Gold & Precious Metals

Click HERE or on Chart for Larger image

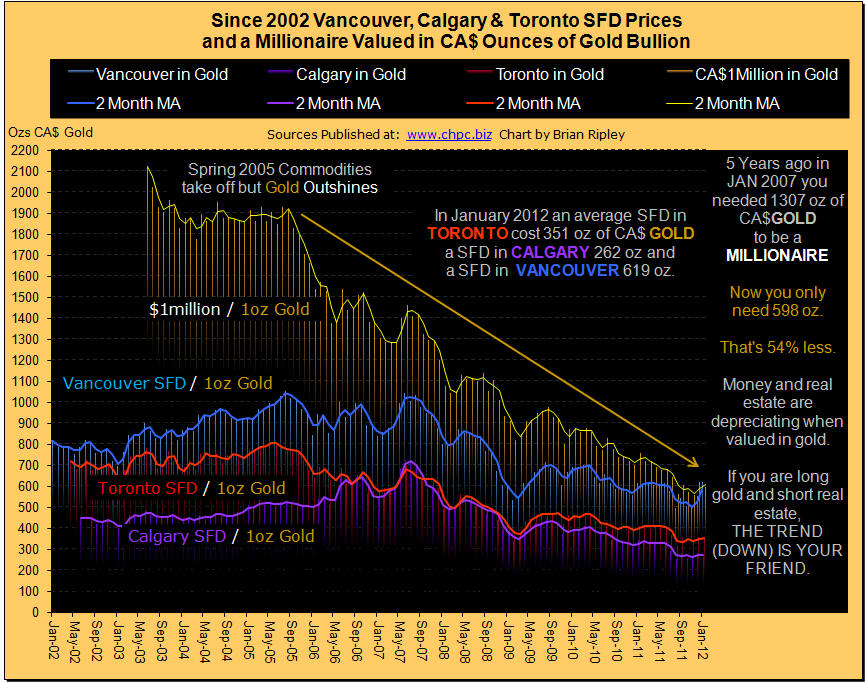

The chart above shows Vancouver, Calgary and Toronto detached housing priced in ounces of gold valued in CA$. Gold mining share prices rise as the “real price” of gold rises eg: the Gold/Commodities Ratio because the commodity cost (fuel, materials, equipment) is falling against the nominal price. See the Homestake Mining Chart from 1924 to 1935. Bullion attracts investment when credit markets contract because of its classic use as a hedge against currency depreciation and its ability to act as money. The millionaire metric allows you to see what your dollar is worth and the (declining) amount of gold you need to be a millionaire. In January 2012 the spot price of gold bounced back up causing the millionaire metric to tick back down towards trend but the sudden January data spike in Vancouver SFD prices has now priced an average house beyond that of a millionaire. Despite the Vancouver outlier, it requires 54% less gold to be a millionaire now than it did 5 years ago. See also the GOLD/CRB ratio here.

…more charts at http://www.chpc.biz/charts.html

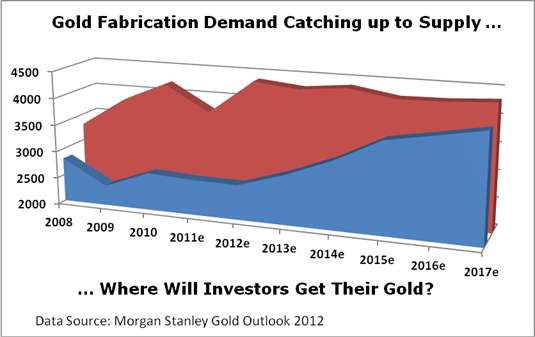

It’s a chart of gold fabrication demand — including jewelry, coin, dental, electronic and other industrial uses — that I made using data from Morgan Stanley.

In a moment, I’ll tell you why this is so important for you to know. But first, let me say that I’m not disputing its data or projection of gold fabrication demand. There’s something else to this chart. Take a look …

The red line is supply from gold mines, and the blue line is gold fabrication demand. Morgan Stanley’s numbers show that fabrication demand for gold is rising, and estimates indicate that it should soar in the years ahead. The company resolves this by saying that investment demand is going to go down. With all due respect to Morgan Stanley, I believe it has that part of the equation wrong, and the only way this demand squeeze will be resolved is through much, MUCH higher prices that force fabricators to look for substitutes.

After all, when the price of an investment — whether it’s gold or stocks or anything else — goes higher, do investors want less of it? Heck no! They usually want more — much more!

And this is exactly what I think we’re going to see in gold — a rip-roaring rally that sends gold prices much, much higher.

I have more forces that I’ll be covering in my presentation in Orlando. But even now, there are other bullish factors falling into place for gold, like pieces to a gleaming metal puzzle. Let me tell you about three important developments that will drive gold prices higher, starting with the fact that……

China’s Gold Imports Are Soaring!

China’s gold imports from Hong Kong more than tripled in 2011 from the year before, hitting a record 428 metric tons.

China does not release official data on gold imports or demand. So the Hong Kong import numbers, published by the Hong Kong Census and Statistics Department, are considered to offer a partial view of overall demand.

According to sources quoted in the Financial Times, one trader at a Chinese bank said China’s total imports last year were at least 30% higher than the Hong Kong numbers. And for 2012, analysts believe China’s gold imports are going to continue to ramp up.

Bottom line: China is going to overtake India as the world’s largest gold consumer, probably sooner rather than later. And China’s hunger for the yellow metal is going to be a major force driving gold prices going forward.

And not only are prices going up, but so is the cost to produce it. Which begs the question …

Have We Hit Peak Gold?

Steve Letwin, the CEO of IAMGold, thinks so. In an interview with Mineweb, Mr. Letwin said: “I think you hit peak gold three or four years ago. You cannot find the large deposits anymore. Most of it (is) lower-grade and in more-remote locations, so it’s going to be difficult for anybody to produce gold at less than $1,200 per ounce in terms of new discoveries.”

Ore grades are falling — from around an average grade of 12 grams per ton in 1950 to about 3 grams per ton in the U.S., Canada and Australia. Miners are now going after ore they used to drive over to get to the big deposits.

They aren’t chasing low-grade ore because it’s fun. They’re going after low-grade ore because it’s all they can find. Now, there are mines going into production with less than a gram per ton of gold, and they’re quite profitable!

Sure, there probably are some high-grade deposits waiting to be discovered. But those higher-grade deposits will be smaller — that’s why they were overlooked the first time around.

People are Losing Faith in Fiat Currency

Fiat currency is paper money — in other words, it gets its value from government say-so. And with the government creating more and more money all the time — the Federal Reserve’s latest weekly money supply report from last Thursday shows that money supply has surged yet again, by more than 35% on an annualized basis — this shakes people’s faith in the value of paper money.

So more and more people are turning to REAL money — gold and silver.

That’s why U.S. Mint sales of American Eagle silver coins were the second highest EVER in January. Meanwhile, gold-coin sales totaled 127,000 ounces last month, the most since January 2011.

But I’m not just talking about individuals. Some state-level legislators are getting so worried about the U.S. dollar, they want out. Lawmakers from 13 states — including Minnesota, Tennessee, Iowa, South Carolina and Georgia — are seeking approval from their state governments to either issue their own alternative currency or explore it as an option. Just three years ago, only three states had similar proposals in place.

Of all the state proposals circulating right now, South Carolina, Georgia, Idaho and Indiana have the best chance of passing their proposed bills this year. If those bills become law, it could have a domino effect, cutting away one of the underpinnings of the U.S. dollar’s value.

And that would be just the latest problem for the U.S. dollar. The greenback has only held its value so well in the last year because the euro looks so bad that the dollar looks downright good in comparison.

When the rug finally gets pulled out from under the dollar’s wobbly feet, the fall could shake the world as we know it.

Bottom line: Gold is Ramping up for its Next Big Move

I could give you many more reasons why gold looks so good here. In fact, I’ll be giving a bunch of them in my presentation at the World Money Show in Orlando. But whether you see that presentation or not, know this — the fuse is lit on gold.

The forces of supply and demand are lighting the fuse on gold’s next big move. You’ll want to be onboard this metal rocket when it takes off.

Yours for trading profits,

Sean

P.S. Gold is going up, but not straight up. You’ve got to pick the right companies to invest in, AND grab them at the right time so you can get the biggest-possible return.

Frankly, that’s why I think the best investment you can make right now is to join my Red-Hot Global Resources service. We just got locked-and-loaded in three potentially rocket-fueled precious-metals trades. There’s still time to get in before these names blast off. Don’t miss out – join today and get access to these new trades!

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair