Currency

Recommendation:

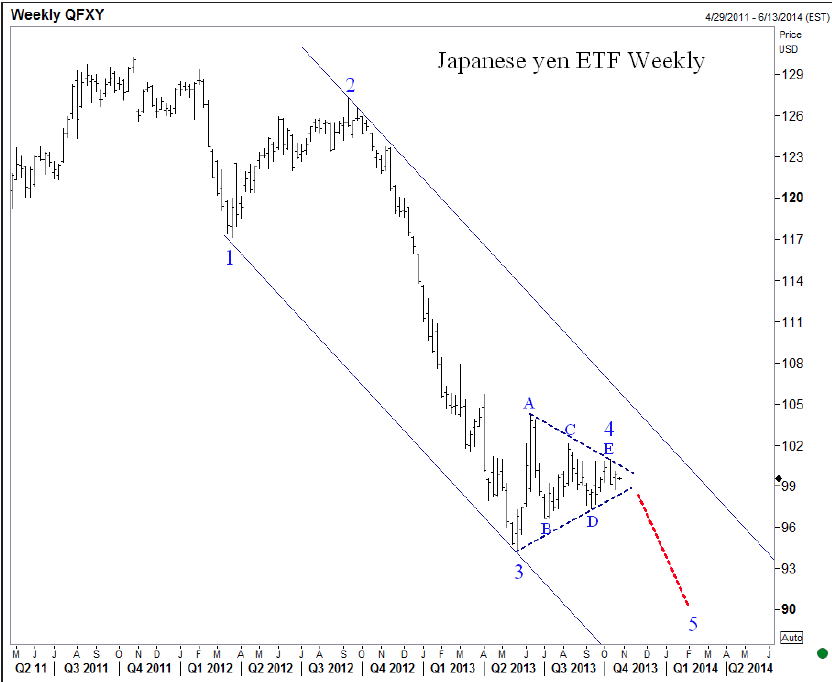

Adding Japanese yen ETF 98 puts! Targeting 421% profit.

21 October 2013/12:30 p.m. ET

Issue #1

Today Japan recorded its 15th straight trade deficit in a row. It suggests there is a significant transition taking place within the Japanese economy-either a natural or forced transition to an economy dependent more on domestic growth than the standard export-driven Asian model. The jury is still out, no doubt, on whetherPrime Minister Abe’s three-arrow strategy will succeed. But the ongoing Bank of Japan mandate to weaken the yen seems on track and there has been a direct correlation between trade deficits and the yen, as you can see in the chart below. I believe the yen continues to weaken in the months ahead and suggest you add this new position to your currency options portfolio today:

Please click the link below to view the issue:

Regards,

Jack Crooks

Black Swan Capital

They are Calling it a Collapse in Capitalism – by Martin Armstrong

They are Calling it a Collapse in Capitalism – by Martin Armstrong

The view of the American budget crisis from outside the USA is one that is blaming Wall Street and the banks and calling for the next crisis to be the final meltdown of Capitalism. This view is rising around the world. The fact that it is just pushed off into January with the funding ending on February 7th is seen as this debt crisis will merely take place time and time again until capitalism collapses. It is curious that there is a rising tide against capitalism but there is no understanding exactly what that truly means other than the Wall Street bankers. Obama is too busy trying to destroy the Republicans so he can pursue unrestrained socialism/communism and cannot see that this will destroy the world economy. It is the private sector that creates national wealth – not the state as communism proved.

….read more HERE

Too Big To Even Name

With the announcement that JP Morgan Chase will pay a $13 billion fine for past crimes against its customers – while the bankers who actually committed the crimes will remain not only unprosecuted but unnamed – a lot of people are wondering how it is that crimes worthy of billions in restitution don’t rate a single perp-walk. Earlier this year a senator wondered the same thing in a hearing and got some illuminating answers. From Harper’s Magazine:

Too Big To Jail

From the transcript of a March 7 Senate Banking Committee hearing on enforcement of the Bank Secrecy Act of 1970, which requires U.S. financial institutions to help the federal government prevent money laundering. Elizabeth Warren is a Democratic senator from Massachusetts; David Cohen is the Treasury’s undersecretary for terrorism and financial intelligence; Jerome Powell is a governor of the Federal Reserve.ELIZABETH WARREN: In December, HSBC admitted to laundering $881 million for Mexican and Colombian drug cartels, and also admitted to violating our sanctions against Iran, Libya, Cuba, Burma, the Sudan. They didn’t do it just one time. It wasn’t like a mistake. They did it over and over and over again over a period of years. And they were caught doing it. Warned not to do it. And kept right on doing it. And evidently making profits doing it. Now, HSBC paid a fine, but no one individual went to trial. No one individual was banned from banking. And there was no hearing to consider shutting down HSBC’s activities here in the United States. So what I’d like is — you’re the experts on money laundering. I’d like your opinion. What does it take? How many billions of dollars do you have to launder for drug lords and how many economic sanctions do you have to violate before someone will consider shutting down a financial institution like this? Mr. Cohen, can we start with you?

DAVID COHEN: Certainly, Senator. No question, the activity that was the subject of the enforcement action against HSBC was egregious. For our part, we imposed on HSBC the largest penalties that we had ever imposed on any financial institution. We looked at the facts and determined that the appropriate response there was a very, very significant penalty.

WARREN: But let me just move you along here, Mr. Cohen. What does it take to get you to move toward even a hearing? Even considering shutting down banking operations for money laundering?

COHEN: Senator, we at the Treasury Department don’t have the authority to shut down a financial institution.

WARREN: I understand that. I’m asking, in your opinion, you are the ones who are supposed to be the experts on money laundering. You work with everyone else, including the Department of Justice. In your opinion, how many billions of dollars do you have to launder for drug lords before somebody says, “We’re shutting you down”?

COHEN: We take these issues extraordinarily seriously. We aggressively prosecute and impose penalties against the institutions to the full extent of our authority. And one of the issues that we’re looking at —

WARREN: I’m sorry, I don’t mean to interrupt. I just need to move this along. I’m not hearing your opinion on this. Treasury is supposed to be one of the leaders in how we understand and work together to stop money laundering. I’m asking, what does it take, even to say, “We’re going to draw a line here, and if you cross that line, you’re at risk for having your bank closed”?

COHEN: We will, and have, and will continue to exercise our authority to the full extent of the law. The question of pulling a bank’s license is a question for the regulators.

WARREN: So you have no opinion on that? You tell me how vigorously you want to enforce these laws, but you have no opinion on when it is that a bank should be shut down for money laundering? Not even an opinion?

COHEN: Of course we have views on —

WARREN: That’s what I asked you for. Your views.

COHEN: I’m not going to get into some hypothetical line-drawing exercise.

WARREN: Well, it’s somewhere beyond $881 million of drug money.

COHEN: Well, Senator, the actions that we took in the HSBC case we thought were appropriate in that instance.

WARREN: Governor Powell, perhaps you can help me out here?

JEROME POWELL: Sure. So the authority to shut down an institution or hold a hearing about it, I believe, is triggered by a criminal conviction. And we don’t do criminal investigation. In the case of HSBC, we gave essentially the statutory maximum civil money penalties. We gave very stringent cease-and-desist orders. And we did what we have the legal authority to do.

WARREN: I appreciate that, Mr. Powell. So you’re saying you have no advice to the Justice Department on whether or not this was an appropriate case for a criminal action?

POWELL: It’s not our jurisdiction. They don’t do monetary policy. We collaborate with them, and we did on HSBC. They ask us specific questions. We answer those questions. That’s what we do.

WARREN: So you are responsible for these banks, but you have no view on when it’s appropriate to consider even a hearing to raise the question of whether or not these banks should have to close their operations when they engage in money laundering for drug cartels?

POWELL: I’ll tell you exactly when it’s appropriate. It’s appropriate where there’s a criminal conviction.

WARREN: I’ll just say here, if you’re caught with an ounce of cocaine, the chances are good you’re going to go to jail. If it happens repeatedly, you may go to jail for the rest of your life. But evidently if you launder nearly a billion dollars for drug cartels and violate our international sanctions, your company pays a fine and you go home and sleep in your own bed at night. I think that’s fundamentally wrong.

Some thoughts

When the Savings & Loan industry gorged on junk bonds and self-dealing and imploded in 1990, the Justice Department sent hundreds of industry insiders to jail and fined hundreds more. This time around, has anyone gone to jail? Apparently not. A cynic might say that Treasury, Justice and the Fed now operate more like in-house council for Wall Street, cleaning up messes and negotiating settlements that keep the deals flowing without touching the deal makers.

This isn’t hyperbole. It is now generally accepted that a stint in congress or a regulatory agency is an extended job interview, giving the lobbying firms and big banks a chance to look you over and see if you’re a team player. So negotiating a fig-leaf settlement is a sign of initiative, while going after individual bankers upsets your future bosses and dramatically lowers your long-term earning potential. Hence the unwillingness of Powell and Cohen to state obvious truths.

On the other hand, the increasing size of the fines seems to indicate that something has changed. Maybe, having won re-election, the president is thinking more about his legacy and less about ad spending, and is willing to forego some of Wall Street’s millions in order to seem tough on the banking aristocracy. Wonder what the democrats who do have to run for election think of this sudden change?

But if legacy is the motivating factor here, the strategy is failing, because the size of the fines only serves to illustrate the magnitude of the crimes – and the outrageousness of letting the actual people who committed the crimes go untouched and unshamed. – by John Rubino DollarCollapse.com

The Consumer Price Index (CPI) rose 1.1% in the 12 months to September, matching the increase in August.

The Bank of Canada’s core index rose 1.3% in the 12 months to September, matching the increase in August.

On a monthly basis, the seasonally adjusted core index rose 0.1% in September, after posting no change in the previous month.

As the CPI came in as expected the Canadian Dollar is unchanged on the day.

Drew Zimmerman

Investment & Commodities/Futures Advisor

604-664-2842 – Direct

604 664 2900 – Main

604 664 2666 – Fax

800 810 7022 – Toll Free

You are about to learn one of the biggest secrets in the history of the world…it’s a secret that has huge effects for everyone who lives on this planet. Most people can feel deep down that something isn’t quite right with the world economy, but few know what it is. Gone are the days where a family can survive on just one paycheck…every day it seems that things are more and more out of control, yet only one in a million understand why. You are about to discover the system that is ultimately responsible for most of the inequality in our world today. The powers that be DO NOT want you to know about this, as this system is what has kept them at the top of the financial food-chain for the last 100 years…

You are about to learn one of the biggest secrets in the history of the world…it’s a secret that has huge effects for everyone who lives on this planet. Most people can feel deep down that something isn’t quite right with the world economy, but few know what it is. Gone are the days where a family can survive on just one paycheck…every day it seems that things are more and more out of control, yet only one in a million understand why. You are about to discover the system that is ultimately responsible for most of the inequality in our world today. The powers that be DO NOT want you to know about this, as this system is what has kept them at the top of the financial food-chain for the last 100 years…

Learning this will change your life, because it will change the choices that you make. If enough people learn it, it will change the world…because it will change the system . For this is the biggest Hidden Secret Of Money. Never in human history have so many been plundered by so few, and it’s all accomplished through this…The Biggest Scam In The History Of Mankind.

IRELAND: THE LIFEBLOOD OF THE EUROZONE FOR THE NEXT FEW DAYS

IRELAND: THE LIFEBLOOD OF THE EUROZONE FOR THE NEXT FEW DAYS

J.R.R. Tolkien

Greetings!

The 20-period Bollinger Bands on a chart of EIRL (iShares MSCI Ireland Capped ETF) narrowed dramatically. And now they are expanding. Along those lines, an indicator I like to watch suggests EIRL is in the second day of a five-day move to the upside.

I suspect such a move could coincide with the last hurrah for Eurozone markets in the intermediate-term …

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair