Mike's Content

Get all three reports for one low price

Get all three reports for one low price

It has been a strong start to 2016 in precious metals, today notwithstanding. Gold was able to break above daily resistance at $1080 to $1090 while miners climbed higher until Friday’s reversal. Rather than focus on the nominal gains I want to turn our attention to Gold’s performance against other markets and asset classes. It is starting to turn in Gold’s favor and that is imperative if the precious metals bear market is to end in 2016.

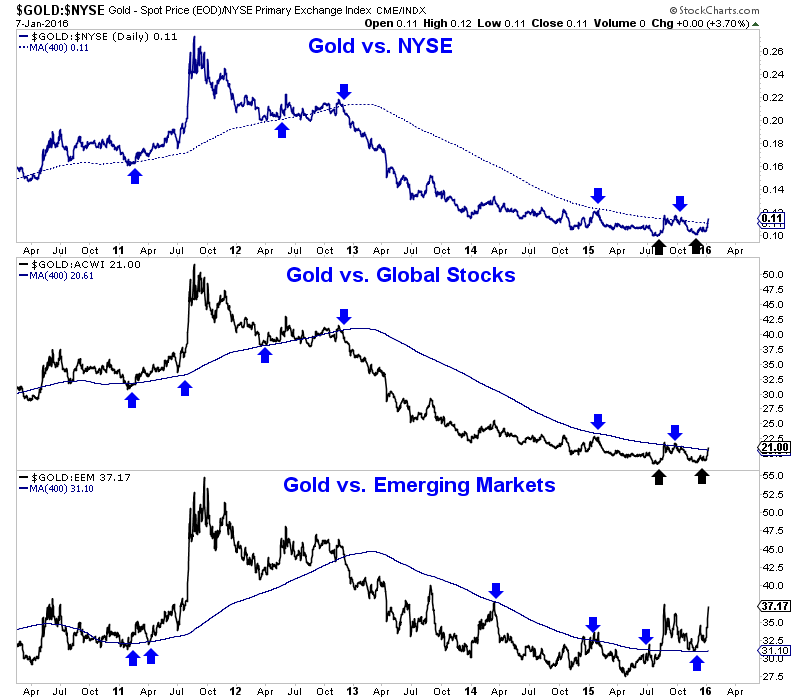

We plot Gold against various equity markets in the chart below. These are daily line charts that include the 400-day moving average. Note how the moving average has been an excellent indicator of trend. At the bottom of the chart, we see that Gold last year broke its downtrend against emerging markets. The ratio is holding well above the moving average and nearing a test of its two year high. Gold against the NYSE and global equities is more interesting. The two ratios appear to have bottomed and are in the process of transitioning from downtrends to uptrends. It may take a few months or longer but we expect it to happen this year.

Gold vs. Equities

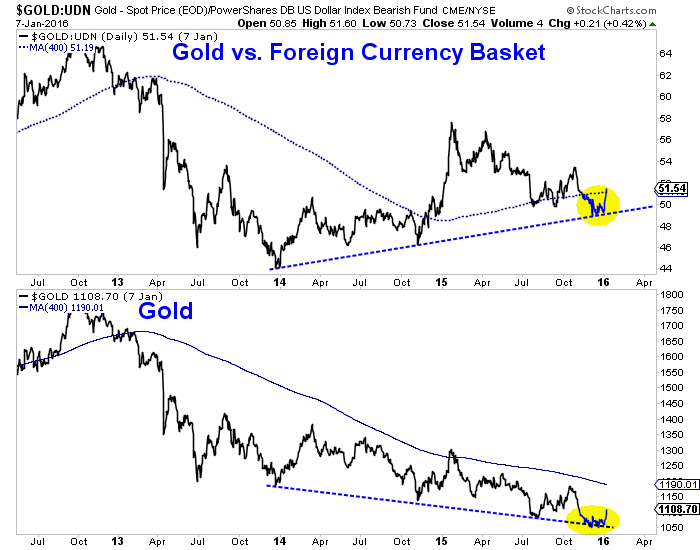

Gold’s relative strength is also apparent in the context of foreign currencies. We plot Gold against foreign currencies (FC) and Gold in US$ below. Although Gold/FC recently lost its 400-dma it rebounded after testing trendline support. Gold/FC has made higher lows over the past two years while Gold has made lower lows. This is not a total surprise given how Gold/FC has led Gold at key sector bottoms dating back to 2008, 2005 and 2001.

Gold vs. Foreign Currencies

Gold’s performance against other asset classes such as equities and currencies gives us additional insight to its current and future trend. We continue to expect the US$ to strengthen and Gold to have another leg down before its bear market ends. Gold’s performance against equities and foreign currencies can help us decipher the size and scope of Gold’s next leg down. If Gold is breaking out relative to stocks and holding strong against foreign currencies amid a nominal decline then Gold is gaining underlying strength and will be in position to rebound substantially when its nominal decline ends.

As for the short-term, we have rally targets of $1120 and $1130 to $1140 for Gold. Despite the strong decline in miners today we feel the group (GDX, GDXJ) has minimum upside targets at the 200-day moving averages. We intend to hedge our long positions when we feel the downside risk is increasing and we hope to be buyers in the event of sub $1000 Gold.

Jordan Roy-Byrne, CMT

One of the (many) fascinating things about this latest global financial crisis is that there’s no single catalyst. Unlike 2008 when the carnage could be traced back to US subprime housing, or 2000 when tech stocks crashed and pulled down everything else, this time around a whole bunch of seemingly-unrelated things are unraveling all at once.

China’s malinvestment binge is crashing global commodities, an overvalued dollar is crushing emerging markets (most recently forcing China to devalue), the pan-Islamic war has suddenly gone from simmer to boil, grossly-overvalued equities pretty much everywhere are getting a long-overdue correction, and developed-world political systems are being upended as voters lose faith in mainstream parties to deal with inequality, corporate power, entitlements, immigration, really pretty much everything. For one amusing/amazing example of the latter problem, consider Germany’s response to the mobs of men that suddenly materialized and began molesting women: Cologne mayor slammed after telling German women to keep would-be rapists at arm’s length.

Why do causes matter at times like this? Because where previous crises were “solved” with a relatively simple dose of hyper-easy money, it’s not clear that today’s diverse mix of emerging threats can be addressed in the same way. Interest rates, for instance, were high by current standards at the beginning of past crises, which gave central banks plenty of leeway to comfort the afflicted with big rate cut announcements. Today rates are near zero in most places and negative in many. Cutting from here would be an experiment to put it mildly, with myriad possible unintended consequences including a flight to cash that empties banks of deposits and a destabilizing spike in wealth inequality as negative interest rates support asset prices for the already-rich while driving down incomes for savers and retirees.

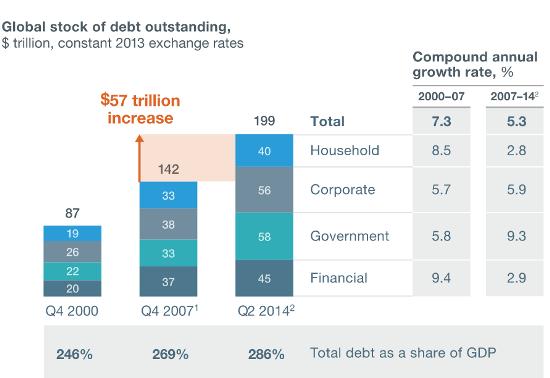

And with debt now $57 trillion higher worldwide than in 2008, it’s not at all clear that another borrowing binge will be greeted with enthusiasm by the world’s bond markets, currency traders or entrepreneurs. Here’s that now-famous chart from McKinsey:

Easier money will have no effect on the supply/demand imbalance in the oil market, which is still growing. The

likely result: Sharply lower prices in the year ahead, leading to a wave of defaults for trillions of dollars of energy-related junk bonds and derivatives.

As for stock prices, in the previous two crises equities plunged almost overnight to levels that made buying reasonable for the remaining smart money. Today, virtually every major equity index remains high by historical standards, so the necessary crash is still to come — and will add to global turmoil as it unfolds.

The upshot? It really is different this time, in a very bad way. And this fact is just now dawning on millions of leveraged speculators, mutual fund and pension fund managers, individual investors and central bank managers. Right this minute virtually all of them are staring at screens, scrolling over to the sell button, hesitating, pulling up Bloomberg screens showing how much they’ve lost in the past few days, calling analysts who last year convinced them to load up on Apple and Facebook, getting no answer, going back to Bloomberg and then fondling the sell button some more. Think of it as financial collapse OCD.

What happens next? At some point — today or next week or next month, but probably pretty soon — the dam will break. Everyone will hit “sell” at the same time and find out that those liquid markets they’d come to see as normal have disappeared and yesterday’s prices are meaningless fantasy. The exits will slam shut and — as in China last night where the markets closed a quarter-hour into the trading session — the whole world will be stuck with the positions they created back when markets were liquid and central banks were omnipotent and government bonds were risk-free and Amazon was going to $2,000.

And one thought will appear in all those minds: Why didn’t I load up on gold when I had the chance?

The bulls sure have been on the ropes so far in 2016. In fact, the Dow Jones Industrial Average just suffered its worst start to ANY year since Charles Dow first constructed the index in 1896.

The bulls sure have been on the ropes so far in 2016. In fact, the Dow Jones Industrial Average just suffered its worst start to ANY year since Charles Dow first constructed the index in 1896.

The credit markets? They had their second-worst start to a year ever. The only worse year was 2008, which you probably don’t need me to remind you was a disaster for investors.

It looked like they caught a break overnight when the Chinese market stabilized. Then at 8:30 a.m., the Labor Department released some “hot” jobs figures.

The details:

– The economy added 292,000 jobs in December, well above the average forecast for 200,000. The readings for October and November were also revised higher by a combined 50,000 jobs. That pushed full-year additions to 2.65 million, down from 3.1 million in 2014 but still a solid result.

– By industry, construction added 45,000 jobs, health care added 52,600, and even manufacturing added 8,000 positions. Temporary help jobs rose by 34,000. But mining shed another 8,000 jobs, bringing total 2015 losses to 129,000.

– By industry, construction added 45,000 jobs, health care added 52,600, and even manufacturing added 8,000 positions. Temporary help jobs rose by 34,000. But mining shed another 8,000 jobs, bringing total 2015 losses to 129,000.

– On the flip side, the unemployment rate held at 5% rather than improved further. Wages went nowhere too, with average hourly earnings unchanged from the prior month. The year-over-year rate of improvement (2.5%) missed forecasts by two-tenths of a percentage point.

Dow futures surged to as much as +220 or so after the figures came out. But they started fading shortly thereafter. After attempting a midday bounce, the Dow plunged into the close, finishing down 167 points.

Not only that, but many of the financial stocks I watch suffered huge technical breaks earlier in the week … then

took out yesterday’s lows today. The Russell 2000 Index also sank to yet another 15-month low. And several corners of the credit market continue to behave as if something bad lurks.

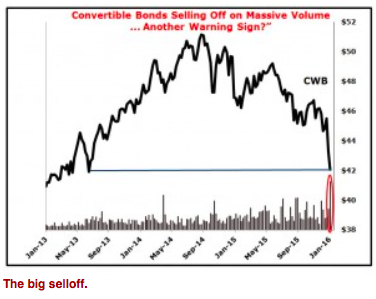

Just look at the SPDR Barclays Convertible Securities ETF (CWB), a benchmark ETF that tracks the convert market. Those are hybrid securities that share some characteristics of both stocks and bonds.

CWB’s top holdings are in sectors like pharmaceuticals, banks, techs and autos, NOT energy. In fact, energy only represents 5% of its portfolio. Yet it’s getting hammered by heavy liquidation. Excluding an anomalous “flash crash” print back in the August market chaos, it hasn’t been this low since June 2013.

So sure, the jobs figures were strong. The auto sales figures we got earlier in the week were, too.

So sure, the jobs figures were strong. The auto sales figures we got earlier in the week were, too.

But the market reaction to those news items suggests a couple of things to me: A) The problems in China, and throughout the emerging markets, are so severe, they offset U.S. domestic economic strength and B) Investors are placing bets that this is “as good as it gets,” and that the economy here will weaken later in 2016.

We won’t know for sure if those judgments are correct until later. But I think they probably are. Indeed, I’ve been worried sick about where markets are headed since last spring — and nothing I’m seeing now tells me that stance is wrong.

Just be sure to buckle up and take protective action. Specifically…

- Carry a higher percentage of cash than you did in 2009-early 2015.

- Hedge or target downside profits with select inverse ETF and option positions (at the right time).

- If you’re going to own stocks, favor non-economically sensitive stocks over growth and industrial names.

- And keep your eye on those sickly financials and the action in the credit markets. They could hold the key to where we go next.

Other Developments of the Day

– Saudi Arabia is out there floating the idea of selling shares in its national oil company, Saudi Aramco. It reportedly may list a percentage of its shares, a portion of its businesses, or otherwise take the company public in a limited fashion.

But it’s hard to see investors stepping up to the plate and buying aggressively given the fact oil prices are at 11-year lows. There’s also a lot of skepticism about Saudi Arabia’s willingness to list on major worldwide exchanges, and provide the detailed financial and reserve data it would have to in that case. Aramco has historically played its cards very close to the vest.

– European authorities believe they found the location where the Paris bombers constructed their deadly explosive devices. Belgian officials say they found materials used to put together the bombers’ suicide belts in a Brussels apartment, and have a man in custody who rented the unit.

– Chinese stocks rallied around 2% overnight after officials refrained from devaluing the yuan currency for one day, and after the government made state-backed funds buy Chinese equities.

But many investors say they’re losing faith in China’s competence, given all the flip-flopping on policy and the belief officials are just throwing things at the wall to see what sticks. Said one emerging market fund manager in a Bloomberg story: “They are changing the rules all the time now … The risks seem to have increased.”

So what do you think? Would you buy into the world’s largest oil company here? Will Europe get a better handle on terrorism in the coming months? Is China finally getting ahead of the market turmoil, or is this just a temporary respite?

Until next time,

Mike Larson

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair