Gold & Precious Metals

The recent selloff is just one of the many shakeouts that somehow manages to occur when precious metals are about to take off. For weeks we have stated that we were on the verge of a breakout at $35 in silver, $4 copper and $1800 gold. Coincidence??? Gold Stock Trades thinks not.

In 2012, we have recently witnessed a dramatic 18% move in gold from $1525 to approximately $1800 gold and silver has made an impressive 30% move from $27.5 to $37.50 since the beginning of the year. It is characteristic in gold and silver to witness short term volatile pullbacks at the beginning of major moves to shakeout the short term speculators looking for overnight riches and who lack patience and fortitude.

…..read more HERE

Peter Grandich “This an opportunity for those not yet fully invested in gold and silver. Last call! Train to pull out of the station on the way to new highs by summertime”……….. Mark Leibovit – “The bottom line here is we will still see a big move to the upside because we have a tight physical market and that’s going to cause the price to explode higher.”

GOLD – ACTION ALERT – BUY – Written 3/01/2012 by Mark Leibovit

Perhaps I had a sixth sense that something may be ‘rotten in Denmark’ when I wrote yesterday morning: “Though I am on a BUY signal, remember, chasing any market is not a wise financial practice. If you have been slowly accumulating positions all along (at all levels), there is less stress in trying to ‘catch up’ and chase prices when they are rising. The ‘boys’ have the power to pull the plug at any time. We learned that last year. I suspect the ‘big’ players (hedge funds) are also part and parcel to the current upside action. When they change their mind, watch out. I suppose NOT seeing gold and silver into new record highs this year might act as such a catalyst on their part.”

Gold prices were selling off Wednesday after Federal Reserve Chairman Ben Bernanke indicated that an additional round of quantitative easing was becoming increasingly unlikely. We experienced a ‘flash-crash’ type scenario yesterday. Short-term, a ‘Key Reversal’ and Negative Leibovit Volume Reversal patterns on some daily and weekly charts. At the worst levels, spot gold declined $106.00 measuring from Tuesday’s 1792.40 high to yesterday’s 1686.40 low. Silver declined from the morning high of 37.62 to 33.88 or $3.74.

Central planners can’t announce they are going to have constant and massive QE or everything would go to the moon. So the idea is floated around that QE3 is off the table. If gold and silver are going to head a lot higher from here, this is what you would expect the manipulators to do ahead of that move to make sure as few people as possible are on the long side. The bottom line here is we will still see a big move to the upside because we have a tight physical market and that’s going to cause the price to explode higher.

Seasonals warn of a top at the end of February for Gold and an equivalent top by mid May, so much of this may be just a cyclical phenomenon regardless of Bernanke. That said, technicals rule and until we clear highs from earlier today and/or Positive Leibovit Volume Reversals are formed, some caution needs to be exercised if you’re trading. I am in the camp that any washout (including this one) is a buying opportunity, so I remain on my BUY signal. That said, picking the exact bottom of such events is more of an art than a science – so I cannot provide you a precise downside target for this correction. Indeed, we could have seen the lows yesterday. If you believe as I do that silver is headed into triple digits (maybe high triple digits) and gold could see $11,000 an ounce in the current decade, any washout is an opportunity to do some buying.

For details the Leibovit VR Gold Letter (www.vrgoldletter.com) and the VR Forecaster (Annual Forecast Model) report which is now available at: https://www.vrtrader.com/subscribe/index.asp

After Gold’s No-QE3 Plunge, Market Clear For Another Rally

posted @ 3/01/2012 @ 4:37PM by Forbes

“What caused such a violent drop? Evidence points to Fed Chairman Ben Bernanke’s omissions regarding further easing, and QE3 specifically, in Wednesday’s Congressional testimony. Dennis Gartman and UBS’ Edel Tully agree on that, and so does the price chart. “

…read full article HERE

Opportunity Knocking

I see gold close near $1700 and silver under $35. I am travelling back from vacation in Florida and consider this an opportunity for those not yet fully invested in gold and silver. Last call! Train to pull out of the station on the way to new highs by summertime. Peter Grandich Written 02/29/12 Grandich.com

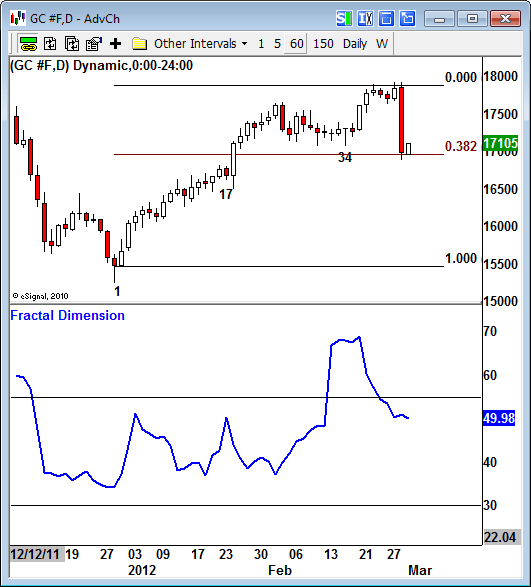

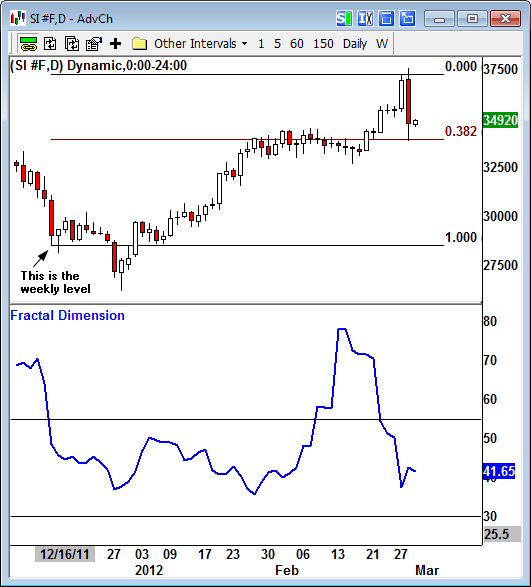

Fractal Gold Report: Flash Crash

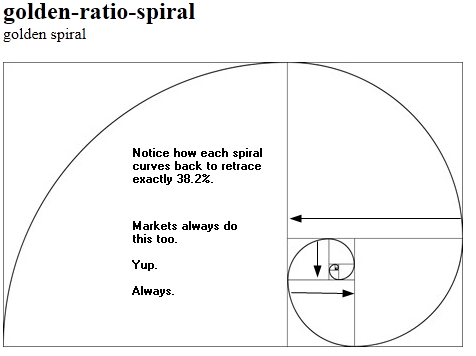

One of the really interesting things about Wednesday was how the carnage was for the most part limited to gold and silver. Other markets saw an uptick in volatility, and some scattered selling, but really nothing close to gold. Even oil came down for a 38.2% retracement and bounced right back up, and stocks didn’t really do all that much.

So what the heck happened?

It seems hard to believe, but gold did a 38.2% retracement of the entire move off the bottom in just one trading day, and almost right to the tick. Such a super-intense retracement can still be part of a bullish pattern — in fact, if the market survives such a test, this sort of hard retracement can become the impetus for a giant rebound, and a trending move that extends for weeks.

Silver also completed a to-the-tick 38.2% retracement of its full move off the bottom.

So even though it didn’t remotely resemble anything bullish, this type of sell-off can still be considered part of an ongoing bullish pattern, in both gold and silver. The problem is the size and scope of the moves in precious metals right now, as these patterns are not exactly unfolding on a “user-friendly” scale. It’s crazy out there, and that’s not likely to change anytime soon.

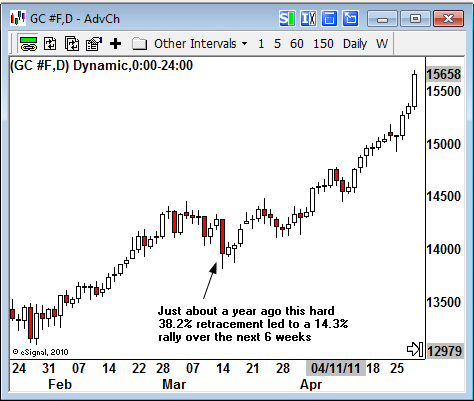

In fact, this set-up reminds me of another Bernanke-inspired sell-off about a year ago that was the direct precursor to 14% rally over the ensuing 6 weeks.

An equivalent rally from here will take gold back to the all-time highs around $1,920. But I think this could actually be the set-up for a bigger rally up to the $2,100 target area. A very hard 38.2% retracement typically triggers an even bigger response in the direction of the trend. And I can’t recall ever seeing a harder 38.2% retracement.

So it’s alarming to see gold plunge like this, but it’s definitely not over yet for this emerging pattern. However, the bullish case will suffer a major set-back, at least in the short-term, if gold sinks below $1,690 and can’t get right back over.

But if gold holds here, and especially it if quickly rebounds over $1,733, then the bullish pattern should be stronger than ever. In fact, this could be a perfect set-up for options, futures, and leveraged positions, as a market that survives and rebounds after a hard retracement will often see relentless upside pressure for weeks.

Fractal Editor’s Note: 38.2% retracements are the building blocks of every single trending move in markets, and the closest thing to a “market law” that will ever be characterized. This is because the 38.2% retracement is a component of the golden logarithmic spiral, which is based on the golden ratio and the Fibonacci series. The golden spiral is a foundational pattern for financial markets, as it is a universal shape that is infinitely scalable in both directions, both outwards and inward, which is a necessary characteristic for fractal systems like markets.

1. Ancient wisdom says, “your friend is your enemy and your enemy is your friend”. In the gold & silver market, this ancient wisdom may be particularly valuable for investors today.

2. Gold plays the role of punisher in this crisis, and punishes the debt-a-holics. The crisis is enormous, and could go on for decades, but just because the crisis may have decades to run doesn’t mean that gold rises forcefully, all the time.

3. The economy can have enormous bouts of strength while slowly disintegrating, and you have all seen the shockingly bullish economic reports pouring out, in recent months. Analysts continue to under-estimate the economic numbers.

4. Something has got to give here; either the analysts are correct and economic numbers are about to nose-dive, or the economy is surfing a much bigger up wave than the analysts comprehend.

5. You can click here to view a larger version of the current gold chart below. Note the small head and shoulders top pattern in play, and the broken uptrend line. I personally couldn’t care less about the microscopic fall in price implied by this technical action. I’m only interested in buying price sales of $100 or more.

{kind=link}

6. My interest lies with the divergence between gold and silver, and why that divergence may be occurring. Silver investors can click here for a larger version of the chart below. I’ve talked about the importance of silver investors holding your ground against “big sister gold”. Life as the little brother can be frustrating at times, but this could well be your time to shine, but not because silver is “poor man’s gold”.

{kind=link}

7. Last night the price of silver ripped thru its right shoulder high, and the price action is beginning to resemble the action of the Dow, even more so than that of gold. Click here to view a larger version of the Dow “chomping at the 13,000 point bit”. Silver’s price action in the $36 area is very similar to the price action of the Dow in the 13,000 point area.

{kind=link}

8. If we are on the cusp of an institutional capitulation, one that acknowledges that a much bigger recovery has started, then silver, platinum, and palladium could all out-perform gold.

9. If not, then silver is likely to resume its role as “gold’s sidecar”, and still fare pretty well. Platinum and palladium may not fare as well as silver if the crisis accelerates dramatically.

10. Gold appears to be silver’s best friend, but if a shocking economic revival is just around the corner, perhaps it is the supposed enemies of silver, the Dow and real estate, who will become silver’s friends, at least for a period of economic time.

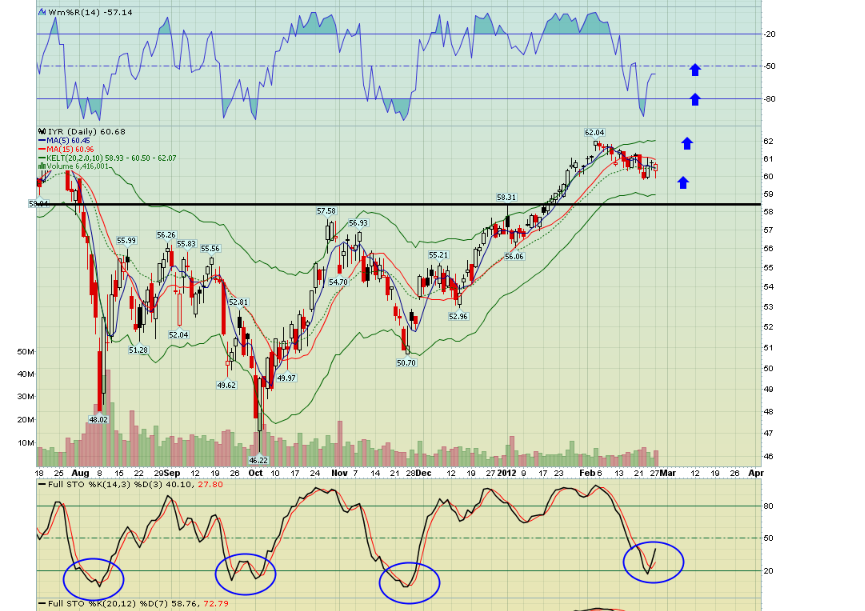

11. How big of an economic surge am I talking about? To view the shocking super-rally in real estate that I am predicting, click here for a larger chart.

{kind=link}

12. That’s the IYR-nyse real estate ETF from ishares, and I’m predicting a near-immediate rise in price to my $100 price target, a scenario that will cause 99% of the gold community to do the ultimate “double take”.

13. There’s an enormous head & shoulders pattern on the monthly chart, and the daily chart also looks extremely positive. Click for a larger chart here. Note the position of the Stochastics oscillator, and the solid support in the $58 price range.

14. Both real estate and the Dow may add surprising fuel to the silver rally, but that doesn’t mean you should buy today. Bullish price patterns reveal where price might go on the upside, but they are not buy signals.

15. It’s critical to understand that surprise is the theme of this crisis. It’s equally critical to understand that the markets are a fight more than an investment. You don’t really have “fellow investors”. You have opponents that you need to ravage and destroy. You can face that fact, or be destroyed by those who live the markets in fight-mode.

16. You can’t buy silver after it has skyrocketed, because you will be buying it from strong hands, and doing so alongside weak hands. If you don’t feel morbid when you buy, don’t buy.

17. What’s better, to feel morbid when you buy, or morbid when you sell out at a loss? Buy in the morbid zone and sell in your personal party and analysis zone. Those who want to feel good both on the buy and on the sell are likely living a pipedream.

18. If we are entering a period of shocking economic growth, albeit growth printed out of an electronic photocopier machine, then perhaps silver and other industrial-precious hybrid metals will substantially outperform gold for a period of time.

19. If real estate joins the Dow in ravaging the dollar, then gold stocks could also join silver in outperforming gold. I’m fully aware that most of the gold community is highly invested in gold stocks, with many in the community owning no gold bullion at all.

20. While the policy of holding no gold bullion is a bad mistake, that doesn’t change the fact that it could be your time to shine, if you are all-in on gold stocks. Real estate and the Dow, the gold stock community’s “enemies”, may soon become your trusted friend, for at least a period of time.

21. You can click here for a larger chart to view the GDX chart. I’m an immediate buyer at the $55.50 and $53.50 price points. Note the action around the $58 price point. GDX is attempting to blast over the red trend line. If the Dow surges through 13,000 and the IYR rips up through $61.68, I think GDX could experience a “price flash” to $70.

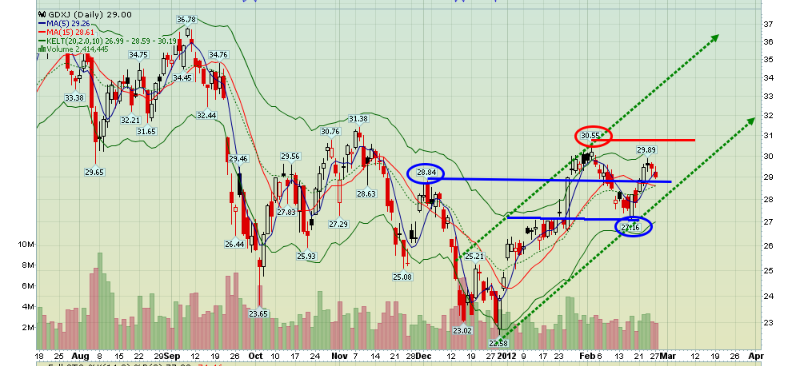

22. The incredible 35% rally in gold junior stocks, via GDXJ, has been all but forgotten, and with good reason. Most gold junior investors are 50-70% underwater, and more so in some cases. Just because the Dow investors of 1929 were wiped out didn’t mean the Dow couldn’t rise from the ashes, and it is the same with junior gold stocks today.

23. Click here for a larger chart to view the asset class most likely to continue the out-performance that it began two months ago. GDXJ has entered an uptrend channel and is showing light volume on this decline.

24. You should be an immediate buyer of GDXJ at $27.16, if you are lucky enough to see price go there. If you like gold junior stocks, stare hard into the copper, real estate, platinum, and palladium charts. Those asset classes look set to blast higher and may drastically outperform gold!

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

email for questions: stewart@gracelandupdates.com

email to request the free reports: freereports@gracelandupdates.com

Tuesday Feb 28, 2012

Special Offer for 321Gold readers: Send an email to freereports@gracelandupdates.com and I’ll send you my free “Platinum & Palladium, Your Spaceship To Mars?” report!

Graceland Updates Subscription Service: Note we are privacy oriented. We accept cheques. And credit cards thru PayPal only on our website. For your protection we don’t see your credit card information. Only PayPal does.

Subscribe via major credit cards at Graceland Updates – or make checks payable to: “Stewart Thomson” Mail to: Stewart Thomson / 1276 Lakeview Drive / Oakville, Ontario L6H 2M8 / Canada

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair