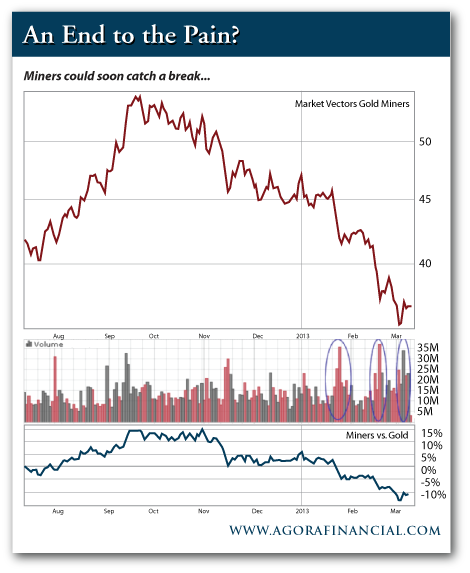

Today, a lot of mines are mining above the reserve grade. If a mine is doing that, it can only mean that over the longer term the average grade on that mine is coming down, with resulting higher costs.

The biggest cost driver in the gold industry is falling grades. Grades have come down from 7–8 grams per ton (7–8 g/t) in the 1950s and 1960s to less than 1 g/t. Of course, technology developments, like heap leaching, have helped us mine lower grades.

At the same time, the new mines are being built in the middle of nowhere. I nearly fell over backward at the cost of one mine in Ghana. Diesel fuel accounted for 50% of its production costs because all of its power had to be provided by diesel generators—on a deposit mining just 2 g/t.

TGR: When you first put this chart together, the obvious strategy was to overweight the “better free-cash-flow generators.” Now that the gold price has fallen, where does that leave that strategy?

JB: With the gold price being so close to the free cash flow price, investors need to do their homework. You cannot put all gold companies into one basket. There are huge differences in geography, risk profile, geology. There are hydrothermal deposits, deposits with copper as byproduct, gold-silver deposits. You need to go through the technical side of the company if possible, visit the mine and speak to management, geologists and mining engineers. Do a detailed financial analysis.

TGR: Would it be fair to call you a gold bull?

JB: No, I am agnostic when it comes to the quasi-religious camps of gold bulls and bears. I would like to see a gold price that helps us maintain the industry. We do not have that today. So, to that extent, I am bullish on the gold price. It needs to be significantly higher in the mid to longer term.

TGR: Much of your group’s strategy involves what you call bottom-up analysis. Tell us more about that, as it pertains to being a stock picker.

JB: It is a very detailed analysis, including field visits. We all are geologists, mining engineers or geophysicists. We not only have degrees in these subjects, but field experience working for exploration companies or gold producers. At least three of us have been sell-side analysts, so we understand how to build very detailed financial models.

We do not invest in any companies without building a detailed financial model, generally using a discounted cash-flow analysis. The whole investment team analyzes and discusses every investment case. Once everybody is happy with the financial model, it goes into a ranking system where we compare a gold company with a copper company and an oil company and so on.

We also are very transparent with the geographic locations of our investments. We have an in-house risk system. Every country gets a mark (A, B, C or D); A is the lowest risk where we go fully invested. We do not invest in D countries. A company rated C would be a maximum of 2% of the portfolio; B companies a maximum of 5%.

TGR: There are about 3,500 publicly traded mining companies. How do you sift through all their financials, drill results and such?

JB: In many cases you can scan very quickly. For example, it does not take long to eliminate a company with an average ore body of 1.5–2 g/t on a project in the Congo and no cash.

We generally look for a buffer on the balance sheet to support the company for the next 18 to 24 months to allow for exploration. There must be good management with a solid track record.

TGR: Are some jurisdictions better understood and appreciated by the European investor than the North American investor?

JB: I think the North American investor is much better educated regarding natural resources than the European investor. I would like to speak more to North American investors, but we are a European fund, so we cannot market the fund in North America.

Having said that, North American investors generally are not well educated about Africa. They might not understand the differences among Ghana, Congo, South Africa and Zimbabwe; all of Africa gets thrown into the same basket. There is a huge risk aversion to Africa in North America. The European investor is more open to Africa.

However, North American investors are generally more open to and better educated about South America.

TGR: What did you take away from your recent trip to Africa?

JB: I noticed three trends. First, cost cutting is really coming into play in Ghana, Burkina Faso and South Africa. For example, to cut costs, companies are not putting a single dollar into exploration.

Second, in Burkina Faso projects are being downscaled. Prefeasibility studies that had already been presented are being scaled down 40–50% because the money is not there and capital markets are closed. This tells us we are looking at a reduction in production over the next few years. It also points to the importance of looking at the exploration and capital expenditures in Q1/13 quarterly results for the mid and large caps. Are they committed to their capital projects? What are they doing on the grade side?

Third, a new generation of CEOs is coming in. They will have four or five years at the helm and they want to leave that company with a big check in their pockets. The only way to get that check is to make a good return for the investors. Unfortunately, that means they will not focus on investing in exploration for future production, but on cost cutting. They will start high-grading.

TGR: You and others have identified a number of companies with high capex and sustaining capex costs per ounce. Are you willing to name names?

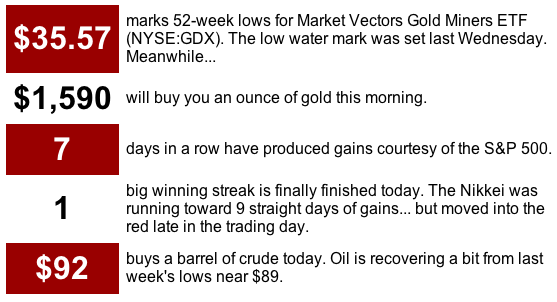

JB: Among the large caps, Goldcorp Inc. (G:TSX; GG:NYSE), IAMGOLD Corp. (IMG:TSX; IAG:NYSE) and Barrick Gold have all-in costs at $1,900/oz. They have no free cash flow.

Other companies in the mid-cap field, and even some large caps, look better. Gold Fields seems to be attractively valued on a free cash flow basis. It is producing at $1,400/oz all-in. AngloGold Ashanti Ltd. (AU:NYSE; ANG:JSE; AGG:ASX; AGD:LSE) is also attractive.

TGR: What midtier names offer value at current prices?

JB: We quite like Eldorado Gold Corp. (ELD:TSX; EGO:NYSE). The company is not the cheapest producer, but it has great exploration upside.

I also like Randgold Resources Ltd. (GOLD:NASDAQ; RRS:LSE). The company is not cheap, and you need to have a trading strategy in place if you buy. Like Eldorado Gold, it has a good track record for developing mines in difficult terrain and difficult jurisdictions.

TGR: If investors buy Randgold, when should they get out?

JB: Investors need to look at the share price, at where it fluctuates. Look at the quarterly reports, at money going in and coming out.

TGR: What positions do you have among the sub-$1 billion market-cap companies?

JB: I followed CEO Mark O’Dea, a structural geologist, from Fronteer Gold Inc. to Pilot Gold Inc. (PLG:TSX). We made a lot of money in the months before Fronteer Gold was taken out.

Pilot Gold has two big projects in Turkey, TV Tower and Halilaga, plus the Kinsley Mountain deposit in Nevada. Kinsley has a similar structural setting to Fronteer Gold’s Long Canyon, but Pilot Gold has more drilling to do.

TGR: Which of those projects excites you most?

JB: At this stage, the Turkish assets look more promising than Kinsley Mountain. I really like TV Tower. Pilot Gold might divest Halilaga for the right price.

TGR: Could it not develop both?

JB: I doubt it. It would have to raise capital. It has enough cash for exploration, but not enough to build two mines.

TGR: What do the drill results tell you about TV Tower, especially in the KCD zone?

JB: The results show some fairly high-grade cores, all located around the same bore hole. Producing core bulk of 4–5 g/t within 100 meters of the previous bore does not extend the deposit. The company needs to do some drilling that defines a bigger resource.

TGR: Is it meaningful to European investors that TV Tower is on Europe’s eastern edge, or do they just want the best?

JB: They want the best. European investors understand gold in Turkey as well as they understand gold in South Africa or in the Carlin Trend. They care about general risk, and Turkey is not perceived as a country with too high a risk. If this deposit were in Zimbabwe or Ecuador, they would have more questions.

TGR: Any other small-cap names you want to talk about?

JB: We like Torex Gold Resources Inc. (TXG:TSX) in Mexico. The company’s Morelos project is one of the few really high-grade deposits. It is a skarn deposit and recent drill results are shooting the lights out. There also are deposits south of the river. When we visited, it was obvious that the deposit is not confined to Morelos.

There are two issues here. The biggest is political risk. There are some drug bands and crime in the area. The Mexican army is there and Torex has hired security companies. The other issue is whether Torex can build the mines itself. So far management has done well. Torex is well capitalized and has already raised most of the money it needs.

TGR: Torex recently took out a $250 million ($250M) line of credit backed by five banks. Do you prefer to see that rather than an equity issue?

JB: At the current price, definitely. The company recently did another $380M bought-deal financing on top of that. At current equity prices, if a company can secure bank financing at attractive rates, I prefer a bank deal to an equity raising. Equity raising is very expensive.

TGR: How did Torex get the bank financing?

JB: As I recall, it was done by BMO Capital Markets. A bank typically will do its due diligence on such projects. There is still money available for high-quality projects. The taps are not as closed as they were in 2008.

For example, look at Aureus Mining Inc. (AUE:TSX; AUE:LSE) in West Africa. The banks are actually lining up to finance it with no hedging required. Generally, when a bank provides a loan to a gold miner, it wants hedging in place. Hedging and other obligations linked to a bank loan generally reduce the profitability of the project in the longer term.

TGR: Do you have a position in Aureus?

JB: Yes, we do. We have confidence in CEO Dave Reading, who had been the CEO of European Goldfields Ltd., which was taken over by Eldorado Gold.

In November 2012, Aureus closed an $18M offering and it can probably attract cash. Management has a good track record and the company has an interesting, doable project in West Africa. This is a bit of light at the end of the tunnel.

TGR: The project you are talking about is in Liberia, right? What about jurisdiction risk?

JB: Yes, it is in Liberia. The project is close to infrastructure. The new government is looking for investment. It wants mining to take place.

TGR: Do you have one more name in the small-cap space?

JB: I like Continental Gold Ltd. (CNL:TSX; CGOOF:OTCQX) in Colombia. It has a hydrothermal deposit, with strong exploration upside. The latest drill results support our view that it is open at strike and there seem to be a few parallel structures adjacent to it. Everything being equal, you want to be in the high-grade deposits. Continental Gold is one of those deposits.

The company is well financed and has cash on the balance sheet. Management is well respected; we know the team and adviser Greg Hall well.

TGR: Its resource in all categories is currently 5.9 Moz. How much higher might the next resource estimate go?

JB: Continental Gold has to do in-fill drilling and move the Inferred resource into Measured and Indicated. It is important for the company to issue a prefeasibility study and a feasibility plan and get into production.

TGR: Jamie Spratt at Clarus Securities models production of 225,000 oz (225 Koz) per year, generating cash flow in the neighborhood of $337M at $1,500/oz gold. What do you think of those numbers?

JB: We are playing around with 200–300 Koz production. Mining costs are the big question. In that part of Colombia, mining costs are probably at $70–80/ton. Given that it is hard ore, you need to add $40/ton for milling. Once you add G&A expenses, you have a mine that can produce cash flow relatively easily.

Deposits like Torex and Continental Gold—high-grade deposits, close to infrastructure—are scarce and that makes them potential takeover targets. I would be surprised if these companies have not signed confidentiality agreements with some of the bigger players.

TGR: Other exploration projects in Colombia have defined ounces in the ground, but none has advanced to production. Will Continental be the first?

JB: Definitely not. We were invested in Ventana Gold Corp. and Galway Resources Ltd. Both were taken out by Eike Batista and are private now. But they are further along than Continental. They are building mines, but are very secretive about it.

TGR: Will Continental be the first public company? The Colombian government has not been generous with mining licenses, has it?

JB: That is a problem. I was very impressed when I visited Colombia two years ago. I was expecting a drug dealer on every corner in Bogota. I was worried, but it was pleasant to speak with the mining geologists and CEOs. They all agreed that Colombia is a great country to operate in.

The government wants mining. Geologically, Colombia is a prosperous area. At one point, the northeast part of South America was hanging onto West Africa. Both regions are of the same age and have the same kind of deposit. The same is true of Guyana, where I saw the same rocks that I saw in West Africa.

Of course, there is risk. There is no guarantee of getting a mining license or of the taxes staying the same. But you have that everywhere. That is part of the game we play.

TGR: What one message do you want investors to take away from our interview today?

JB: Our industry needs to take risk. Companies are not investing to develop the new mines that will be needed to create and produce gold over the next 10 years.

We cannot sustain the industry if the current level of risk aversion continues, and mining companies are pressed to pay more dividends and cut costs. We need to maintain production and put risk capital into the market. We cannot have a short-term view on capital gains, dividend yields and so on.

TGR: How does a retail investor prosper today?

JB: There is only one way: Do your homework.

If you are not a real specialist on specific projects, stay with those management teams that have a good track record. Those are the teams that will go for the better-quality projects. If you are a North American investor, look to Africa and be open minded.

If everything is equal—jurisdiction, infrastructure, tax regimes—go for high grades. Those generally provide better cash flows than lower-grade deposits.

Finally, go for companies that are well capitalized. Exploration companies burning $1M or $2M a month, with no cash on the balance sheet, will not survive for long.

TGR: Joachim, thank you for your time and your insights.

RELATED ARTICLES

- Repositioning into Royalties for Richer Returns: Kwong-Mun Achong Low

- Leonard Melman: Are You Prepared for Hyperinflation?

About Joachim Berlenbach:

Is an adviser to the Earth Exploration Fund UI and the Earth Gold Fund UI. He holds a Master of Science degree in economic geology from the University of Cologne, a Ph.D. in structural/mining geology from RAU (now University of Johannesburg/South Africa) and an MBA from UDW, South Africa. Berlenbach worked for 11 years in the South African gold and platinum mining industry. Following his operational occupation, he worked for five years as a sell-side analyst in the South African investment banking industry (Standard Bank, Citibank) where he was rated best South African gold analyst in 2001 and 2002. In 2003 he co-founded the boutique Craton Capital and in 2006 he founded the Earth Resource Investment Group, which advises the Earth Funds under the umbrella of Universal Investment in Frankfurt, Germany. He is a guest lecturer in economic geology at the mining school in Freiberg, Germany, and at the University of Münster, Germany, as well as a retained speaker on mining valuations in the international CFA program.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Brian Sylvester conducted this interview for The Gold Report and provides services to The Gold Reportas an employee or as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Pilot Gold Inc. and Continental Gold Ltd. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Joachim Berlenbach: I or my family own shares of the following companies mentioned in this interview: None (only invested in the Earth funds). I personally or my family am paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Universal Investment (Frankfurt). I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

James Dines: Another Legend, Founder of The Dines Letter & Acclaimed Author will be an exciting guest for Michael and Money Talks because of his legendary bull market predictions. Legendary, because they were both correct while at the same time in complete contradiction to the rest of the financial community. In an industry where it takes courage and conviction to go against the crowd, Mr. Dines defiantly warned investors of the “invisible crash” that would bring down stocks in 1966, the unexpected gold boom of 1974, the Internet revolution of 1996, the market top in 2000, the “Coming Uranium Boom” and more.

James Dines: Another Legend, Founder of The Dines Letter & Acclaimed Author will be an exciting guest for Michael and Money Talks because of his legendary bull market predictions. Legendary, because they were both correct while at the same time in complete contradiction to the rest of the financial community. In an industry where it takes courage and conviction to go against the crowd, Mr. Dines defiantly warned investors of the “invisible crash” that would bring down stocks in 1966, the unexpected gold boom of 1974, the Internet revolution of 1996, the market top in 2000, the “Coming Uranium Boom” and more.