Currency

If growth and yield, in their typical feedback loop, are still considered key drivers of currencies over the intermediate-term (and I think they are), it suggests the dollar should be well supported relative to the euro in the months ahead.

The USD index has been trending upwards within the dark-green trend-channel since 2008, whereas major buy-signals were generated at the apex of the red triangles as thereafter the so-called „thrusts“ started.

However, the goal of a thrust is to rise above the high of the triangle and transform this resistance into a new support – in order for a new upward-trend to commence thereafter.

As we go through the first significant pullback in the market for 2012, the dollar seems to be at a turning point that should influence market trends for the next few months. Going all the way back to 2002, there has been a strong inverse correlation between stocks and commodities, and the US dollar. For the most part, the dollar has been falling during this period, which has helped drive cyclical bull markets in stocks and commodities. More recently, the stock market panic of 2008 and the first euro crisis of 2010 drove significant countertrend rallies in the dollar, and corrections in stocks and commodities.

Martin Armstrong is offering you an opportunity to buy ancient Roman Coins:

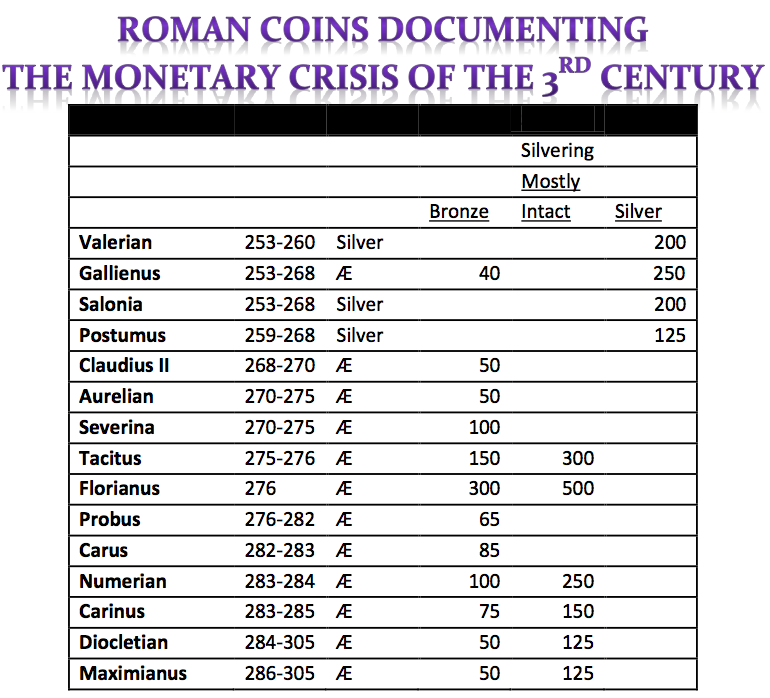

The response to the offering of Roman Coins was simply overwhelming. So many people have written asking how they can buy Roman Coins and others realizing these are from the 3rd Century have asked are there examples available documenting the collapse of the monetary system? I have contacted some old friends with respect to making available a selection of Roman coins of this 3rd Century period for those interested in owning a piece of real live history and/or demonstrating the Monetary Crisis that led to the fall of Rome from a hoard of Roman coins.

Because of the turmoil of the 3rd Century and precisely the dangers we face today as government goes after citizens hunting down their wealth to confiscate to sustain their existence, what happens is they cause capital to hoard reducing the VELOCITY of money. Hoards of Roman coins of earlier chaotic periods exist, although much fewer in number. Consequently, the earlier coins tend to be much rarer. As shown above, here are two gold coins from the Post-Caesarian Civil War period (44-42BC) that followed the assassination of Julius Caesar. In the case of Brutus, a non-portrait silver denarius would bring generally $2,000-$5,000 where a silver EID MAR (bragging he killed Caesar) would be $25,000-$100,000. There are only two gold EID MAR (Ides of March) coins and these today would bring more than $1 million. The gold Ahenobarbus (supporter of Brutus) would bring well over $50,000 today.

Hoards of the 3rd Century are far more common. Pots with up to 50,000 coins have been discovered, but of course the condition is often well corroded making such coins worth perhaps $10 simply because they are a relic of the past and a piece of history. Silver and gold coins endure through the ages much better than bronze. Thus, condition of coins during the 3rd century does help to reduce the supply of decent well preserved coins in proportion to the bulk that are found over time.

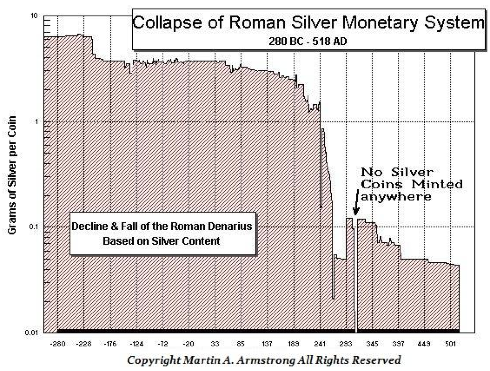

Consequently, those asking the question: Is it possible to obtain coins showing the drastic collapse in silver content of the 3rd Century? This collapse took place during the reign following Valerian I (253- 260AD) who was captured by the Parthians (Persians) and stuffed as a wild animal trophy upon his death. His son, Gallienus (253-268AD) made no effort to rescue his father and the economic collapse thereafter is easily seen in the coinage. So the answer is yes! I have made arrangements for those seeking such an example of the Monetary Crisis of the 3rd Century.

This is an accommodation – not a business

The quality of these coins is virtually Extremely Fine without corrosion. All names are legible. These are the selected quality from the hoard and and are not the typical low grade junk often sold. This provides a good sampling of this period (minus the extreme rarities) that have survived thanks to the tremendous economic upheavals of the times that led people to burry their wealth.

Set of 15 one average coin of the above non-corroded, Very Fine condition all readable $595 (suitable for non-collectors)

Set of 16 above with (2) Gallienus (Silver/Bronze) Extremely Fine Top Grade all readable $2450.00 (with silvering largely intact where noted)

Prices include shipping. Payment is acceptable at: ArmstrongEconomics@HotMail.COM” data-mce-href=”mailto:ArmstrongEconomics@HotMail.COM“>ArmstrongEconomics@HotMail.COM

Or checks may be send to:

Armstrong Economics

Two Penn Center – 1500 JFK Blvd, Suite 200 – Philadelphia, Pa 19102

#1 Gold Timer of the Year 2011 Stephen Todd March 6th/2012: “GOLD: Gold got clobbered along with stocks. This finally puts us on a sell.”

#2 Gold Timer of the Year 2011 & #1 Gold Market timer for the 5 year period ending in 2010 Mark Leibovit March 6th/2012: GOLD – ACTION ALERT – BUY (And Take Delivery Of The Physical Metals)

Billionaire Sprott: What are the repercussions of all this money printing?

2012 is proving to be the ‘Year of the Central Bank’. It is an exciting celebration of all the wonderful maneuvers central banks can employ to keep the system from falling apart. Western central banks have gone into complete overdrive since last November, convening, colluding and printing their way out of the mess that is the Eurozone. The scale and frequency of their maneuvering seems to increase with every passing week, and speaks to the desperate fragility that continues to define much of the financial system today.

The first major maneuver took place on November 30, 2011, when the world’s G6 central banks (the Federal Reserve, the Bank of England, the Bank of Japan, the European Central Bank [ECB], the Swiss National Bank, and the Bank of Canada) announced “coordinated actions to enhance their capacity to provide liquidity support to the global financial system”. Long story short, in an effort to avert a total collapse in the European banking system, the US Fed agreed to offer unlimited US dollar swap agreements with the other central banks. These US dollar swaps allow the other central banks, most notably the ECB, to borrow US dollars from the Federal Reserve and lend them to their respective national banks to meet withdrawals and make debt payments. The best part about these swaps is that they are limitless in scope — meaning that until February 1, 2013, the Federal Reserve is, and will be, prepared to lend as many US dollars as it takes to keep the financial system from imploding. It sounds absolutely great, and the Europeans should be nothing but thankful, except for the tiny little fact that to supply these unlimited US dollars, the Federal Reserve will have to print them out of thin air.

Don’t worry, it gets better. Since unlimited US swap lines weren’t enough to solve the problem, roughly three weeks later, on December 21, 2011, the European Central Bank launched the first tranche of its lauded Long Term Refinancing Operation (LTRO). This is the program where the ECB flooded 523 separate European banks with 489 billion euros worth of 3-year loans to keep them going through Christmas. A second tranche of LTRO loans is planned to launch at the end of February, with expectations for size ranging from 300 billion to more than 1 trillion euros of uptake. The good news is that Italian, Portuguese and Spanish bond yields have dropped since the first LTRO went through, which suggests that at least some of the initial LTRO funds have been reinvested back into sovereign debt auctions. The bad news is that the Eurozone banks may now be hooked on what is clearly a back-door quantitative easing (QE) program, and as the warning goes for addictive drugs — once you start, it can be very hard to stop.

Britain is definitely hooked. On February 9, 2012, the Bank of England announced another QE extension for 50 billion pounds, raising their total QE print to £325 billion since March 2009. Japan’s hooked as well. On February 14, 2012, the Bank of Japan announced a ¥10 trillion ($129 billion) expansion to its own QE program, raising its total QE program to ¥65 trillion ($825 billion). Not to be outdone, in the most recent Fed news conference, US Fed Chairman Bernanke signaled that the Fed will keep interest rates near zero until late 2014, which is 18 months later than he had promised in Fed meetings last year. If Bernanke keeps his word, by the end of 2014 the US government will have enjoyed near zero interest rates for six years in a row. Granted, extended zero percent interest rates is not nearly as satisfying as a proper QE program, but who needs traditional QE when the Fed already buys 91 percent of all 20-30 year maturity US Treasury bonds? Perhaps they’re saving traditional QE for the upcoming election.

All of this pervasive intervention most likely explains more than 90 percent of the market’s positive performance this past January. Had the G6 NOT convened on swaps, had the ECB NOT launched the LTRO programs, and had Bernanke NOT expressed a continuation of zero interest rates, one wonders where the equity indices would trade today. One also wonders if the European banking system would have made it through December. Thank goodness for “coordinated action”. It does work in the short-term.

But what about the long-term? What are the unintended consequences of repeatedly juicing the system? What are the repercussions of all this money printing? We can think of a few.

First and foremost, without continued central bank support, interbank liquidity may cease to function entirely in the coming year. Consider the implications of the ECB’s LTRO program: when you create a loan program to save the EU banks and make its participation voluntary, every one of those 523 banks that participates is essentially admitting that they have a problem. How will they ever lend money to each other again? If you’re a bank that participated in the LTRO program because you were on the verge of bankruptcy, how can you possibly trust other banks that took advantage of the same program? The ECB’s LTRO program has the potential to be very dangerous, because if the EU banks start to rely on the loans too heavily, the ECB may find itself inadvertently attached to the broken EU banking system forever.

The second unintended consequence is the impact that interventions have had on the non-G6 countries’ perception of western solvency. If you’re a foreign lender to the United States, Britain, Europe or Japan today, how comfortable can you possibly be in lending them money? How do you lend to countries whose sole basis as a going concern rests in their ability to wrangle cash injections printed by their respective central banks? Going further, what happens when the rest of the world, the non-G6 world, starts to question the G6 Central Banks themselves? What entity exists to bailout the financial system if the market moves against the Fed or the ECB?

The fact remains that there are few rungs left in the financial confidence chain in 2012, and central banks may end up pushing their printing schemes too far. In 2008-2009, it was the banks that lost credibility and required massive bailouts by their respective sovereign states. In 2010-2011, it was the sovereigns, most notably those in Europe, that lost credibility and required massive bailouts by their respective central banks. But there is no lender of last resort for the central banks themselves. That the IMF is now trying to raise another $600 billion as a security buffer doesn’t go unnoticed, but do they honestly think that’s going to make any difference?

When reviewing today’s macro environment, we keep coming back to the same conclusion. The non-G6 world isn’t blind to the efforts of the Fed and the ECB. When the Fed openly targets a 2 percent inflation rate, foreign lenders know that means they will lose, at a minimum, at least 2 percent of purchasing power on their US loans in 2012. It therefore shouldn’t surprise anyone to see those lenders piling into alternative assets that have a better chance at protecting their wealth, long-term.

This is likely why China reduced its US Treasury exposure by $32 billion in the month of December (See Figure 1). This is also why China, which produced 360 tonnes of gold internally last year, also imported an additional 428 tonnes in 2011, up from 119 tonnes in 2010. This may also be why China’s copper imports hit a record high of 508,942 tonnes in December 2011, up 47.7 percent from the previous year, despite the fact that their GDP declined at year-end. Same goes for their crude oil imports, which hit a record high of 23.41 million metric tons this past January, up 7.4 percent year- over-year. The so-called experts have a habit of downplaying these numbers, but it seems pretty clear to us: China isn’t waiting around for next QE program. They are accelerating their move away from paper currencies and into hard assets.

2012 is proving to be the ‘Year of the Central Bank’. It is an exciting celebration of all the wonderful maneuvers central banks can employ to keep the system from falling apart. Western central banks have gone into complete overdrive since last November, convening, colluding and printing their way out of the mess that is the Eurozone. The scale and frequency of their maneuvering seems to increase with every passing week, and speaks to the desperate fragility that continues to define much of the financial system today.

The first major maneuver took place on November 30, 2011, when the world’s G6 central banks (the Federal Reserve, the Bank of England, the Bank of Japan, the European Central Bank [ECB], the Swiss National Bank, and the Bank of Canada) announced “coordinated actions to enhance their capacity to provide liquidity support to the global financial system”. Long story short, in an effort to avert a total collapse in the European banking system, the US Fed agreed to offer unlimited US dollar swap agreements with the other central banks. These US dollar swaps allow the other central banks, most notably the ECB, to borrow US dollars from the Federal Reserve and lend them to their respective national banks to meet withdrawals and make debt payments. The best part about these swaps is that they are limitless in scope — meaning that until February 1, 2013, the Federal Reserve is, and will be, prepared to lend as many US dollars as it takes to keep the financial system from imploding. It sounds absolutely great, and the Europeans should be nothing but thankful, except for the tiny little fact that to supply these unlimited US dollars, the Federal Reserve will have to print them out of thin air.

Don’t worry, it gets better. Since unlimited US swap lines weren’t enough to solve the problem, roughly three weeks later, on December 21, 2011, the European Central Bank launched the first tranche of its lauded Long Term Refinancing Operation (LTRO). This is the program where the ECB flooded 523 separate European banks with 489 billion euros worth of 3-year loans to keep them going through Christmas. A second tranche of LTRO loans is planned to launch at the end of February, with expectations for size ranging from 300 billion to more than 1 trillion euros of uptake. The good news is that Italian, Portuguese and Spanish bond yields have dropped since the first LTRO went through, which suggests that at least some of the initial LTRO funds have been reinvested back into sovereign debt auctions. The bad news is that the Eurozone banks may now be hooked on what is clearly a back-door quantitative easing (QE) program, and as the warning goes for addictive drugs — once you start, it can be very hard to stop.

Britain is definitely hooked. On February 9, 2012, the Bank of England announced another QE extension for 50 billion pounds, raising their total QE print to £325 billion since March 2009. Japan’s hooked as well. On February 14, 2012, the Bank of Japan announced a ¥10 trillion ($129 billion) expansion to its own QE program, raising its total QE program to ¥65 trillion ($825 billion). Not to be outdone, in the most recent Fed news conference, US Fed Chairman Bernanke signaled that the Fed will keep interest rates near zero until late 2014, which is 18 months later than he had promised in Fed meetings last year. If Bernanke keeps his word, by the end of 2014 the US government will have enjoyed near zero interest rates for six years in a row. Granted, extended zero percent interest rates is not nearly as satisfying as a proper QE program, but who needs traditional QE when the Fed already buys 91 percent of all 20-30 year maturity US Treasury bonds? Perhaps they’re saving traditional QE for the upcoming election.

All of this pervasive intervention most likely explains more than 90 percent of the market’s positive performance this past January. Had the G6 NOT convened on swaps, had the ECB NOT launched the LTRO programs, and had Bernanke NOT expressed a continuation of zero interest rates, one wonders where the equity indices would trade today. One also wonders if the European banking system would have made it through December. Thank goodness for “coordinated action”. It does work in the short-term.

But what about the long-term? What are the unintended consequences of repeatedly juicing the system? What are the repercussions of all this money printing? We can think of a few.

First and foremost, without continued central bank support, interbank liquidity may cease to function entirely in the coming year. Consider the implications of the ECB’s LTRO program: when you create a loan program to save the EU banks and make its participation voluntary, every one of those 523 banks that participates is essentially admitting that they have a problem. How will they ever lend money to each other again? If you’re a bank that participated in the LTRO program because you were on the verge of bankruptcy, how can you possibly trust other banks that took advantage of the same program? The ECB’s LTRO program has the potential to be very dangerous, because if the EU banks start to rely on the loans too heavily, the ECB may find itself inadvertently attached to the broken EU banking system forever.

The second unintended consequence is the impact that interventions have had on the non-G6 countries’ perception of western solvency. If you’re a foreign lender to the United States, Britain, Europe or Japan today, how comfortable can you possibly be in lending them money? How do you lend to countries whose sole basis as a going concern rests in their ability to wrangle cash injections printed by their respective central banks? Going further, what happens when the rest of the world, the non-G6 world, starts to question the G6 Central Banks themselves? What entity exists to bailout the financial system if the market moves against the Fed or the ECB?

The fact remains that there are few rungs left in the financial confidence chain in 2012, and central banks may end up pushing their printing schemes too far. In 2008-2009, it was the banks that lost credibility and required massive bailouts by their respective sovereign states. In 2010-2011, it was the sovereigns, most notably those in Europe, that lost credibility and required massive bailouts by their respective central banks. But there is no lender of last resort for the central banks themselves. That the IMF is now trying to raise another $600 billion as a security buffer doesn’t go unnoticed, but do they honestly think that’s going to make any difference?

When reviewing today’s macro environment, we keep coming back to the same conclusion. The non-G6 world isn’t blind to the efforts of the Fed and the ECB. When the Fed openly targets a 2 percent inflation rate, foreign lenders know that means they will lose, at a minimum, at least 2 percent of purchasing power on their US loans in 2012. It therefore shouldn’t surprise anyone to see those lenders piling into alternative assets that have a better chance at protecting their wealth, long-term.

This is likely why China reduced its US Treasury exposure by $32 billion in the month of December (See Figure 1). This is also why China, which produced 360 tonnes of gold internally last year, also imported an additional 428 tonnes in 2011, up from 119 tonnes in 2010. This may also be why China’s copper imports hit a record high of 508,942 tonnes in December 2011, up 47.7 percent from the previous year, despite the fact that their GDP declined at year-end. Same goes for their crude oil imports, which hit a record high of 23.41 million metric tons this past January, up 7.4 percent year- over-year. The so-called experts have a habit of downplaying these numbers, but it seems pretty clear to us: China isn’t waiting around for next QE program. They are accelerating their move away from paper currencies and into hard assets.

China is not alone in this trend either. Russia has reportedly cut its US Treasury exposure by half since October 2010. Not surprisingly, Russia was also a big buyer of gold in 2011, adding approximately 95 tonnes to its gold reserves, with 33 tonnes added in the fourth quarter alone. It’s not hard to envision higher gold prices if the rest of the non-G6 countries follow-suit.

The problem with central bank intervention is that it never works out as planned. The unintended consequences end up cancelling out the short-term benefits. Back in 2008, when the Fed introduced zero percent interest rates, everyone thought it was a great policy. Four years later, however, and we’re finally beginning to appreciate the complete destruction it has wreaked on savers. Just look at the horror show that is the pension industry today: According to Credit Suisse, of the 341 companies in the S&P 500 index with defined benefit pension plans, 97 percent are underfunded today. According to a recent pension study by Seattle-based Milliman Inc., the combined deficit of the 100 largest defined-benefit plans in the US increased by $236.4 billion in 2011 alone. The main culprit for the increase? Depressed interest rates on government bonds.

Let’s also not forget the public sector pension shortfalls, which are outright frightening. In Europe, unfunded state pension obligations are estimated to total $39 trillion dollars, which is approximately five times higher than Europe’s combined gross debt. In the United States, unfunded pension obligations increased by $2.9 trillion in 2011. If the US actually acknowledged these costs in their deficit calculations, their official 2011 fiscal deficit would have risen from the reported $1.3 trillion to $4.2 trillion. Written the long way, that’s a deficit of $4,200,000,000,000,… in one year.

There is unfortunately no economic textbook to guide us through these strange times, but common sense suggests we should be extremely wary of the continued maneuvering by central banks. The more central banks print to save the system, the more the system will rely on their printing to stay solvent — and you cannot solve a debt problem with more debt, and you cannot print money without serious repercussions. The central banks are fueling a growing distrust among the creditor nations that is forcing them to take pre-emptive actions with their currency reserves. Individual investors should take note and follow-suit, because it will be a lot easier to enjoy the “Year of the Central Bank” if you own things that can actually benefit from all their printing, as opposed to things that can only be destroyed by it.

Regards,

Eric Sprott and David Baker

for The Daily Reckoning

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair