Gold & Precious Metals

On April 24 I posted a blog stating that Gold was within a week or so of declaring its next $250 move. See here.

The Gold market worked higher for about a week after the post above, reaching a high of $1,672 on May 1 (a day that became a one-day minor reversal).

Has the $250 move in Gold begun? I am not sure — but I am sure that Gold is right at the edge of the cliff hanging on by its finger nails.

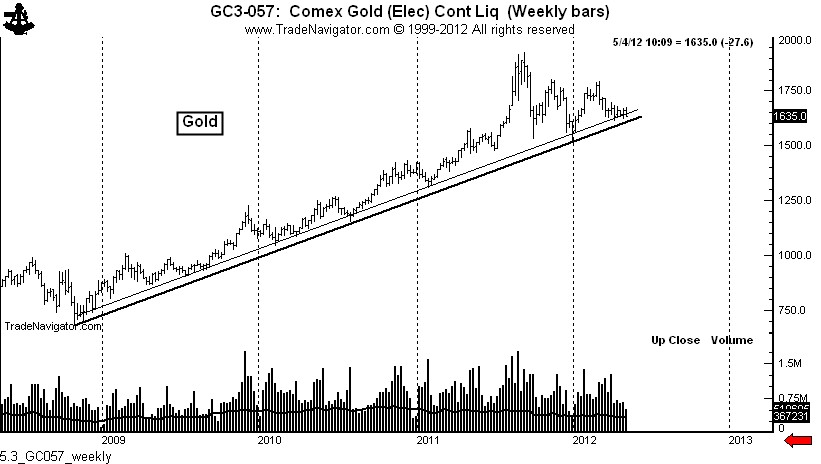

The weekly chart below of Gold shows the major trendline from the 2008 low under the orthodox lows (thick line) and through the week-end closes (thin line).

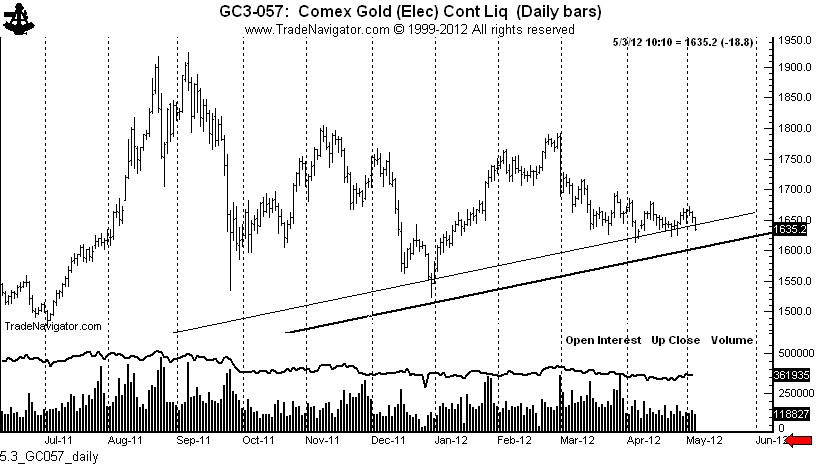

The next chart is a blow up of the previous graph — showing the two key trendlines superimposed on a daily chart.

I need to openly declare that I want to be a bull in Gold — yet I am not presently long. I accept the conventional wisdom bull story in Gold — even though I know that conventional wisdom is usually wrong.

Yet, as the daily chart shows, Gold needs to make a stand at present levels. A move below the April low at $1613 (especially if it’s on Friday) would not be good news for the bulls. Of course there is always the chance the market will spring an historic bear trap by taking out all the stops beneath the April low and immediately turning higher. But, fortunately, bear and bull traps quickly reveal themselves and provide excellent opportunities to get right with the market. Yet, as a chartist, I would have to respect a decisive violation of the trendlines just below the market.

To Read More CLICK HERE

It was Bob Prechter of Elliott Wave fame, likely among others who noted that correlations between all asset classes are quite strong during a Depression. This is true in a cyclical sense but not in a structural sense. Stocks tumbled in the 1929-1941 period while commodities, led by Gold and gold producers, increased in value. We’ve experienced similar phenomena in the past 12 years. Cyclically, there has been a correlation between these asset classes. Structurally, stocks have been in a bear market and resource sector has been in a bull market. The driving force has been a weak economy and bear market which usually leads to more inflationary policy, which in turn benefits the resource sector. Are we soon to see a replay of this scenario?

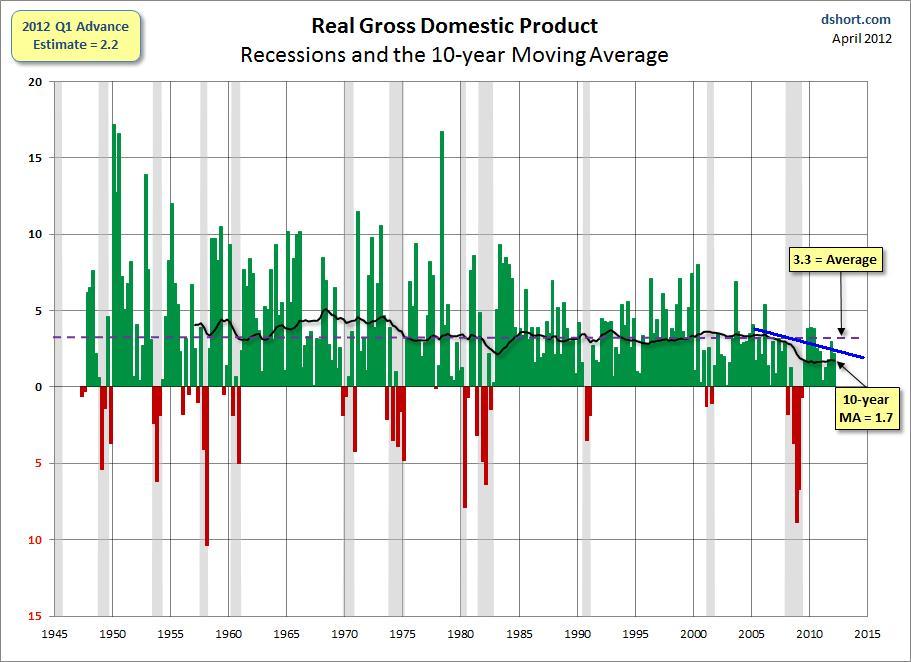

Despite unprecedented monetary inflation, stimulus and bailouts, the economy has barely recovered. The chart below (from Doug Short) displays post-war real gdp growth. The black line shows the 10-year average which has been in a steep decline since 2006. At the time, the Bush II recovery was the weakest on record. It has been surpassed by a pathetically weak recovery (statistically) under Obama. The growth rate in each of the past seven quarters has been below the the 10-year moving average.

Meanwhile, economic data as a whole is okay but is currently failing to meet expectations. The Citigroup Economic Surprise Index, (economic data relative to expectations) has gone negative for the US, and the rest of the world is not far behind. Clearly, continued disappointing economic data combined with any weakness in equities would prompt more Fed action. Judging from what happened in 2010 and 2011, it is a near certainty.

To Read More CLICK HERE

Investment fund manager and author of the ‘Gloom, Boom & Doom Report’ recommends physical over mining stocks and says another move to downside of gold is possible, but worldwide printing of money assures long-term support.

Swiss-born and educated Marc Faber’s distinct voice is a common sound on CNBC and Bloomberg TV when it comes to big-picture forecasting in investments. The contrarian views of his “Gloom, Boom & Doom Report” often garner headlines, but Faber does go along with the crowd when it comes to pointing out the dangers of rising government debt and unabated monetary intervention. HAI Managing Editor Drew Voros caught up with Faber at his Hong Kong residence and spoke to him about gold, the Treasury market, which countries should be out of the eurozone and what an ideal portfolio allocation looks like.

Hard Assets Investor: At Inside Commodities last December in New York City, you presented a line chart that compared gold prices to U.S. federal debt and showed the parallel trajectory lines of both. With debt increasing every day, your charts say gold will keep increasing, right?

Marc Faber: People say the price of gold is in a bubble stage and it is up substantially from the lows in 1999, which was, at the time, around $252 per ounce. But at the same time, we had an explosion of debt, not just government debt, but private sector debt, and an explosion of unfunded liabilities such as in the pension fund industry, and not just with Medicare, Social Security and Medicaid.

So now, 12 years after the gold’s low, we are essentially in a situation where maybe the price of gold should be much higher because the economic and financial conditions are worse than they were 12 years ago. I go to lots of conferences and I usually ask the audience, “How many of you own gold?” Normally, hardly anyone owns it. I’ve been to conferences with thousands of people attending, and nobody owned any physical gold.

I doubt we are in a bubble stage. When you went to an investment conference in 1989, everybody owned Japanese stocks. And in 2000, everybody owned tech stocks. That is the bubble, when the majority of market participants own an asset. I think there are more people that own Apple stock than gold.

HAI: What’s the biggest influence on gold right now? Is it all this sovereign debt?

Faber: We had the big move. The gold price overshot when it went to $1,921 on Sept. 6 last year. And then we oversold on Dec. 29, when gold went down very quickly to $1,522. I suppose around this level, gold’s price is moving sideways. I wouldn’t mortgage my house expecting prices to go up. They could still go down more and we would still be in a bull market even if gold prices dropped to $1,200/oz, although that’s not in my forecast.

I’m telling every investor, in the long run, that central banks all over the world are going to print money because they know nothing else. The purchasing power of currencies will continue to go down. In other words, the price of gold and silver will move up in the long run.

HAI: Why are central banks becoming net buyers of gold?

To Read More CLICK HERE

Dear Readers,

BIG GOLD’s Jeff Clark recently caught up with Charles Oliver, the senior portfolio manager of the Sprott Gold and Precious Minerals Fund (SPR003, Series A; unavailable in the US). He made a splash with a gold-price prediction four years ago that didn’t quite come true, with consequences that have created a new legend for the man, as you can see below.

That amusing episode now behind us, we have to say that we like and respect Charles, so Jeff interviewed him to learn what he sees coming next. Charles also discussed the lag in gold stocks and what may turn them around, the possibility of companies hedging their production, why he’s bullish on silver, and more.

I’m actually with Jeff now, in Florida at our Recovery Reality Check Summit, where we are both doing our best to add value for participants as well as keep the next issues of BIG GOLD and Casey International Speculator on track for publication this week. The speakers are doing a fantastic job – Doug was as feisty and funny as ever, Rick Rule as precise and eloquent as ever, and David Stockman was highly informative, persuasive, and entertaining… a great show all around, so far. If you were not able make it, I do encourage you to order the recordings of the sessions.

Sincerely,

Louis James

Sprott Fund Manager: “Gold Stocks Are the Cheapest I’ve Ever Seen”

Jeff Clark: Charles, I understand you lost a bet predicting the gold price.

Charles Oliver: Yes, I did. I made a bet four years ago at one of my first meetings with Sprott clients. Gold was trading just over $920 an ounce, and I told them it was going to $2,000 in the next four years and that if I was wrong, I would shave the hair off my head. Well, we got close, but a bet is a bet, so on April 16 my hair was shaved on BNN.

Jeff: Very honorable, holding up your end of the deal. I understand you raised money for charity, too.

Charles: Yes, as part of the event I put together a charity program, and we’ve raised about a million dollars so far. I personally donated $100,000, because if I’m going to ask everybody in the mining industry who’s benefited from this rise in gold and silver prices to give, then I have to put up my own money, too. We actually have four different charities – a quarter each to World Vision, Care Canada, UNICEF, and Terry Fox, which people can read about at the link.

Jeff: So how about going on record and making another bet where gold will be four years from now?

Charles: [chuckles] You know, I’ve just lost all my hair, and I’m thinking before I make any new bets I’ll wait until gold actually gets to $2,000. I’m optimistic that will happen this year, though.

Jeff: Gold has been stuck in a trading range since last September. In your view, what’s kept the price from advancing?

To Read More CLICK HERE

By John Mauldin

There are times, my friends Michael Lewitt and Dr. Lacy Hunt agreed today at lunch, when the study of economics is best informed by a sound knowledge of history. Indeed, Michael’s son wants to follow his father into the finance world, and Michael is starting him off in history. I have spent hours listening to Lacy stroll through economic history, detailing the path of economic thought from Fisher to Kindleberger to Minsky. The last few days have been one of those times when I realized how much I don’t know and how much more there is to learn. Not only Lacy and Michael are here in Florida, but a long list of bright minds to learn from. James Rickards, who has recently written the tour de force book Currency Wars, Harry Dent, Doug Casey, Porter Stansberry, Greg Weldon, and John Williams of Shadow Stats, with whom I look forward to meeting (do I have questions for him!). And so many more.

And it is because I simply have to stop, listen and learn (and visit with friends) that this week I will kind of take the weekend off and instead send you one of the more remarkable essays I have read in a long time. It is a speech by Jim Grant to the New York Federal Reserve. The always erudite Grant takes us back in time to the very beginnings of the Federal Reserve, to show us how far we have strayed from the original intent. I really think you should read this. I have perused it several times and intend to read it yet again – and then some more.

Grant argued for a return to the gold standard in the very halls of fiat money! It seems the New York Fed is asking some of its critics to come and speak. I have read some of the speeches, but this is the best so far for several reasons, not the least of which is that it contains some very funny lines. If you find yourself invited to the lion’s den, Grant seems to think it is best to make fun of their teeth! You really do have to admire his courage. I think I would be a little concerned that I might be on the menu!

I will make a few comments at the end of his speech and then note some upcoming speaking events in Atlanta and Philadelphia. But let’s jump straight away into today’s main event.

A Piece Of My Mind

By Jim Grant

My friends and neighbors, I thank you for this opportunity. You know, we are friends and neighbors. Grant’s makes its offices on Wall Street, overlooking Broadway, a 10-minute stroll from your imposing headquarters. For a spectacular vantage point on the next ticker-tape parade up Broadway, please drop by. We’ll have the windows washed.

You say you would like to hear my complaints, and, on the one hand, I do have a few, while on the other, I can’t help but feel slightly hypocritical in dressing you down. What passes for sound doctrine in 21st-century central banking—so-called financial repression, interest-rate manipulation, stock-price levitation and money printing under the frosted-glass term “quantitative easing”—presents us at Grant’s with a nearly endless supply of good copy. Our symbiotic relationship with the Fed resembles that of Fox News with the Obama administration, or—in an earlier era—that of the Chicago Tribune with the Purple Gang. Grant’s needs the Fed even if the Fed doesn’t need Grant’s.

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair