Bonds & Interest Rates

Bank of Canada’s chief finally said what we had been patiently waiting for over the past several months: admission that Europe’s experiment with negative rates is about to cross the Atlantic. From Market News:

Bank of Canada’s chief finally said what we had been patiently waiting for over the past several months: admission that Europe’s experiment with negative rates is about to cross the Atlantic. From Market News:

- BOC POLOZ: NOW SEES EFFECTIVE LOWER BOUND FOR POLICY RATE AROUND -0.5%

- BOC POLOZ: CANADN FIN MKTS COULD FUNCTION IN A NEG INT RATE ENVRIONMNT

- BOC POLOZ: ‘SHOULD THE NEED ARISE’ FOR UNCONVENTIONAL MONETARY POLICY, ‘WE’LL BE READY’

That, as they say, is “forward guidance” of what is coming.

And what is coming, is also precisely what Keith Dicker from IceCap Asset Management said in his latest monthly letter, would happen in Canada in the very near future. To wit:

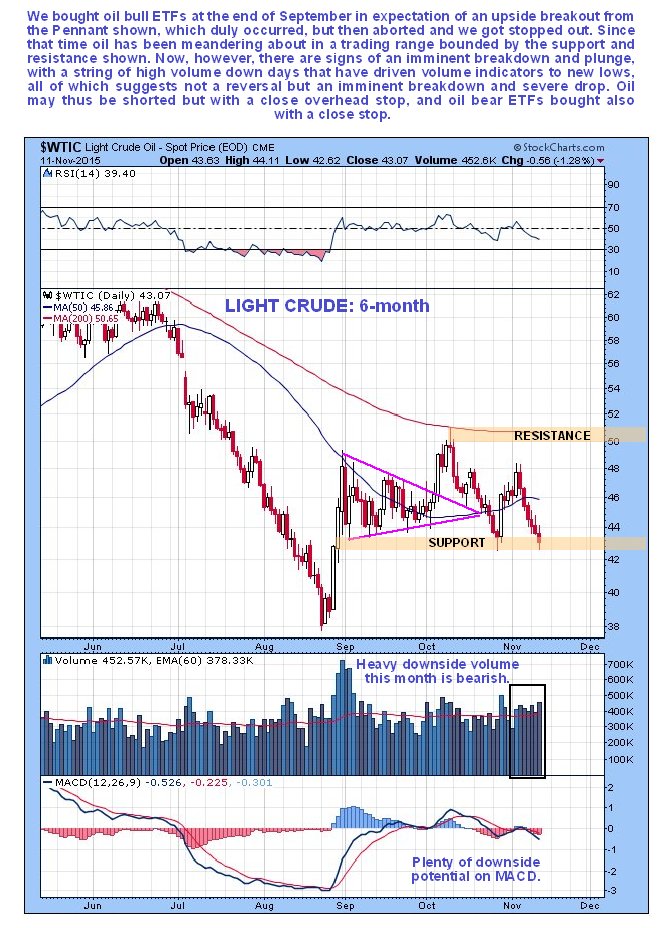

Going on price alone you may be tempted to think that oil is a buy here, after dropping for 6 days in a row, as we can see on the 6-month chart for Light Crude shown below. However, the volume pattern looks bearish. The drop so far this month has been on heavier than normal volume which has had the effect of driving volume indicators to new lows – way below where they were at the August trough. This persistent heavy downside volume implies that oil is on the verge of crashing this support and dropping much more steeply, and at the time of writing it appears to be, with the broad market dropping hard too.

I’ve got to hand it to the majority of pundits out there. They just never learn or think for themselves. They keep dishing out the same nonsense, over and over again.

I’ve got to hand it to the majority of pundits out there. They just never learn or think for themselves. They keep dishing out the same nonsense, over and over again.

For instance, the notion that rising interest rates will kill off equity market gains, particularly in the United States … or choke off a real estate recovery … or kill the gold market for good — is a myth. Period.

It might be true if interest rates were at record highs and well above the rate of inflation. But they are not. Interest rates are at or coming off of historic record lows in many parts of the world, and there is no inflation to speak of. There is the opposite, deflation.

That’s important to understand. As rates rise from historic low levels — many investors will run for cover. But the only market that rising interest rates will truly hurt is the value of sovereign bonds.

Let’s consider real estate. Why would rising mortgage rates — at this point in the economic cycle and recovery — be bad for property prices?

They won’t be bad. For the simple reason that as mortgage rates rise, all the pent-up demand for property will come out of the woodwork and start buying — in anticipation of further increases in the cost of borrowed funds.

That’s just the property markets. Rising interest rates are also going to ultimately prove positive for equity markets. While equity markets in the U.S. and Europe remain vulnerable to a short-term pullback, over the long haul, rising rates will be a bullish factor.

It means the velocity of money turnover is improving, and it means increasing demand for credit — all of which are bullish fundamental forces for equities.

It means the velocity of money turnover is improving, and it means increasing demand for credit — all of which are bullish fundamental forces for equities.

Ditto for commodities. The notion that gold will simply rollover and die and that a new bull-market leg higher is impossible with rising interest rates, is nonsense.

Just consider the last big bull market in gold, from 1973 to 1980, when interest rates were soaring, as was the price of gold and most commodities.

Sure, inflation was roaring higher then, too. But that doesn’t negate the fact that gold soared with higher interest rates. Moreover, there have been numerous other times throughout history when gold rose along with rising interest rates.

That said, right now, most commodities still have some work to do on the downside before they bottom. But bottom they will — and they will rise again — along with rising interest rates.

Indeed, as I pen this column, gold and silver remain on target for a potential major low soon to be made or confirmed. Ditto for mining shares and platinum and palladium.

Given that we may be so close to a major low in both time and price, it’s only natural to ask if one should start aggressively buying now.

My answer: No. Wait until I give you the final major buy signal. That’s what I am personally waiting for before I load up for my family.

Best wishes,

Larry

P.S. Supercycle Trader is about to release a NEW bundle of recommendations! Click here to activate your membership in the wealth-building service that led members to 13 winners in 14 completed trades last month.

Larry Edelson, one of the world’s foremost experts on gold and precious metals, is the editor of Real Wealth Report and Supercycle Trader.

Larry has called the ups and downs in the gold market time and again. As a result, he is often called upon by the media for his investing views. Larry has been featured on Bloomberg, Reuters and CNBC as well as The New York Times and New York Sun.

– Charles Swindoll

By adopting a Negative Interest Rate Policy, the Bank of Canada is at least signaling its own preparedness for an economic crisis or a period of sustained deflation. Given the sluggish Annual Growth Rates of advanced economies in 2015 (2.1 % versus 4.2% for Emerging Economies according to the IMF) and the continued decline in the Canadian Resource, Energy and Oil Sectors (WTI at $37.51 USD today), it is probably just prudent planning for a worst case scenario.

However, if preparedness is good enough for The Bank of Canada, isn’t good enough for you and your business?

If so, here is what I recommended in a September, 2014 article in the Globe and Mail – Report on Business. I believe the course of action outline below, combined with building a strong cash position, focusing on sales expansion and leveraging the relationships with your current customers, will separate the winners from the losers in the turbulent period ahead.

When business cycles change, it may not be the end of the world as we know it, but it certainly feels like it for the unprepared business. According to the U.S. Bureau of Economic Research, since 1933 there have been 13 recessions, averaging 11 months in duration, and with a corresponding drop in GDP ranging from 18 to 2 per cent. In the same period we have experienced multiple currency crisis, stock market crashes, trade wars, stagflation, globalization, technological change, and many other types of apparent mayhem that can wreak havoc on your business, customers and market. The next downturn is only a matter of time.

Since no business owner is clairvoyant and can anticipate every conceivable calamity, hope lies in preparation. A good business leader can build in a safety margin or shock absorber, to help the company survive during periods of excessive turmoil, and then thrive while their less-prepared competitors are picking up the pieces. Great shock absorbers start with exceptional leadership, a strong financial position, a clear core competency and exceptional staff. That is not enough, since each of those factors are subordinate to human error.

However, since people are fallible, an unstructured business highly dependent on human intervention will quickly succumb to pressures outside of the status quo. In fact, maintaining the status quo can become the biggest risk, creating a pervasive sense of complacency.

The best shock absorber is a scalable business system that drives value to your customers, creates a culture of continuous improvement, supersedes behavioural flaws and constantly aligns the company with market need. To build this scalable system, do the following:

Identify: A business system is the integration of the key process steps in your business that create value for your customers by leveraging your core competency. As an example, business systems can focus on product or technology development, service delivery, design iteration or manufacturing excellence.

Select: Focus on systems that create value for the customer and drive cultural excellence. For instance, Toyota adopted the principles of Lean Manufacturing at the end of the Second World War, which propelled it to the position of largest automotive manufacturer in the world today.

Build: Start with your core process that delivers value to your customer base, and ensure it is clear, efficient and aligned with the customer need and maximizing what you do best. If you are in a highly competitive sector, start to build a new core competency focused on higher-margin business.

Iterate: Strive constantly to improve your system by measuring effectiveness, setting improvement targets and hiring external expertise that will be more critical and objective. Focus on improving the weakest link by testing and then improving.

Sustain: Put a system in place to manage the system. This could be as simple as internal audits or adding key metrics to your management review, or as comprehensive as adopting an external ISO (International Organization for Standardization) standard of practice, such as 9000 for Quality, 14000 for Environmental or 31000 for Risk Management. Be vigilant and don’t let your guard down when everything is going smoothly.

Embed: The end game is to embed this approach into the culture of your business, so it becomes something the organization is, rather than something the organization does. Link the systematic approach to compensation and recognition, and make its adoption a condition for advancement in the company. Lead by example.

Be prepared for significant push back in the short run for taking such a pedantic systems approach, but in the long run and with the benefit of hindsight, your leadership courage will be rewarded.

Putting rigorous and disciplined processes or systems in place is a thankless leadership job, but it is absolutely necessary in order to build a dominate market position and to protect you and your employees against inevitable and regular shocks.

By Eamonn Percy

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair