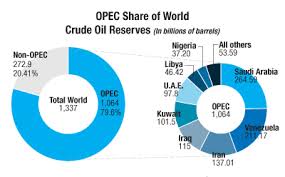

For OPEC, however, the sudden 50% diminution in export revenue is a clear and present danger, and the response is noteworthy:

Oil-Rich Nations Are Selling Off Their Petrodollar Assets at Record Pace

Now that oil prices have dropped by half to $50 a barrel, Saudi Arabia and other commodity-rich nations are fast drawing down those “petrodollar” reserves.

In the heady days of the commodity boom, oil-rich nations accumulated billions of dollars in reserves they invested in U.S. debt and other securities. They also occasionally bought trophy assets, such as Manhattan skyscrapers, luxury homes in London or Paris Saint-Germain Football Club.

Now that oil prices have dropped by half to $50 a barrel, Saudi Arabia and other commodity-rich nations are fast drawing down those “petrodollar” reserves. Some nations, such as Angola, are burning through their savings at a record pace, removing a source of liquidity from global markets.

If oil and other commodity prices remain depressed, the trend will cut demand for everything from European government debt to U.S. real estate as producing nations seek to fill holes in their domestic budgets.

“This is the first time in 20 years that OPEC nations will be sucking liquidity out of the market rather than adding to it through investments,” said David Spegel, head of emerging markets sovereign credit research at BNP Paribas SA in London.

Saudi Arabia, the world’s largest oil producer, is the prime example of the swiftness and magnitude of the selloff: its foreign exchange reserves fell by $20.2 billion in February, the biggest monthly drop in at least 15 years, according to data from the Saudi Arabian Monetary Agency. That’s almost double the drop after the financial crisis in early 2009, when oil prices plunged and Riyadh consumed $11.6 billion of its reserves in a single month.

In Angola, reserves dropped last year by $5.5 billion, the biggest annual decline since records started 20 years ago. For Nigeria, foreign reserves fell in February by $2.9 billion, the biggest monthly drop since comparable data started in 2010.

Algeria, one of the world’s top natural gas exporters, saw its funds fall by $11.6 billion in January, the largest monthly drop in a quarter of century. At that rate, it will empty the reserves in 15 months.

Excluding Iran, whose sales are subject to some sanctions, members of the Organization of Petroleum Exporting Countries are expected to earn $380 billion selling their oil this year, according to U.S. estimates. That represents a $350 billion drop from 2014 — the largest one-year decline in history.

“The shock for oil-rich countries is enormous,” Rabah Arezki, head of the commodities research team at the IMF in Washington, said in an interview.

Oil-rich countries will sell more than $200 billion of assets this year to bridge the gap left between high fiscal spending and low revenues, Spegel said.

Good, Bad, or Irrelevant?

When a central bank wants to tighten monetary policy, it sells bonds from its portfolio to investors in return for cash. That shrinking supply of spendable funds slows the economy down, moderates inflation — and frequently causes a recession.

Saudi Arabia selling bonds has exactly the same effect, but on a global scale, depending on which bonds are being sold for which currency. So the projected $200 billion of annual asset sales by oil exporters will be a modest (compared to US, Japanese or European QE programs) tightening of world monetary policy, other things being equal.

In ordinary times this would push interest rates up a bit. But with central banks and their unlimited currency creation machines now dominating the market it may not make much of a difference.

And in a perverse way these bond sales provide more liquidity to a tight part of the market. It seems that central banks have been buying up all the high quality debt in the global financial system, leaving pension funds and bond funds that need such paper unable to get enough of it (an astounding situation when you think about it: Governments around the world are borrowing trillions of dollars each year but there’s not enough of that debt to satisfy pension funds). See The Worldwide Deficit of High-Quality Debt.

So, a non-event? Let’s not go that far. Oil exporting countries have designed their budgets around the assumption of much higher oil revenues. And many of them have failed to diversify their economies and create entrepreneurial cultures for the day when the oil is gone. So if prices stay low for a few more years they’ll start to run out of reserves, default on their debt, etc., etc. Maybe that’s the oil market black swan that we should be worried about.

Globally, water demand is threatening to dangerously outpace supply, while in the US, dry states such as Texas and California are suffering from shortages and the future forebodes more suffering. For the North American shale boom, the lack of water is suffocating. Amid this doom and gloom, a water revolution emerges, led by energy industry figures who realized the endless potential of tapping into new water sources and processing them with advanced desalination technology that, for the first time ever, is economically feasible.

Globally, water demand is threatening to dangerously outpace supply, while in the US, dry states such as Texas and California are suffering from shortages and the future forebodes more suffering. For the North American shale boom, the lack of water is suffocating. Amid this doom and gloom, a water revolution emerges, led by energy industry figures who realized the endless potential of tapping into new water sources and processing them with advanced desalination technology that, for the first time ever, is economically feasible.

The water revolution is here, according to Stanley Weiner, CEO of STW Resources-a Texas-based company that has the exclusive North American license for Dutch-developed next generation Salttech desalination technology.

In an interview with James Stafford Oilprice.com, Weiner discusses:

• The new technology behind the water revolution

• How communities in Texas can be spared drought

• Advancements that finally make desalination commercially viable

• How it’s already working-and where

• How we can turn toilet water into tap water

• What it means for the oil and gas industry

• How vital water is to energy independence

• How much oil and gas companies can save with new desalination systems

• The next phase of the water revolution

• Why everyone can finally benefit from conservation

James Stafford: A global study warns that by 2030 demand for water will outstrip supply by 40%. What are we facing in the US alone?

Stanley Weiner: The situation can only be described as extremely urgent. We’re looking at continual drought and predictions of a new ‘mega drought’ for Texas. The current drought started in 2010, and it’s still in play. In the meantime, we’re seeing a lot of new people moving into Texas, as well as industry, and they all need water that they don’t have.

California is running out of water. A NASA scientist has recently warned that California has only about one year’s worth of water left in storage, while its groundwater is rapidly depleting. According to scientists, 40% of the state is undergoing an ‘exceptional drought’-the most severe it has seen in 1,200 years. Earlier this month, California Governor Jerry Brown issued the state’s first-ever mandatory water restrictions. It sounds apocalyptic because it is, even if we don’t feel it immediately.

And a dry California is a disaster for the entire US. California is our breadbasket-where more than one-third of our vegetables come from and some two-thirds of our fruits. What it means immediately is higher food prices across the US. It’s not enough anymore to think that if you don’t live in a dry state you won’t be affected. The water crisis affects us all in many ways. Parts of Oklahoma are hard hit by drought. Drought conditions have intensified in Nevada and Utah, and Arizona is facing a similar problem to California-it’s growing thirstier by the day.

Water is behind every single sector of our economy and our way of life. It’s more valuable than oil because at the end of the day, there is no oil without water. It’s important that everyone understands that finding a solution for our growing water crisis is hands-down the most important endeavor of our time-from both a human and an industrial standpoint.

James Stafford: Ok, so where do we stand today in terms of new technology that can address urgent water supply issues on a global level?

Stanley Weiner: Until recently, new technology that could realistically address urgent issues of water supply around the world had been relegated to the realm of science fiction. Even though the technology has existed and was continually advanced, it was unfeasible on a commercial scale-until now.

So what we’re seeing today is a breakthrough that is far more significant than the technological advancements in horizontal drilling and hydraulic fracturing that ushered in the shale revolution. Today, we can provide a solution to droughts; we can provide dry communities with more drinking water than they ever could have imagined-and we can prop up the shale boom by providing drillers with more sources of water, ultimately leading to America’s energy independence. We can also economically recycle the water they use in the process.

James Stafford: What you’re describing is no less than a water revolution, then?

Stanley Weiner: Absolutely. This is a revolution, and it’s only just emerging, so we can expect a lot of technological advancements along the way to make desalination even more efficient and cost-effective. But there is no turning back now.

On the desalination front, Netherlands-based Salttech has developed breakthrough technology called Salttech DyVaR, for which STW has the exclusive license in North America. Salttech is a think tank with brilliant engineers and scientists who are always asking how they can make it better. After such a long time trying to bring feasible desalination technology to the world, this is finally the game changer.

Everything is connected to everything else-that’s the first message to be heard loud and clear from this emerging ‘water revolution’. Tighter environmental regulations have expanded the market for companies that encompass not only the use of ‘green’ technology, but also of ‘blue’, or clean water technology. But there’s a third color here that is just as important, and we’ll call it black, which means it has to make sense economically. Until now, desalination technology has been too expensive, with projects operating in the red, rendering them economically unfeasible on a commercial scale. ‘Blue’ technologies have also until now not been ‘green’ enough to make sense for the environment.

James Stafford: Ok, so first take us through what this next-generation desalination technology is capable of …

Stanley Weiner: First off, this is largely mobile technology, so it’s easy to set up in all kinds of venues and to move around, which also contributes to cost-effectiveness, but it can also be a fixed facility situation. What it does is this: It takes dirty water and turns it into potable water using vaporization. It can clean up the oil industry’s frack flowback water and the dirty water produced by oilfields, and it can also desalinate ocean water.

James Stafford: And how does it work, exactly? There has been a lot of talk lately about thermal distillation using Dynamic Vapor Recompression (DVR), but for the layman, what does this mean?

Stanley Weiner: OK, yes, DVR is a key aspect of the Salttech desalination system. DVR is a new type of mechanical vapor recompression-which is the process of evaporating water at moderate temperatures through the use of a vacuum and then condensing it in a higher-pressure chamber. The heat of condensation is transmitted to the influent stream through a heat exchanger. All of this requires very little energy compared to conventional process that rely on “flash distillation” and large amounts of energy. Where the term “dynamic” comes into play in the DVR is in relation to the use of a cyclone during the evaporation process. This cyclone separates the crystallized salts from the brine by centrifugal force.

James Stafford: On a ‘green’ level, how is this new generation technology different? What makes it actually ‘green’?

Stanley Weiner: The key aspect of this technology is what we call zero liquid discharge (ZLD). All these ‘permanent’ desalination plants that are being put up around the world-including nine just in Texas and one in Carlsbad, California-are harming the fragile ecosystem of our oceans and waterways. They can’t process more than 35-50% of the water in the desalination process, and what they don’t process into potable water is rejected back into the ocean in the form of harmful liquid discharges. Studies have found that if they are processing 50 million gallons a day, they are putting 25 million gallons of harmful liquids back into the ocean. The studies are frightening, and they will impinge on the ability of these plants to get permits to keep feeding reject liquids back into the waterways. In Israel, for instance, there are contracts to build these permanent desalination plants, but now it looks like the permits aren’t going to come through.

James Stafford: So how does the Salttech system avoid rejecting harmful liquids back into the waterways?

Stanley Weiner: First, this new technology processes around 97% of the water, so there’s much less rejected. Second, the 3% or so that it can’t process, it turns into a solid, so there is zero liquid discharge. And there are no chemicals used in the process whatsoever. Let me put it this way: the ‘permanent’ desalination plants are discharging 50-65% of what’s rejected in the process in the form of a waste stream of highly concentrated brine liquid-directly into the oceans. The new mobile technology, developed by the Dutch, discharges its 3% reject in the form of solid salts and minerals, so there is no harmful discharge into waterways and no disposal problem. Importantly, this means there is no need for deep well waste water injections, evaporation ponds and other recognized methods for disposing of concentrated brine waste from desalination activities.

James Stafford: How do the costs compare with conventional desalination technologies?

Stanley Weiner: Typically, the price of desalinated oilfield water projects has hovered around $4-$8 per barrel, but Salttech makes it possible at around $1.50-$2.00 per barrel. To process brackish or seawater, the cost is about $1,100-$1,350 per acre-foot of water. These prices make fresh water economically available for everyone who needs it.

James Stafford: How important is water to the overall energy equation?

Stanley Weiner: It’s absolutely a vital part of the energy equation. Water is what enables the US to drill more oil and gas wells and to wean itself off of foreign oil and reduce vulnerability to geopolitical whims.

James Stafford: Is there a point at which the energy industry-one of the bigger consumers of water itself-can actually contribute to the solution rather than the problem?

Stanley Weiner: Oilfield water use represents much less than people think: It’s only about 3% of total fresh water consumed. For 2005, most of the fresh-surface-water withdrawals-about 41%–were used in the thermo-electric power industry to cool electricity-generating equipment. Water used in this manner is most often returned to the water body from which it came. That is why the more significant use of surface water is for irrigation-in the agricultural sector-which uses about 31% of all fresh surface water. Ignoring thermoelectric-power withdrawals, irrigation accounted for about 63% of the US’ surface-water withdrawals. Public supply and the industrial sector were the next largest users of surface water. However, the energy industry can still contribute to the solution in a significant way through water reclamation. Just like we drill for new oil and gas, we can drill for new sources of water deep underground and tap into water resources that were never before accessible for potable water.

James Stafford: Where can we find new sources of water and how do we tap into them?

Stanley Weiner: The new sources of water aren’t really new at all-they’ve always been there; we just didn’t have the economically viable technology to tap into them on a commercial scale. These sources include the ocean, brackish water from reservoirs deep underground and municipal wastewater, which will be tapped into using our toilet-to-tap technology.

James Stafford: What will the next advancement in desalination technology be that will render it even more economically rewarding?

Stanley Weiner: Now that it’s already commercially viable, the next step will be to lower the energy costs even further with wholesale solar, wind and geothermal power. In fact, the first desalination plant already in operation in Mentone, Texas, is entirely run on solar power and is providing the city of Mentone with as much drinking water as it could ever want.

James Stafford: This technology was first deployed in Mentone, Texas?

Stanley Weiner: Yes. This is where it really all started in July last year-in this small town in the Permian Basin. This was a highly successful pilot project that is now providing residents with all the drinking water they need. And, as I mentioned before, the entire operation is run on solar power. It was this system that convinced me of the viability of licensing it and commercializing it to make water available to everyone in need of it.

But Mentone was just the genesis of this water revolution. The desalination project in Fort Stockton-also in Texas-is much larger. Right now, in Fort Stockton’s Capitan Reef Aquifer we are drilling our first production well, and will be drilling several additional wells here and in other brackish aquifers. We’re drilling to new water sources about 2,000-4,500 feet under the surface, to tap into as much as 14 million acre-feet of new water-or about 5.6 trillion gallons. In the second quarter of this year we will start selling that water. The beneficiaries will be several west Texan municipalities suffering from drought.

James Stafford: What about the oil and gas industry? Are they jumping on this water revolution bandwagon yet?

Stanley Weiner: Our pilot project in the Permian Basin has definitely attracted the attention of oil and gas companies who are hurting for water supplies and struggling with low oil prices and thus have problems justifying costs. You have to understand that Texas is both a highly competitive playing field for oil companies-with the sleeping giant that is the Permian Basin and the prolific Eagle Ford shale-but it is also water starved. So the competition for water resources is just as competitive as the competition for oil and gas licenses. There is also a great deal of competition among industries who are heavy users of water. With the advent of hydraulic fracturing-which uses exponentially more water-this competition has grown even fiercer. Demand for water is soaring, and now we can meet that demand. Over half of the 40,000 wells Americans have drilled since 2011 have been in areas of drought, and in total these wells have used 97 billion gallons of water.

Over the next six to nine months, we will be launching another major desalination project for an NYSE-listed oil and gas company-so the word is out.

James Stafford: Specifically, how much money could oil companies potentially save in Texas’ Permian Basin or Eagle Ford using this technology?

Stanley Weiner: The numbers are actually fantastic: They could save approximately $150,000+ per well using this desalination technology.

James Stafford: What is the future of water reclamation and desalination? Where do you see the technology going over the next 5-10 years? Where is there room for improvement?

Stanley Weiner: Advancements will continue but improvements will always be about the bottom line, making it cheaper and more economical to use. It can only get cheaper and more efficient at this point. Listen, we used to think fresh water was endless, and we squandered it. Not any longer. Now we need to squeeze every drop out of brackish reservoirs and oceans desalination operations. There is no turning back the tide now. It’s already the new ideal: The technology uses no chemicals or filtration and requires very little power, and at the end of the process you have clear, fresh water. The revolution has begun.

James Stafford: So at the end of the day, from an investor’s perspective, the water revolution could outshine the financial glitz of the shale revolution?

Stanley Weiner: You know, when we initially set up shop with STW, we were simply planning on targeting frack water in the oil business. We didn’t see further than that. It didn’t occur to us that there were endless possibilities for actually accessing and processing water that no one would have thought could be for human consumption. Once we realized the potential here-the potential that goes so far beyond the oil and gas industry-our goals became clearer. We can provide water not only to the oil and gas industry and to every other industry, but to municipalities in dry states; to communities. There is a great deal of money to be made in what amounts to conservation at the end of the day, and for once it can be made without harming the environment. That is exactly what is revolutionary about it. Everyone benefits.

James Stafford: What’s the bigger picture here?

Stanley Weiner: This is all about conservation, and the first chance we have seen where it is possible to actually make money on conservation. If a project can be energy efficient-such as the pilot Salttech project in Mentone, Texas, which is run entirely on solar power-and can process vastly more than it rejects, then we are talking about conservation. We are wasting our precious fresh water resources every minute of every day when we could be reusing it. Everyone needs to realize that water is our most precious commodity and it needs to be conserved in every way possible.

Source: http://oilprice.com/Interviews/The-Game-Changing-Water-Revolution-Interview-with-Stanley-Weiner.h

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair