Currency

In Switzerland, it’s not just the clocks that are cuckoo. Over the past four years Swiss politicians and central bankers have gone on an unprecedented buying spree of foreign exchange reserves. In 2012, their cache swelled to as much as $420 billion worth of various currencies, primarily the euro. This figure is a seven-fold increase since 2008 and equates to 70% of the country’s annual GDP. The sum translates to $200,000 per family of four, enough to keep the Swiss in clocks, chocolates, and fondue for many years to come. The Swiss leadership will claim the money has been “invested” with an eye to the future, but what they’ve done is impoverished themselves in the present. Although such a decision seems perverse, it makes perfect sense when seen through the lens of today’s presiding economic thinking.

In Switzerland, it’s not just the clocks that are cuckoo. Over the past four years Swiss politicians and central bankers have gone on an unprecedented buying spree of foreign exchange reserves. In 2012, their cache swelled to as much as $420 billion worth of various currencies, primarily the euro. This figure is a seven-fold increase since 2008 and equates to 70% of the country’s annual GDP. The sum translates to $200,000 per family of four, enough to keep the Swiss in clocks, chocolates, and fondue for many years to come. The Swiss leadership will claim the money has been “invested” with an eye to the future, but what they’ve done is impoverished themselves in the present. Although such a decision seems perverse, it makes perfect sense when seen through the lens of today’s presiding economic thinking.

For the past few generations Switzerland has enjoyed some of the strongest economic fundamentals in the world. The country boasts a high savings rate, low taxes, strong exports, low debt-to-GDP, balanced government budgets, and prior to a few years ago one of the most responsible monetary policies in the world. These attributes made the Swiss franc one of the world’s “safe haven” currencies. But in today’s global economy, no good deed goes unpunished.

Central bankers around the world, particularly in Washington, Frankfurt and Tokyo, have been engaged in a massive and coordinated campaign of currency debasement to combat the recession. But for years the Swiss refused to join in the printing parade. As a result, investors around the world wisely decided to park their savings in the reliable Swiss franc. From December of 2008 to August 2011 the franc appreciated an astounding 59% against the U.S. dollar and approximately 30% against the Japanese yen. More importantly, the franc gained 42% against the euro. As the Eurozone completely surrounds Switzerland, its trade with those countries represents the vast majority of its international transactions.

During this massive run up in its currency, the Swiss economy continued to prosper. Wages and purchasing power increased and GDP grew consistently faster than other countries in Western Europe. Despite generally positive export statistics, some Swiss exporters noticed that at times the strong franc put them at a disadvantage against foreign competitors. In addition, the strengthening currency helped keep a lid on consumer prices, giving Switzerland a consistently low inflation rate with occasional bouts of actual deflation. Despite the fact that Switzerland was an island of economic health amidst a sea of problems, the reigning economic orthodoxy convinced Swiss leaders that their strong currency was a burden rather than a blessing. More pointedly, the rise in the franc was seen as a repudiation of the expansionary policies occurring in other countries. And so the Swiss government decided to join the currency killing party.

In early August 2011, the Swiss National Bank took a series of steps to reverse the fortunes of the franc. In the simplest terms, they sold francs and bought foreign currencies, most notably the euro. The announcement included a promise to buy unlimited quantities of foreign exchange to maintain a floor of 1.20 francs per euro. In so doing, the Swiss essentially outsourced their monetary policy to the Eurozone. Any moves taken by the European Central Bank would need to be matched by the Swiss. Ironically, it was fear of this outcome that kept the Swiss from adopting the euro in the first place. Despite the former bias toward independence, the Swiss have de facto adopted the euro anyway. Since that time, the franc has fallen 16% against the dollar, Swiss foreign exchange reserves have skyrocketed, and investors who bought francs as a means to escape debasement have been betrayed.

Productive nations generate excess goods and services that can be sold abroad and their growth and stability attract investment funds from abroad. These conditions will tend to increase demand for the nation’s currency, thereby pushing up its price. A strong currency keeps capital and raw materials costs low, enabling more productive workers to earn higher real wages. But according to most economists, a strong currency will bring down an economy because it destroys international competitiveness and can even lead to lower prices (deflation) which they see as economic quicksand. These fears have ignited a “global currency war” in which countries are expending huge amounts of national savings in order to ensure that their currencies stay cheap. In today’s economic logic we must fail in order to succeed.

But it is very easy to have a weak currency. All that is needed is an unlimited willingness to print. A strong currency requires real fiscal discipline and actual production. Yet, like the weight loss TV show, economists believe that the winner of a currency war is the biggest loser. You win not by killing your competitors, but by killing yourself! It’s like a student convincing his parents that an “F” is a better grade than an “A.” And if a straight “F” report card results in parental accolades rather than anger, the students will lack any incentive to improve performance. Similarly, as nations like Switzerland strive to reduce their own grades, the failing nations have a reduced incentive to change their study habits. Without outside support, nations with collapsing currencies would see huge increases in consumer prices. The resulting fall in living stands would force productive reform.

I take the minority position that just as it is better to be rich than poor, a strong currency is better than a weak one. Although much more credentialed economists may try to muddle the arguments, the truth may be seen when a particular position is taken to its logical extreme. If a weaker currency is preferable to a stronger one, then logic would dictate that a currency of no value will be preferable to one with an infinite value. But how would economies with these drastically different currencies operate?

It is true that the country with the zero value currency will tend to see full employment and strong exports. The relative low cost of labor will mean that the locals could be easily employed in even the most marginal activity. But since holders of other currencies will be able to outbid the domestic population for all of their production, everything produced will be exported. Imports will be zero as the local population would be unable to afford anything produced in countries with more valuable currencies. As a result, actual consumption would be extremely low. In essence this economy would be analogous to impoverished, subsistence level economies such as Bolivia, Zimbabwe, and Haiti.

In contrast, a country with an infinitely valuable currency would see the best of all possible worlds. Even the smallest amount of money would allow citizens to buy huge amounts of goods from abroad. An evening’s babysitting money would deliver more purchasing power than months of hard labor in poorer countries. The strong currency would mean that consumption would soar even while hours worked fell. Savings would increase in value, and people would have more ability to travel and pursue leisure activities. In essence, we are describing a rich economy.

Placed in such a context, it’s easy to see the preferred option. Those who believe in the benefits of weak currencies do not specify when a falling currency becomes a bad thing. Clearly there must be a tipping point where lost purchasing power overcomes supposed gains in growth. Yet they are silent on that point. My position is that a rising currency is always good. No magic tipping point needs to be identified.

The problem is that economists now believe that the goal of an economy is to provide employment, not goods and services. They see a job as an end in and of itself, rather than as a means for people to get the things they really want. But if we can get all that we want without having to work, who needs to bother? A strong currency takes us closer to this goal. It is a testament to how far the “science” of economics has fallen that this goal has been utterly forgotten.

But this junk science is killing real growth. As long as this “black is white” ideology remains in place, the biggest printers will continue to be the biggest actual losers.

To order your copy of Peter Schiff’s latest book, The Real Crash: America’s Coming Bankruptcy – How to Save Yourself and Your Country, click here.

For in-depth analysis of this and other investment topics, subscribe to Peter Schiff’s Global Investor newsletter. CLICK HERE for your free subscription.

And Why The Yen Plunged.

Yen Weekly Chart Above: The yen has lost 13 percent of its value against the U.S.dollar in 3 months

Japan, the nation that pretty much invented quantitative easing, is now following in Ben Bernanke’s footsteps, launching an open-ended asset purchase plan and a 2% inflation target to fight the steady drop in prices that have plagued the world’s third largest economy for twenty years. The Bank of Japan (BoJ) is joining others in what could be dubbed a new era for central banks, as ailing economies and massive debt loads have eroded the barrier of independence and essentially pushed monetary policymakers into trying to spark growth via stimulus, as the debate on the effectiveness of those policies ranges on.

The market’s verdict……

……read more HERE

“Money is not the only answer, but it makes a difference” – President Obama

Here’s the article reference: Senior Obama Official: “We Are Going To Kill The Dollar”. Youtube 1:13 video of the original interview HERE

Has the first currency crisis begun?

by Toby Connor

I expect the eventual endgame to this whole Keynesian monetary experiment that has been going on ever since World War II to finally terminate in a global currency crisis. I’m starting to wonder if we aren’t seeing the first domino start to topple.

I’m talking about the Japanese yen of course.

I think everyone just naturally assumes that the yen is dropping in response to Prime Minister Abe’s intent to imitate U.S. policy and print its way out of its troubles. The problem with this strategy is, of course, eventually Japan will break its currency. Japan is in a particularly tenuous situation in that their debt-to-GDP dwarfs most of the rest of the world. The only hope they have of servicing this debt is for interest rates to stay basically at zero.

Any move by interest rates above this artificially low level and Japan’s debt becomes unserviceable, without resorting to a greater and greater debasement of the currency. Unfortunately that will also result in an acceleration of the collapse of the currency, which would just cause Japanese bonds to be sold even more aggressively — a nasty catch-22 situation.

At this point there is no way out for Japan. The only question is when the endgame will arrive? Japanese bond bears have been asking themselves this question for almost two decades.

The recent move in the yen has started me wondering if that end game hasn’t now begun.

In the chart below I have marked the successive yearly cycle lows with blue arrows. As you can see this major cycle bottom tends to arrive between March and May most years. If the 2013 yearly cycle low arrives in the normal timing band, then there may be a big problem developing with the Japanese currency. The reason I say that is because the Japanese yen is basically already in free fall and we may still have another one-three months to go before a final bottom.

…..read & view 2 more charts on page 2 HERE

Gold had a very negative Weekly Key Reversal Down last week…it has trended lower from $1800 since October 2012…it SHOULD be getting a lift from the dramatic Japanese reflationary activities…indeed it traded to All Time Highs against the Yen…but it’s weak against a number of other important measures…it’s trading at 12 month lows against the Euro…it’s fallen ~13% against WTI in the last 6 weeks…and in terms of the S+P 500 gold is at 2 year lows…stocks are stealing “market share” from gold…see charts below.

Negative price action:

Gold saw very negative price action…foreshadowing lower prices ahead… on November 28 when it fell $40 on the Comex futures market on All Time Record High Volume…(I discussed that price action on my November 30 blog [hyperlink: http://www.victoradair.com/blog/marktet-trades-sound-bites-nov-30] and speculated that a break of $1700 could ignite some real downside pressure.) In November 2012 the selling pressure on gold seemed restricted to the “paper” futures market…anecdotal reports were that “physical” gold buying was increasing as prices fell…indeed, outstanding Gold ETF’s rose to new record highs in early December.

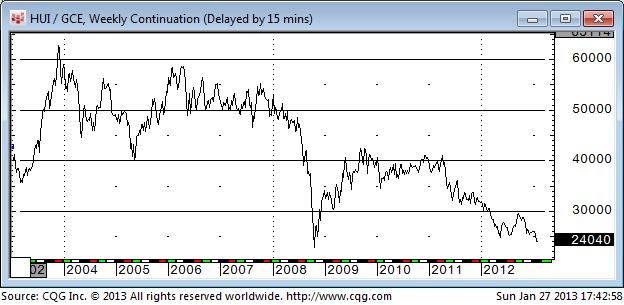

But now the bearish Market Psychology seems broad based…the selling is not just in the “paper” market…gold ETFs are declining and the gold share market is a disaster…the HUI/Gold ratio is at an 11 year lows (save for a very brief period in October 2008) and other gold share/gold ratios are also at multi-year lows…as the gold share indices themselves fall to new lows. I cautioned against buying gold shares several times last year…I called it, “The mistake you are dying to make”…in addition to the usual reasons given for the gold share weakness [gold ETFs, rising operating costs, country risk etc.] I suggested that there were simply WAY TOO MANY gold shares outstanding…that the SUPPLY of gold shares had overwhelmed DEMAND.

The Weak US$/Strong Gold relationship is breaking down…because the Euro is strong:

Gold is falling in US$ terms even as the US$ falls relative to the Euro. Last summer the Euro was under severe pressure…trading at 2 year lows near 1.20…Spanish bond yields were north of 7% and short term interest rates in several of the “strong” European countries were trading at negative nominal yields…then Draghi made his “whatever it takes” comments and the Euro has been climbing ever since…now very close to last year’s highs of 1.35 against the US$ …up 22% in the last 4 months against the Yen…obviously there has been a serious change in Euro Market Psychology and some serious “short covering” in the Euro…and not just against the US$.

A Gold Bug sees what he wants to see, and disregards the rest…Gold to Germany:

With apologies to Paul Simon…I don’t see any bullish significance in Germany’s plan to repatriate some of their gold. They moved the gold away from the Russian Front during the Cold War…now they think it’s safe to move it back home. The Gold Bugs, however, see the repatriation plan as bullish because they believe that the German gold is “missing” (along with a lot of other gold that is supposedly in secure storage at the Fed and the BOE.) Their theory is that the gold has been fraudulently sold into the market to keep prices down…and that Germany’s plans will expose this fraud and gold prices will soar.

Charts:

Gold had a Weekly Key Reversal Down last week…setting up a possible challenge of the late December $1625 lows.

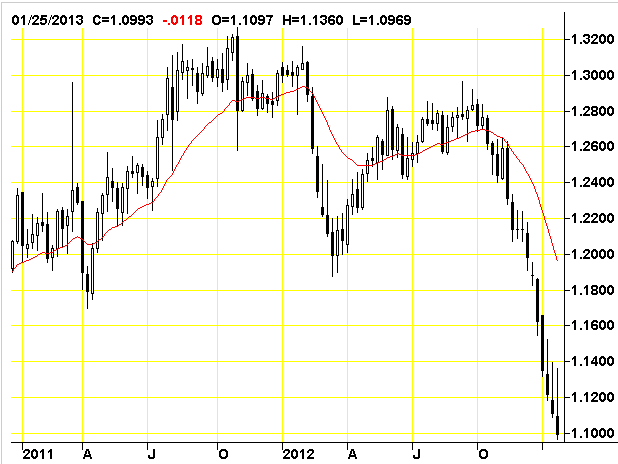

Gold is trading near last year’s lows in terms of the Euro…down over 10% from the All Time Highs made last September.

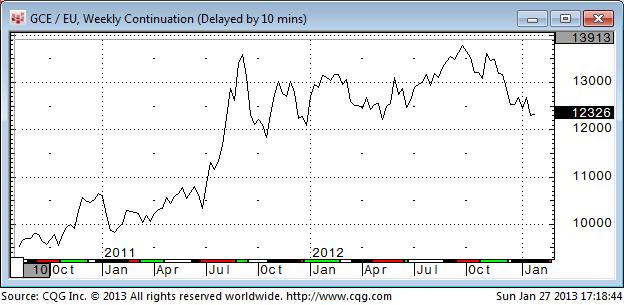

But in terms of the Japanese Yen Gold made new All Time Highs in early January.

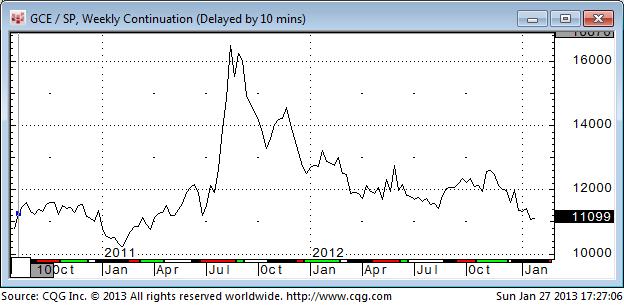

In terms of the S+P 500, however, gold is trading at 2 year lows…down 32% from the 23 year highs made August 2011…(gold is down 13% against the US$ since then)…global stock markets have greatly out-performed gold…and especially gold stocks since the summer of 2011.

While gold has trended down from its All Time Highs made September 2011 the S+P 500 (and most other global stock indices) have trended higher. The S+P is now at 5 year highs…only 5% away from its ATH made October 2007. Market Psychology is very bullish in stocks…the VIX is at a 5 ½ year low…the market thinks it has a “blank check” from the Central Banks…and stocks are clearly stealing “market share” away from gold.

Gold share indices are even weaker than gold…with the HUI at an 11 year low (save for a very brief period in Oct 2008) against Gold.

Futures markets provide an efficient and effective way to trade the Gold Market. If you would like to speak to a broker at PI Financial about trading gold in the futures market please call 604-664-2842.

Market Psychology has had a VERY BIG swing from bearish to bullish since the Key Turn Date in mid-November 2012 as it became clear that Abe was going to win the Japanese elections and begin implementing VERY aggressive reflationary measures to end two decades of deflation in Japan. The inter-connectedness of global financial markets insured that the BIG changes in Japan would contribute to BIG changes in markets around the world.

Since mid-November 2012:

Since mid-November 2012:

1) the Yen has fallen ~15% Vs. the US$…now down 10 weeks in a row to a 2 ½ year low,

2) The Yen has fallen ~20% Vs. the Euro,

3) Gold has risen to All Time Highs Vs. the Yen,

4) Global stock markets have risen with the major US Indices at 5 year highs (VIX at 5 year lows,)

5) The Nikkei stock index has risen ~26%,

6) European peripheral bond yields have fallen sharply,

7) It has been “Risk-On” in global financial markets in a BIG way!

…..read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair