Energy & Commodities

Before we get started with this week’s news please take a few moments to read our latest presentation on the future of the energy sector: 5 new energy booms every investor should see right now

Before we get started with this week’s news please take a few moments to read our latest presentation on the future of the energy sector: 5 new energy booms every investor should see right now

Ukraine was set to sign a landmark trade association agreements with the European Union on 29 November, much to the dismay of Moscow, but the deal is now officially dead according to reports coming out of Kiev.

Ukrainian Deputy Prime Minister Yuriy Boyko announced today that Kiev has suspended its preparations for the signing of the EU-Ukraine Association Agreement until a “solution” can be found. Internal politics aside, at issue are industrial production decline and relations with the countries of the Commonwealth of Independent States (CIS)—both of which would need to be compensated by the European market.

One of the EU’s key conditions for the signing of the agreement was the release of Yulia Tymoshenko—at least to travel to Germany for medical treatment. Yesterday, Ukraine’s parliament rejected draft laws that would have allowed this to happen. Opposition leader and former prime minister Tymoshenko is a staunch opponent of Ukrainian President Viktor Yanukovych. She is serving a seven-year sentence in prison on abuse of office charges.

In the meantime, there has been a flurry of activity between Moscow and Kiev, including a Ukrainian pledge to readjust the payment schedule for Russian natural gas imports and address overdue payments to Moscow. Officials in Kiev are now saying they will pay $1 billion in overdue gas payments by the end of this year. Only last week, Ukraine had said it was suspending gas purchases from Russia and would instead rely on its own storage facilities, but it quickly backtracked on that.

Quite simply, there is just too much domestic political and geopolitical baggage attached to the EU-Ukraine deal, and according to Robert Bensh, senior energy advisor to Boyko and senior consultant for Cub Energy, the timing isn’t quite right.

Perhaps five years from now the climate will be more favorable for a deal and until then Ukraine will have to continue to balance relations with the EU and Russia.

Back in North America, it’s a busy week in energy as we head into the winter holidays, which promise to leave a lot of loose ends to tie off in the New Year, among them the five-year-pending approval of the controversial Keystone XL project and over 20 applications for exporting US natural gas to countries that don’t have Free Trade Agreements (FTAs) with the US.

This week has been a rather disappointing one for Keystone XL and LNG exporter-hopefuls.

First, the Freeport LNG export project in Texas saw its capacity hopes dashed by a Department of Energy (DOE) conditional approval of only 400,000 Mcf/d in LNG exports—a far cry from the 1 Bcf/d the company had asked for based on capacity and future expansion plans.

At the same time, it looks like one other project—at most—will be approved by the DOE before the end of the year, based on the approximately one month it has taken for each of the four LNG exports projects approved so far.

While some analysts were suggesting there would be a moratorium on further approvals this year, the DOE has stated that it is not suspending the approval process, but the process has been slowed because of October’s federal government shutdown.

The 16-day government shutdown “impacted our ability to move forward” on approving pending LNG export applications, Christopher Smith, DOE’s acting assistant secretary for fossil energy, said during his Senate Committee on Energy and Natural Resources nominationhearing.

Smith’s statement is more or a less a response to growing criticism from some senators that the DOW has been dragging its feet on LNG exports to non-FTA countries.

Then we have Keystone XL, the planned start-up of which has now been delayed for the second time this year, to 2016. It has become clear to TransCanada Corp. that its pipeline will not be getting approval this year, but the company remains hopeful that early 2014 will see the presidential green light. Once approval is granted, it will take at least two years for the pipeline to become operational.

In the meantime, though, the estimated costs of the project continue to climb along with the start-up delays. On Tuesday, TransCanada announced the new estimated costs of the project would be at least $5.4 billion–$100 million more than earlier estimates.

Colin Soares, CEO of Canada’s High North Resources, recently told us in an interview that Keystone XL isn’t as fundamentally important as it used to be because of huge increase in crude being transported by rail. “But from a market point of view, it’s still a big deal, and market valuations will increase with Keystone approval.”

Our analysis for readers this week comes from the Executive Report in Premium and takes a look at Egypt’s dying energy sector and the measures the interim military-backed government is trying to put things right—sort of. (The full report is below the introduction)

For those of you interested in Oilprice.com premium, we have a great letter lined up for subscribers. Dan Dicker our expert trader and legend in the oil markets takes a detailed look at the direction he believes oil prices will be heading in (This is a must read for ALL traders and analysts).

Our Opportunities letter take a look at a report recently put out by Ernst & Young which sounded a warning on the future of the E&P sector. Telling investors they need to beware of a silent killer that is stalking producers in some parts of the world. Places stock buyers should be looking at reducing their exposure. (if you have oil & gas investments in North America this is a must read report)

Our intelligence notes look at developing situations in Mozambique and Kenya and we issue our security risk rankings for East Africa.

This is another must read issue and you can do so completely free. We offer a 30 day free trial to readers in which time you will receive 30 reports that look at trading opportunities, unique investments, industry developments, geopolitical updates and much more. You can cancel at any time during these 30 days if you think our research isn’t for you.

You have no risk and need make no payment to try our premium service – we can’t be fairer than that. To find out more about how you can start a 30 day free trial – click here

That’s it from us this week.

I hope you enjoy the report below and have a great weekend.

Best regards,

James Stafford

I mention alternative energy infrequently. Mostly because I’m not convinced much of the sector is investable.

I mention alternative energy infrequently. Mostly because I’m not convinced much of the sector is investable.

One possible exception being geothermal.

Speakers at the GeoPower Latin America Conference this week in Santiago, Chile revealed some insights about the sector. Showing that it could be a viable source of baseload power. Almost.

Several industry presenters noted that geothermal plants work well once up and running. Power is available most of the time, at competitive operating costs.

The problem pointed to by all of these experts is development costs.

Drilling exploration test wells for a prospective geothermal project is expensive. These are wide-diameter holes, that require an array of specialized completions.

The whole process is somewhat akin to oil-well drilling. But unfortunately the geothermal drilling sector isn’t nearly as developed as its sister services industry in the petroleum business.

The reason is scale. Oil and gas is a big enough business that it attracts a lot of services companies. Creating intense competition and driving down costs.

But geothermal drilling is an incredibly small space. Especially today, when geothermal power is a completely new idea in many of the places globally where investors have been trying to establish projects.

This is a chicken-and-egg challenge. Geothermal developers need more services companies in order to make projects profitable. And services firms need enough projects to warrant setting up shop.

That’s a tough dilemma to solve. It may mean that geothermal will only take root in places with very high power prices–the type that can lure capital into project developments. Countries like Chile and South Africa might be candidates.

But until there are some definitive answers on this front, the sector will languish. We’ll see what the world comes up with.

Here’s to recognizing the barriers to entry,

OIl & Gas: “All Hell is Breaking Loose in the Arctic”

On days like today, I don’t have to spend much time deciding which of the dozens of teaser pitches we receive to cover — it’s unanimous, Gumshoe readers are crying out for a solution to the latest pitch from Dr. Kent Moors.

Moors is an energy expert and Duquesne professor, and he sells the expertise he’s gained as an energy consultant over the years by turning it into stock ideas that are sold through both an entry level newsletter (Energy Advantage) and an “upgrade” letter for those folks who want his very best super-secret ideas called Energy Inner Circle.

That basic strategy is not, of course, unique to Dr. Moors or to his publisher, Money Map Press — every newsletter publisher’s goal is to break even on the $39 subscriptions and use those people as the marketing pool for their super-lucrative $300 or $1,200 or $5,000 newsletters. From the comments I get this makes readers crazy (“I already paid for this guy’s information that he promised would be awesome, why is he now offering to sell me something better for a lot more money?”), but it also must work great … because everyone does it.

But anyway, most of you don’t care about this “behind the veil” stuff about newsletterland — you just want the idea, right? So let’s try to ID it for you.

Dr. Moors’ pitch is based on the Russian push to dominate the next wave of oil discovery and production in the Arctic — they got a lot of attention for planting their flag on the sea bed at the North Pole six years ago, part of a global dispute over territory in the arctic, territory that is becoming open to energy exploration and additional sea traffic partly because of receding ice and partly because of new technologies. Norway, Denmark, Canada, the US and several other countries with arctic borders are disputing Russia’s claim that it “owns” the 2/3 or so of the subsea arctic that extends North of their land mass, and the current international agreement is for a 200 mile “economic zone,” so the political squabbling will no doubt continue for a long time — and become much more vociferous if natural resources can feasibly be extracted. Moors reports the claim that 20% of the world’s oil and gas reserves are waiting to be discovered or developed deep under the northern ice, and it’s a huge area so, well, who knows?

But his big claim for this pitch is that the other pundits who recommend the arctic explorers and the oil majors who are staking claims off of Greenland or Alaska or north of Russia or Canada aren’t the best idea for making money — largely because it will take years and years before any of this bears fruit.

No, he says that the best way to profit immediately is by buying the subsea pipeline expert that can build the infrastructure for this arctic work.

Here’s a taste of the big picture tease, just to get you up to speed:

…..read more HERE (Warning, its long)

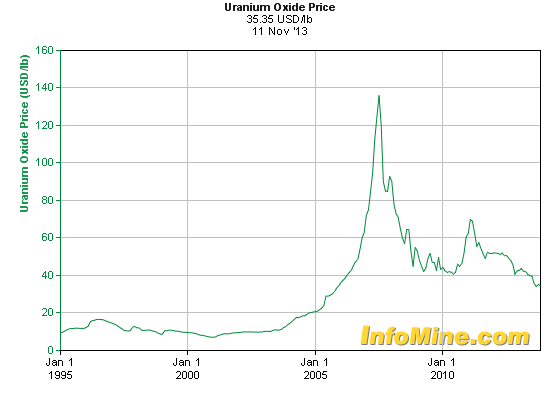

Uranium prices have been on a downward slide for half a decade now.

Trading around $35 per pound, uranium simply can’t stay this low for much longer.

Over the coming months and years, uranium prices will creep higher — and uranium companies sitting on currently undervalued deposits will offer investors tremendous upside.

Let me explain…

The Last Uranium Boom

The last uranium boom kicked off in 2005 as part of the “commodity supercycle.”

Its upward ascent ultimately peaked in June 2007 at around $140 pound. Oil would touch $145 a year later.

Commodities were already in an upward trend. But something special happened to uranium…

A new uranium mine called Cigar Lake was supposed to come online in 2007. It is the largest undeveloped high-grade uranium mine in the world.

However, Cigar Lake didn’t come online. Instead, it experienced a major flood.

With the world expecting this new source of uranium supply, prices started spiking quickly — all the way up to $138 per pound — before the popping of the housing bubble and the financial crash brought them back down. The incident at Fukushima helped keep them low.

Now things are starting to change…

Uranium demand is starting to creep back up. And with Cigar Lake still in a perpetual state of limbo, the world is starting to scramble for new supply.

The stage is set for a new uranium boom.

Why Uranium, Why Now?

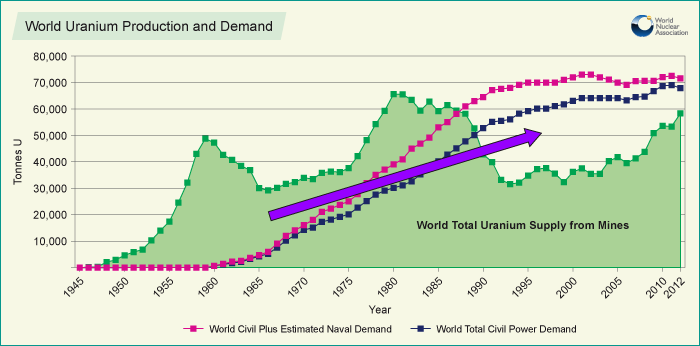

At the very basic level, there simply isn’t enough supply to meet demand.

The world’s reactors will need 65,000 tonnes of uranium in 2013; but the world’s mines will only produce around 58,000 tonnes.

Some of the difference is made up with reprocessed fuel, but a supply crunch still looms for a litany of reasons.

For starters, global electricity demand is growing twice as fast as overall energy demand. Worldwide demand for electricity will rise 75% by 2035.

Nuclear is the cleanest (no emissions) and safest (per kWh generated) than any other fuel source. It will be the go-to source for the world to provide clean baseload energy.

Even Japan is not shying away, with Prime Minister Abe calling those who want to end nuclear power in Japan “irresponsible.”

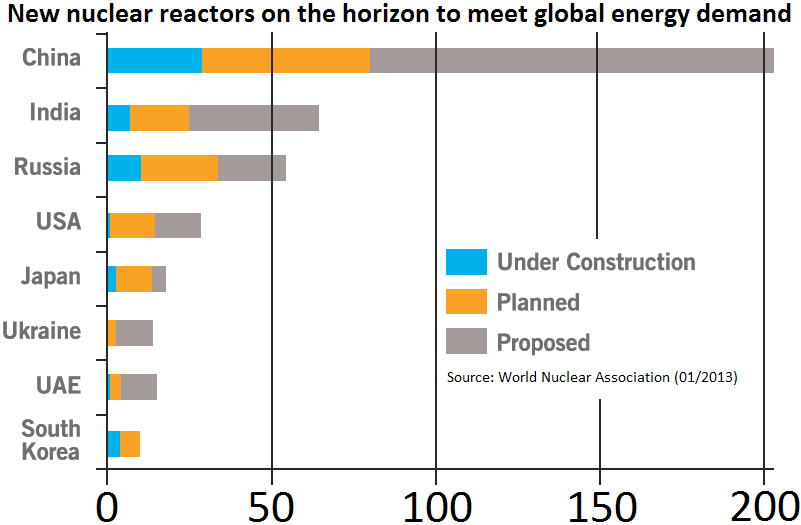

There are nearly 70 reactors under construction worldwide, more than 160 planned, and 315 proposed…

According to Rockstone Research:

A supply shortage is anticipated post-2013/2014: primary supply capacity must increase by around 90 million lbs. U3O8 in the next 6 years until 2020 only to meet demand requirements. During the last 8 years (2003-2011), global mine output solely increased by 48 million lbs…

For output to increase to meet rising future demand, uranium prices have to rise.

That’s why analyst forecasts for uranium prices in 2014 and 2015 are some 65% to 85% higher than they are today.

Lastly, some 20 million pounds of uranium per year have been coming to the United States from Russia for the past 20 years.

For reasons I lay out here, this agreement will soon come to an abrupt end, leaving a wide gap in U.S. uranium supply.

With uranium prices slated to rise some 85% in the coming two years, what’s the best way to play it?

Uranium Investing in 2014 and Beyond

Because uranium stocks typically rise 2x-4x the rate of the underlying uranium price, my money is on uranium stocks.

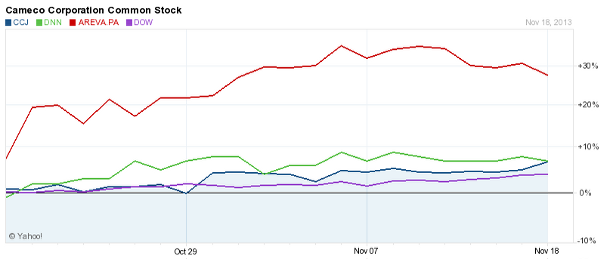

There’s a reason uranium miners like Cameco (NYSE: CCJ), Denison (AMEX: DNN), and Areva (PA: AREVA) are outperforming the market twice over (or more) since mid-October:

This is only a sign of things to come.

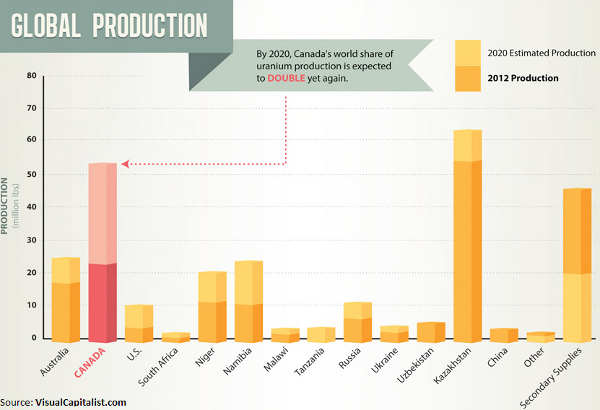

Increasingly, one region is being looked to as a large supplier of future uranium. Currently, the Athabasca Basin provides 16% of global uranium production. This is second only to Kazakhstan.

Over the next few years, though, Athabasca will be the fastest-growing area for uranium production in the word. Its output is expected to double by 2020.

This is and will continue to happen for many reasons:

- Canada is the world’s friendliest mining country;

- Athabasca is utterly underexplored, with only the eastern portion in production;

- The mines there are young and growing, and will easily outpace growth in Kazakhstan; and

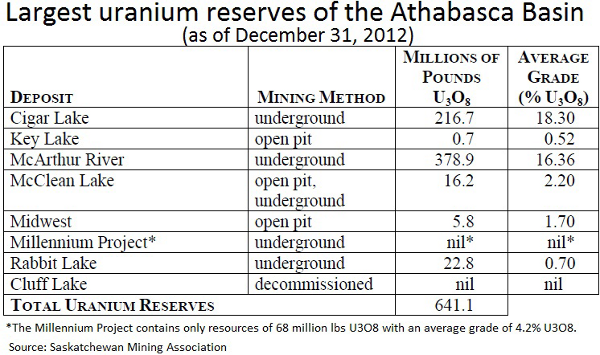

- The deposits are generally the shallowest and most high-grade in the world (10 of the 15 highest-grade deposits are in Athabasca)

For these reasons (and more, which I outline here), Athabasca is about to become the world’s uranium hotspot.

There’s already a land rush on…

A bidding war between Cameco and Rio Tinto (NYSE: RIO) for Hathor’s Roughrider deposit ended at $642 million in early 2012. Denison paid $71 million to Fission Energy for a portfolio of projects in the area earlier this year. It’s also made a $26 million offer to take out Rockgate Capital (TSX: RGT). Areva owns 37% of Cigar Lake, 30% of McArthur River, and the majority of the Midwest Mine.

But it’s still extremely early…

This uranium grab is only getting started. The western and northern portions of the basin are only now being explored, and they look very impressive.

The tiny exploration companies that own them will grow by giant multiples as uranium price start their climb toward $70 per pound.

I have my eye on two of them specifically — and I went to visit them a few weeks ago, more than 2,500 miles from Baltimore.

So you can get ahead of the crowd on this one, I’ve put together a video detailing all the reasons for the coming uranium rush, my tour of the western Athabasca Basin, and why these two companies are poised for the highest gains.

Call it like you see it,

Nick Hodge

@nickchodge on Twitter

@nickchodge on TwitterNick is the Founder and President of the Outsider Club, and the Investment Director of the thousands-strong stock advisory, Early Advantage. Co-author of two best-selling investment books, including Energy Investing for Dummies, his insights have been shared on news programs and in magazines and newspapers around the world. For more on Nick, take a look at his editor’spage.

*Follow Outsider Club on Facebook and Twitter.

NEW YORK (Reuters) – Short-seller Jim Chanos said Tuesday it is time for typical equity investors to be “a little more cautious” even as the stock market may continue to rise.

Chanos, speaking the Reuters Global Investment Outlook Summit in New York said his fund Kynikos Associatesis “very bearish on coal” and he is “pretty much short” all the U.S. leveraged coal companies.

Chanos also said he was bearish on national oil companies and the integrated majors like Exxon-Mobil, which he said are experiencing a “dropping return on capital” that “is really ominous.”

The famous short-seller said Exxon-Mobil and other oil companies like it increasingly look like “value trap.”

He also said investors would be “well warned” to analyze Caterpillar Inc’s financial unit.

This post originally appeared at Reuters. Copyright 2013.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair