Bonds & Interest Rates

The law of unintended consequences is becoming ever more prominent in the economic sphere, as the world becomes exponentially more complex with every passing year. Just as a network grows in complexity and value as the number of connections in that network grows, the global economy becomes more complex, interesting, and hard to manage as the number of individuals, businesses, governmental bodies, and other institutions swells, all of them interconnected by contracts and security instruments, as well as by financial and information flows.

It is hubris to presume, as current economic thinking does, that the entire economic world can be managed by manipulating one (albeit major) subset of that network without incurring unintended consequences for the other parts of the network. To be sure, unintended consequences can be positive or neutral or negative. This letter you are reading, which I’ve been writing for over 15 years and which reaches far more people than I would have ever dreamed possible, is partially the result of a serendipitous unintended consequence.

But as every programmer knows, messing with a tiny bit of the code in a very complex program can have significant ramifications, perhaps to the point of crashing the program. I have a new Microsoft Surface Pro 3 tablet that I’m trying to get used to, but somehow my heretofore reliable Mozilla Firefox browser isn’t playing nice with this computer. I’m sure it’s a simple bug or incompatibility somewhere, but my team and I have not been able to isolate it.

However, that’s a relatively minor problem compared to the unintended consequences that spill from quantitative easing, ZIRP, and other central bank shenanigans. We have discussed the problem of how the Federal Reserve has pushed dollars on the rest of the world and is playing havoc with dollar inflows and outflows from emerging markets. More than one EM central banker is complaining aggressively.

My good friend Dr. Woody Brock makes the case that an unintended consequence of QE is that the Federal Reserve’s normal transmission of monetary policy through periodic changes in the fed funds rate has been vitiated. He contends that soon we will no longer care about the fed funds rate and will be focused on other sets of rates.

My good friend Dr. Woody Brock makes the case that an unintended consequence of QE is that the Federal Reserve’s normal transmission of monetary policy through periodic changes in the fed funds rate has been vitiated. He contends that soon we will no longer care about the fed funds rate and will be focused on other sets of rates.

This is an important issue and one that is not well understood. Woody has given me permission to reproduce his quarterly profile. For Woody, this is actually a fairly short piece; but as usual with Woody’s work, you will probably want to read it twice.

Woody is one of the most brilliant economists I know, and I make a point of spending time with him as our schedules permit. We are making plans to get together at his Massachusetts retreat in August. He is restructuring his business in order to spend more time writing and less time traveling, and he intends to lower the price of his subscription. It will still be pricey for the average reader, but for funds and institutions it should be a staple. You can find his website at www.SEDinc.com or email him at SED@SEDinc.com.

Before we go to Woody’s letter, if you’re going to be at my conference this coming week, you’ve already made arrangements. I know a lot of people wanted to go but just couldn’t work it into their schedules. I won’t say it’s the next best thing to being there, but you can follow me on Twitter, where my team and I will be sending out real-time tweets about the important ideas and concepts we are hearing, not just from the speeches but from all the conversations that spring up during the day and late into the evening. If you’re curious as to who will be there, here’s a page with the speakers. If you’re at the conference, look me up.

The Fed Funds Rate: R.I.P. ‒ The Third and Final Transformation of Monetary Policy

By Woody Brock, Ph.D.

Strategic Economic Decisions, Inc.

The policy announcements of the US Federal Reserve Board are dissected and analyzed more closely than any other global financial variable. Indeed, during the past thirty years, Fed‐Watching became a veritable industry, with all eyes on the funds rate. Within a few years, this term will rarely appear in print. For the Fed will now be targeting two new variables in place of the funds rate. One result is that forecasting Fed policy will be more demanding.

To make sense of this observation, a bit of history is in order. During the last nine years, US monetary policy has been transformed in three ways. To date, only the first two have been widely discussed and are now well understood. The third development is only now underway, and is not well understood at all. To review:

First, the Fed lowered its overnight Fed funds rate to essentially zero, not only during the Global Financial Crisis of 2008–2009, but throughout nearly six years of economic recovery thereafter. The average level of the funds rate at the current stage of recovery was about 4% during the past dozen business cycles. It was never 0% as it is in this cycle. In past essays, we have argued that this overutilization of “ultra‐easy monetary policy” reflected the failure of the government to utilize fiscal policy correctly (profitable infrastructure spending with a high jobs multiplier), and to introduce long‐overdue incentive structure reforms. It was thus left to monetary policy to pick up the pieces after the global crisis of 2008. This development was true in most other G‐7 nations, not just in the US.

Second, the Fed inaugurated its policy of Quantitative Easing whereby it increased the size of its balance sheet five‐fold from $900 billion to $4,500 billion. Such an expansion would have been inconceivable to Fed watchers during the decades prior to the Global Financial Crisis. In the US, QE is now dormant, and the only remaining question (answered below) is how and when the Fed will shrink its bloated balance sheet back to more normal levels.

Third, the way in which the Fed conducts standard monetary policy (periodic changes in the funds rate) is currently undergoing a complete makeover. In particular, the traditional tool of changing the funds rate via Open Market operations carried out by the desk of the New York Fed no longer works. For as will be seen, the vast expansion of the size of its balance sheet (bank reserves in particular) has rendered traditional policy unworkable. From now on, therefore, the Fed will conduct monetary policy via two new tools that were not even on the drawing board of the Fed prior to 2008.

Summary: In this PROFILE, we explain in Part A why traditional (non‐QE) monetary policy has been vitiated by QE. In Parts B and C respectively, we discuss the two new tools that will be used in the future to conduct standard (non‐QE) monetary policy: what exactly are these tools, and how do they work? In Part D, we discuss why these new tools will not be required by the European Central Bank, which has a different institutional structure than the US Fed. Finally, in Part E, we turn to QE and discuss when and how the Fed will shrink its balance sheet back to a more traditional size in the years ahead.

In this write‐up, we largely rely on the remarks set forth in a recent paper by Fed Vice Chairman Stanley Fischer, formerly chief economist of the IMF, Governor of the Central Bank of Israel, and professor of economics at MIT. We also benefitted from clarifications by Professor Benjamin Friedman at Harvard University.

Part A: So Long to Setting the Funds Rate via Open Market Operations

Prior to the financial crisis, bank reserve balances with the Fed averaged about $25 billion. With such a low level of reserves, a level controlled solely by the Fed, minor variations in the amount of reserves via Fed open market sales/purchases of securities sufficed to move the Fed funds rate up or down as desired. Analytically, the market for bank reserves (Fed funds) consisted of a demand curve for bank reserves reflecting the nation’s demand for loans, and a supply curve reflecting the supply of reserves by the Fed. The so‐called Fed funds rate is the point of intersection of these two curves (the interest rate). If the Fed targeted, say a 2% funds rate, it achieved and maintained this rate by shifting the supply curve left or right by adding to/subtracting from the quantity of reserves. As the Fed was a true monopolist in the creation/extinction of reserves, it could always target and sustain any funds rate it chose.

These operations constituted “monetary policy” for many decades. But this is no longer the case, as was first made clear in a FOMC policy pronouncement of September 2014. To quote Dr. Fischer in his 2015 speech, “With the nearly $3 trillion in free bank reserves (up from pre‐crisis reserves averaging $25 billion), the traditional mechanism of adjustments in the quantity of reserve balances to achieve the desired level of the Federal funds rate may not be feasible or sufficiently predictable.” What new mechanisms will replace it? There are two.

Part B: The Use of Interest Rates Paid by the Fed on Free Bank Reserves

“Instead of the funds rate, we will use the rate of interest paid on excess reserves as our primary tool to move the Fed funds rate.” The ability of the Fed to pay banks an interest rate on their free reserves dates back to legislation of October 2008. This rate has been set at 0.25% during the past few years. (“Excess” or “free” bank reserves are defined as the arithmetic difference between total reserves and required reserves. Currently, as of March 30, required reserves were $142 billion, and total reserves were $2.79 trillion.)

The Logic: Whatever the level of the reserve interest rate that the Fed chooses, banks will have little if any incentives to lend to any private counterparty at a rate lower than the rate they can earn on their free reserve balances maintained at the Fed. The higher the reserve remuneration rate is, the greater will be the upward pressure on a whole range of short‐term rates.

Part C: The Use of the Reverse Repo Rate

“Because not all institutions have access to the excess reserves interest rate set by the Fed, we will also utilize an overnight reverse repurchase purchase agreement facility, as needed. In a reverse repo operation, eligible counterparties may invest funds with the Fed overnight at a given interest rate. The reverse repo counterparties include 106 money market funds, 22 broker‐dealers, 24 depository institutions, and 12 government‐sponsored enterprises, including several Federal Home Loan Banks, Fannie Mae, Freddie Mac, and Farmer Mac.”

The Logic: Fischer continues: “This facility should encourage these institutions to be unwilling to lend to private counterparties in money markets at a rate below that offered on overnight reverse repos by the Fed. Indeed, testing to date suggests that reverse repo operations have generally been successful in establishing a soft floor for money market interest rates.”

Summary

Due to the explosion of the size of its balance sheet (bank reserves in particular), the Fed has been forced to abandon management of the Fed funds rate via traditional open market operations. This activity is now being replaced by two new policy tools, both of which are somewhat “softer” than the older tool. First, bank’s free reserves now earn an interest rate on excess bank reserves which is available to banks with access to the Fed’s reserve facility. Second, financial institutions such as money market funds lacking access to the reserve facility will be able to lodge funds overnight (not necessarily merely one night) at the Fed and receive the reverse repo rate offered by the Fed.

Part D: Irrelevance of these Developments to the European Central Bank

Interestingly, the European Central Bank does not need and will probably not implement the policy innovations now being implemented by the US Fed. The reason is that in Europe, lending is dominated by banks far more than here in the US. Moreover, most all European financial institutions can in effect deposit funds with the central bank. Finally, the ECB has long been able to vary the reserve remuneration (interest) rate that it pays for excess reserves. As a result, the ECB does not need to utilize the reverse repo rate tool that the Fed is introducing.

One final point should be made. Whereas Professor Fischer above asserts that the primary tool of the Fed will be variations in the reserve remuneration rate applicable to banks, other scholars believe it is the reverse repo rate that will be the primary tool of US monetary policy. This is partly because of the ongoing reduction of the role of banks in lending to private sector borrowers, a longstanding development that has accelerated with the new regulations imposed on banks since the Global Financial Crisis.

Part E: Will the Fed Shrink its Balance Sheet Back Down? If So, How?

Professor Fischer answers this point directly. Yes, the Fed will shrink its balance sheet, but not to the size of yesteryear. More specifically:

“With regard to balance sheet normalization, the FOMC has indicated that it does not anticipate outright sales of agency mortgage‐backed securities, and that it plans to normalize the size of the balance sheet primarily by ceasing reinvestment of principal payments on our existing securities holdings when the time comes… Cumulative repayments of principal on our existing securities holdings from now through the end of 2025 are projected to be $3.2 trillion. As a result, when the FOMC chooses to cease reinvestments of principal, the size of the balance sheet will naturally decline, with a corresponding reduction in reserve balances.”

Hopefully these remarks have helped clarify past and future changes in Fed policy—changes that amount to a thoroughgoing transformation of US monetary policy that would have been unimaginable a decade ago.

In the future, we suspect that the press will refer to the Fed’s targeting of the “reverse repo rate” in place of the Federal funds rate when analyzing prospective monetary policy.

San Diego, Raleigh, Atlanta, New York, New Hampshire, and Vermont

I am excited about going to the 2015 Strategic Investment Conference on Tuesday. If for some reason you get there early on Wednesday, I intend to be in the gym at the hotel about 2:30, so come by and let’s work out together. Again, don’t forget to follow me on Twitter while I’m at the conference.

In the middle of May I go to Raleigh to speak for the Investment Institute and then on to Atlanta, where I’m on the board of Galectin Therapeutics. I’m going to New York the first week of June, then up to New Hampshire, where I will be speaking with a number of friends at a private retreat. I will then somehow get to Stowe, Vermont, to meet with my partners at Mauldin Economics. The rest of the summer looks pretty easy, with a few trips here and there.

Next week I intend to share my speech at the conference, or at least the gist of it. I have been thinking about it and working on it for some time. I had dinner this week with Mari Kooi, former fund manager who has become deeply imbedded with the Santa Fe Institute, an intellectual hotspot famous for its maverick scientists and interdisciplinary work on the science of complexity. Some of their people are working on something called complexity economics, which is an attempt to move on from the neoclassical view of general equilibrium. If you wonder why the theories and models don’t work, it is because traditional economists are still busy trying to describe a vastly complex system by assuming away all the change except for that they believe they can control with the knobs they twist and pull. Their model of the economy resembles some vast Rube Goldberg machine where, if you put X money in here at Y rate, it will produce Z outcome over there. Except that they don’t really know how the actions of the market will play out, since the market is made up of hundreds of millions of independent agents, all of whom change their behavior on the fly based on what the other agents are doing. Not to mention the effects of herding behavior and incentive structures and a dozen things beyond the ken or control of economists. There is only equilibrium in theory.

And that’s why it is becoming increasingly difficult to predict the future. The agents of change are multiplying and changing faster than we can keep up. But next week I will throw caution to the wind (unless I give up in despair), and we’ll see what my very cloudy crystal ball suggests lies in our future.

I am really looking forward to seeing old friends and making new ones at the conference. Have a great week.

Your trying to find simple in a complex world analyst,

John Mauldin

subscribers@mauldineconomics.com

Federal Government Increases Annual TFSA Contribution Limit to $10,000

Federal Government Increases Annual TFSA Contribution Limit to $10,000

After years of promises, our Conservative party government has finally done it. No, we are not talking about balancing the budget. We are talking about something even more important to Canadian investors. Stephen Harper and his Tory’s have delivered on their promise to increase contribution limits for the Tax Free Savings Account (TFSA).

Going back to even before the Conservatives were elected to their majority government, they made a promise to Canadians that they would double the TFSA contribution limit once they had the budget balanced. Now, we have heard tempting promises from politicians before (ummmm…remember their promise not to touch the Income Trust structure) and have learned over the years not to get too excited until the package is delivered. But on Monday, April 20th, the government announced that they were increasing the annual contribution limit for TFSAs to $10,000 (from $5,500) – effective immediately.

Okay, so this wasn’t exactly a doubling of the TFSA contribution limit (an 82% increase in fact). But technically speaking, it is double the amount of the contribution limit at the time that the Conservatives starting making the promise. In any event, we consider this to be great news and highly beneficial for Canadian investors.

For those that would like a refresher, the TFSA is a tax-free investing account that was started in 2009. Initially, the annual contribution limit was $5,000 but it increases over time with inflation in increments of $500 (the limit went up in 2014 to $5,500). The way that it works is you contribute (up to your limit) with money that has already been taxed. Any investment returns generated inside of the TFSA accrues tax free and investors don’t pay taxes on any withdraws either. This makes the TFSA a very powerful tool for increasing investment returns and portfolio size over time. Any unused contribution room from previous years can also be carried forward to future years indefinitely. Any withdraws can also be re-contributed in future years (you just have to wait until the next calendar year to do so). Another attractive attribute of the TFSA is that (unlike the RRSP) withdraws in future years do not count as income and will not affect eligibility for federal income-tested benefits and credits, such as Old Age Security, the Guaranteed Income Supplement, and the Canada Child Tax Benefit. See www.tfsa.gc.ca for more details.

That all sounds great doesn’t it? Well, unfortunately not everyone loves the increased TFSA limits. The most notably opponents are (not surprisingly) the government’s two opposition parties (the Liberals and NDP). Of course it is the job of any political party to automatically disparage the policies and actions of their chief opponents.

Politics aside, the main criticism seems to be that as the TFSA continues to grow, the lost tax revenue for the government will cause a significant budget shortfall. Unlike in an RRSP (which is only a tax deferred account), any investment returns or withdraws from the TFSA will never be taxed (theoretically). We think that these claims are exaggerated and don’t provide the full picture of what happens when more people invest. One point that seems to be missing from this argument is higher TFSA limits will likely (certainly should) encourage higher levels of saving and investment. Economic growth is a function of a country’s savings and investment rate (which in Canada are at meager levels) and higher levels of economic growth and GDP translate into greater tax generating potential for the government. We also have to take into account that when people make withdraws from their TFSA they typically do so with the intentions of spending that money. Money spent in the economy is taxed at the time that most products and services are purchased and then again when it flows through the companies that provide those products and services – as corporate tax and income tax paid by employees (who have a job because these products and services are being purchased). Of course, future governments will always have the option to take certain actions if several years (or decades) down the road TFSA contributions do start getting out of hand. But if there is so much capital inside this structure that it makes a significant impact on government revenues then that means more capital is being saved and invested which is a positive driver for the economy long term.

At this point, our biggest concern over the higher TFSA contribution amounts is that it might make the TFSA a target of future governments. Although the thought of substantially negative change to the TFSA structure sends ripples of fear down my spine, the very possibility that this could happen is only more reason to start maxing out your contributions today and generate those tax free returns while you can.

“It is the financial repression of the ordinary individual in America. It is happening through three main avenues or arteries”

SPECIAL GUEST: JOHN BROWNE is the Senior Market Strategist for Euro Pacific Capital, Inc. Mr. Brown is a distinguished former member of Britain’s Parliament who served on the Treasury Select Committee, as Chairman of the Conservative Small Business Committee, and as a close associate of then-Prime Minister Margaret Thatcher. Among his many notable assignments, John served as a principal advisor to Mrs. Thatcher’s government on issues related to the Soviet Union, and was the first to convince Thatcher of the growing stature of then Agriculture Minister Mikhail Gorbachev. As a partial result of Brown’s advocacy, Thatcher famously pronounced that Gorbachev was a man the West “could do business with.” A graduate of the Royal Military Academy Sandhurst, Britain’s version of West Point and retired British army major, John served as a pilot, parachutist, and communications specialist in the elite Grenadiers of the Royal Guard.

SPECIAL GUEST: JOHN BROWNE is the Senior Market Strategist for Euro Pacific Capital, Inc. Mr. Brown is a distinguished former member of Britain’s Parliament who served on the Treasury Select Committee, as Chairman of the Conservative Small Business Committee, and as a close associate of then-Prime Minister Margaret Thatcher. Among his many notable assignments, John served as a principal advisor to Mrs. Thatcher’s government on issues related to the Soviet Union, and was the first to convince Thatcher of the growing stature of then Agriculture Minister Mikhail Gorbachev. As a partial result of Brown’s advocacy, Thatcher famously pronounced that Gorbachev was a man the West “could do business with.” A graduate of the Royal Military Academy Sandhurst, Britain’s version of West Point and retired British army major, John served as a pilot, parachutist, and communications specialist in the elite Grenadiers of the Royal Guard.

In addition to careers in British politics and the military, John has a significant background, spanning some 37 years, in finance and business. After graduating from the Harvard Business School, John joined the New York firm of Morgan Stanley & Co as an investment banker. He has also worked with such firms as Barclays Bank and Citigroup. During his career he has served on the boards of numerous banks and international corporations, with a special interest in venture capital. He is a frequent guest on CNBC’s Kudlow & Co. and a former contributing editor and columnist of NewsMax Media’s Financial Intelligence Report and Moneynews.com. He holds FINRA series 7 & 63 licenses.

FINANCIAL REPRESSION

“It is the financial repression of the ordinary individual in America. It is happening through three main avenues or arteries.

- POLITICALLY – The government is increasing its power almost everyday and repressing the public individual and particularly the rights of the individual. Always under the guise that it to help you! Published statistics are highly questionable; growth rates, inflation rates, unemployment rates. They are confusing people and today I read how they are forcing people out of using cash!

- ECONOMICALLY – We have had an enormous, unprecedented injection of cash into the economy with a $3.8T QE program. Its an experiment! It was initiated in Japan where two decades ago the BOJ said it wouldn’t work but the politicians insisted they do it. After two decades it still hasn’t worked. We are now doing it on a grand scheme without a pilot program. It is creating a (liquidity) trap. It is a major distortion and is crushing savers.

- FINANCIALLY – ZIRP is (also) crushing savers! It is savings which forms investment for the future. 62% of employment comes from small businesses where formation must be incented. That needs capital from savings. This along with increasing regulation is not only killing the consumer but the incentive to start a small business which is the key to the creation of jobs, which is key to the creation of income which is then key to savings and growth in the economy. It has all been killed by these policies.

“I don’t believe the central bank is necessarily evil, just unbelievably Irresponsible!

LIQUIDITY TRAP

“I think we are now seeing a situation which you could call a liquidity trap. There is so much money around that if they start to raise interest rates they are going to discourage people even more from spending. Ordinary individuals have low wages (wages have been flat for six years at least) yet taxes are going up (the number of taxes) as well as charges (licenses and fees)”

“They are pushing on a string. It isn’t liquidity that matters but wages and income!”

“How does the Fed create income without just giving us cash in the post (mail) by just sending us checks?

BY DESIGN

“I’m afraid I believe at the very top it is devious! If I connect all the dots together I cannot feel it is by accident – it by design. I think the president wants to distribute American wealth around America, but even worse is to distribute American wealth around the world. Its killing the economy and its kiliing America.”

“It means (eventually) everyone is going to look towards the government for solutions – that is when totalitarian governments come in (to existence)”

“The only solution is single term politicians – Turkey’s don’t vote for an early Thanksgiving!”

40 Minutes

…..Will U.S. Seize Gold?

…..Will U.S. Seize Gold?

Richard Russell: “Subscribers may remember that I thought the stock market would have a melt-up before it settled into a destructive bear market. It occurs to me that the chances of a melt-up are diminishing because the market is losing its upside momentum.

Prepare For Something Worse Than 1929 – 1932

My thinking is that the market is preparing for one of the worst bear markets in history, one that will out do the 1929-32 affair.

…continue reading HERE

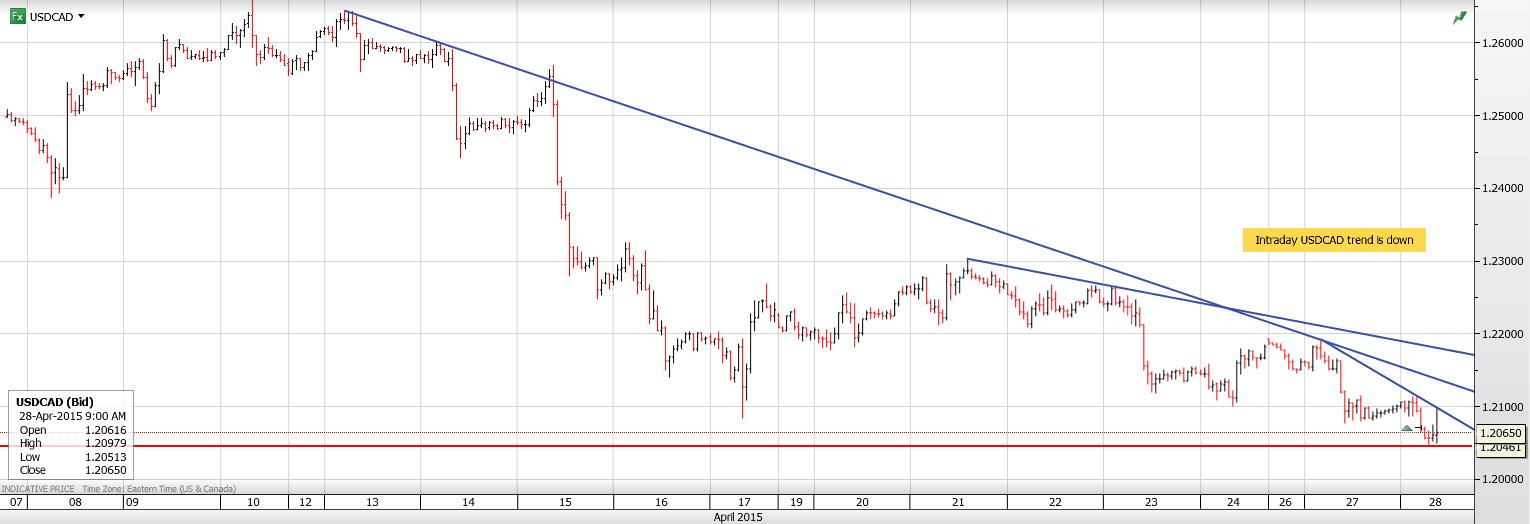

USDCAD Overnight Range 1.2052-1.2112

The US dollar is down across the board as traders continue to trim positions ahead of tomorrow’s FOMC statement, exacerbated by the absence of top tier data.

The Asian session was quiet. USDJPY traders ignored Fitch’s downgrade of Japans long term debt while AUDUSD traders ignored a speech by Glenn Stevens. The fact that Mr. Stevens didn’t say anything about monetary policy was probably why. Europe started quietly but EURUSD hasn’t looked back after breaking above 1.0900.

USDCAD is testing support in the 1.2050 area undermined by firm oil prices and dovish expectations for tomorrow’s FOMC statement. The IMM speculative short CAD positions, as reported by the Commitments of Traders Report (CoT) showed a modest decline to $2.7 billion from the previous week’s $3.2 billion. It is not unrealistic to assume that further unwinding is weighing on USDCAD.

Bank of Canada Governor, Stephen Poloz, testifying before the House of Commons Finance Committee this morning, didn’t really deviate from his April 15th Monetary Policy Statement which was a non-event for the currency.

USDCAD technical outlook

USDCAD is probing support at 1.2050 which is guarding the key 1.1980 level reprenting the uptrend from September 2014. A break of this level will extend losses below the 2015 low resulting in a move to 1.1660.

The intraday technicals are bearish while trading below 1.2105 looking for a break of 1.2050 to extend losses to 1.1970-1.2010. A move above 1.2105 will lead back to 1.2140.

Today’s Range 1.2050-1.2110

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair