Asset protection

“As we enter into 2016, Western civilization, the product of thousands of years of striving, hangs in the balance. Degeneracy is everywhere before our eyes. As the West sinks into tyranny, will Western peoples defend their liberty and their souls, or will they sink into the tyranny, which again has raised its ugly and all devouring head?”

OPEC says that $10 trillion worth of investment will need to flow into oil and gas through 2040 in order to meet the world’s energy needs.

OPEC says that $10 trillion worth of investment will need to flow into oil and gas through 2040 in order to meet the world’s energy needs.

The OPEC published its World Oil Outlook 2015 (WOO) in late December, which struck a much more pessimistic note on the state of oil markets than in the past. On the one hand, OPEC does not see oil prices returning to triple-digit territory within the next 25 years, a strikingly bearish conclusion. The group expects oil prices to rise by an average of about $5 per year over the course of this decade, only reaching $80 per barrel in 2020. From there, it sees oil prices rising slowly, hitting $95 per barrel in 2040.

Long-term projections are notoriously inaccurate, and oil prices are impossible to predict only a few years out, let alone a few decades from now. Priced modeling involves an array of variables, and slight alterations in certain assumptions – such as global GDP or the pace of population growth – can lead to dramatically different conclusions. So the estimates should be taken only as a reference case rather than a serious attempt at predicting crude prices in 25 years. Nevertheless, the conclusion suggests that OPEC believes there will be adequate supply for quite a long time, enough to prevent a return the price spikes seen in recent years.

Part of that has to do with what OPEC sees as a gradual shift towards efficiency and alternatives to oil. The report issued estimates for demand growth five years at a time, with demand decelerating gradually. For example, the world will consume an extra 6.1 million barrels of oil per day between now and 2020. But demand growth slows thereafter: 3.5 mb/d between 2020 and 2025, 3.3 mb/d for 2025 to 2030; 3 mb/d for 2030 to 2035; and finally, 2.5 mb/d for 2035 to 2040. The reasons for this are multiple: slowing economic growth, declining population rates, and crucially, efficiency and climate change efforts to slow consumption. In fact, since last year’s 2014 WOO, OPEC lowered its 2040 oil demand projection by 1.3 mb/d because it sees much more serious climate mitigation policies coming down the pike than it did last year.

Of course, some might argue that even that estimate – that the world will be consuming 110 mb/d in 2040 – could be overly optimistic. Coming from a collection of oil-exporting countries, that should be expected. Energy transitions are hard to predict ahead of time, but when they come, they tend to produce rapid changes. Any shot at achieving the world’s stated climate change targets will require a much more ambitious effort. While governments have dithered for years, efforts appear to be getting more serious. More to the point, the cost of electric vehicles will only decline in real dollar terms over time, and adoption should continue to rise in a non-linear fashion. That presents a significant threat to long-term oil sales.

At the same time, OPEC also issued a word of caution in its report. While oil markets experience oversupply in the short- to medium-term, massive investments in exploration and production are still needed to meet demand over the long-term. OPEC believes $10 trillion will be necessary over the next 25 years to ensure adequate oil supplies. “If the right signals are not forthcoming, there is the possibility that the market could find that there is not enough new capacity and infrastructure in place to meet future rising demand levels, and this would obviously have a knock-on impact for prices,” OPEC concluded. About $250 billion each year will have to come from non-OPEC countries.

In a similar but more disconcerting conclusion, the Oslo-based Rystad Energy recently concludedthat the current state of oversupply could be “turned upside down over the next few years.” That is because the drastic spending cuts today will result in a shortage within a few years. To put things in perspective, Rystad says that the oil industry “needs to replace 34 billion barrels of crude every year – equal to current consumption.” But as a result of the collapse in prices, the industry has slashed spending across the board and “investment decisions for only 8 billion barrels were made in 2015. This amount is less than 25% of what the market requires long-term,” Rystad Energy concluded. The industry cut upstream investment by $250 billion in 2015, and another $70 billion could be cut in 2016. The latter figure did not take into account the recent decision by OPEC to abandon its production target, which sent oil prices falling further.

So what are we to make of this? There could be plenty of oil supplies in the future, but as it stands, the industry is massively underinvesting? This illustrates a troubling tension within the oil industry. Oil prices will be set by the marginal cost of production, and recent efficiency gains notwithstanding, marginal costs have generally increased over time. Low-cost production depletes, and the industry becomes more reliant on deep-water, shale, or Arctic oil, all of which require higher levels of spending. In many cases, these sorts of projects are not profitable at today’s prices. The price spikes seen in 2011-2014 sowed the seeds of the current bust, but the pullback today could create the conditions of another spike in the future. OPEC could be a bit too sanguine with its call for $95 oil in 2040.

At the same time, future price spikes set up the possibility of much greater demand destruction, especially if alternatives become more viable. This is the difficult balancing act that the industry must pull off over the next few decades.

One would have hoped that financial rip-offs committed by medieval princes would have been permanently shelved when liberal enlightenment ended the divine right of kings.

One would have hoped that financial rip-offs committed by medieval princes would have been permanently shelved when liberal enlightenment ended the divine right of kings.

Continuing promises by Chairman Reckless to use the “printing press”, “helicopters” and more recently “bazookas” to inflate anything should be considered startling only in the resort to honesty. Euphemisms for currency depreciations started with the original promoters of the Fed and the tout was that a “flexible” currency would prevent serious financial contractions.

Although policymakers have been convinced that currency depreciation would keep every “recovery” going, the 95 percent depreciation of the dollar’s purchasing power has exaggerated the booms and busts.

This is particularly ironical as government intervention did not prevent massive contractions such as with the commodities collapse of 1921 and with the collapse of virtually everthing after 1929. Moreover, the timing and percent declines on the 2008 crash replicated those of 1929 with remarkable fidelity. That infamous crash had replicated the 1873 example.

The establishment’s experiment in artificial money, artificial securities and artificial credit ratings culminated in the biggest credit disaster in history.

Eventually, the post-1873 contraction became so relentless by 1884 that it was described as the “Great Depression”. It lasted until 1895 when another lengthy expansion began.

The post-2007 bust has been described as the “Great Recession”. Deservedly so, and the first cyclical expansion and bull market turned into another financial bubble that can be described as the “Great Complacency”. This is now mature and vulnerable to the inevitable changes in credit markets that always seem to surprise the establishment.

Nineteenth Century liberals, so rational and principled in their views, could not have imagined the greedy craft developed by many modern governments in confiscating private money earned by productively working citizens. Are we seeing medieval financial tyranny replicated by today’s proponents of the divine right of bureaucrats? A look at history provides perspective.

Although outrageous when imposed, the passage of time makes early examples of princely finance somewhat amusing: the colourful Richard I (1189-1199) sold property to finance his joining the crusade of Peter the Hermit. Upon returning, he took it back on the pretense that originally he had no right to sell it.

The infamous King John (prompted the Magna Carta in 1215) introduced the clever plan of imprisoning and ransoming the mistresses of priests, confident that the funds he could not obtain from their greed he would from their lust.

Edward I (1272-1307) confiscated money and silver or gold plate from monasteries and churches, faked a voyage to the Holy Land and, in keeping the money, refused to go.

Edward IV (1461-1483) was described as the handsomest tax-gatherer in the country; and when he kissed a widow because she gave him more than he expected, it is said she doubled the amount in hopes of another kiss.

The fiscally sound Henry VII (1485-1509) approached wealthy families with two arguments. If the household was not extravagant in expenditure, then he attacked what they had saved by thrift; while if they lived extravagantly they were considered opulent and could afford any exaction. Named after his minister of finance, the ploy was called “Morton’s Fork”.

A broader form of wealth confiscation capable of tapping even the poor was accomplished by currency debasement and extreme examples in ripping off everyone provoked severe social disorder. No matter what method employed, financial outrage prompted the evolution of parliament as a necessary means of constraining fiscal ambitions of the governing classes.

The struggle between individual freedom and authoritarian state proceeded until the late 1600s when growing commercial wealth and political power in London began to become influential with its financial common sense. The specific event that formalized the victory over the ancient status quo was the “Glorious Revolution” of 1688, which maneuvered the pro-business and Protestant William of Orange into the British Crown and displaced James II as the last absolutist king. How refreshing this was is indicated by the oppressive politics of his and his predecessor, Charles II. Starting with the restoration of the monarchy with Charles in 1660, both kings were bribed by France to change the culture of England – consistently in an authoritarian direction. Scornful remarks by miffed establishment were similar to those directed to today’s “Tea Party”, which is pro-business and pro-family.

No matter how imaginative or despotic princely financing was, it can’t compare with the long- running compulsion to spend other people’s money by today’s bureaucrats and politicians, virtually unrestrained by the checks and balances of constitution or mainstream media.

But before expanding this point, consideration should be given to the other event that formally ended the old world, which was the beginning of modern finance with the incorporation of the Bank of England in 1694. As history shows, central banking is fine when disciplined by a convertible currency and, when not, it becomes a tool of state ambition to confiscate wealth though currency depreciation. That the dollar has lost more than 90% of its value in only 50 years exceeds most princely devaluations and, like those, has been no accident.

Indeed, the Fed’s compulsion to “print” could be an attempt to go for the final 10%. While many outside central banking would consider this as infinite folly, it is uncertain as to how long this endeavour will maintain credulity in even academic circles. Regrettably, modern financial agencies such as the Treasury or Federal Reserve System have become as corruptible as their medieval counterparts.

Fortunately, history provides some antidotes to governmental abuse of the productive sector. Short of rebellion, the most effective of course has been government and its financial agencies being forced to be accountable to the taxpayer. As for those who have wrecked the currency (also a government responsibility), Dante, in his Inferno, reserves a special place in hell for “false moneyers”.

The Anglo-Saxon Chronicles record something equivalent, albeit more temporal:

“1125 A.D. In this year before Christmas King Henry sent from Normandy to England and gave instructions that all moneyers … be deprived of their members … Bishop Roger of Salisbury commanded them all to assemble at Winchester by Christmas. When they came hither they were then taken one by one, and each deprived of the right hand and the testicles below. All this was done in twelve days between Christmas and Epiphany, and was entirely justified because they had ruined the whole country by the magnitude of their fraud which they paid for in full.” – The Laud Chronicle (E)

Fortunately, history indicates that the public will eventually figure out that no matter how beguiling the claims about currency management and taxation are, the gambit has been mainly to confiscate private earnings. They will then demand the return of sound money and accountable government.

Most “first-level investors” spent the holiday season dumping any and all fixed income holdings like expired eggnog. The Fed rate hike got in their heads, and in their panic they tossed some perfectly good funds in the return bin.

Many closed-end funds are now trading at double-digit discounts to their net asset values (NAVs). Doubleline Capital founder and famed bond guru Jeffrey Gundlach recently told CNBC that buying a fund trading at a 15-20% discount is “sort of a no-brainer.”

Reason being, you’re getting $1 worth of assets for just 80 or 85 cents. That’s free money for us calculated second-level thinkers. All we need to do to collect it is buy these issues on sale, wait for the discount to close, and collect monthly yields of 0.5% or better while we wait.

Of course there’s no guarantee that a cheap fund won’t get cheaper in the short term. But over time, the market will normalize and discounted funds will see their prices trend up towards their underlying NAVs. Fund managers can even force the appreciation by buying back their own shares.

I love watching these closed-end fund discounts because they’re clear contrarian indicators. The more investors dislike a strategy at the moment, the greater the discount they demand. The irony being that most people love chasing recent performance, which means they’re most inclined to sell a loser at the moment it’s most likely to turn around.

Another good thing about closed-end funds is that their pool of investors – and hence capital – is actually fixed. An open-end fund issues as many shares as investors want to buy. That’s great until investors decide they want out, and the manager must sell perfectly good positions for cheap to cash out fleeing shareholders.

Closed-end fund investors, on the other hand, have to sell their shares to someone else on the way out. So, these managers don’t have to worry about a capital crunch. They’ve got a set pool of money thanks to the public markets, and they can sit tight on their positions through any panic.

5 Funds With 6-10% Yields and 10-15% Upside

Looking for some contrarian income today? Here are five closed-end funds with 6% yields or better, with double-digit upside to boot thanks to their current discounts. Let’s review them from cheap, to cheapest…

The Nuveen Municipal Opportunity Fund (NIO) is a nice way to capitalize on the periodic panic that engulfs the municipal bond market. “Muni bonds” are issued by states, cities, and counties to raise money for capital projects (like public transportation and infrastructure improvements).

The fund sells for a 10.8% discount to NAV today, and pays a 6.2% annual dividend that’s distributed monthly. It’s rarely this cheap:

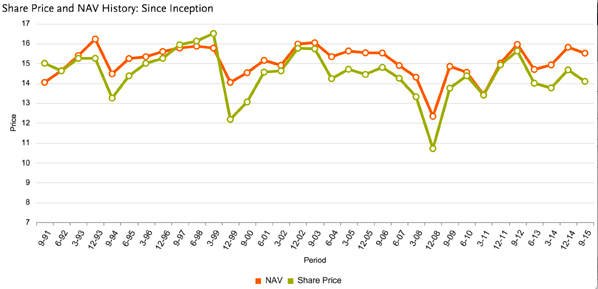

NIO Is Rarely This Cheap

The BlackRock Corporate High Yield Fund (HYT) is a direct way to make a contrarian play on the recent free-fall in high yield. It’s a 4-star Morningstar fund with an 11.4% discount to NAV – about as steep as there’s ever been since the fund’s 2003 inception.

HYT owns debt issued by companies such as Ally Financial, HD Supply, and First Data. It pays a monthly dividend that adds up to an 8.4% annual yield.

The Calamos Strategic Total Return Fund (CSQ) invests in common stock, corporate bonds, and convertible bonds. It pays a juicy 10% annual dividend and sells at an 11.8% discount to NAV.

My problem with CSQ is its high allocation (59%) to common stocks. When stocks got crushed in 2008, the fund saw its NAV fall by 45%. The next time equities see a bear market, this fund is going to follow them south.

That’s why I like to see a little more “alpha” from my closed-end fund managers. The BlackRock Enhanced Equity Dividend Trust (BDJ) fits the bill from a strategy perspective. It buys dividend payers and sells covered call options on its holdings to generate additional income.

In doing so, BDJ is giving up the upside of a stock rally (because its shares will be “called” away). But in return, it will receive a bit of capital appreciation, the dividends, and the income from the call options it writes.

The net result is a portfolio that yields 7.8% annually. After fees, the fund pays 7.4% to investors. It sells at a 12.8% discount to NAV today.

Finally you can buy your own virtual toll bridge with the Cohen & Steers Infrastructure Fund (UTF). It invests in infrastructure companies that own and operate utilities, airports, toll roads, railroads, and other physical framework.

Since inception 11 years ago, UTF has returned 7.8% annually to investors, outpacing the S&P 500’s 7% gain. It will likely outperform in the years ahead thanks to its current 8.7% yield and 16% discount to NAV.

Before You Buy, Verify The “No-Brainer”

Sometimes cheap funds are “cheap for a reason.” Do your homework, and make sure you know what issues a fund holds before you buy it. Also be sure to research management’s track record and current strategy – they’re the ones pulling the strings.

Otherwise, you might end up with a fund like CSQ that delivers yield and looks great – until a bear market hits and you lose 40% or more!

If that sounds like a lot of work, don’t worry about it. I’m wrapping up my research in the next edition of the Contrarian Income Report as we speak. I’ll highlight my favorite closed-end fund for you to buy right now. We’ll also review the best bargains in our current portfolio.

If you’re not yet a subscriber, and you’d like to receive my favorite high yield picks immediately (which pay an average of 7.1%), you can learn more right here.

As 2015 comes to an end, gold feels solid. There are many factors coming into play in 2016 that should incentivize investors to add to their positions, and do so with comfort.

As 2015 comes to an end, gold feels solid. There are many factors coming into play in 2016 that should incentivize investors to add to their positions, and do so with comfort. - Please click here now. Double-click to enlarge this daily gold chart. A week ago, I suggested gold was forming a key inverse head and shoulders bottom pattern.

- The pattern has two heads, and a bit more work may be required to complete a right shoulder in the $1062 area. Overall, I like the technical action, and Chinese New Year buying is likely the fundamental catalyst that can launch a nice January rally.

- Please click here now. Inflation is suddenly on the move in Saudi Arabia, and in a country that already embraces gold, that’s going to add to demand.

- The Saudi government has announced that the price of gasoline with an octane content of 91 will be hiked by about 66%! The government’s budget deficit is approaching $100 billion, and FOREX reserves are sinking.

- Ominously, as the financial situation of the Saudi government deteriorates, the risk of civil unrest grows. Will a terrible crisis in Saudi Arabia be the trigger of the next global financial meltdown? I don’t know, but I do know that it’s critical to own gold bullion before geopolitical risk gets out of control.

- Please click here now. Double-click to enlarge this important US dollar versus Japanese yen weekly chart.

- If Saudi Arabia does tumble into a crisis, US dollars and US bonds may not be the safe haven they were during the 2008 financial crisis. Incredibly, the dollar began losing upside momentum against the yen a year ago, in spite of unprecedented QE in Japan.

- There’s a big head and shoulders top pattern in play for the dollar on that chart, and it’s testing a major uptrend line that extends back to 2012.

- Also, Janet Yellen is trying to raise rates with experimental tools, and if her experiment fails, money could pour out of the dollar, and into gold and the yen!

- It’s important for gold investors to be proactive rather than reactive. A lot of US stock market investors were badly burned in the 2000 and 2008 meltdowns, and they reacted by buying gold. They bought general equity stocks before those meltdowns, also as a reaction, to low rates.

- Investors should only react to price changes, and do so with modest buying on declines. Price rallies should be used to “prune” holdings. Pruning a tree (very light selling) or adding fertilizer to it (very light buying) is not the action known as “trading”.

- Traders use my www.guswinger.com trading service to trade GLD & GDX very successfully, but trading needs to be separated from investing. In the big picture, Western gold market investors should think like gardeners. They can use my unique pyramid generator at www.gracelandupdates.com to systematically prune and fertilize any golden tree!

- When an investor reacts to fundamental events and perceived scenarios with sudden movements of sizable capital, the odds of achieving long term success in any asset class become negligible.

- The world has experienced many crises, and it will experience many more, until the end of time. If Saudi Arabia disintegrates into a “Mad Max” state like Iraq or Syria, it will be far too late for investors to “react” to the situation by buying gold.

- Fear trade enthusiasts should also embrace the idea that the next major crisis in the West may not be as predictable as a lot of analysts want to believe it is.

- Please click here now. India continues to move closer to a massive 80% chop in the gold import duty.

- In India, gold is traditionally the scapegoat for high crude oil imports and massive government corruption. In early 2013, the Indian current account deficit had reached almost 5% of GDP. It’s down to under 2% now, and India’s most powerful jewellers are getting very good vibes from the nation’s finance ministry. A duty chop in the next national budget appears to have a green light

- Also, the PBOC-controlled Shanghai Gold Exchange (SGE) is set to launch a gold fix around April. That’s around the same. time that India’s next budget is released. April is shaping up to be a very interesting time for gold price enthusiasts!

- The news for silver is, arguably, even better than for gold! On that note, please click here now. Indian imports of silver have been surging, and are approaching 8000 tons on an annualized basis. The import duty applies to silver as well as to gold. A chop in that duty could lead to even bigger demand for silver.

- In the Western gold community, the World Gold Council (WGC) has a bit of a bad name. A new World Silver Council is being launched, in India, and that should also help to significantly boost silver demand.

- Please click here now. Double-click to enlarge. That’s the daily silver chart.

- There’s a nice inverse head and shoulders bottom pattern in play, and a January rally would take the price of this mighty metal closer to the “AISC Threshold” for many miners. A number of Western silver mining companies have AISC (all-in sustaining costs) in the $16 area.

- Some investors may be wondering whether they should own silver bullion or the silver mining stocks. I suggest owning both assets. If Indians are buying over 7000 tons a year, Western investors should buy some too. With the launch of the WSC (World Silver Council), silver mining companies may have a new friend. 2016 will be a great year for gold, and an even better one for silver!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Dec 29, 2015

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

email for questions: stewart@gracelandupdates.com

email to request the free reports: freereports@gracelandupdates.com

Graceland Updates Subscription Service: Note we are privacy oriented. We accept cheques. And credit cards thru PayPal only on our website. For your protection we don’t see your credit card information. Only PayPal does.

| Subscribe via major credit cards at Graceland Updates – or make checks payable to: “Stewart Thomson” Mail to: Stewart Thomson / 1276 Lakeview Drive / Oakville, Ontario L6H 2M8 / Canada |

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am. The newsletter is attractively priced and the format is a unique numbered point form; giving clarity to each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualifed investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an invetor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair