Bonds & Interest Rates

QUESTION: Hi Marty,

I continue to read your blog and if I understand correctly, interest rates are going up.

My question is, can one profit from higher interest rates such as buying CD or bank stocks like Wells Fargo?

ANSWER: The one thing you do not want to do is buy a CD with maturity. As rates go higher, you will be locked in and unable to take advantage of the rising rates. Bank stocks will not benefit from higher rates in general. So that is not a valid reason to buy bank stocks. The safest thing would be to buy US TBills or agency paper no more out than 90 days and keep the cash rolling in that area until we reach a point when the rates are peaking. Toward the end, the yield curve will invert so that means the short-term rates will exceed long-term when confidence is shaken.

In an upward cycle for interest rates, never lock & load – always stay nimble if you are the investor. If you are the borrower – load & load fixing the rate out as long as possible.

….related from Martin: Russia Dumps US Bonds – Is it Politics or Yield?

US junk-bond issuance in June plunged 31% from a year ago to just $14.5 billion, the lowest of any June in five years, according to LCD of S&P Global Market Intelligence. During the first half of the year, junk bond issuance dropped 23% from a year ago to $110.6 billion.

Is investor appetite for risky debt drying up? Have investors given up chasing yield? On the contrary! They’re chasing harder than before, but they’re chasing elsewhere in the junk-rated credit spectrum…. CLICK for the complete article

The Federal Reserve’s decision today to hike its policy rate by 25 basis points (bps) to a range of 1.75% to 2.0% was widely expected. The Federal Open Market Committee (FOMC) also signaled growing consensus that the robust pace of economic activity warrants two more rate hikes this year, for a total of four in 2018. But the elimination of forward guidance in the Fed’s statement,coupled with today’s announcement that it will hold a press conference after every meeting starting next January, is perhaps the most interesting aspect of today’s meeting: It underscores the Fed’s medium-term dilemma of how to set policy that sustains the expansion by balancing the risk of overtightening with the risk of overheating the economy.

The Federal Reserve’s decision today to hike its policy rate by 25 basis points (bps) to a range of 1.75% to 2.0% was widely expected. The Federal Open Market Committee (FOMC) also signaled growing consensus that the robust pace of economic activity warrants two more rate hikes this year, for a total of four in 2018. But the elimination of forward guidance in the Fed’s statement,coupled with today’s announcement that it will hold a press conference after every meeting starting next January, is perhaps the most interesting aspect of today’s meeting: It underscores the Fed’s medium-term dilemma of how to set policy that sustains the expansion by balancing the risk of overtightening with the risk of overheating the economy.

Finding neutral

Late-cycle fiscal stimulus, a flat Phillips curve and the high degree of uncertainty around the neutral interest rate – the rate at which the Fed is no longer accommodative and starts restricting the economy’s growth – complicate the Fed’s medium-term risk management task.

On the one hand, uncertainty over the neutral rate, coupled with the long lags needed for monetary policy to affect the real economy, argues for hiking gradually – or even pausing to assess the cumulative effects of the seven hikes, including today’s, since late 2015. The flattening Treasury yield curve could indicate that monetary policy is close to becoming restrictive, which could choke off growth more than the Fed intends.

On the other hand, late-cycle fiscal stimulus and still-easy financial conditions with unemployment at historically low levels raise the risk that inflation accelerates. If inflation expectations start to rise, the Fed could find itself in a nasty inflation spiral. As in the late 1970s and early 1980s, this could require a recession to restrain.

Focusing on overtightening could steepen curves and boost inflation-risk premiums

On its own, the elimination of forward guidance points to wider possibilities and more divergent views of the future path of the fed funds rate, as rates approach neutral. Today’s Statement of Economic Projections maintains the path of interest rate hikes will remain gradual (it showed an additional hike in 2018, but this was balanced by one less hike in 2020) and foresees only a small inflation overshoot. Taken together, this suggests that policymakers may still be slightly more focused on managing the risk of overtightening (while not ignoring overheating risks). Little evidence of U.S. financial market imbalances and well-behaved inflation also support this focus.

We continue to expect The New Neutral framework of low equilibrium policy rates will anchor Fed policy and U.S. fixed income markets. However, it’s important to keep the risks in mind. At a minimum, the Fed’s continued focus on managing the risks of overtightening and its stated commitment to a “symmetric” inflation target still argue for steeper interest rate curves, and higher inflation-risk premiums, as outlined in “Key Takeaways From PIMCO’s Secular Outlook: Rude Awakenings.”

Tiffany Wilding is a PIMCO economist focusing on the U.S. and is a regular contributor to the PIMCOBLOG.

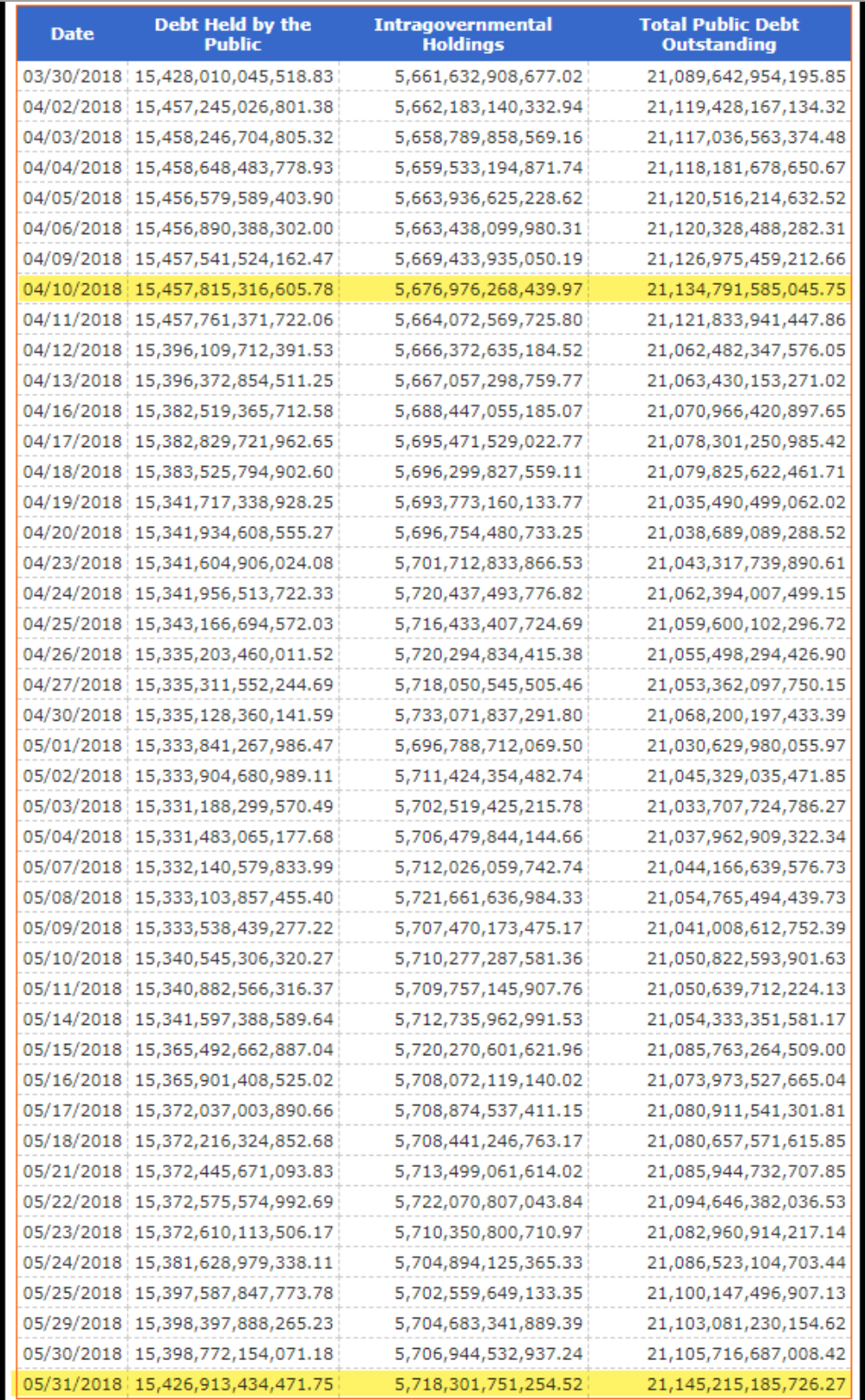

The total U.S. public debt hit a new record high of $21.145 trillion on the last day in May. As the U.S. debt increased, so did the interest expense which jumped by more than $26 billion in the first seven months of the fiscal year. That’s correct; the United States government forked out an additional $26 billion to service its debt (Oct.-Apr) versus the same period last year.

While the U.S. debt reached a new high on May 31st, it took nearly two months to do it. Let me explain. During tax season, the total U.S. public debt actually declined from a peak of $21.135 trillion on April 10th to a low of $21.033 trillion on May 3rd. Since then, the U.S. debt has been steadily moving higher (including some daily fluctuations):

If you spend some time on the TreasuryDirect.gov site, you will see that the total public debt doesn’t go up in a straight line. There are days or weeks where the total debt declines. However, the overall trend is higher.

Now, a rising debt level impacts the interest the U.S. Treasury must pay on this debt… especially when the average interest rate also increases. According to the TreasuryDirect.gov, the interest expense rose from $257.3 billion (Oct-Apr) 2017 to $283.6 billion (Oct-Apr) this year:

As I mentioned, the U.S. government paid an additional $26 billion to service the debt than it did last year. Now, $26 billion may not seem like a lot of money these days, but it could buy the total global Registered Silver inventory:

Thus, the extra $26 billion paid by the U.S. Treasury to service its debt would have purchased the 1+ billion ounces of silver held in the COMEX (270 million oz) and all the Global Silver ETFs. And, this would include the 138 million oz of silver supposedly stored at the JP Morgan vaults.

However, with the remaining $10 billion ($26 billion minus $16 billion), the U.S. government could have also purchased all the Silver Eagles minted since 1987. According to my figures, the U.S. mint sold over 510 million Silver Eagles from 1987-2018. If we give a value of $20 for each, that would be roughly $10.5 billion.

And remember, this is just the ADDITIONAL interest expense paid from Oct-April to service the massive U.S. public debt. If interest rates continue to stay the same or rise for the remainder of the fiscal year, the U.S. government will likely pay between $45-50 billion more in 2018 to service its debt.

Lastly, I am quite surprised by some of the analysis coming from the precious metals community. I will be writing about this at length in a new article, but it’s quite frustrating to see precious metals analysts totally disregard energy in their work or change the facts to promote a certain ideology.

For example, Bix Weir recently posted a new video on the “10 Reasons to own Silver.” While I agree with some of the reasons he states to own silver, I was quite stunned to see Mr. Weir state in his 8th Reason was due to a 1/1 Ratio of Gold to Silver. Bix remarked that there were about 6 billion ounces of above ground gold and silver, so this One-to-One ratio meant that silver was undervalued.

I get it. However, Bix has been claiming that the world has millions of tons of gold in the world. But if he states there are 6 billion oz of gold above ground, that is roughly 187,000 metric tons… a figure that I have reported to be accurate for several years.

So, which is it??

Check back for new articles and updates at the SRSrocco Report.

With things beginning to come unglued in key global markets led by the Italian trouble, is all hell about to break loose?

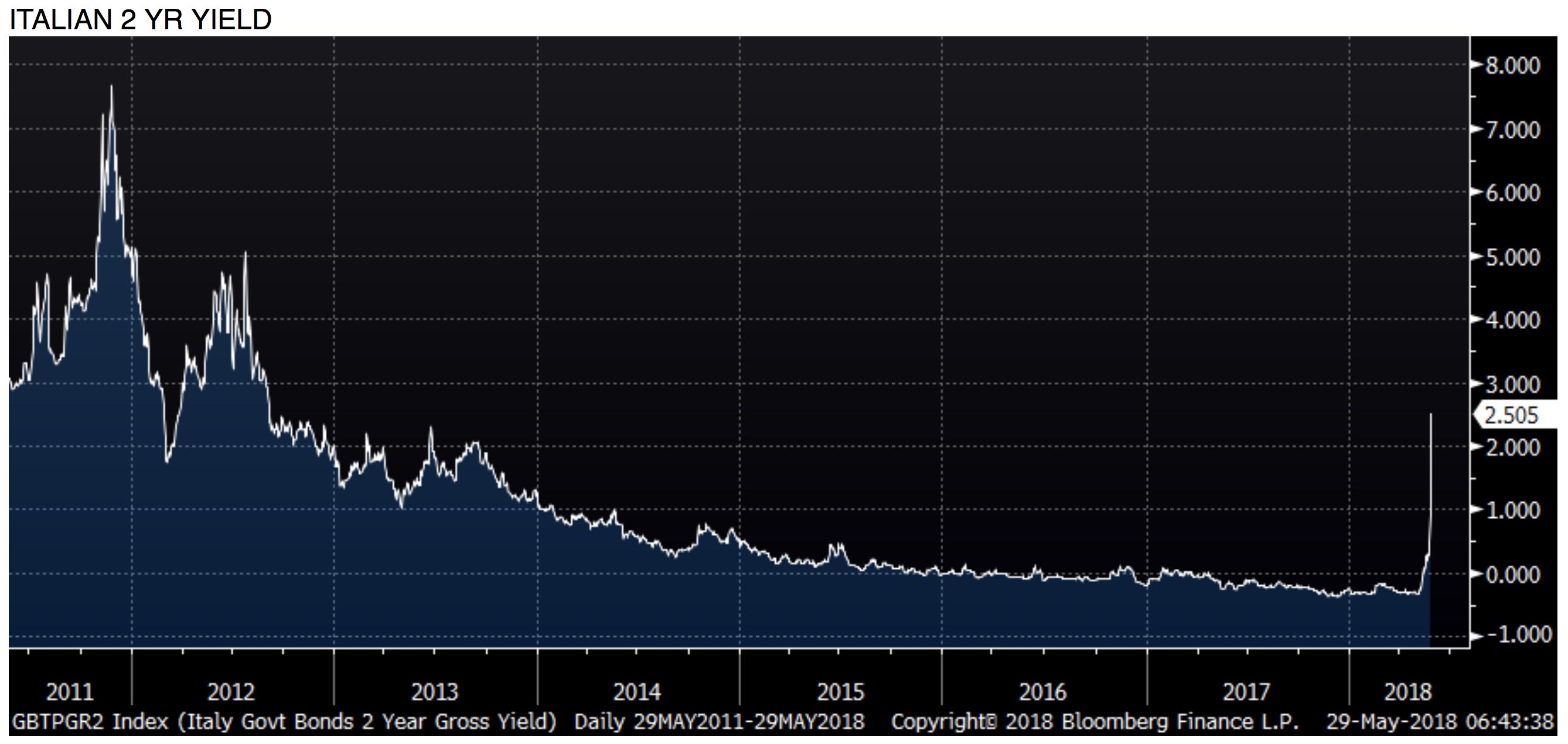

May 29 (King World News) – Here is what Peter Boockvar had to say as the world awaits the next round of monetary madness: The unwind of everything the ECB tried to suppress in the Italian bond market is now truly extraordinary and scary in its rapidity. The 163 bps (as of this writing) spike (or crash in bond price) takes the yield to 2.53%, the highest level since September 2012, just a few months after Mario Draghi said “whatever it takes” in wanting to save the euro.

The yield was about .60% when negative interest rate policy took hold in June 2014. The 10 yr jump is more tame, only 43 bps to 3.10% and that is about where it was in June 2014. I’ve called for a while the European bond market as an epic bubble that at least in Italy so far is coming undone. It’s however intensifying again in the flight to safety countries such as Germany, France and the UK. I can’t even begin to know how Mario Draghi deals with the mess that he sowed the seeds for (see chart below).

Massive Spike In Italian Yields!

also from KingWorldNews:

Is The Gold Market Finally Setup To Break The Gold Ceiling?

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair