This remarkable ascent, which has also driven the euro to its highest level against the yen since the 2008-09 financial crisis, means that European exporters are losing competitiveness, Americans and Asians who live or travel in Europe are feeling like poor relations and many economists are starting to worry that Europe’s nascent economic recovery will be snuffed out.

Purely financial players, by contrast, seem to be more enthusiastic about the euro’s strength than they have been for years. Speculative futures bets in favor of further euro appreciation have reached their highest level since the summer of 2011 — and the only time they were higher than that in the past decade was in the period just before the Lehman shock. Significantly, both of these speculative crescendos were followed by sharp euro declines, since currency markets generally turn when bullish sentiment reaches extreme levels. But there is a deeper reason to expect the euro’s seemingly irresistible rise to reverse.

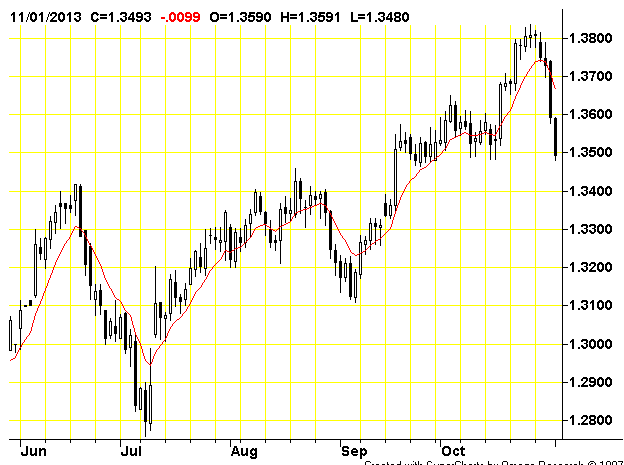

Currencies tend to move in trends for many years, and the fact is that the euro’s long-term trend against the dollar is still almost certainly downwards, despite the big gains of the past few months.

The euro’s long-run trend against the dollar turned down decisively more than five years ago. Since the euro hit an all-time peak of $1.60 in April 2008 it has moved in several cycles, making lower highs and lower lows. The previous peak before this week’s was in April 2011 at $1.48 and the one before that was in November 2009 at $1.52. The subsequent lows, in June 2010 and July 2012, were both around $1.20. It seems reasonable to expect this level to be tested again in the next year or so.

The direction of the dollar’s long-term trend against the euro (and before that the deutsche mark) has always been determined mostly by events in America, rather than Europe. The dollar rose strongly from 1980 to 1985, driven by the surging confidence in U.S. geopolitical power and economic revival under Ronald Reagan. The dollar then fell even more sharply from 1985 to 1991, as Presidents Reagan and then Bush consciously pursued a policy of dollar devaluation. After trading sideways until 1995, the dollar then appreciated strongly again until 2001 as the U.S. enjoyed the extraordinary economic growth and fiscal improvement under President Clinton, with the federal budget deficits completely eliminated for the first time. This trend reversed within weeks of President George W. Bush’s election and the dollar declined almost monotonically from January 2001 until April 2008.

Behind the scenes there has been official disgust with Germany at the highest policy levels for years now because of their seeming explicit exploitation of the credit crunch. While the other big countries did their fair share to provide stimulus-the US, UK, Japan, and China -Germany did their share to make their captive little market called the Eurozone viable enough for German industrialists to get their hooks in deeper to the periphery countries who have seen domestic industry vanish.

Behind the scenes there has been official disgust with Germany at the highest policy levels for years now because of their seeming explicit exploitation of the credit crunch. While the other big countries did their fair share to provide stimulus-the US, UK, Japan, and China -Germany did their share to make their captive little market called the Eurozone viable enough for German industrialists to get their hooks in deeper to the periphery countries who have seen domestic industry vanish.

“Our main format is now video analysis…”

“Our main format is now video analysis…”