Timing & trends

It has been 81 months, and counting. The US Federal Reserve has missed another opportunity to raise interest rates. Instead, Janet Yellen and her fellow committee members cited global economic and financial uncertainty, sidelining Fed policy for at least another month. The problem with the Federal Reserve’s decision Thursday, and in turn their decision making process is that it paves way for greater uncertainty. Furthermore, investors are now right to question the outlook for the US economy, the ongoing impact of the slowdown in emerging markets, and what the path forward is for the US Fed as Yellen made clear a rate hike could come as soon as October, or perhaps not until 2016. It will now be difficult for the Fed to avoid something they’ve worked so hard not to do, and that’s not surprise the markets.

It has been 81 months, and counting. The US Federal Reserve has missed another opportunity to raise interest rates. Instead, Janet Yellen and her fellow committee members cited global economic and financial uncertainty, sidelining Fed policy for at least another month. The problem with the Federal Reserve’s decision Thursday, and in turn their decision making process is that it paves way for greater uncertainty. Furthermore, investors are now right to question the outlook for the US economy, the ongoing impact of the slowdown in emerging markets, and what the path forward is for the US Fed as Yellen made clear a rate hike could come as soon as October, or perhaps not until 2016. It will now be difficult for the Fed to avoid something they’ve worked so hard not to do, and that’s not surprise the markets.

Without a doubt it was the recent financial market volatility, which emanated in Chinese stocks but spread all the way to US exchanges that kept the Fed on hold. Very succinctly, the FOMC statement read that they continue “to see the risks to the outlook for economic activity and the labor market as nearly balanced but [are] monitoring developments abroad.” What is meant by that statement is that with an employment rate approaching 5 per cent and GDP growth expected between 2.5 and 3 per cent, uncertainty from emerging markets is what has kept them on hold. This in turn revised their outlook lower for interest rates in the US in 2016.

This change from their most recent June meeting was their future forecasts for the federal funds rate and the path of liftoff became a lot

more gradual. The projected timeline for higher interest rates will be a lot longer than previously anticipated. This is in part to do with weak domestic inflation, but also allows the Fed breathing room between rate hikes to ensure the economy does not see tightening occur too quickly. As many have cited, recent financial market activity has had a tightening effects on the economy already. Whether it’s higher interest rates, hits to market value of equity portfolios, or the rising dollar depreciating foreign revenues, American’s are being hit with the same deflationary pressures they put on their trading partners when they embarked on quantitative easing. This deflationary dilemma could remain a substantial issue for the Fed as it keeps a lid on US inflation.

Finally, it cannot be forgotten that the idea of a hike in interest rates is based on a strengthening outlook for the economy. September 17 of 2015 was the highly anticipated date for the Fed to raise interest rates because of labour market improvement, a recovering housing market, and a recovering economy. It seems we’ve hit a snag. There is an argument with the US economy at full employment as wage growth in the labour market could jump start inflation. As there is a shortage of workers to hire and productivity increases, firms compete for labour and pay skilled workers more to retain talent. The problem with this theory is the participation rate is at the lowest level since the 1970’s and accounting for underemployment (estimated at approximately 10 million American’s) means the employment rate may be more likely to go sideways than lower. The US labour market still has further to recover.

Whether or not the Federal Reserve was right to not raise interest rates is no longer the issue from Thursday’s policy announcement. The issue is that the Fed, after years of increased transparency and attempting to deliver a clear message to the market, just became a little less transparent. Janet Yellen and her team will be hard pressed to minimize the uncertainty they created from today’s inaction. The reason is not because they didn’t raise interest rates, but when the investors have been led to expect them to raise rates, the question is why not.

What is an Exchange Traded Fund (ETF)?

What is an Exchange Traded Fund (ETF)?

Exchange Traded Funds or ETFs operate very much like mutual funds except that instead of taking in capital and issuing redemptions on a daily basis they are closed end which means they trade like a stock and are bought and sold on a normal stock exchange. ETFs can be actively or passively managed. They come in all types and at all risk levels. For our purposes, we are going to focus on passively managed indexed ETFs as a means of tracking the performance of a market, style or industry index.

How to Use ETFs?

Our discussion on ETFs will center on using them to create a passively managed segment of your portfolio. The purpose of the indexed ETF is that it tracks a particular index. For example, if you wanted to allocate 10% of a $100,000 portfolio to the TSX Composite index, then you could purchase $10,000 worth of units in an ETF like the S&P/TSX Capped Composite Index Fund which bears the trading symbol XIC. A quick look through iShares.com and you will quickly see that you have access to a wide range of indexed ETFs for virtually every industry in the Canadian market, U.S. based and global equities, as well as style funds, such as the Dividend Aristocrats Index. The same products are also available from other ETF providers such as www.vanguardcanada.ca as well as all of the major banks.

Passive Mutual Funds (Index Funds) versus ETFs

Although most mutual funds are actively managed, there is a certain class, indexed mutual funds, which provides the same type of passive stock market exposure as indexed ETFs. The difference between the two types of instruments is the structure. Indexed mutual funds are open end funds and receive contributions and redemptions on a daily basis. The fund itself manages these transactions and issues new fund units or redeems existing units for cash based on the daily calculated net asset value (NAV).

ETFs are closed end funds and maintain a consistent number of units which trade on an exchange like a regular stock. The ETF itself does not deal with contributions or redemptions on a daily basis. Just like with a stock, when you want to acquire units you buy them on an exchange and when you want to redeem you sell them on the exchange…the ETF itself doesn’t have anything to do with these transactions.

There is no clear answer for which is better – indexed funds or indexed ETFs. The open ended structure of the indexed mutual fund does require the fund to maintain a higher ongoing cash balance to ensure they can honour daily redemptions. This can create a “cash drag” as not all capital is fully invested and earning a return. ETFs don’t have to deal with daily redemptions and therefore don’t need to carry as much cash. Another interesting characteristic of ETFs is the ‘in kind’ redemption feature which provides tax deferral for unit holders. When an index fund sells stock to fulfill redemption requests, the capital gain tax liability is spread amongst the unit holders, regardless of whether or not they are redeeming. Investors in ETFs can realize return by either selling their units on the open market or by exercising the ‘in kind’ redemption, whereby they would receive a basket of securities proportional to their fractional interest of the securities owned by the ETF. For the “in kind” redemption, no tax liability is incurred unless sales from the basket of securities are made.

Understanding Discounts and Premiums

Another thing worth knowing is that because ETFs trade on an exchange, the price is determined by supply and demand and at times, ETF units can trade at a premium or a discount to their net asset value. Normally, this isn’t too much of a concern as discounts and premiums tend to be very marginal. However, it is worth noting whether you are paying a discount or a premium on the ETF when you purchase it. In general, indexed ETFs should trade at a very modest discount to their NAV.

Conclusion

Indexed Exchange Trade Funds (ETFs) can be highly efficient vehicles through which investors are able to purchase diversified exposure to an entire market index, sector, or geographic region. Benefits include a competitive fee structure, simplicity of trading, tax advantages over indexed mutual funds, and unique features such as in kind redemption. However, ETFs come in all types and risk levels and it is important that investors much understand the type of investment they are purchasing. We advocate the appropriate use of non-leveraged ETFs that are indexed to diversified indices, but warn investors against more exotic ETFs such as those that use leverage or are tied to the performance of commodities or other risky assets.

|

KeyStone’s Latest Reports Section 9/10/2015 |

Disclaimer | ©2015 KeyStone Financial Publishing Corp.

You can watch The Forecaster in it’s entirety on your computer, tablet or smart TV until Sept 30th for 1/2 price using the special MoneyTalks discount code. Just click on the movie poster image below.

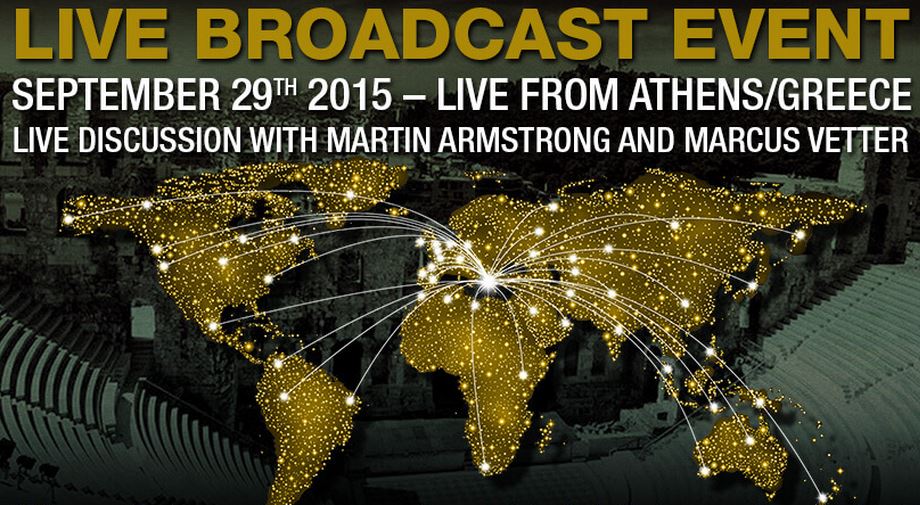

Join a live discussion with Martin Armstrong and Marcus Vetter from Athens Greece on the day prior to the 2015.75 . This live streaming event will have participants from around the world.

Join a live discussion with Martin Armstrong and Marcus Vetter from Athens Greece on the day prior to the 2015.75 . This live streaming event will have participants from around the world.

We are facing a major sovereign debt crisis in Europe beginning on October 1st, 2015 – Martin Armstrong

“THIS IS A UNIQUE OPPORTUNITY TO TAKE PART IN A WORLDWIDE HISTORICAL EVENT. NEVER BEFORE HAS THIS IMPORTANT AN ECONOMIC TOPIC BEEN DISCUSSED LIVE WITH SO MANY PARTICIPANTS JOINING IN FROM ALL OVER THE WORLD.“

Marcus Vetter

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair