Bonds & Interest Rates

QUESTION: Do you support Trump increasing the debt by a trillion dollars? I thought you were conservative?

PY

ANSWER: Well the first thing you have to do is get a grip on what is a reality. Governments around the globe borrow every single year with absolutely no intention of ever paying off their national debts. So what is the difference? If you think giving the money back to the people is wrong and it is better going out the back door for political contributions, then sorry, I oppose that.

There is no “conservative” v “liberal” when it comes to the debt. They all spend more than they take in and nobody cares about paying off the debts. So I do not care what political persuasion you are, we will end up at the same place when the dice stop rolling. BROKE!

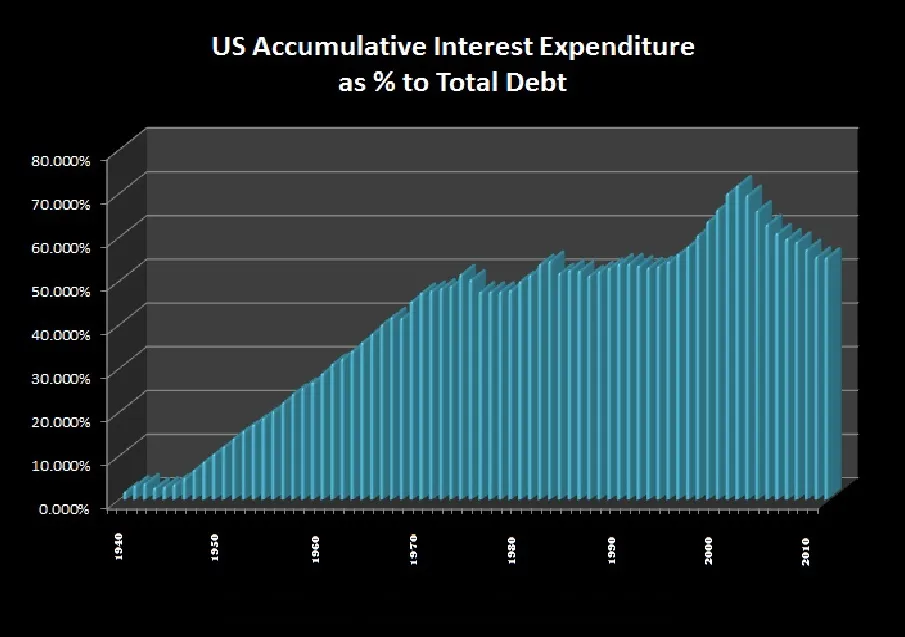

I support cutting income taxes to ZERO. The government should just create the money it needs to cover its expenses. Let’s get real here! All national debts, including Germany, show that on average 70% of the debt is just accumulative interest. So that is money out the back-door.

Rome never had a national debt and the first 500 years they existed by creating money to pay their expenses with minimal inflation because of the economic growth. About 80% of their budget was paid with the creation of new money.

Even the Bible said giving 10% was realistic, not 40% to 60% as we have under the current Marxist style governments in the West.

The first country that wakes up and abolishes income taxes will blow everyone else out of the water. All they have to do is say they will adopt the way the United States became great. There were only indirect taxes between 1792 and 1913. If the nation survived with no income taxes, we can do it again and let the people spend their own money. You will see massive job creation and governments will stop competing with the private sector to borrow money.

….also from Martin:

The US economic boom is still in progress, where a boom is defined as a period during which monetary inflation and the suppression of interest rates create the false impression of a growing/healthy economy*. We know that it is still in progress because the gap between 10-year and 2-year Treasury yields — our favourite proxy for the US yield curve — continues to shrink and is now the narrowest it has been in 10 years.

Reiterating an explanation we’ve provided numerous times in the past, an important characteristic of a boom is an increasing desire to borrow short to lend/invest long. This puts upward pressure on short-term interest rates relative to long-term interest rates, which is why economic booms are associated with flattening yield curves. The following chart shows the accelerating upward trend in the US 2-year yield that was the driving force behind the recent sharp reduction in the 10yr-2yr yield spread.

The above paragraph explains why a yield-curve trend reversal from flattening to steepening invariably occurs around the time of a shift from economic boom to economic bust. Such a reversal is a sign that the willingness and/or ability to take on additional short-term debt to support investments in stocks, real estate, factors of production and long-term bonds has diminished beyond a critical level. From that point forward, a new self-reinforcing trend involving debt reduction and the liquidation of investments becomes increasingly dominant.

The recent performance of the yield curve indicates that the US economy hasn’t yet begun the transition from boom to bust.

*The remnants of capitalism enable some genuine progress to be made during the boom phase, but the bulk of the apparent economic vibrancy is associated with monetary-inflation-fueled price rises and activities that essentially consume the ‘seed corn’.

Folks, the ‘yield’s rising to the limiters’ near-term plan has been frustrating. Not for my own investment and trading because I’ve stayed balanced with a focus on interest rate neutral sectors, but because it makes so much sense within the context of several different macro items that could one day come together to form a massive macro fundamental sell signal on the stock market.

Those components are for stocks to finish outperforming vs. gold, 10 & 30yr yields to rise to 2.9% & 3.3% (+/-), respectively and for the yield curve to make a low. Thing 2 seemed like it was engaging when the daily 10 & 30yr yield charts made bottoming patterns and Things 1 & 3 are in process but could still have quite a way to go.

A couple days ago I affixed my tin foil hat and speculated about the coming of Operation Twist by another name and method. Who knows whether or not the bond market is factoring any of that in yet but taken at face value, its implication would hinder long-term yields and while it serves to keep the macro nice and bullish with a flattening yield curve, it would at least drive the curve down toward future resolution.

Here again are the big picture components. By all views there appears a playable amount of upside left in risk ‘on’ items, especially stocks. The graphic has aged a couple weeks and the yield curve has actually dropped further, but you get the picture.

….for more charts and analysis go HERE

….also from NFTRH:

It’s been awhile since I’ve used this terminology. But global markets this week recalled the old “Bubble in Search of a Pin.” It’s too early of course to call an end to the great global financial Bubble. But suddenly, right when everything looked so wonderful, there are indication of “Money” on the Move. And the issues appears to go beyond delays in implementing U.S. corporate tax cuts.

It’s been awhile since I’ve used this terminology. But global markets this week recalled the old “Bubble in Search of a Pin.” It’s too early of course to call an end to the great global financial Bubble. But suddenly, right when everything looked so wonderful, there are indication of “Money” on the Move. And the issues appears to go beyond delays in implementing U.S. corporate tax cuts.

The S&P500 declined only 0.2%, ending eight consecutive weekly gains. But the more dramatic moves were elsewhere. Big European equities rallies reversed abruptly. Germany’s DAX index traded up to an all-time high 13,526 in early Tuesday trading before reversing course and sinking 2.9% to end the week at 13,127. France’s CAC40 index opened Tuesday at the high since January 2008, only to reverse and close the week down 2.5%. Italy’s MIB Index traded as high as 23,133 Tuesday before sinking 2.5% to end the week at 22,561. Similarly, Spain’s IBEX index rose to 10,376 and then dropped 2.7% to close Friday’s session at 10,093.

Having risen better than 20% since early September, Japanese equities have been in speculative blow-off mode. After trading to a 26-year high of 23,382 inter-day on Thursday, Japan’s Nikkei 225 index sank as much as 859 points, or 3.6%, in afternoon trading. The dollar/yen rose to an eight-month high 114.73 Monday and then ended the week lower at 113.53. From Tokyo to New York, banks were hammered this week.

Perhaps the more important developments of the week unfolded in fixed-income.

– Diversify, rebalance investments and prepare for interest rate rises

– UK launches inquiry into household finances as £200bn debt pile looms

– Centuries of data forewarn of rapid reversal from ultra low interest rates

– 700-year average real interest rate is 4.78% (must see chart)

– Massive global debt bubble – over $217 trillion (see table)

– Global debt levels are building up to a gigantic tidal wave

– Move to safe haven higher ground from coming tidal wave

Editor: Mark O’Byrne

Source: Bloomberg

Last week, the Bank of England opted to increase interest rates for the first time in a decade. Since then alerts have been coming thick and fast for Britons warning them to prepare for some tough financial times ahead.

The UK government has launched an inquiry into household debt levels amid concerns of the impact of the Bank of England’s decision to raise rates. The tiny 0.25% rise means households on variable interest rate mortgages are expected to face about £1.8bn in additional interest payments whilst £465m more will be owed on the likes of credit cards, car loans and overdrafts.

The 0.25% rise is arguably not much given it comes against backdrop of record low rates and will have virtually no impact on any other rate. However it comes at a time of high domestic debt levels, no real wage growth and a global debt level of over $217 trillion.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair