Currency

Statistics Canada says Canada’s annual inflation rate was 1.3 per cent in July, up from 1.2 per cent the previous month.

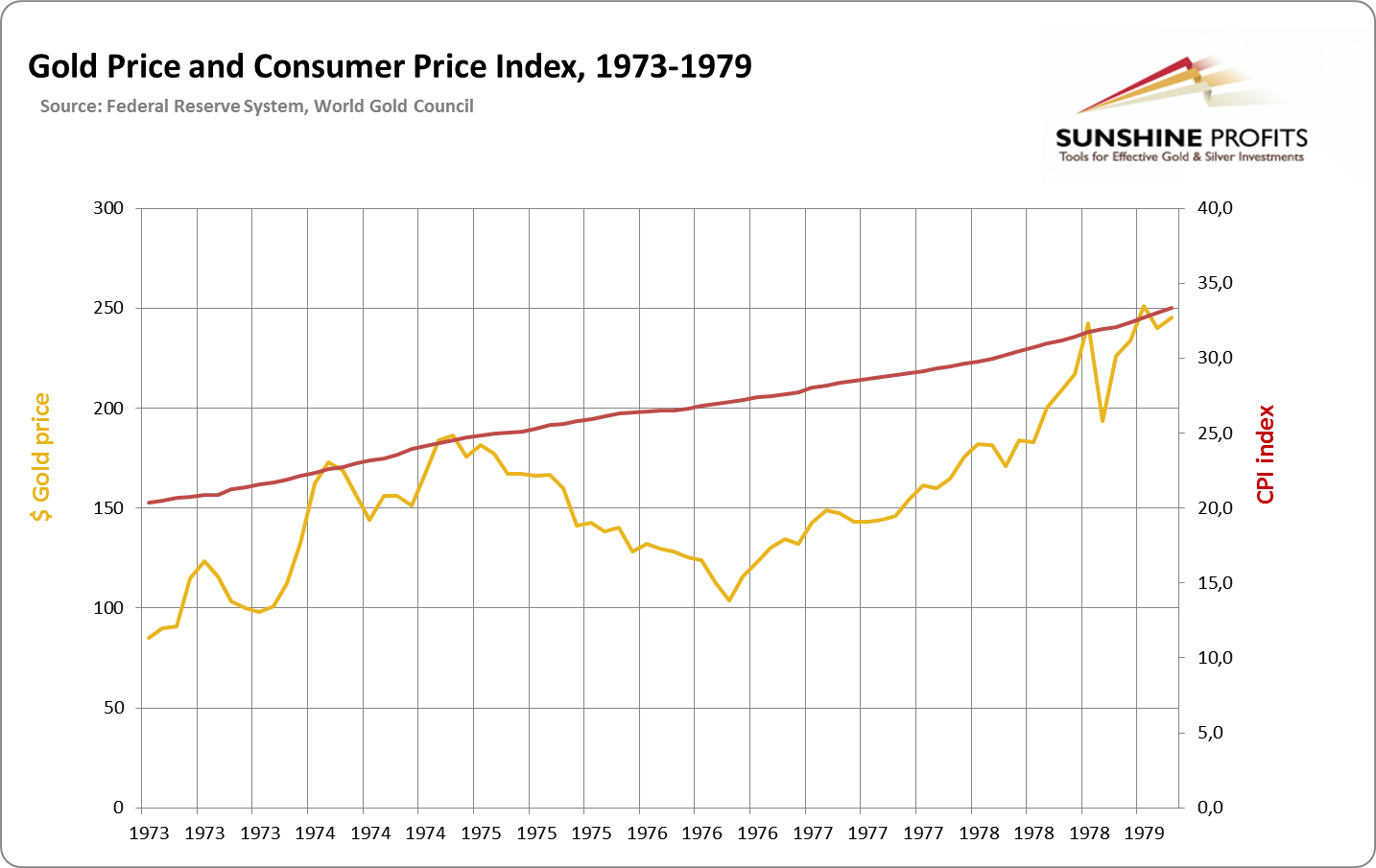

Last week we focused on the idea that gold is not an inflation hedge. Today, we will develop this notion even further. If we’re talking about gold as a hedge, it is rather a system-hedge than an inflation-hedge. Since 1973, when the dollar was allowed to float, gold has confirmed this view.

When it is wanted as a dollar alternative, the price of gold goes up. This takes place when the trust in the dollar plummets, or actually when the trust in the dollar-dominated-system plummets. Gold rose during the end of the 1970s because of expressively high inflation. But it was not only inflation that was decisive. This high inflation led to distrust in the dollar, therefore, gold became the alternative. The general trend of gold looks a lot like increasing CPI:

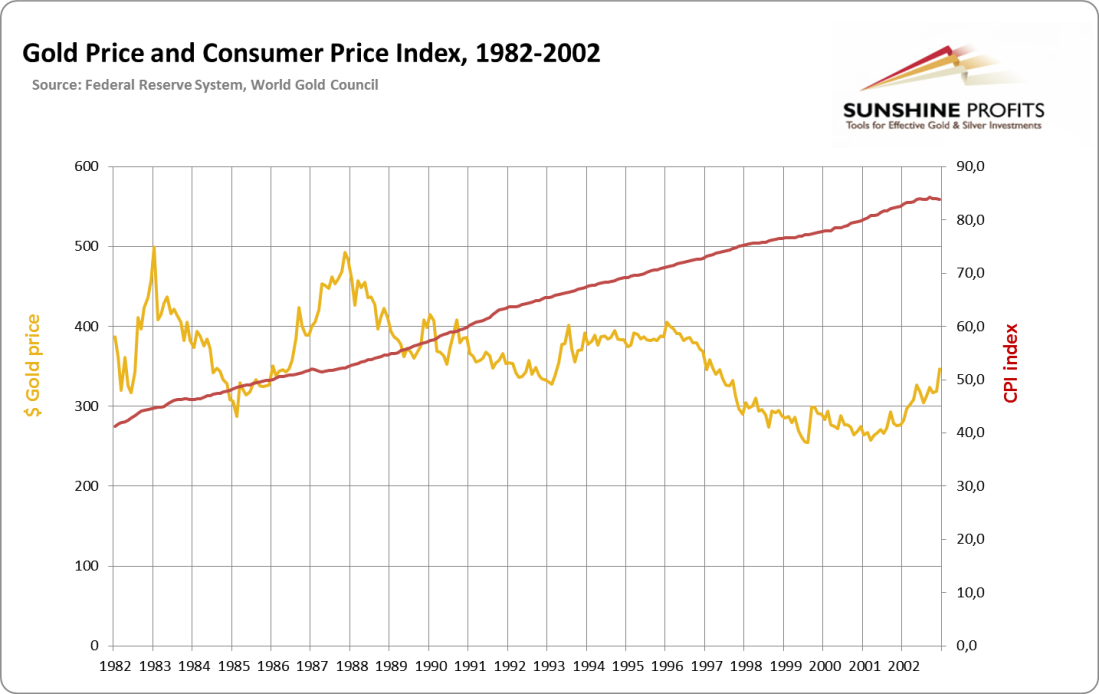

After the 1980s recession and end of the short-lived gold bubble Volcker tamed the dollar, which renew trust in it. The next 20 years were times of a noticeably strong dollar and stronger faith in this paper money. The conditions also paved the way for enormous increases in debt of the economy, which transformed the United States into the greatest debtor in the history of human civilization. During that time despite positive inflation gold was dropped as a “currency alternative”, therefore lost its value. The dollar was drained by mild inflationary forces; gold did not keep the pace and went down:

With oversupply of US dollars, the credit situation was reversed in the 21st century. Over indebtedness in the American economy has shaken the trust in the dollar-dominated system (especially due to agency debt and private debt). As Paul Samuelson called it, the “run on dollar” was triggered from 2001. This was visible in the decline of the dollar against other currencies, and also gold became a reliable alternative. The pace of inflation was overall no more impressive than it was for the previous 20 years. Yet suddenly the relation between gold and dollar had shifted, and the price of gold grew at a much higher pace than the dollar was losing value. Why? Because of the system dynamics and lowered trust in the dollar.

In any case gold is not really an inflation-hedge. It is a special investment vehicle that requires careful focus and analysis separate from only inflationary forces. Those forces no doubt affect the gold market. But not in a way many people often suggest, and in a way which may lead to misplaced investments.

The above is a small excerpt from our latest Market Overview report. The full version includes much more in-depth analysis of this and other fundamental factors that are likely to affect the gold market in the near future. You can sign up for these reports here.

Thank you.

Matt Machaj, PhD

* * * * *

Disclaimer

All essays, research and information found above represent analyses and opinions of Matt Machaj, PhD and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Matt Machaj, PhD and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Matt Machaj, PhD is not a Registered Securities Advisor. By reading Matt Machaj’s, PhD reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Matt Machaj, PhD, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

As you may know, the emerging market (EM) currencies have been crushed over the past year, some over the past two years. Some appear to be interesting setups now. Below are two: 1) Euro-Turkish lira (EUR/TRY), and 2) US$-Brazilian real (USD/BRL)…you may want to place these on your radar screen for potential opportunities.

Please click here to view the issue with charts

Regards,

Jack Crooks

Black Swan Capital

(Just Kidding!)

(Just Kidding!)

What is interesting is that during Japan’s lost decade [from 1991-2001] it outperformed the Eurozone in all categories: growth was faster, debt growth was slower, manufacturing productivity was higher, and labor costs grew more slowly.

Obviously there are several takeaways here, and we haven’t even broached the disastrous social impact of towering unemployment rates [specific country brain drain, birth rates, fall in scientific research, family strife, suicides, etc.]:

- If growth doesn’t resume soon, debt/gdp ratios across the Eurozone will mirror Japan’s; but in many ways because of such poor relative productivity and size of the Eurozone banking system the rise in debt will likely be that much more dangerous.

- As a hub for future industry in a globalized world where multi-nationals have so many choices, it looks bleak for countries inside the euro straight jacket. In short, foreign direct investment will go elsewhere.

- Instead of bringing cultures together, the single currency is helping bring old animosities to the surface, which are numerous thanks to two recent civil wars (WWI and WWII).

It seems unless something very big happens fairly soon, politicos across the Eurozone will be responsible for marginalizing the future of their people simply because they have invested so much political capital in this bold, but seemingly failed, experiment called the single currency despite passing by all the signs that read, “Turn back now!”

So, what is the endgame here?

Just when you think it can’t get any stranger, the U.S. economy – measured by the declining number of full-time jobs, lower household incomes and below target inflation rate – seems to be weakening, while the most speculative asset markets lurch back into full-tilt bubble mode. Home prices in Vegas, Silicon Valley, and Miami are above 2007 levels, equities are near all-time highs, and bank stocks are once again dominant in the S&P 500. It’s as if 2008/2009 never happened. And now this from Bloomberg, about the return of junk bonds:

Bond Hubris Overwhelms Fed in Riskiest Credit-Market Sectors

Bond investors trying to divine when the Federal Reserve will reduce its unprecedented monetary stimulus are increasingly looking to the riskiest parts of the debt market, which are booming like before the financial crisis.

….read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair