Asset protection

Please remember this warning when you go to the ATM to get cash… and there is none.

Please remember this warning when you go to the ATM to get cash… and there is none.

While we were thinking about what was really going on with today’s strange new money system, a startling thought occurred to us.

Our financial system could take a surprising and catastrophic twist that almost nobody imagines, let alone anticipates.

Do you remember when a lethal tsunami hit the beaches of Southeast Asia, killing thousands of people and causing billions of dollars of damage?

Well, just before the 80-foot wall of water slammed into the coast an odd thing happened: The water disappeared.

The same thing could happen to the money supply…

There’s Not Enough Physical Money

Here’s how… and why:

It’s almost seems impossible. Hard to imagine. Difficult to understand. But if you look at M2 money supply – which measures coins and notes in circulation as well as bank deposits and money market accounts – America’s money stock amounted to $11.7 trillion as of last month.

But there was just $1.3 trillion of physical currency in circulation – about only half of which is in the US. (Nobody knows for sure.)

What we use as money today is mostly credit. It exists as zeros and ones in electronic bank accounts. We never see it. Touch it. Feel it. Count it out. Or lose it behind seat cushions.

Banks profit – handsomely – by creating this credit. And as long as banks have sufficient capital, they are happy to create as much credit as we are willing to pay for.

After all, it costs the banks almost nothing to create new credit. That’s why we have so much of it.

A monetary system like this has never before existed. And this one has existed only during a time when credit was undergoing an epic expansion.

So our monetary system has never been thoroughly tested. How will it hold up in a deep or prolonged credit contraction? Can it survive an extended bear market in bonds or stocks? What would happen if consumer prices were out of control?

Less Than Zero

Our current money system began in 1971.

It survived consumer price inflation of almost 14% a year in 1980. But Paul Volcker was already on the job, raising interest rates to bring inflation under control.

And it survived the “credit crunch” of 2008-09. Ben Bernanke dropped the price of credit to almost zero, by slashing short-term interest rates and buying trillions of dollars of government bonds.

But the next crisis could be very different…

Short-term interest rates are already close to zero in the U.S. (and less than zero in Switzerland, Denmark, and Sweden). And according to a recent study by McKinsey, the world’s total debt (at least as officially recorded) now stands at $200 trillion – up $57 trillion since 2007. That’s 286% of global GDP… and far in excess of what the real economy can support.

At some point, a debt correction is inevitable. Debt expansions are always – always – followed by debt contractions. There is no other way. Debt cannot increase forever.

And when it happens, ZIRP and QE will not be enough to reverse the process, because they are already running at open throttle.

What then?

The value of debt drops sharply and fast. Creditors look to their borrowers… traders look at their counterparties… bankers look at each other…

…and suddenly, no one wants to part with a penny, for fear he may never see it again. Credit stops.

It’s not just that no one wants to lend; no one wants to borrow either – except for desperate people with no choice, usually those who have no hope of paying their debts.

Just as we saw after the 2008 crisis, we can expect a quick response from the feds.

The Fed will announce unlimited new borrowing facilities. But it won’t matter….

House prices will be crashing. (Who will lend against the value of a house?) Stock prices will be crashing. (Who will be able to borrow against his stocks?) Art, collectibles, and resources – all we be in free fall.

The NEXT Crisis

In the last crisis, every major bank and investment firm on Wall Street would have gone broke had the feds not intervened. Next time it may not be so easy to save them.

The next crisis is likely to be across ALL asset classes. And with $57 trillion more in global debt than in 2007, it is likely to be much harder to stop.

Are you with us so far?

Because here is where it gets interesting…

In a gold-backed monetary system prices fall. But the money is still there. Money becomes more valuable. It doesn’t disappear. It is more valuable because you can use it to buy more stuff.

Naturally, people hold on to it. Of course, the velocity of money – the frequency at which each unit of currency is used to buy something – falls. And this makes it appear that the supply of money is falling too.

But imagine what happens to credit money. The money doesn’t just stop circulating. It vanishes. As collateral goes bad, credit is destroyed.

A bank that had an “asset” (in the form of a loan to a customer) of $100,000 in June may have zilch by July. A corporation that splurged on share buybacks one week could find those shares cut in half two weeks later. A person with a $100,000 stock market portfolio one day could find his portfolio has no value at all a few days later.

All of this is standard fare for a credit crisis. The new wrinkle – a devastating one – is that people now do what they always do, but they are forced to do it in a radically different way.

They stop spending. They hoard cash. But what cash do you hoard when most transactions are done on credit? Do you hoard a line of credit? Do you put your credit card in your vault?

No. People will hoard the kind of cash they understand… something they can put their hands on… something that is gaining value – rapidly. They’ll want dollar bills.

Also, following a well-known pattern, these paper dollars will quickly disappear. People drain cash machines. They drain credit facilities. They ask for “cash back” when they use their credit cards. They want real money – old-fashioned money that they can put in their pockets and their home safes…

Dollar Panic

Let us stop here and remind readers that we’re talking about a short time frame – days… maybe weeks… a couple of months at most. That’s all. It’s the period after the credit crisis has sucked the cash out of the system… and before the government’s inflation tsunami has hit.

As Ben Bernanke put it, “a determined central bank can always create positive consumer price inflation.” But it takes time!

And during that interval, panic will set in. A dollar panic – with people desperate to put their hands on dollars… to pay for food… for fuel…and for everything else they need.

Credit may still be available. But it will be useless. No one will want it. ATMs and banks will run out of cash. Credit facilities will be drained of real cash. Banks will put up signs, first: “Cash withdrawals limited to $500.” And then: “No Cash Withdrawals.”

You will have a credit card with a $10,000 line of credit. You have $5,000 in your debit account. But all financial institutions are staggering. And in the news you will read that your bank has defaulted and been placed in receivership. What would you rather have? Your $10,000 line of credit or a stack of $50 bills?

You will go to buy gasoline. You will take out your credit card to pay.

“Cash Only,” the sign will say. Because the machinery of the credit economy will be breaking down. The gas station… its suppliers… and its financiers do not want to get stuck with a “credit” from your bankrupt lender!

Whose credit cards are still good? Whose lines of credit are still valuable? Whose bank is ready to fail? Who can pay his mortgage? Who will honor his credit card debt? In a crisis, those questions will be as common as “Who will win an Oscar?” today.

But no one will know the answers. Quickly, they will stop guessing… and turn to cash.

Our advice: Keep some on hand. You may need it.

Regards,

![]()

Bill

As most of you probably know by now, it’s been my belief for about a year that gold’s bear market would not end until at least testing the previous C-wave top at $1,050. Every D-wave correction in the secular bull has at least retraced to the previous C-wave top except one.

So until gold tests the $1,000-$1,050 level, I think it’s premature to call the bottom. As a matter of fact, I think over the next several months gold is going to drop down into its final 8-year cycle low, and that move down could be extremely painful. That is the problem with trying to pick a bottom in a bear market. If you are too early, the drawdown into that final low can be extremely damaging both financially and emotionally. Let me explain.

Let’s say you are long gold and miners right now, and I am correct and gold still has a move to $1,000 or lower before the bear market is over. It would mean you are going to suffer a 20% or larger decline in your metals positions over the next several months. If you are heavily into mining stocks, this could be a 30-40% drawdown. Needless to say, almost no one can survive that kind of loss on their portfolio. It’s easy to imagine yourself holding through one of these multiyear cycle lows before it happens, but I can guarantee you almost no one can actually do it in real time.

What happens emotionally is that when gold gets to $1,000, the magnitude of the decline will make it look like gold is going to $800, $700 or $600. You may think that you can hold on, but in real time it’s going to look like the losses are never going to end. $1,000 gold won’t look like a bottom so you won’t be able to hang on.

But here’s what really happens to every trader trying to hold through a drawdown of that magnitude: At some point your emotions just cannot take the day after day losses and you panic and sell. At that point you are so emotionally drained by the magnitude of your losses and shell shocked by the force of the decline that it becomes impossible to reenter the market. So when we do get the bottom, whether it comes at $1,000 or $950 or $900, you are just too emotionally damaged to pull the trigger again.

And unfortunately, that’s exactly what you need to do. You need to buy at the bottom of the bear market. Buying at the bottom of a bear market is where millionaires and billionaires are made. Some time in the next several months we are going to get that once-in-a-lifetime opportunity. In order to seize it you need to avoid the drawdown and emotional damage from the final move down into the bear market bottom.

I suspect there are many of you out there who have been holding onto positions, listening to the multitude of gold gurus telling you that any day now gold is going to turn and rocket to the moon. Yes, gold will eventually turn and head much, much higher. Personally, I think it’s going to at least $5,000. However, if you don’t avoid the last leg down in the bear market, there’s no way you will be able to hold on for the ride back up.

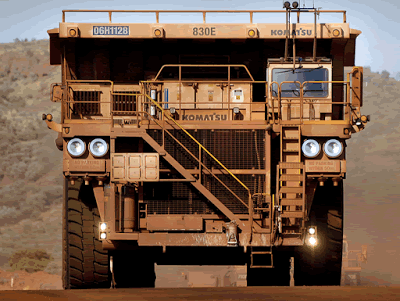

Replacing $200,000/yr Operators; Big Layoffs Coming

Replacing $200,000/yr Operators; Big Layoffs Coming

The Alberta oilsands region and the ore mining regions in Australia use some of the biggest trucks in the world.

Above: Komatsu heavy earthmoving truck at the Tom Price iron ore mine, operated by Rio Tinto Group, near Perth, Australia.

Drivers of these behemoths cost as much as $200,000 a year. With that incentive, the push to driverless is on.

Big Layoffs Coming

The Calgary Herald reports on the and the “threat of big layoffs” as Canada’s Oilsands Pave the Way for Driverless Trucks.

The 400-tonne heavy haulers that rumble along the roads of northern Alberta’s oilsands sites are referred to in Fort McMurray as “the biggest trucks in the world,” employing thousands of operators to

drive the massive rigs through the mine pits.

Increasingly, however, the giant trucks are capable of getting around without a driver. Indeed, self-driving trucks are already in use at many operations in the province, although they are still operated by drivers while the companies test whether the systems can work in northern Alberta’s variable climate.

That is about to change.

Suncor Energy Inc., Canada’s largest oil company, confirmed this week it has entered into a five-year agreement with Komatsu Ltd., the Japanese manufacturer of earthmoving and construction machines, to purchase new heavy haulers for its mining operations north of Fort McMurray. All the new trucks will be “autonomous-ready,” meaning they are capable of operating without a driver, Suncor spokesperson Sneh Seetal said.

For Suncor’s roughly 1,000 heavy-haul truck operators, however, the prospect of driverless trucks has raised more immediate fears of significant job losses.

“It’s very concerning to us as to what the future may hold,” said Ken Smith, president of Unifor Local 707A, which represents 3,300 Suncor employees. Smith said Suncor has signed agreements to purchase 175 driverless trucks.

“It’s not fantasy,” Suncor’s chief financial officer Alister Cowan told investors at an RBC Capital Markets conference in New York last week. He said the company is working to replace its fleet of heavy haulers with automated trucks “by the end of the decade.”

“That will take 800 people off our site,” Cowan said of the trucks. “At an average (salary) of $200,000 per person, you can see the savings we’re going to get from an operations perspective.”

Not Just Suncor

Some companies though will not comment on the prospect.

- Imperial Oil Ltd. spokesperson Pius Rolheiser would not say whether his company was testing the trucks at the company’s Kearl oilsands mine.

- Shell Canada Ltd. said it is “exploring” automated hauling.

- Canada’s largest drillers, Precision Drilling Corp. and Ensign Energy Services Ltd., use high-tech drilling rigs capable of moving autonomously between oil wells throughout North America.

As soon as one company makes the push the others have to follow or their ongoing operating expenses will be higher.

These truck driving jobs will be the first to go.

Then again, please keep in mind Today’s G7 Communique that seeks a 70% Reduction in carbon emissions by 2050, and 100% by 2100.

Apparently we don’t need these stinking jobs anyway. They will be replaced by free wind-power from all the windbags in D.C.

Gold bugs around the world got a shock a few weeks ago when a tiny Canadian start-up called BitGold bought venerable GoldMoney, the second biggest (after BullionVault) precious metals storage firm.

Gold bugs around the world got a shock a few weeks ago when a tiny Canadian start-up called BitGold bought venerable GoldMoney, the second biggest (after BullionVault) precious metals storage firm.

Now come the questions. Is this a case of a flashy tech company using its temporarily-inflated stock to buy real assets, a kind of AOL/Time Warner deal which goes sour when the new tech turns out to be a bubble? Or are these the young visionaries who finally solve the puzzle that eluded their elders?

First, a little digression: Back in the late 1990s while writing mostly about the excesses of the dot.com bubble, I was looking for a more optimistic theme. After interviewing GoldMoney’s James Turk for a couple of magazine articles, I fixated on his and others’ attempts to use the Internet to turn gold back into a functioning currency. This was a libertarian fantasy made real, allowing people to keep their spare cash in sound money while bypassing the increasingly dysfunctional, predatory banks with their hidden fees and stupid rules.

Lots of magazine articles and book proposals followed, but despite gold’s decade-long bull market, its digitization failed completely. eGold, the first mover, soon discovered that anonymity meant money laundering and was shut down by the police. GoldMoney required its users to disclose their identities, thus avoiding that legal minefield, but still ran up against regulations designed to limit the ability of alternative currencies to compete with central bank fiat. It eventually gave up, focusing instead on the boring but lucrative storage business.

Now, at the dawn of the age of cryptocurrencies, BitGold is reviving and updating the concept by storing bullion for customers and letting them spend their gold online or via debit cards. Among its cool new features is a tax calculator that figures users’ capital gains/losses for the countries that tax gold as a commodity.

It’s too soon to tell whether BitGold will succeed where its processors failed, but the early debate is, as you’d expect, lively. On the negative side, UK financial journalist (and author of a book on bitcoin) Dominic Frisby makes a cogent case for its probable failure. Here’s an excerpt:

Don’t touch this gold and bitcoin combo with a ten-foot bargepole

Last week, Canada saw the initial public offering (IPO) of BitGold.

It opened with a lot of publicity and a bang.

Today we consider BitGold.

We don’t ask whether you should run away – but how fast.

Bitcoin plus gold = sexy name, but not a lot of substance

BitGold is listed on the Venture Exchange in Canada with the rather handy ticker of XAU.V.

There are 36.6 million shares outstanding, of which 20 million are controlled by insiders. Based on Friday’s close at C$4.14 per share, it has a market capitalisation of around C$161m.

It has C$9m cash and, with 6.4 million warrants (3.9 million exercisable at C$1.35), another potential C$5m in the pipeline. The marketing budget this year is C$5m.

Among its early investors are, notably, Soros Brothers Investments and Sprott Asset Management.

The idea is for the company to become a PayPal for gold. You can go into a coffee shop or a grocer’s and buy everyday items with gold. You can also buy and store gold.

The company makes its money by charging 1% on transactions. For now, storage is free (although that is going to be an issue going forward – gold costs money to store).

As blogger Otto Rock notes, last year BitGold’s founders were paid in shares worth 3.3c a piece. The seed placements and pre-IPO fund raisings were at 90c plus warrants. The stock went public at C$2.70. After hitting C$4.50 on Thursday, the stock closed the week at C$4.14. Almost 701,000 shares traded on Friday.

Some people have done very well out of this already. But the business has hardly got going yet. It has very little market share, let alone profit. As someone who’s seen what Vancouver is capable of, this has set all my alarm bells off.

There’s been a lot of hype and now somebody is selling. There’s an expression for that. Can’t for the life of me remember what it is.

Frisby goes on to point out that there’s nothing preventing regulators from strangling this newborn in its crib as they did with GoldMoney and eGold, and that the concept of digital gold is inherently flawed because anyone with both fiat currency and gold would logically save the gold and spend the fiat.

These are good points. The regulators now gearing up to counter bitcoin can easily adapt to digital gold. But the idea that no one will want to spend gold is debatable. A checking account requires currency to be on deposit, where it can depreciate before being spent. Better to have that cash sitting in an asset like gold that will appreciate over time. Presented this way, a digital gold account might be an attractive combined savings/checking account for people who understand money.

And the upside of a functioning digital gold currency might be spectacular: If gold begins to flow into such accounts, the added buying pressure would send the price higher, which would make it even more attractive relative to fiat currency, leading to more buying, etc. The resulting feedback loop would be fun to watch.

So the prudent approach to BitGold is the same as for bitcoin: Acknowledge that the idea has promise, sample it if you’re so inclined, but don’t trust it with large amounts of capital until it’s been tested by regulators, the markets, and time.

Summer is the season of interns and young financiers bustling through an industry several times their age. So Business Insider reached out to veterans and asked, what are you reading?

Summer is the season of interns and young financiers bustling through an industry several times their age. So Business Insider reached out to veterans and asked, what are you reading?

We’ve compiled their suggestions here in a list surprisingly diverse in genre, topic, time period, and style. Together, they form a comprehensive picture of Wall Street’s in and outs, and deepen the reader’s understanding of forces driving the market

We’ve compiled their suggestions here in a list surprisingly diverse in genre, topic, time period, and style. Together, they form a comprehensive picture of Wall Street’s in and outs, and deepen the reader’s understanding of forces driving the market.

So crack one open. It’ll help you get through the dog days of summer.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair