Asset protection

On the heels of the recent panic selloff in the gold market, today the top trends forecaster in the world warned King World News that the panic that’s happening right now is much bigger than just the gold market. Celente also went on to discuss the shocking truth about what is really happening in countries around the world.

On the heels of the recent panic selloff in the gold market, today the top trends forecaster in the world warned King World News that the panic that’s happening right now is much bigger than just the gold market. Celente also went on to discuss the shocking truth about what is really happening in countries around the world.

“Writes John Williams, “inflation adjusted June retail sales declined by .6%, weakening annual growth signaled an intensified recession.” The Fed cannot face the idea that they’ve pumped trillions in new money and the US economy is sinking into recession. If the Fed finally concedes that we’re in a recession, it will open the spigots wide, producing something which I think will be close to hyperinflation.

“Writes John Williams, “inflation adjusted June retail sales declined by .6%, weakening annual growth signaled an intensified recession.” The Fed cannot face the idea that they’ve pumped trillions in new money and the US economy is sinking into recession. If the Fed finally concedes that we’re in a recession, it will open the spigots wide, producing something which I think will be close to hyperinflation.

The dollar is rising to new highs. If the recession story is true, the dollar should crash and gold should regain its bull market. In the meantime, turning to Greece, it is testing the patience of the euro nations. My guess is that Greece will end up on its own, and not as a partner in the great euro experiment.” – Richard Russell

The above is an excerpt from the 90 year old Richard Russell’s Dow Theory Letters, a letter that has been coming to subscribers every 3 weeks since 1958. Richard also posts daily updates to his subscibers to his newsletter., a service that began with the advent of the internet. Richard is also responsible for a proprietary indicator call the PTI. Click HERE to subscribe to this valuable service

With the recently concluded nuclear deal between Iran and the P5+1 countries, oil prices have already started heading downward on sentiments that Iran’s crude oil supply would further contribute to the already rising global supply glut. The economic crisis in Greece, OPEC’s high production levels and China’s market turmoil have created more pressure on oil prices, making a price rebound lookhighly unlikely in the near future.

So, with the prices of both Brent and WTI moving towards $50 per barrel, the short to medium-term outlook for oil remains mostly bearish. This is bad news for the U.S. shale sector which is already dealing with rising debt and the ever-increasing risk of default.

A recent Bloomberg report stated that U.S. driller’s debts stood at $235 billion at the end of first quarter of 2015, which is quite worrying. Does this mean that the U.S. oil sector is likely to witness a lot more layoffs than we have seen so far? Surprisingly, a recent IHS study had revealed that the U.S. shale sector has been boosting job creation in addition to supporting around 1.7 million jobs in U.S.

All this as the overall unemployment rate in U.S. has been declining since previous years. But with rising negative sentiment pertaining to oil prices, is U.S. the shale sector prepared to face one of its biggest tests yet? Will the industry be able to sustain another long period of low oil prices or will it once again resort to trimming its workforce?

Low oil prices will most likely result in more job losses

Since the oil price collapse of last year, we have seen how oil field services and drilling companies have slashed thousands of jobs in order to reduce costs and cut their operational spending. Some of the major oilfield companies like Schlumberger, Halliburton and Weatherford have already announced close to 20,000 layoffs as of February 2015.

Source: CNN Money

However, the markets turned bullish when oil prices were hovering in the range of $60 per barrel during the last two months, raising hopes

that oil companies would be sending close to 150 drilling rigs back into operation.

Now that oil prices are again moving towards the $50 per barrel mark, high drilling costs make almost a third shale oil in the U.S. too expensive to produce. Even Goldman Sachs has admitted that the $50 per barrel oil price level would deter any kind of a drilling recovery in U.S. this year, as there would only be around 20 to 50 rigs returning to work by end of this December. In fact, analysts from Goldman predict WTI will fall to $45 a barrel by October this year.

“Oil rebalancing remains in its early stages with the current cash flow and funding mix stalling it, we believe that as fundamentals reassert themselves and we move past the seasonal peak in demand, oil prices will continue to sequentially decline,” said analysts from Goldman Sachs.

U.S. shale sector faces another challenge as hedges expire

The U.S. shale industry had been somewhat insulated from the effects of low oil prices in the past as companies had hedged their production. This meant that companies had fixed their future selling price in order to temporarily circumvent the ongoing volatility in the oil markets. Since most of the companies had hedged their production before the last oil price crash, they were well protected from the erratic oil price movements. However, the situation is quite different now as most of these hedges are about to expire. For small and medium shale companies that had hedged their production at $85 or $90 per barrel previously, having more of their production exposed to $50 per barrel prices will be painful.

What to expect over the coming months

The coming few months will prove challenging for the sector, and some small and medium U.S. producers may start missing their debt repayments or even file for bankruptcy. Quicksilver Resources and American Eagle Energy are two of the six U.S. based companies that have filed for bankruptcy in 2015 so far. Sabine Oil and Gas Corp. is the latest, and the biggest, U.S. producer to file for bankruptcy so far.

Even mergers and acquisitions have slowed down considerably for the U.S. oil and gas industry in 2015. If the present trend persists, companies will have no choice but to cut their workforces even further to remain competitive and reduce their rising overheads. If oil prices remain in the range of $50 per barrel for longer than expected, even big operators such as Exxon Mobil, Chevron and ConocoPhillips (who have so far not made any major layoffs) could start downsizing their workforce.

First, precious metals peaked and began drifting lower. Then copper fell, oil plunged and it became obvious that these weren’t isolated events. The entire commodities complex — that is, all the physical inputs a modern economy uses to power, transport and build stuff — was in sustained decline. Here’s the Bloomberg Commodities Index over the past five years:

Now, after the past week’s free-fall, commodities are front-page news:

Commodities crash to 11-year low as deflation fears grow: Latest price slump complicates backdrop for interest rate hikes

Global commodity prices have slumped amid a glut of supply and low demand – and now experts are foreseeing the prospect of deflation in the West.

A basket of commodities measured by the Bloomberg commodities index has fallen to an 11-year low, and the index is down 42 per cent since its peak in 2008.

The “commodity supercycle” was the term to describe the boom in commodity prices pre-crisis, when global growth was steaming ahead and supported demand. Although commodities have had a hard time post-crisis, falls in the price of everything from from gold and oil, to copper and nickel have accelerated. Tin has fallen 25 per cent so far this year, Nickel is down 54 per cent from its February 2011 high, and natural gas has slumped 40 per cent over the same period.

There is a glut of industrial commodities on the world market and with growth flagging, demand is simply not strong enough.

Slightly different dynamics are at play in the oil market, as Saudi Arabia has vowed to keep Opec’s production high despite weak demand. Already-low oil prices have fallen 10 per cent in the last month, ahead of the lifting of US sanctions against Iran. There is known to be a significant amount of supply stacked up in Iran and waiting to hit the world market. Brent crude for September was down to $56.75 a barrel yesterday morning.

46% – fall in copper prices since 2011

25% – fall in tin prices so far this year

ASK DOCTOR COPPER

Perhaps most telling is the price of copper, which is trading around its lowest level since the financial crisis.Known as Dr Copper due to its use as a barometer of global economic health, the industrial metal fell to $5,240 a metric tonne last week, heading towards weakness last seen in the summer of 2008.

The slump in copper is a “direct consequence of the actions we are seeing in China, the increasingly flustered and desperate government [measures]”, says Alastair McCaig at IG Index.

The nation accounts for 50 per cent of global copper demand, and despite official GDP data released last week stating that growth has confounded expectations to hit seven per cent in the second quarter, the figures have been widely ridiculed.

A range of other indicators show China is struggling. Not only is the debt-laden country going through a difficult transition from infrastructure-led growth to a consumption-led economy, but a stock market bubble has recently burst and $3 trillion (£1.9 trillion) has been wiped off the value of local shares. Authorities have taken a heavy-handed approach, banning the sale of some stocks for six months and going after short sellers.

“All of those [measures] independently might not be seen as too much of an issue but bundle them all together and we are seeing increasingly nervous oversight of the Chinese economy,” McCaig says.

DEFLATION

Looking ahead, the ongoing weakness in oil is likely to spell deflation for Western economies. Black gold plays a large part in dictating inflation levels in the West. The last round of inflation data — showing the UK had zero consumer price inflation — was correlated before the latest squeeze on oil prices kicked in.“The latest fall in oil prices will push many economies including the UK into deflation in the next month or two,” says Michael Pearce at Capital Economics.

DELAYING RATE HIKES

Now experts suggest planned interest rate hikes could be delayed. “The UK is already skirting with deflation in the next couple of months and that is going to keep the Bank of England sitting on its hands,” says Neil Williams at Hermes Investment Management.Consensus in the market is for the first US rate hikes to appear in December, with the UK set to follow suit early next year. But dozens of central banks have been forced to ease policy so far this year, painting a weak global picture. “The US and UK are talking of raising rates but with 30 banks having cut rates, the way things are going those numbers are likely to increase,” says McCaig.

So…

Q: Why did it take so long for the commodities crash to penetrate the conventional wisdom?

Because it conflicted with the general theme of global economic recovery. The US was reporting lower unemployment (though a lot of analysts continued to point out the bogus nature of that stat) and Europe and Japan had begun aggressive QE programs (which always leads to more borrowing and spending, right?). So despite the occasional hiccup, 3%+ growth was a lock going forward. Consider the opening paragraphs of this July USA Today article:

The International Monetary Fund cut Thursday its projection of global economic growth in 2015 to 3.3% from 3.5% issued in April, citing sluggish conditions in the U.S. in the first quarter.

Setbacks in the U.S. – like harsh winter weather, port strikes, and downsizing in the energy sector – have contributed to slower growth worldwide, it said in its latest “World Economic Outlook” update.

While the rest of the world should pick up pace by next year, advanced economies like Germany could make headway faster than developing nations, it said.

Growth of 3.3% is not bad at all, and it remains the consensus forecast for 2016. This implies fairly robust demand for commodities, so the fact that their prices are declining was easy to dismiss as an aberration soon to be rectified by rising sales.

Q: Can there be growth, inflation and all the other good things that governments have been promising while raw materials prices are tanking?

The answer is probably no, which means the other numbers — GDP, deficits, interest rates — will have to be adjusted to conform with the commodities complex rather than the other way around.

Which in turn means that the world’s governments are about to panic. Expect some Hail Marys in 2016, including sharply negative interest rates, a serious war on cash to facilitate those negative rates, and a return to QE in the US, where the idea of raising interest rates will be quickly abandoned.

Since these policies are just more aggressive versions of what has already failed, they’re unlikely to stop the carnage, leaving the developed world with one final weapon against global deflation: a coordinated devaluation of all major currencies, probably against gold. Though it’s taking a really long time, the currency war continues to play out according to Jim Rickards’ script.

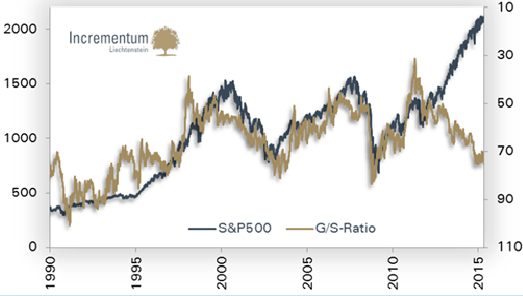

Compelling article and video interview with David Morgan, a big-picture macroeconomist. Morgan, in the video preaches patience, as well as assembles and presents the facts and information that allows him to have conviction in his recommendations and investment holdings.

One of the points he covers is revealed in the dramatic divergence seen in this chart below. Morgan interprets it as Silver being a significantly “better buy than Gold” and that this chart also reveals something else important. To find out quickly what that important fact is go HERE. In the video Morgan explains why Silver is the best inflation edge, not the best deflation hedge, and that Gold is the best deflation hedge. – Money Talks Editor

…..to read the article and view the 32 minute video go HERE

If you want to skip the article summary, the 32 min video is below:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair