Energy & Commodities

Why would oil find a bottom here? Because everyone thinks it’s going lower, is one answer. We could conjecture till the cows come home on rationales, but we would fast run out of paper and time. So I won’t. But interestingly, the move has met a symmetrical wave low (5-waves down to complete larger C) in distance and time…no guarantees. Note the divergence in the Relative Strength Index (RSI) at the bottom pane of the chart, i.e. price made and new low but RSI didn’t confirm. Of course implications for CAD here (see page 3).

Why would oil find a bottom here? Because everyone thinks it’s going lower, is one answer. We could conjecture till the cows come home on rationales, but we would fast run out of paper and time. So I won’t. But interestingly, the move has met a symmetrical wave low (5-waves down to complete larger C) in distance and time…no guarantees. Note the divergence in the Relative Strength Index (RSI) at the bottom pane of the chart, i.e. price made and new low but RSI didn’t confirm. Of course implications for CAD here (see page 3).

Please click on the link below to view:

https://gallery.mailchimp.com/dcfeb4b3bc5ba9ed1d447e92e/files/091615_oil_and_cad.pdf

Regards,

Jack Crooks

Black Swan Capital

Tomorrow afternoon the entire world will know whether or not Janet Yellen will raise the official Fed Reserve Federal Funds interest rate for the first time since June 29, 2006 — a very long nine years ago.

Tomorrow afternoon the entire world will know whether or not Janet Yellen will raise the official Fed Reserve Federal Funds interest rate for the first time since June 29, 2006 — a very long nine years ago.

And the first time it’s made any kind of move on rates since it lowered its discount rate in February 2010.

I personally think Yellen should hold off. The U.S. economy is not strong enough, foreign economies, especially Europe, are in shambles, and the dollar is already soaring.

A rate rise now threatens to derail the U.S. economy, push Europe further underwater and send the dollar soaring, worsening global deflation.

Be that as it may, today I want to clarify something I believe is very important: The myth of higher interest rates. That rising interest rates are bad for the stock market, and that declining rates are good for stocks.

If you’re like any average investor, you’ve heard that theory literally hundreds, if not thousands, of times. Tune into any media show today, and I’m sure you’ll hear it at least once, if not more.

If you’re like any average investor, you’ve heard that theory literally hundreds, if not thousands, of times. Tune into any media show today, and I’m sure you’ll hear it at least once, if not more.

Most stock brokers, and the majority of analysts and newsletter editors, espouse the same causal relationship between interest rates and stock prices.

But the fact of the matter, the plain truth, is that there is no “standard relationship” between interest rates and stock prices. Period.

Consider the period from March 2000 to October 2002, where the Federal Funds rate declined from 5.85% to 1.75%, and the Nasdaq plunged 78%.

Put simply, stocks and interest rates went down together! Exactly the opposite of what most would expect.

Or the period from March 2003 to October 2007, where the Federal Funds rate more than tripled and rose from 1.25% to

4.75% … And the Dow exploded higher, launching from 7,992 to 13,930 — a 74% gain. Stocks and interest rates went higher together!

The fact is that the relationship between interest rates and stock prices varies considerably depending upon a host of factors, including the value of the dollar, inflation and where the economy is in terms of the economic cycle.

The same myth applies to interest rates and gold: Higher interest rates, most pundits claim, is bad for gold.

But that is almost entirely wrong. Most strong bull markets in precious metals have occurred with rising interest rates, not declining rates.

There are numerous examples, the most vivid of which was the late 1970’s bull market in gold and silver which occurred simultaneously to a massive rise in interest rates. Once rates peaked, so did gold and silver.

Now, to a few other items on my list for today. No matter what the Fed decides tomorrow:

First, the long-term trends for precious metals remain down. Neither gold, silver, platinum nor palladium has bottomed. That said, don’t be surprised if you see a short-term rally.

Second, the long-term picture for the U.S. equity markets remains exceptionally bullish. That is, once the pullback that is still very much in progress is completed, probably in mid-October at much lower levels.

Third, the bull market in the U.S. dollar — and conversely, bear markets in most other currencies — remains intact.

Fourth, deflation in the commodity sector is not yet over. With the mere exception of natural gas, for every commodity I look at, my system models point still lower.

Fifth, is global unrest. Per my war models, global unrest is about to accelerate higher, yet again. Driven by the refugee crisis in Europe, by ISIS, by currency devaluations outside the U.S., by rising taxes and an increased hoarding of cash (dollar bullish by default).

Sixth, is the great sovereign-debt crisis that is about to explode onto the scene. The evidence is overwhelming now. From Trump’s popularity, in the sense that he’s an outsider vilifying career politicians, to Bernie Sanders proposing $18 trillion in new spending (where’s the money to come from?) …

To the refugee crisis, which will break the European Union’s back … to our own debt ceiling which will hit Oct. 1 …

To the patently unpayable debts and IOUs of Europe, Japan and the U.S.

So beware, the waters are going to get rough ahead, increasingly rough. But they’ll also be loaded with many opportunities.

Best wishes and stay safe,

Larry

Some major banks — which over the past few decades have grown into the biggest financial entities the world has ever seen — appear to have hit a wall, and are now shedding tens of thousands of workers. Some recent examples:

Some major banks — which over the past few decades have grown into the biggest financial entities the world has ever seen — appear to have hit a wall, and are now shedding tens of thousands of workers. Some recent examples:

Barclays plans to cut more than 30,000 jobs

(CNBC) – Barclays plans to cut more than 30,000 jobs within two years after firing Chief Executive Antony Jenkins this month, The Times reported on Sunday.

This redundancy program, which could reduce the bank’s global workforce below 100,000 by 2017 end, is considered as the only way to address the bank’s chronic underperformance and double its share price, the newspaper said, citing senior sources.

These job cuts are likely to affect staff at middle and back office operations, where largest savings are achieved, the Times said.

The paper said that a potential candidate, who would replace Jenkins, is expected to ax jobs much faster and more deeply than the ousted boss.

Deutsche Bank to cut workforce by a quarter

(Reuters) – Deutsche Bank aims to cut roughly 23,000 jobs, or about one quarter of total staff, through layoffs mainly in technology activities and by spinning off its PostBank division, financial sources said on Monday.

That would bring the group’s workforce down to around 75,000 full-time positions under a reorganization being finalised by new Chief Executive John Cryan, who took control of Germany’s biggest bank in July with the promise to cut costs.

Deutsche’s share price has suffered badly under stalled reforms and rising costs on top of fines and settlements that have pushed the bank down to the bottom of the valuation rankings of global investment banks. It has a price-book ratio of around 0.5, according to ThomsonReuters data.

Deutsche is mainly reviewing cuts to the parts of its technology and back office operations that process transactions and work orders for staff who deal with clients.

A significant number of the roughly 20,000 positions in that area will be reviewed for possible cuts, a financial source said. Back-office jobs in the group’s large investment banking division will be concentrated in London, New York and Frankfurt, the source said.

PostBank has about 15,000 positions, pointing to roughly 8,000 layoffs at Deutsche once the unit’s spinoff is completed as planned in 2016.

UniCredit plans to cut around 10,000 jobs

(Reuters) – UniCredit (CRDI.MI), Italy’s biggest bank by assets, is planning to cut around 10,000 jobs, or 7 percent of its workforce, as it seeks to slash costs and boost profits, a source at the bank told Reuters on Monday.

The planned cuts will be concentrated in Italy, Germany and Austria, several sources said, adding that they include 2,700 layoffs in Italy that have already been announced.

A UniCredit spokesman declined comment beyond noting that the bank’s CEO Federico Ghizzoni had on Sept. 3 said there were no concrete numbers on potential lay-offs, after a report said it was considering eliminating 10,000 positions in coming years.

UniCredit, which has 146,600 employees across 17 countries, is under pressure to boost its profits as low interest rates are expected to keep hurting its earnings in coming years.

Such a sudden, widespread retrenchment can mean several things:

-

Technology is making a lot of back office staff redundant. That’s reasonable and to be expected. Automation of knowledge work will be one of the big stories of the coming decade and finance is a prime target. A quick look at the growth of crowdfunding (from zero in 2009 to an estimated $50 billion in peer-to-peer loans in 2016) tells you all you need to know about the future of conventional bank lending.

-

The profitability of core banking operations is going to crater in the coming year and these guys are trying to get out in front of it — while hoping to hide the deterioration within massive workforce reduction write-offs.

-

The availability of good jobs for European college graduates — already too low — is going to shrink further. It’s virtually impossible for a finance-dependent system to grow while major banks are shrinking, so Europe will remain stuck in neutral while its governments pile up ever-greater debts and more peripheral countries join Greece on the public dole. And the euro will, at some point, be devalued suddenly and drastically.

-

The other big banks can’t be in much better shape, since they’re all operating in the same zero-interest rate, low-growth world. In the US, where auto loans have been a singular bright spot, what happens when cars stop selling? We may be about to find out. See U.S. factory output declines on sharp drop in auto production.

-

The global recovery is a mirage. Six years in, with stock and bond prices near record levels, demand for support staff in deal-driven entities like banks should be rising. Layoffs on this scale are bottom-of-a-recession events.

Add it all up, and significant Fed tightening looks like a hard sell. The opposite is much more likely.

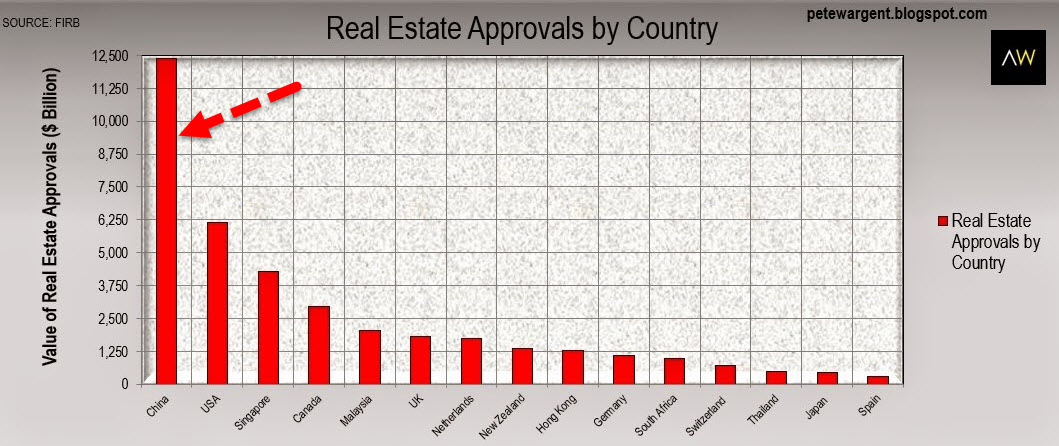

Given the recent admission by the Australian Central Bank that property prices “have gone crazy,” it appears new Chinese ‘regulations’ may just kill Australia’s golden goose of ‘weath creation’ as Aussie’s largest trade partner sees its economy collapse. While the Aussies themselves proclaimed a “war on cash,” it appears, as AFR reports, that Chinese purchases of Australian property have dropped significantly in the past month, according to agents, as buyers struggle to shift money out of the country following Beijing’s move to tighten capital controls. With Chinese banks now limiting any overseas transfer to USD50,000 – in an effort to control capital outflows – and with China dominating the Aussie housing market, one agent exclaimed, “it has affected 70 to 80 per cent of current transactions and some have already been suspended.”

As the world awaits the Fed decision this week, the Godfather of newsletter writers, 91-year-old Richard Russell, says the U.S. has a ticking time bomb, rigged markets and a desperate Fed. The legend also covered the major markets and the ultimate refuge.

As the world awaits the Fed decision this week, the Godfather of newsletter writers, 91-year-old Richard Russell, says the U.S. has a ticking time bomb, rigged markets and a desperate Fed. The legend also covered the major markets and the ultimate refuge.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair