Bonds & Interest Rates

With US$4.8 trillion in assets — or about the size of Japan’s economy — no one manages more money than BlackRock Inc. So, it’s worth paying attention when the firm says it’s time to cast aside its trusted models for assessing risk in bonds.

With US$4.8 trillion in assets — or about the size of Japan’s economy — no one manages more money than BlackRock Inc. So, it’s worth paying attention when the firm says it’s time to cast aside its trusted models for assessing risk in bonds.

The gyrations gripping the world’s fixed-income market are so great that it’s almost impossible to make sense of them on a historical basis. In Germany, for example, yields on 10-year securities have surged from almost nothing in late April to about 1 per cent last week — a move so swift that some strategists are likening it to a once-in-a-generation event.

“The German bund market is incalculably volatile,” said Scott Thiel, BlackRock’s deputy chief investment officer for fundamental fixed income in London. “It doesn’t make sense to measure it in traditional respects.”

Across Europe, investors are ripping up their old models to analyze the US$100 trillion global bond…..continue reading HERE

If you go to apply for a mortgage, you will suddenly encounter the REAL hunt for money. My sister just bought a house and to get the mortgage she had to explain every deposit and cash withdrawal in her account going back 5 years. My mother had simply written her a check for $400 to reimburse her for picking up some medicine. They wanted her to explain why my mother gave her $400.

If you go to apply for a mortgage, you will suddenly encounter the REAL hunt for money. My sister just bought a house and to get the mortgage she had to explain every deposit and cash withdrawal in her account going back 5 years. My mother had simply written her a check for $400 to reimburse her for picking up some medicine. They wanted her to explain why my mother gave her $400.

Another friend who lived with a girlfriend for 5 years and shared an apartment encountered the full fury of the government’s hunt for spare change. His girlfriend had written him checks for half the rent for 5 years. Every one of those checks had to be explained before they would get a mortgage to buy a home together.

This is completely illegal, yet banks are complying. This is all under the pretense of TERRORISM whereby they have to know where every penny goes. This is not applying a new law with notice that from this date forward you have to keep track of everything you do with anyone else as in East Germany Stasi, this is being applied retroactively. The banks then report that info to the IRS and if you lie somewhere they will convert that to perjury and threaten you with 5 years in jail. My sister would withdraw $2,000 in cash every few months for my mother for incidental purchases. Every one of those cash withdrawals had to be explained. This is between family member – there is no pretense of TERRORISM. We are watching all our privacy and right vanish before our eyes.

It is no longer good enough that you pay your taxes. Now they want to know to whom you are giving any money right down to $50. As a matter of law, if I pay a lawyer for work, I must issue a 1099 to document I pay him any fees. They are tracing every dime.

This sort of red tape will come into play seriously capping real estate in the housing market. We should expect prices to peak out in general for this asset class is being hunted. It may be that the high end holds up better. But the low end that needs a mortgage to transact, will find it increasingly more difficult as the economy turns down, rates move higher, and banks back away from long-term loans.

Cash is rushing into the short-end. The long-end is starting to falter. This should be the same for most real estate markets. This is a 26 year high in Switzerland as well and the rush for condos in Toronto and NYC should top out on this wave where prices depend upon mortgages. Expect the core real estate to peak out with this wave that requires mortgages. This type of unconstitutional tracking of money will eventually discourage people from getting mortgages and as buyers are discouraged in the USA, they will move elsewhere. Caution is advisable.

…more from Martin:

The End of Bonds? Look Out Below 2015.75

Let’s see…a heavily-indebted country can’t pay its bills, engages in a long series of failed attempts to manage a partial, controlled default, sees most of its capital flee to safer venues, and then, in a final act of desperation, imposes capital controls.

Let’s see…a heavily-indebted country can’t pay its bills, engages in a long series of failed attempts to manage a partial, controlled default, sees most of its capital flee to safer venues, and then, in a final act of desperation, imposes capital controls.

But it quickly realizes that it’s too late. Capital controls, to the extent that they ever work, have to be imposed by surprise, while there’s still some capital to control. If you wait until everyone expects them, the banks empty out in anticipation and you’ve locked a barn sans horses.

That’s pretty much what Greece is looking at in the next couple of weeks. Though a bailout remains possible, the markets have decided that it’s no longer a sure thing and capital is streaming towards the exit:

Greece bonds, stocks collapsing as the market re-panics

(MarketWatch) – This time we’re really panicking. That’s what some markets seem to be saying this morning on the heels of failed talks over the weekend between Greece and its European creditors.

Those discussions lasted anywhere between 45 minutes to an hour, with the breakdown a painful reminder of the fact that the International Monetary Fund bailed on its own talks with Greece last week. The can has now been kicked all the way to the last-stand June 25 European Union leaders summit in Brussels, where some say Prime Minister Alexis Tsipras has all his hopes riding.

But there’s also a meeting of Eurogroup finance ministers on Thursday, and many are looking anxiously for Athens to come up with new reform proposals ahead of that. June 30 remains the big line in the sand as Greece has a 1.6-billion-euro ($1.8 billion) payment to the IMF looming, after it bundled all its four June repayments into one.

The question is, what will markets do in the meantime? At least as far as Greek bonds and stocks are concerned, maybe just keep panicking. The yield on the 10-year Greek bond pushed above 12% in Europe’s morning, on track for its highest close since late April. It was up 90 basis points at 12.72%, according to electronic trading platform Tradeweb. The yield on 2-year bonds surged 3.9 percentage points to 28.66%.

Let this continue for just a few more days and Greece will be, financially as well as socially, a smoking ruin. It will also be a glimpse of the future for the rest of the developed world. The fact that the US, Great Britain and Japan can create their own currency allows them a bit of flexibility that Greece doesn’t have. But just a bit. As debt continues to rise faster than GDP, the gap between what’s owed and what can be repaid is becoming a chasm, with consequences that are both inevitable and inescapable.

Viewed this way the difference between Greece and the rest of us is cosmetic and very temporary. Where Greece negotiates with the IMF and ECB, the big debtor nations negotiate with the financial markets via QE and other kinds of debt monetization. The goal in both cases is to placate creditors without changing the behaviors that caused the problem. In both cases it has worked, for a time.

The fact that Greece is blowing up while the printing-press-endowed countries are not just means that the stock and bond markets are easier to fool than the ECB and IMF. But no one is permanently credulous. Everyone catches on eventually, and the soaring volatility in stocks and bonds around the world imply that Greece isn’t the only con artist about to be exposed. In bonds, for example:

Bond crash is so crazy BlackRock Inc is ripping up its risk models

(Financial Post) – With US$4.8 trillion in assets — or about the size of Japan’s economy — no one manages more money than BlackRock Inc. So, it’s worth paying attention when the firm says it’s time to cast aside its trusted models for assessing risk in bonds.

The $1.2 trillion meltdown in just three months is an early sign that it will not be easy to wean the world off six years of zero rates — and central banks have used up their arsenal. The gyrations gripping the world’s fixed-income market are so great that it’s almost impossible to make sense of them on a historical basis. In Germany, for example, yields on 10-year securities have surged from almost nothing in late April to about 1 per cent last week — a move so swift that some strategists are likening it to a once-in-a-generation event.

“The German bund market is incalculably volatile,” said Scott Thiel, BlackRock’s deputy chief investment officer for fundamental fixed income in London. “It doesn’t make sense to measure it in traditional respects.”

Across Europe, investors are ripping up their old models to analyze the US$100 trillion global bond market that dictates how much consumers and companies pay to borrow. Volatility is soaring as central-bank policies diverge, whiffs of inflation emerge and new regulations cause big banks to back away from their traditional role facilitating buying and selling. Continue reading here.

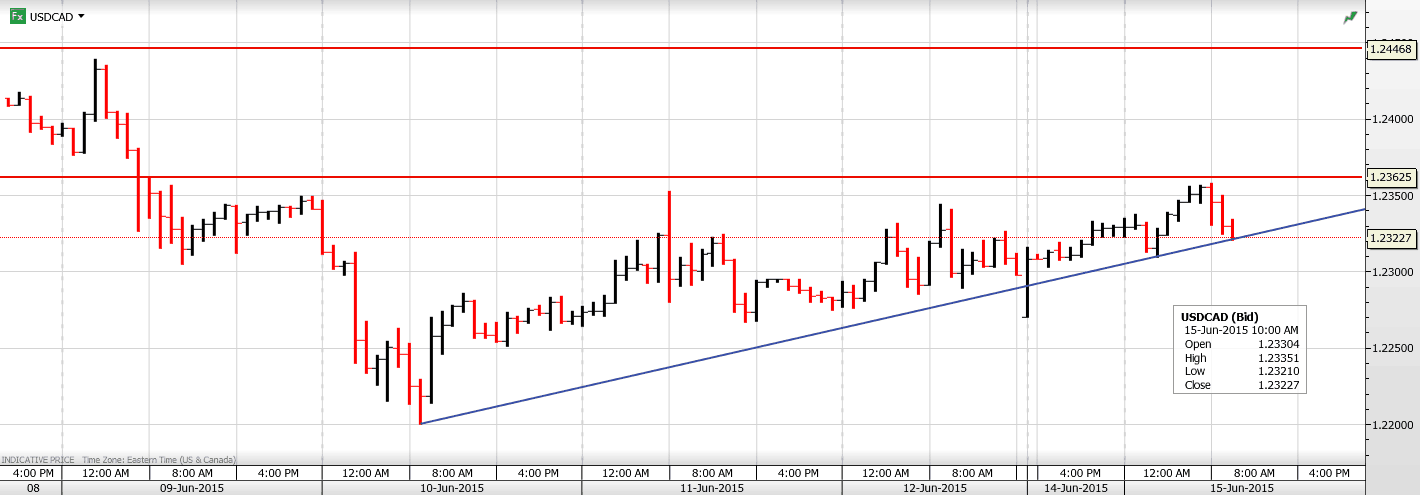

USDCAD Overnight Range 1.2310-1.2358

USDCAD edged higher in a thin overnight market, caught up in a combination of general US dollar strength and a small decline in oil prices.News that Canada’s Hudson’s Bay Corporation (HBC) was buying a German retailer for EUR2.38 billion, may have contributed to the USDCAD demand although that conclusion is a bit of a stretch.

The weekend news that the Greece/EU negotiations appeared to have collapsed drove the US dollar higher across the board in a thin Asian session. The move wasn’t sustained in Europe and the US dollar has given back most of its gains. This morning’s US data has been mixed. The NAHB housing starts index beat forecasts (Actual 59 vs. forecast 56) while both Industrial Production and Capacity utilization missed. All in all, it was a slow start to the week.

Canadian and US data is scarce until Wednesday’s FOMC meeting leaving headlines and oil prices to drive USDCAD direction. El

USDCAD technical outlook

The intraday technicals are bullish while trading above 1.2320 looking for a break of resistance at 1.2360 to extend gains to1.2440. A move below 1.2320 will lead to another test of 1.2280 and possibly back to 1.2240.

Today’s Range 1.2310-60

Chart: USDCAD hourly Larger Chart

DEFLATION RULES! – because periodic recessions, necessary to rebalance the economy after periods of growth, cannot be put off forever by the short-term expedient of printing money. The result of such corrupt and evasive practices is that the deflationary forces build up to catastrophic and overwhelming proportions leading to economic collapse and depression. This is the point that we have arrived at now. Why can’t governments keep the game going indefinitely by printing more and more money? – because the debt grows and grows until it becomes apparent even to dull-witted bond / Treasury holders that they are never going to get their money back, so they start selling and the selling snowballs into an avalanche, driving interest rates through the roof. Bond and stockmarkets crash and the economy sinks into a dangerously deep depression, all because governments stubbornly refused to do the right thing all along, and interfered with and obstructed normal market forces, culminating in their idiotic and ruinous QE, ZIRP and now even NIRP.

Of course, the mainstream financial media are trying to portray the recent trend of rising interest rates as a sign that the economy is recovering, saying that it is increasing demand in the economy that is driving rates up. If this is so then why is the Baltic Dry Index, which is a measure of shipping rates, at rock bottom depression levels, and why are commodity prices near to their 2008 – 2009 crash lows?? No – the reason that rates are going up is that bond holders have finally seen the writing on the wall and woken up to the fact that governments around the world not only have no intention of honoring their debts, but are incapable of doing so, even if they wanted to, so why should they hold on to piles of ultimately worthless paper that don’t even yield anything in the here and now? This is why bond and Treasury prices have been dropping, and notwithstanding any short-term bounce to alleviate the short-term oversold condition, look set to go into a self-feeding downward spiral that will drive rates sharply higher, turning the Fed into an impotent bystander. All this looks set to happen with a rapidity that will surprise many people and catch them off guard, particularly those who complacently assume that the long uptrend in many stockmarkets is set to continue forever.

Alright, so what is set to happen and what will drop and what will go up? Bond, commodity and stockmarkets look set to crash, with the rising rates associated with falling bond prices ripping the rug out from under the stockmarket. A wild “dash for cash” would be the result of this that will drive the dollar to possibly dizzying heights, like 2008 on steroids. Eventually, after this “swansong” rally, the dollar will crash and burn, especially when China – Russia roll out their gold backed new world reserve currency, an event which could trigger a war. Gold and silver will likely get caught up in this maelstrom and drop to new lows, despite imminent positive seasonal factors, but will later emerge into spectacular bullmarkets, and it will be important for any investors wanting to buy physical gold and silver to aim to do so ahead of the crash bottom, because after the turn it will be almost impossible to buy physical, and also to keep in mind that governments can be expected to pass laws enabling them to forcibly steal your gold and silver – so give some thought to where you are going to store it.

Our tactics therefore involve 2 main planks – cash: the US dollar, and bear ETFs, in bonds on any bounce and in stocks immediately. The more daring may consider out of the money Puts, and you should “swing until you hit”, rolling into the next series until the plunge occurs. We hold off buying the Precious Metals sector until this last takedown has run its course, which will likely see gold drop to the $850 – $1000 area and silver to about $10. Then we come out “guns blazing” because the ensuing rally in gold and silver is likely to be spectacular, dwarfing what occurred in the late 70’s.

Let’s now quickly review some relevant charts.

We start with the 13-year chart for TLT, which is a good long T-Bond proxy. On this chart we see that despite the recent sharp drop, predicted on the site in the last Bond Market update, it still hasn’t broken down from its long-term uptrend. The later stages of its bullmarket advance were of course fuelled by ZIRP, but since interest rates can’t go much below 0, it is pretty obvious that this bullmarket has run its course, especially with rates looking set to rise in the face of Sovereign defaults. It is therefore expected to break down from this long-term uptrend to enter a bearmarket.

Next yields. Yields have risen sharply over the past couple of months as bonds have dropped in price. This is a

process that looks set to continue, even if we see a short-term pause, and to accelerate…

The Baltic Dry Index, which measures shipping rates, is at rock bottom economic depression levels, indicating that global trade is weak and contracting, with the risk of more trade wars. This is a sign of deflation at large…

Likewise the commodity index chart shown below hardly indicates a robust world economy…

The US dollar is now at a very interesting juncture. In March its parabolic uptrend peaked and it burned out temporarily. At the time and soon after we had thought that it was done, and would go on to drop away, but given the prospect for a mass exodus from bonds and stocks, it looks set to become the beneficiary of a massive “dash for cash” that could drive another strong dollar rally. Technically, this is certainly possible as it is still above a rising 200-day moving average which means that arguably its trend is still up, and the reaction of recent months has allowed its earlier overbought condition to completely unwind.

Looking at recent dollar action in more detail on its 1-year chart (dollar index) we see that a consolidation Triangle may be forming above its rising 200-day moving average, which is now coming into play and could power another major upleg from here. This of course would be bad news for commodity prices, including gold and silver which would be tipped into another downleg.

Bondmarkets are expected to enter a confirmed a bearmarket soon, the first for many years, triggered by a wave of selling ahead of Sovereign defaults leading to more steep rises in interest rates. This will cause bloated stockmarkets to crash and commodities to drop further. The torrent of funds liberated as a result of this selling can be expected to flow into the US dollar, sending it sharply higher again. If this scenario prevails then the way to go for investors is cash and bear ETFs, with the eventual aim of switching into Precious Metal sector investments as they approach downside targets, for the ensuing rally in gold and silver should be massive. Physical metal purchases should be made ahead of the bottom, as physical will likely be very hard to source hard after the turn.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair