Bonds & Interest Rates

|

These Stocks Yield Up to 13.5%… But I Doubt You Know About Them |

|

My husband Melvin and I bought our first home when we were expecting our first child. After an exhaustive search, we settled on an up-and-down duplex. It was built in the 1940s and had a rental suite in the basement. The purchase was a good decision from a financial standpoint. Rental payments covered a substantial part of our mortgage, and about two years later we were able to sell it for 20% more than we paid. But from a lifestyle perspective, it was not ideal. First, the rental suite’s bathroom faucet started leaking. Then ceiling tiles came tumbling down. Soon the rent was a week overdue and counting. There was always something. I learned some important lessons from that experience. First, carefully selected real estate could be highly profitable. Second, I didn’t want to deal with the upkeep required by rental properties. Thankfully, there are real estate investment trusts (REITs). As an income investor, you likely know plenty about these securities. REITs own leased property, letting investors own a diversified portfolio of properties and letting someone else look after the hassles of managing them. As one of my first picks for my premium High-Yield Investing advisory, I added shopping center REIT Simon Property Group (SPG) at $53.00 per share in August 2004. I sold it nearly three years later at $94.95, after collecting $9.06 per share in distributions, for a total return of 96%. Equity Inns (NYSE: ENN), a lodging REIT added shortly after in January 2005, did even better. Total returns were 118% in just under three years. Sun Communities (NYSE: SUI), which runs manufactured home communities, was added in October 2010 and so far has provided total returns of about 40% in just over a year and a half. You can see why I like REITs. There’s just one problem. U.S. REITs have been sharply bid up since the spring 2009 bottom. As a result, their yields, which move inversely to prices, have come down. U.S. equity (non-mortgage) REITs are yielding an average 3.4%, according to the benchmark MSCI U.S. REIT index. The solution? Canadian REITs. You may not have heard of them, but Canadian REITs (CanREITs) are similar in many ways to their U.S. counterparts. As in the United States, to qualify as a REIT in Canada at least 75% of revenues must come from rental income. CanREITs also pay out most of their taxable income to avoid paying corporate taxes and maintain their REIT status. Better yet, while most U.S. REITs pay dividends quarterly, most CanREITs pay monthly. One difference between the two is that most U.S. REITs are corporations, but CanREITs are generally unincorporated investment trusts. That means, in case of bankruptcy, unitholders would be responsible for the REIT’s liabilities. However, CanREITs typically guard against this possibility by purchasing insurance and excluding unitholders from liability in their loan contracts wherever possible. The biggest difference, though, is their size. In the United States, you can choose among dozens of large capitalization REITs. Simon Property Group (NYSE: SPG), for example, has a market cap of around $45 billion. In Canada, the selection is more limited. The largest REIT by market cap is RioCan (TSX: REI.UN; OTC: RIOCF), a shopping center developer with a market cap of $7 billion. Only 16 CanREITS have market caps over $1 billion.

But at this point, many Canadian REITs are yielding higher than their U.S. counterparts. The average Canadian REIT pays a 5.0% yield, compared to 3.4% for U.S. REITs. This includes Canada’s Scott’s REIT (TSX: SRQ.UN; OTC: SOREF), which owns buildings leased to KFC, Taco Bell, Subway, and Shell gas stations, among others. Right now the shares yield more than 13.5%. Meanwhile, Canada has a healthy housing market, strong banks, and effective government policy that underlie a healthy business environment. As measured by the S&P Case-Shiller U.S. Home Price Index, housing prices in the U.S. have declined 26% as of the end of 2011. In contrast, housing prices across Canada actuallyincreased 17% during that period, as measured by Canada’s National Bank Home Price Index Composite. Of course, the key to successful REIT investing is selecting the specific property sector most likely to benefit from the current economic environment. There’s no guarantee, but in my view the two strongest Canadian REIT sub-sectors right now are office space and apartments. In many Canadian cities, the going market rate for office rents is now higher than lease rates. When these leases expire, therefore, rents should rise, driving REIT cash flow higher and potentially boosting distributions for office REITs. Meanwhile, there’s a lack of new multi-family supply in Canada. Consistent and stable demand is based on population growth and the housing needs of new immigrants. Proposed legislation to make underwriting standards harder for first-time home buyers may also lead to more people remaining as renters. One more thing… You might think it’s difficult to buy Canadian stocks. However, the vast majority of large-cap Canadian REITs are inter-listed and trade on an over-the-counter (OTC) exchange in the United States. Many U.S. brokers, such as T.D. Ameritrade and Interactive Brokers, provide easy online access to the Toronto exchange, but some brokers may require you to place a phone order. You can also trade Canadian REITs over the counter in the United States, but liquidity is more limited than if you trade directly on the Toronto exchange. Good Investing!

P.S. — If you haven’t already seen it, don’t miss StreetAuthority’s report — Top 5 Income Stocks for 2012. These five select investments pay dividend yields of 7.5%… 8.8%… even 11.5%. For more details on these investments you can visit this link. Disclosure: StreetAuthority owns SUI as part of High-Yield Investing’s model portfolio. In accordance with company policies, StreetAuthority always provides readers with at least 48 hours advance notice before buying or selling any securities in any “real money” model portfolio. Members of our staff are restricted from buying or selling any securities for two weeks after being featured in our advisories or on our website, as monitored by our compliance officer. |

Waving the White Flag

Viva Los Rescates Financieros de los Bancos

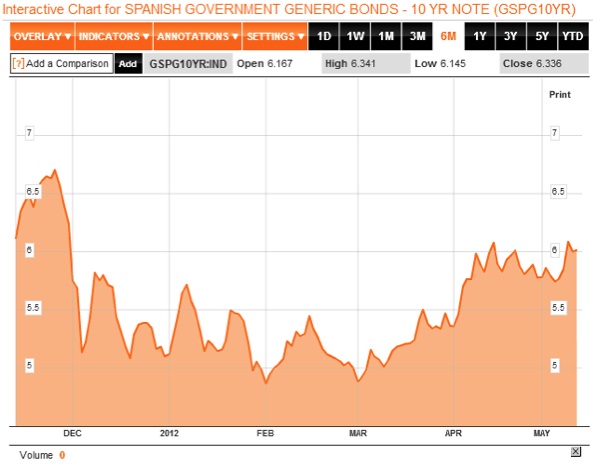

Contagion is Real It Doesn’t End With Spain

New York, Atlanta, and Philadelphia

A common mistake that people make when trying to design something completely foolproof is to underestimate the ingenuity of complete fools.

– Douglas Adams, The Hitchhiker’s Guide to the Galaxy

For quite some time in this letter I have been making the case that for the eurozone to survive, the European Central Bank would have to print more money than any of us can now imagine. That the sentiment among European leaders was that they were prepared for such a move was clear – except for Germany, which is haunted by fears of a return to the days of the Weimar Republic and hyperinflation.

When Germany agreed to a fixed monetary union and a European Central Bank, it was with the clear understanding that it would be run along the lines of the German central bank, the Bundesbank. The members of the Bundesbank and the German members of the ECB were most outspoken about the need for a conservative monetary policy that would keep a clamp on inflation.

However, as I have previously noted, the Bundesbank was a toothless tiger. Germany has two votes out of 23 on the ECB, and the loud drumbeat from most of Europe, which is experiencing the difficulty of austerity accompanied by too much debt, is for a far more accommodating ECB.

The simple fact is that Mario Draghi, the Italian president of the ECB, created €1 trillion euros to help fund European banks, which promptly turned around and bought their respective countrys’ sovereign debt. Germany’s Angela Merkel forced the Bundesbank to “play nice” and go along with what was seen as the only way to solve a growing banking crisis in Europe. Everyone breathed a sigh of relief, thinking that this at least bought a year during which things could be sorted out. But it turns out that a trillion euros just doesn’t go as far as it used to. The “relief” lasted about a month. The last few weeks have presented yet another budding crisis, as least as large as the last one. Where to get the next trillion?

This week the German Bundesbank waved the white flag. The die is cast. For good or ill, Europe has embarked on a program that will require multiple trillions of euros of freshly minted money in order to maintain the eurozone. But the alternative, European leaders agree, is even worse. Today we will look at the recent German shift in policy, why it was so predictable, and what it means. This is a Ponzi scheme that makes Madoff look like a small-time street hustler. There is a lot to cover.

At the end of the letter I will mention a few upcoming speaking engagements, in Atlanta, Philadelphia, and a webinar I will be doing next week. Now let’s jump over to Europe.

Waving the White Flag

It is the world’s worst-kept secret: Germany does not want inflation but wants to abandon the European Union even less. And as we will see, the eurozone simply does not have enough money to keep itself together without massive ECB intervention.

“Cry havoc,” wrote Shakespeare in Julius Caesar, “and let slip the dogs of war.” The military order “Havoc!” was a signal given to the English military forces in the Middle Ages to direct the soldiery (in Shakespeare’s parlance “the dogs of war”) to pillage and incite chaos.

The cry is much the same in Europe today, though it is not the dogs of war that will ravage the land but the hounds of inflation. The English edition of Spiegel Online today carries a story with the headline “High Inflation Causes Societies to Disintegrate.”

To Read More CLICK HERE

Debt, risk and employment are in a death-spiral of malinvestment and debt-based consumption.

Standard-issue financial pundits (SIFPs) and economists look at debt, risk and the job market as separate issues. No wonder they can’t make sense of our “jobless recovery”: the three are intimately and causally connected. An entire book could be written about debt, risk and jobs, but let’s see if we can’t shed some light on a complex dynamic in a few paragraphs.

Risk: As I described in Resistance, Revolution, Liberation: A Model for Positive Change, risk cannot be eliminated, it can only be shifted to others or temporarily masked.

Masking risk simply lets it pile up beneath the surface until it brings down the entire system. Transferring it to others is a neat “solution” but when it blows up then those who took the fall are not pleased.

Risk and gain are causally connected: no risk, no gain. The ideal setup is to keep the gain but transfer the risk to others. This was the financial meltdown in a nutshell: the bankers kept their gains and transferred the losses/risk to the taxpayers via the bankers’ toadies and apparatchiks in Congress, the White House and the Federal Reserve.

Risk is like the dog that didn’t bark. In the story Silver Blaze, Sherlock Holmes calls the police inspector’s attention to the fact that a dog did something curious the night in question: it did not bark when it should have.

When scarce capital is misallocated to unproductive uses such as duplicate tests that can be billed to Medicare, sprawling McMansions in the middle of nowhere, etc., “the dog that didn’t bark” is this question: what productive uses for that scarce capital have been passed over to squander the scarce capital on Medicare fraud, McMansions, Homeland Security (“Papers, please! No papers? Take him away”), etc.

Once the capital has been squandered, it’s gone, and the opportunity to invest it in productive uses has been irrevocably lost.

Debt: Debt has a funny cost called interest. If you have a corrupt, self-serving central bank (a redundancy) that can lower interest rates by printing money to buy government bonds, then this funny thing called interest can be lowered to, say, 1%.

At 1% interest, the government can borrow $100 and only pay 1% in annual interest. That is almost “free,” isn’t it? The key word here is “almost.” If you borrow enough, then that silly 1% can become rather oppressive.

Let’s say the Federal Reserve is willing to loan you $100 billion at zero interest. You have an incredible sum of cash to use for speculation, and it doesn’t cost anything! Wow, you must be an investment banker….

Now what happens when the interest rate goes from zero to 1%? Yikes, you suddenly owe $1 billion a year in interest. That is some serious change. You can of course pay the interest out of the borrowed $100 billion, unless you’ve spent it building bridges to nowhere and supporting crony capitalism.

To Read More CLICK HERE

I recently had a chance to speak at a conference where Dr. Ian Bremmer spoke after me. I was very impressed with his thought process and asked him to give me an outline of his speech to share with you for this week’s Outside the Box. It’s a shorter version of his powerhouse book, Every Nation for Itself: Winners and Losers in a G-Zero World. I highly recommend it.

And what, you’re asking, is a “G-Zero world”? In a word, it’s a leaderless world. A world in which, as Bremmer says, “Not so long ago, America, Western Europe and Japan were the world’s powerhouses. Today, they’re struggling to recover their dynamism…. But nor are rising powers like China, India, Brazil, Turkey, the Gulf Arabs and others ready to take up the slack…. If not the West, the rest, or the institutions where they come together, who will lead? The answer is, no one.”

And that means the world’s big problems won’t get addressed as effectively as they should, as long as the leadership vacuum persists. Talk about Muddling Through!

This book by Bremmer is going to make a difference, and I’m not the only one who thinks so –

“Ian Bremmer combines shrewd analysis with colorful storytelling to reveal the risks and opportunities in a world without leadership. This is a fascinating and important book.” –FAREED ZAKARIA

“Every Nation for Itself is a provocative and important book about what comes next. Ian Bremmer has again turned conventional wisdom on its head.” –NOURIEL ROUBINI

Tonight I am in Chicago, where I spoke at the CFA conference this morning. It went well. I will try to get a link for you later. It hasn’t been all work, either. David Rosenberg, Barry Ritholtz, and I all had dinner gigs, but we met up at the bar and just hung out for about three hours. Got to love O’Doul’s NA beer. Not quite the same as a good chardonnay but healthier for me.

I will hit the send button as I have to get up for a breakfast meeting with Sam Zell. We have never met and I am looking forward to it. He is quite the legend. I will give you an update on the conference next weekend. The reviews are coming in quite strong. It was interesting to see the European elections after the analysis we were given. There is so much that seems up in the air. You can almost feel the changes coming. I feel like the kid in the back of the car on a long road trip: “Are we there yet?”

Your holding out for a world that works analyst,

John Mauldin, Editor

Outside the BoxJohnMauldin@2000wave.com

Every Nation for Itself: Winners and Losers in a G-Zero World

Ian Bremmer

One beautiful fall evening in October 2011, I gave a speech on international politics to a group of Canadian business executives in Napa Valley, California. As part of the introduction, I included a few thoughts on the G20, the forum in which 19 countries plus the European Union bargain over solutions to pressing international problems. I made my case for why I believe the G20 is a dysfunctional institution that will create as many problems as it solves. The speech complete, I joined members of the audience for dinner on a beautiful terrace overlooking a vineyard. Our host, spotting an opportunity for lively conversation, seated me next to a distinguished looking gentleman I’d never met—former Canadian Prime Minister Paul Martin. This is the man who created the G20.

As Canada’s finance minister (1993-2002), then prime minister (2003-2006), Martin warned that Western dominance of international financial institutions couldn’t last and that the world needed a new bargaining table, one that welcomed leading emerging powers as full partners. Martin’s argument fell on deaf ears in America, Europe, and Japan—until the 2008 financial crisis made his point for him.

To Read More CLICK HERE

As I said, there can also be the problem of those in the real world being ignorant of how government truly functions as well. I have straddled both worlds and try to relay what I have learned from a unique position I have had for decades. This is why there has been a major effort by those in New York to shut me up at all costs, because what I have to say will kill the golden goose that fuels the corruption in New York City. Government is NEVER rational or logical in its thinking process. This is exploited by New York banks on a regular basis. Installing bankers as the head of the US Treasury is far better than the head of the Fed. This gives them cabinet status and direct links into Congress as well as the White House.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair