Energy & Commodities

Is US shale about to make a comeback?

Is US shale about to make a comeback?

Oil prices have rebounded strongly since March. The benchmark WTI prices soared by more than 36 percent in two months, and Brent has jumped by more than 25 percent. There is a newfound bullishness in the oil markets – net long positions on Brent crude have hit multi-year highs in recent weeks on a belief that US supply is on its way down.

That was backed up by recent EIA data that predicts an 86,000 barrel-per-day contraction for June. The Eagle Ford (a loss of 47,000 barrels per day) and the Bakken (a loss of 31,000 barrels per day) are expected to lead the way in a downward adjustment.

But that cut in production has itself contributed to the rise in prices. And just as producers cut back, now that prices are on the way back up, they could swing idled production back into action.

A series of companies came out in recent days with plans to resume drilling. EOG Resources says it will head back to the oil patch if prices stabilize around $65 per barrel.

The Permian is one of the very few major shale areas that the EIA thinks will continue to increase output. That is because companies like Occidental Petroleum will add rigs to the Permian basin for more drilling later this year. In fact, Oxy’s Permian production has become a “sustainable, profitable growth engine,” the company’s CEO Stephen Chazen said in an earnings call. Oxy expects to increase production across its US operations by 8 percent this year. Diamondback Energy, another Permian operator, may add two rigs this year.

Other companies – including Devon Energy, Chesapeake Energy, and Carrizo Oil & Gas – have also lifted predicted increases in output for 2015.

In the Bakken, oil production actually increased by 1 percent in the month of March, a surprise development reported by the North Dakota Industrial Commission.

Taken together, momentum appears to be building in the US shale industry.

But let’s not get ahead of ourselves.

The US oil rig count has plummeted since October 2014, falling from 1,609 down to 668 as of May 8 (including rigs drilling for gas, the count dropped from 1,931 to 894). That is a loss of 941 rigs in seven months. Just because a few companies are adding a handful of rigs does not mean that the drilling boom is back. It takes several months before a dramatic drop in the rig count shows up in the production data. The EIA says production will start declining this month – but further declines in production are likely.

Moreover, even if US producers do come swarming back to the oil fields and manage to boost output from the current 9.3 million barrels per day, that would merely bring about another decline in oil prices. Lower prices would then force further cut backs in rigs and spending. The effect would be a seesaw in both prices and the fortunes of upstream producers.

As John Kemp over at Reuters notes, that is not an enviable position to be in. Much has been made about the geopolitical and economic influence that shale drillers have snatched away from OPEC. The oil cartel has lost its ability to control prices, the thinking goes. Now, the US is the new “swing producer,” and with it comes influence and prosperity.

But if oil companies oscillate between cutting back and adding more rigs as the price of oil bobs above and below the $60 mark, they won’t exactly be raking in the profits. Worse yet, EOG and Oxy may be profitable at $60, but there are a lot more drillers in the red.

In other words, there is still a supply overhang. In order for oil markets to balance, a stronger shake out is still needed. That means that the least profitable sources of production – drillers that have loaded up on debt to drill in high-cost areas – have yet to be forced out of the market. The drilling boom is not back yet.

More Top Reads From Oilprice.com:

- Here Is Why Predictions For Lower Oil Prices Are Wrong

- Alberta Election Result Changes Little For Oil Industry

- Did Low Oil Prices Actually Hurt U.S. Economy?

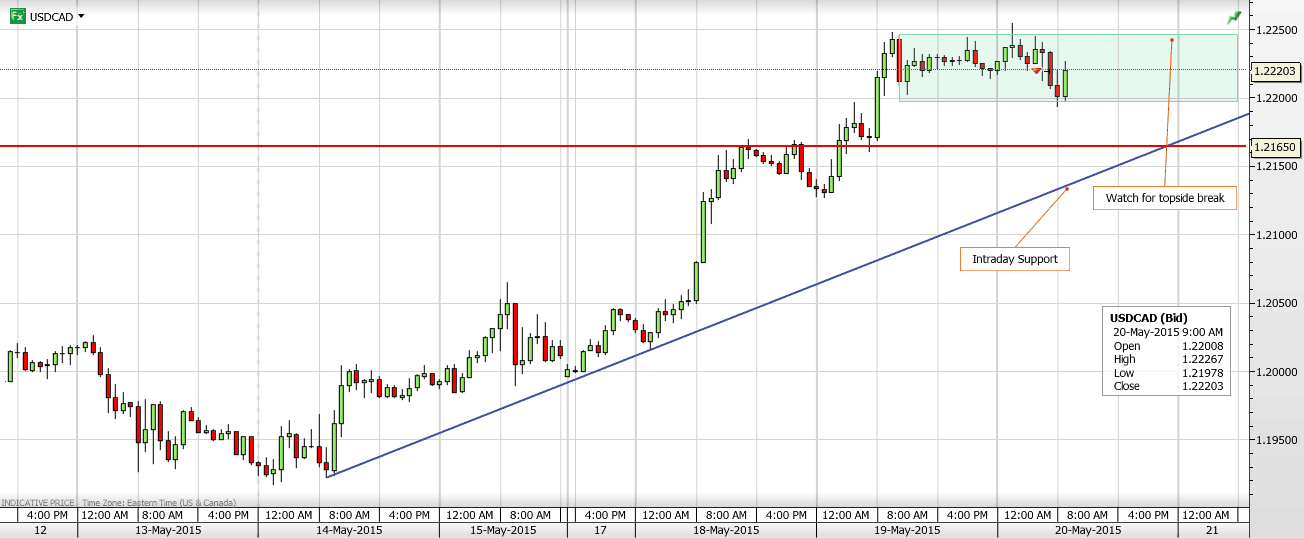

USDCAD Overnight Range 1.2200-1.2254

USDCAD held on to yesterday’s gains despite being largely ignored in a lively overnight session. Across the board US dollar demand was the main theme. USDJPY ignored greatly improved Q1 prelim GDP and tested resistance at 121.05. AUDUSD ignored a stellar Consumer Confidence report and headed lower. In Europe, EURUSD selling drove EURUSD below 1.1100 to 1.1065 on the back of renewed EU/USA economic and interest rate divergences concerns. The BoE minutes were thought to be slightly hawkish which gave GBPUSD a short lived boost.

Yesterday’s speech by the BoC governor was vintage Poloz. He stuck to his view that growth will rebound and the economy will reach full capacity by the end of 2016 while simultaneously stating how uncertain everything was. Traders tuned him out.

FX markets are likely to trade in fairly narrow ranges until this afternoon’s release of the FOMC minutes. Any indication that the minutes were far more hawkish that what the statement implied, will ignite another bout of US dollar buying.

USDCAD technical outlook

The intraday USDCAD technicals are bullish while trading above 1.2140 although the rally has stalled within a narrow 1.2240-1.2260 band. Failure to decisively take out the top side resistance coupled with the breach of the minor uptrend line from Monday (at 1.2230) warns of further weakness to 1.2170. Meanwhile, the downtrend line from the end of March remains intact.

Today’s Range 1.2190-1.2260

Chart: USDCAD 1 hour with resistance zone

Soaring overall automobile sales and the wonders of very upscale cars are making headlines around the world. In China the banner is about the “Electric Car Boom”. Of course, in North America the big numbers are about pickup truck sales. Much of this is on the “never-never” with car loans out to 7 years. For the high-rollers, million-dollar new cars show remarkable performance numbers, but are “chump change” compared to the bids for residential real estate, art pieces and “collector” cars.

Soaring overall automobile sales and the wonders of very upscale cars are making headlines around the world. In China the banner is about the “Electric Car Boom”. Of course, in North America the big numbers are about pickup truck sales. Much of this is on the “never-never” with car loans out to 7 years. For the high-rollers, million-dollar new cars show remarkable performance numbers, but are “chump change” compared to the bids for residential real estate, art pieces and “collector” cars.

The premier production supercar is the Bugatti Veyron. Priced at $2.7 million, it features a W-16 cylinder engine with 4 turbochargers. Putting out some 1006 bhp the top speed is 253 mph. Full-on braking will bring the car down to a stop in only 10 seconds, but it uses half a kilometre of road.

Wheels as objets d’art have been bid up with a 1961 Ferrari California Spider in sadly deteriorated condition selling recently at auction for $18.5 million.

Where are cars going?

The last speculative surge in such cars soared up with the Tokyo Financial Bubble of 1989. It was a hot market for “Trophy” hotels, golf courses and collector cars. Over the decade to 1989, the price for a 1968 Ferrari 275 GTB 4 cam soared from $10,000 to $1.2 million. With the Nikkei crash. The price plunged to the $300,000 level. This was a reasonable proxy for the overall sports car market and one has recently traded for $1.3 million.

However, returns on some cars since the 1990s bottom have been outstanding.A friend just missed buying a 1939 Alfa Romeo 2900 for $180,000. Recently, one traded for $10 million.

The highest price for a car sold at auction was $38 million for a 1962 Ferrari GTO. That was in 2014.

Even micro-cars from the early 1950s have been collected. More a motorcycle than a car, a Messerschmitt Kabinenroller (Cabin Scooter) recently sold for over $300,000. This holds two people with the driver in front steering with motorcycle handlebars. The “Kabin” is clear plastic bubble and it provided some shelter from wind and rain. It was called a “Bubble Car”. Another such car was the BMW Isetta, which was the biggest seller with a production run of some 161,000 units.

With no little irony, the 1950s bubble cars have been caught up in yet another financial bubble. From the ridiculous to the sublime.

The last huge mania in sports cars peaked with the Nikkei in 1989. This one will likely peak as the current bubble in stocks and bonds exhausts itself.

Glowing stories about sensational automobiles have been frequently published. “Auto Makers Are Cruising Down the Road to Excess” was a headline of a WSJ article which included a description of the Mercedes Gelaendewagon, a SUV with a sticker price of over U.S. $150,000. The AMG version has a V12 turbo engine.

However, a tough-go anywhere vehicle was not the subject of a story on “James Bond” cars such as the new V-12 engine for Aston Martin. After suffering a setback with the 2008 recession, Ferrari is “enjoying the best financial position in history”. That goes for Porsche as well. Extravagant cars and great bull markets do go together.

With the good times of the financial boom, traditional manufacturers have been acquiring the exciting names. Fiat owns Ferrari, and Ford took over Aston Martin and Jaguar. Particularly ambitious, VW’s shopping spree picked up Lamborghini as well as the Bugatti and Bentley brand names. The latter’s concept car features a V-16 engine, the first for a proposed production car since the magnificent examples of the booming 1920s.

However, this ostentatious part of the boom now seems particularly vulnerable. Despite the worst markdown in stock market capitalization since the early 1930s, the consumer kept their own bubble going by buying cars.

“Zero” cost financing, and rapid introduction of “new” models to defer saturation, some, such as a Cadillac “pickup truck” and Porsche SUV, and more recently Rolls Royce and Lamburghina and developing SUVs.

However, threats to the action have been mounting.

Today’s cars boast the greatest longevity in history and the price of used cars has been pushed down to economically attractive levels by the discounting. The dramatic credit downratings for Ford and GM are forcing their borrowing rates up, which will impair their ability to continue “0” financings.

The boom started in the 1990s with annual world car sales of 39 million units and now it is up to 74 million. The mania is so sweeping that even used car sales are being financed by financial engineering. Underwriters are bundling car loans and selling the certificates to fund managers.

Seems even dodgier than what was going on with the housing boom that created so much trouble beginning in 2007. That was the first miracle of turning sup-prime into AAA. Notwithstanding this speculative history famous billionaires have been buying car dealerships, like there was no tomorrow. Gates has been in the the game already. In March, Warren Buffett closed on the purchase of the largest private dealership in the US. He glowed with “This is the beginning of a journey that will have no end. The fun has just started.”

More down to earth, and as travellers often ask “Are we there yet?”

Yes!

As to “collector” cars, this is part of a fully-blown inflation in financial and tangible assets. The bond part of the bubble has been, by far, the greatest in history and started to fail in April. This will hit most, if not all, asset classes.

Major collections that were acquired over decades are being auctioned, en masse. This suggests distribution.

Cars at any price level are being made with an unprecedented longevity. Ten years as a driver and perhaps another five as a good “beater” is a given. So under pressure many could defer buying or leasing a transportation car for a long time.

All manufacturers are turning to fad items such as SUVs and novelties such as electric or hybrid cars. Even Formula 1 racing is “doing” hybrids.

Generally, emphasis on novelties could increase as the big manufacturers turn to planned obsolescence to keep the assembly lines going.

It won’t be the first time.

Planned obsolescence was “discovered” late in the 1920 boom.

Are these indicating the end of the unprecedented extension of the boom in cars well after the new financial era expired? If so, what’s the significance? Perhaps the pattern of the last example will provide some guidance.

Unintended saturation dramatically reversed automobile sales in the U.S. in the spring of 1929. The importance is that it surprised management and was accompanied by a reversal to unusually weak industrial commodity prices.

For example, although enjoying outstanding sales growth in the 1920s’ new era, any concerns about market saturation were dispelled. In 1928, the head of the Society of Automotive Engineers thought that it could be offset by “changing automobile appearance frequently as to obsolete those in the hands of owners”.

As with the “new and scientific” Federal Reserve System, the concept of obsolescence would keep the good times rolling.

In the same year, Knudsen, President of Chevrolet, estimated that saturation couldn’t be seen even by 1930.

General Motors observed it would tough out the possibility of saturation and “keep ahead of the competition by offering more models with more features than anyone else”. Overcapacity and rationalizations seem to be the consequence of a great boom. This was rapidly dashed in the contraction.

Beyond plunging unit sales, a change in fad now could have more profound consequences. The expansion of SUV production has been phenomenally profitable and a change to conservatism would likely result not only in dropping unit sales, but a shift to lighter as well as used cars. Another serious decline in most industrial commodities seems possible.

In the last great financial boom, the epitome of automobile fashion was not exaggerated ground clearance and four-wheel-drive, but length and weight for a luxurious ride as well as multi-cylinder engines for quieter running. The big car offered bragging rights about “hugging the road” and accelerating from 0 to maximum speed (about 90 mph) in topBOB gear only.

Behind the claims was the practical matter of a balky non-synchromesh manual transmission with a heavy and tricky clutch. Minimizing lunging starts and grinding gears required practice and concentration.

The desirability of a smooth start in top gear was obvious to both engineering and marketing people. For a given engine displacement, torque (for acceleration) is increased by a longer stroke and more cylinders.

Moreover, the latter provided smoother running and engines went from the straight sixes to eights with the V-sixteen being the ultimate in design and sales pitches of the late 1920s.

Whether then or now, the heavier the car, the greater the profit margins prompted similar business decisions and the accomplishments in the late 1920s luxury market in engineering and coachwork were magnificent.

While the Duesenberg, with an in-line eight, was the most formidable car of the era, the theme of this article is automotive fads and booms. Both peaked together and the esteemed cars were V-16s; two production models and one prototype.

Possibly both inspired by and symptomatic of the boom, the concept of the sixteen cylinder luxury car arrived in 1927. In America, work began on the Marmon Sixteen in early 1927. Shortly after that, one of the engineers left to design one for Cadillac and in July, 1929 another left to design the prototype Peerless V-16.

During the 1920s, Cadillac had lost leadership to Packard’s V-12 and, rather than expanding their V-8 to the next configuration and merely match competition, management legend Alfred Sloan insisted on the V-16. Seeming to ignore the bust, 2,500 were sold in 1930.

The engine displaced 452 cubic inches and the car, with a wheelbase of 148 inches, weighed 6,200 pounds. By comparison, the figures for today’s popular Ford Focus are 104 and 3,000 respectively.

Sensitive to changing popular attitudes towards extravagances, management quickly produced a more modest V-12. Only 750 V-16s were sold in 1931 despite heavy discounting down to almost the price for the V-12. Indicating rejection of ostentation, only 346 V-16s were sold in 1932 while 1,709 of the “un-extravagant” V-12s were bought. In 1933, the numbers were 125 and 1,000 respectively.

Although the line, in this case between ostentatious and merely conspicuous consumption, was narrow, post-boom moderation was a compelling fashion – especially when the song Brother, Can You Spare A Dime? described the times. (Bing Crosby’s 1932 recording has it right.)

For the last two decades, General Motors’ Suburban was the big SUV, but Ford’s Excursion, at 19 feet, is almost a foot longer and weighs 8,800 lbs. This provoked GM’s acquisition of the Hummer in 2000, which press releases described as a “monster vehicle” and “image builder”. It seems that management, in also planning to make the Suburban bigger, was responding to forces similar to those during the last great boom when it was compelled to trump Packard’s V-12 with a V-16. BOB HOYE, INSTITUTIONAL ADVISORS – WEBSITE: www.institutionaladvisors.com 5 The big SUV’s status is size, height with plenty of ground clearance, and rugged fourwheel drive. Other than making a dramatic statement, their unique design function is little used in rough terrain. Owners enjoy the up-high authority, but fewer than 6% take them “off road” and don’t seem to mind getting half the fuel mileage that the average car gets. In making up only 15% of new car sales, they deliver 60% of North American industry profits. A $58,000 price tag generates about $19,000 in profit, which is the equivalent to the entire sticker price of many small cars.

The numbers are irresistible and, in 1996, there were 26 models and the numbers are approaching 100.

In 1929, Cadillac developed the synchromesh transmission which eventually, with the smoothness of a well-engineered V-8, made the features of the V-16 redundant. That fad for grand cars, with overall attitudes becoming more conservative after the boom, ended and bankrupted many of their manufacturers.

Today’s wonderfully fast supercars have top speeds of around 200 mph. This compares with the 1932 Duesenberg SJ which, in showroom trim, could do 135 mph. With an improved intake manifold (which became stock), it accomplished 145 mph. In either era, speed is more important as a boast rather than a practice.

For enthusiasts, the two new eras produced some fabulous cars but, beyond that, they are symptomatic of a great financial boom. And, despite (or because of) the enthusiasms, satiation was achieved, which contributed to the 1930s contraction.

Still caught up with the spirit of the greatest bull market in history, engineers and marketing types at Bugatti are talking up more cylinders – this time in a W-18 configuration. Meanwhile, over in Stuttgart, Porsche is still touting its Cayenne. Lamborghini and Rolls Royce are joining the party. So are Alfa Romeo and Maserati. Showing some discretion, Ferrari has announced it would not join the fad. Recalling the brutal cars of 1929, the Bentley pitch is that its Arnage model is “The Most Powerful Sedan in the World”. In the racing world, “Arnage” is one of the sections at Le Mans, which Bentley won from 1927 to 1930.

It seems that “what goes around comes around”.

This is understandably a topic that seems to be on many people’s minds these days.

They have seen the writing on the wall—the unsustainability of the current paper money system—but don’t know what will happen next.

Thus, the question of when and how much one should invest in gold and silver is one of the questions I’m asked most frequently.

No one can predict exactly what will rise up after the collapse of the current monetary system, but here is my take on how you can do your best to prepare yourself no matter what happens—

Tell us your thoughts on gold and silver. Is it important for investors to have them in their portfolio? If so, why?

I don’t think that gold is a good fit for a portfolio. When we think about a portfolio, a portfolio is what we hope to achieve an investment return on. But gold is not an investment.

The idea behind gold is that it is a form of savings, albeit a very long-term savings.

It’s a form of savings that can’t be conjured out of thin air by central bankers’ quantitative easing program. Or printed by a government’s printing press.

And it’s consistently shown to maintain its purchasing power over time.

Thus gold is an anti-currency. It’s a kind of asset that you own because you don’t have confidence in the paper currency issued by governments and central bankers.

So with that in mind, the idea of trading in your paper currency for gold, hoping to trade it back for more paper currency at a later date misses the point entirely.

That said—I think that everybody should consider owning precious metals. Again, not as an investment or speculation, but as a form of savings that exists outside of the conventional system.

Sometimes people buy gold and silver and then they fret over the daily fluctuations in the price. They lay awake at night worrying about whether gold is going to go below a thousand dollar or below whatever level.

I think this is a sign that you probably have too much gold. If you’re worried about it, then you’re probably over exposed.

If you have an app on your phone telling you the gold price and you’re constantly looking at it, then that’s your instinct telling you to lighten up.

Rule number one is to be comfortable with your exposure. That means having a gold position that you are comfortable with, that you can lock away and not even think about how the price is moving.

Then you can go on to sleep well, knowing that you have some real savings that can stand the test of time.

STRATEGY OF THE WEEK

Finding stocks that nobody cares about which suddenly come alive with buyer support is a great way to swing trade your way to profitability. Each morning, I seek out stocks that meet the criteria of my Simple Swing strategy, looking for those with the right chart pattern for a run higher in the relative short term. Some recent examples of stocks meeting my rules are ELNK, MNGA, CAS and CALM.

This strategy tends to have a lower success rate but a higher reward. When it works, it can work really well.

I found a few more this morning, here are three to check out:

STOCKS THAT MEET THE FEATURED STRATEGY

1. OPTT

OPTT started its move from the open this morning, its run higher was pretty swift so I like this one better if it can pull back a bit first. With a few days, it can be lower but looking out a week or two and it has good potential to be higher. Support at $0.65

2. PRAN

PRAN had a jump in volume and price at 10:35 this morning and that allowed it to break its downward trend line. Support at $1.20.

3. ATEN

ATEN broke out of a cup and handle pattern today with strong volume. I picked it up at 9:44ET and the stability in to the close makes me think it has good potential to continue higher. Support at $5.40.

…..read Tylers full newsletter entitled “SEVEN PROBLEMS, SEVEN SOLUTIONS

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair