Asset protection

Listener to MoneyTalks have heard many analysts and conservative money managers talk about using options to protect their portfolio from volatility and increase income.

Listener to MoneyTalks have heard many analysts and conservative money managers talk about using options to protect their portfolio from volatility and increase income.

We’ve arranged, in partnership with Desjardins Online Brokerage, to have Patrick Ceresna, Chief Strategist of Learn to Trade Global, to put on a FREE live webinar on how to use options following the show – 10:05am Pacific on Sept 26th.

Patrick will show examples of how you can use options to protect your capital, generate additional income and obtain quality stocks at discount prices.

The webinar system can support only the first 500 people who register.

If you have any difficulty with the registration system contact daniel.suen@vmd.desjardins.com directly.

As the world awaits the Fed decision this week, the Godfather of newsletter writers, 91-year-old Richard Russell, says the U.S. has a ticking time bomb, rigged markets and a desperate Fed. The legend also covered the major markets and the ultimate refuge.

As the world awaits the Fed decision this week, the Godfather of newsletter writers, 91-year-old Richard Russell, says the U.S. has a ticking time bomb, rigged markets and a desperate Fed. The legend also covered the major markets and the ultimate refuge.

”Come to the edge,” He said. They said, ”We are afraid.” ”Come to the edge,” He said. They came. He pushed them… and they flew.

”Come to the edge,” He said. They said, ”We are afraid.” ”Come to the edge,” He said. They came. He pushed them… and they flew.

Guillaume Apollinaire

The answer to this plain question should always be a resounding no: it never pays to give into panic. The smartest option is to derail this emotion before it gains any traction. Once fear takes over, the end is nigh.

When the markets were disintegrating approximately two weeks ago and if you were one of the lucky few that opted against joining the bandwagon of panic, you should have had a feeling of déjà vu; sort of like the movie ground hogs day. The same-old twaddle that was broadcasted before was once again intoxicating the masses; like cockroaches, these naysayers emerge from the woodwork and hum the same-old hymn “the world is going to end” and or financial disaster is around the corner. In each instance, you will find that the same rubbish is spun in a different way; this is recycling at its best. What they so conveniently omit is how each and every single one of these so-called end of the world events proved to be nothing but a mouth-watering opportunity for the astute investor. Now we are not stating that caution should be thrown against the wind. What we are simply stating is that if you become one with the fear, then this useless emotion will take over and blind you from seeing any opportunity, even if it slaps you hard on the face. Never become one with fear; understand that when it comes to trading fear is on par with toilet paper.

Let’s take a sombre look at what is actually going on, and why these events are unfolding.

It’s more than obvious that the market was in a corrective phase or crashing if one joins the naysayer’s camp; the more appropriate term would be letting out steam that was long overdue. The last week of August, was the worst week for equity markets since 2011. One could also point out that the markets have not experienced a significant pullback since 2011.

So what changed over the span of 1-2 weeks to warrant such negativity? Very little actually.

- China devalued its currency to boost exports; it had to; we are in the midst of a currency war, and most nations other than the U.S. are allowing their currencies to literally collapse. However, devaluing the currency affects sales and profits at many multinational companies, including those back in the U.S. So expect the U.S. to do something that has a negative impact on the dollar.

- The next issue is that the world’s second-largest economy is no longer growing as fast. Growth is slowing down and so far it appears the government’s response to address this has been ineffective. In the short term, this will continue to be the case, but over the long term, we think their policies will be conducive for the economy and stock market.

- Manufacturing activity is slowing down in China, and this has a big impact on the commodity markets. This is the primary reason many markets in this sector are experiencing severe corrections. Copper, oil, and iron to name a few have just fallen apart.

- The extreme plunge in energy prices while a relief for consumers, has unnerved investors. Though to be fair, a lot of this had to do with excess supplies. Demand is not keeping up with supplies, which is a clear indication that worldwide demand for oil is softening.

- Up until recently, the Fed’s decision to start raising rates was another factor weighing on the markets. That uncertainty is no longer an issue as the Fed has now signalled that it will not be raising rates. There is really no inflation problem to tackle. We are referring to the manufactured numbers that suggest all is well when the opposite holds true. This is what the masses believe and so this is what counts, as what they believe drives the markets. Energy prices are down significantly, and the raw materials sector is basically in a bear market. Wages are not rising; at best, they are stagnant. Over 50% of the components of the CPI (consumer price index) have declined in the past six months. TIPS are also signalling that for the foreseeable future, inflation is not going to be an issue. Under these circumstances, a rate hike would make no sense, and only further destabilize the markets. Let’s not forget the additional turmoil; a rate hike would cause in the currency markets. A rate hike would further strengthen the dollar, and adversely affect U.S. exports, making them less competitive in the global markets.

- Again, we do not necessarily agree with the low inflation scenario as rents are rising and the cost of many goods over the past several years have risen dramatically. What we believe in is not of importance, for, in the end, it’s the crowd that drives the market, up to a certain point. When emotions hit a boiling point, which they have not, then one can start taking a position that is opposite to that of the masses.

So what’s on the horizon?

Any expert who claims to know precisely what will occur should be ignored. Even a broken clock is correct twice a day. Hence, if an expert makes a large enough number for pronouncements, one of them is bound to come to pass. It does not mean that individuals cannot determine the direction of the markets. As we have stated many times before, there is a vast chasm that separates spotting market bottoming and topping action, with trying to identify the exact top or bottom.

Investor confidence has taken a beating. Under these conditions, many investors will either sit on the sidelines or take some money out of the markets. This is good for it will drive stocks to even more attractive levels. The masses are well-known for their ability to buy and sell at precisely the wrong time.

Some bullish or reassuring factors to consider:

- Traders are not overtly bullish.

- Stocks are selling for roughly 17 times their trailing earnings. While not cheap, these valuations are by no means excessive. The long-term average is roughly 16.5 times earnings.

- Unemployment is down, and U.S. Manufacturing levels are rising.

- Corporations are flush with money.

- Banks are in much better shape than they were in during the financial crisis a few years ago.

- Insiders are not dumping shares; they are actually stepping in and buying them.

The technical outlook

Our proprietary strength indicator has turned negative on the markets and this indicates that the lows will be tested again. The trend based on our Trend indicator has also turned neutral and V readings (our proprietary tool that measures market volatility) has soared to an all-time new high. Hence, we expect extreme moves to be the norm for the next few months. It would not surprise us if the Dow experiences a 1500-2000 point move over the span of one week.

The Dow is having a remarkably hard time of trading above 17000, former support turned into resistance. After the selloff in August, a lot of technical indicators moved into the extremely oversold ranges. Thus, the corresponding rally should have been much stronger. Additionally our own indicators are not validating the current move up, which strongly hints that the lows will have to be tested again. If the Dow closes below 15500 on a weekly basis, then we expect the Dow to make a quick move down to the 14500-14700 ranges; if this were to occur, we could term it a screaming buy event.

Conclusion

Some additional factors to keep in mind:

- The housing sector is relatively strong. Purchase applications are up 18% year over year.

- U.S. employees added 215,000 jobs in July

- Latest data shows that U.S. Economy grew at 3.7% in the 2nd quarter, up from the initial estimate of 2.3%

It is interesting to note that the naysayers like clockwork start their chanting and howling specifically after the markets have started to correct; their screams are rather muted when the market is trending upwards. If you look at history, their record is rather dismal, as every so-called disaster and or end of the world scenario, these naysayers pandered about turned to be exactly the opposite of what they predicted. Instead, each of these so-called disaster scenarios proved to be nothing but splendid buying opportunities in disguise. Disasters will come and go. Depending on the lens you use to view such a situation, it can either represent a splendid opportunity or a monumental tragedy. History is replete with examples quite clearly illustrating that financial disasters usually make for splendid opportunities.

We are not advocating that you run out and lunge into the markets; we have been stating for quite some time that the markets needed to let out some steam. Note, that the markets have not experienced significant correction since 2011. It would be folly to assume that the markets will trend in one direction without letting out a burst of steam. The markets have already shed roughly 15% from high to low. Given the heights they have run to since 2011, a 20% move would still be acceptable and nothing to fear. At this point, prudence is warranted, but a massive sell-off should be viewed as a buying opportunity, in contrast to a colossal tragedy. Our general suggestion would be to buy when panic sets in, and blood is flowing freely in the streets. Be wary when the masses are joyous and delighted when they are not.

I envy paranoids; they actually feel people are paying attention to them.

Susan Sontag

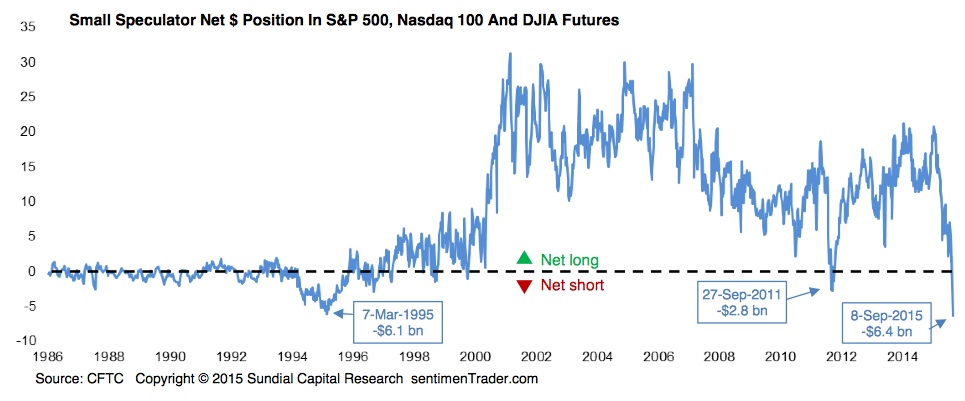

With stocks a bit weaker and crude oil trading lower, today King World News is featuring a stunning piece that reveals small speculators are now gambling on a stock market decline by taking an all-time record short position in stocks. This piece also includes two key illustrations that all KWN readers around the world must see.

With stocks a bit weaker and crude oil trading lower, today King World News is featuring a stunning piece that reveals small speculators are now gambling on a stock market decline by taking an all-time record short position in stocks. This piece also includes two key illustrations that all KWN readers around the world must see.

Jason Goepfert of SentimenTrader warned: “Small speculators in index futures went to $6 billion short this week. New all-time extreme – see charts HERE

There is a growing sense across the financial spectrum that the world is about to turn some type of economic page. Unfortunately no one in the mainstream is too sure what the last chapter was about, and fewer still have any clue as to what the next chapter will bring. There is some agreement however, that the age of ever easing monetary policy in the U.S. will be ending at the same time that the Chinese economy (that had powered the commodity and emerging market booms) will be finally running out of gas. While I believe this theory gets both scenarios wrong (the Fed will not be tightening and China will not be falling off the economic map), there is a growing concern that the new chapter will introduce a new character into the economic drama. As introduced by researchers at Deutsche Bank, meet “Quantitative Tightening,” the pesky, problematic, and much less disciplined kid brother of “Quantitative Easing.” Now that QE is ready to move out…QT is prepared to take over.

There is a growing sense across the financial spectrum that the world is about to turn some type of economic page. Unfortunately no one in the mainstream is too sure what the last chapter was about, and fewer still have any clue as to what the next chapter will bring. There is some agreement however, that the age of ever easing monetary policy in the U.S. will be ending at the same time that the Chinese economy (that had powered the commodity and emerging market booms) will be finally running out of gas. While I believe this theory gets both scenarios wrong (the Fed will not be tightening and China will not be falling off the economic map), there is a growing concern that the new chapter will introduce a new character into the economic drama. As introduced by researchers at Deutsche Bank, meet “Quantitative Tightening,” the pesky, problematic, and much less disciplined kid brother of “Quantitative Easing.” Now that QE is ready to move out…QT is prepared to take over.

For much of the past generation foreign central banks, led by China, have accumulated vast quantities of foreign reserves. In August of last year the amount topped out at more than $12 trillion, an increase of five times over levels seen just 10 years earlier. During that time central banks added on average $824 billion in reserves per year. The vast majority of these reserves have been accumulated by China, Japan, Saudi Arabia, and the emerging market economies in Asia (Shrinking Currency Reserves Threaten Emerging Asia, BloombergBusiness, 4/6/15). It is widely accepted, although hard to quantify, that approximately two-thirds of these reserves are held in U.S. dollar denominated instruments (COFER, Washington DC: Intl. Monetary Fund, 1/3/13), the most common being U.S. Treasury debt.

Initially this “Great Accumulation” (as it became known) was undertaken as a means to protect emerging economies from the types of shocks that they experienced during the 1997-98 Asian Currency Crisis, in which emerging market central banks lacked the ammunition to support their free falling currencies through market intervention. It was hoped that large stockpiles of reserves would allow these banks to buy sufficient amounts of their own currencies on the open market, thereby stemming any steep falls. The accumulation was also used as a primary means for EM central banks to manage their exchange rates and prevent unwanted appreciation against the dollar while the Greenback was being depreciated through the Federal Reserve’s QE and zero interest rate policies.

The steady accumulation of Treasury debt provided tremendous benefits to the U.S. Treasury, which had needed to issue trillions of dollars in debt as a result of exploding government deficits that occurred in the years following the Financial Crisis of 2008. Without this buying, which kept active bids under U.S. Treasuries, long-term interest rates in the U.S. could have been much higher, which would have made the road to recovery much steeper. In addition, absent the accumulation, the declines in the dollar in 2009 and 2010 could have been much more severe, which would have put significant upward pressure on U.S. consumer prices.

But in 2015 the tide started to slowly ebb. By March of 2015 global reserves had declined by about $400 billion in just about 8 months, according to data compiled by Bloomberg. Analysts at Citi estimate that global FX reserves have been depleted at an average pace of $59 billion a month in the past year or so, and closer to $100 billion per month over the last few months (Brace for QT…as China leads FX reserves purge, Reuters, 8/28/15). Some think that these declines stem largely by actions of emerging economies whose currencies have been falling rapidly against the U.S. dollar that had been lifted by the belief that a tightening cycle by the Fed was a near term inevitability.

It was speculated that China led the reversal, dumping more than $140 billion in Treasuries in just three months (through front transactions made through a Belgian intermediary – solving the so-called “Belgian Mystery”) (China Dumps Record $143 Billion in US Treasurys in Three Months via Belgium, Zero Hedge, 7/17/15). The steep decline in the Chinese stock market has also sparked a flight of assets out of the Chinese economy. China has used FX sales as a means to stabilize its currency in the wake of this capital flight.

The steep fall in the price of oil in late 2014 and 2015 also has led to diminished appetite for Treasuries by oil producing nations like Saudi Arabia, which no longer needed to recycle excess profits into dollars to prevent their currencies from rising on the back of strong oil. The same holds true for nations like Russia, Brazil, Norway and Australia, whose currencies had previously benefited from the rising prices of commodities.

Analysts at Deutsche Bank see this liquidation trend holding for quite some time. However, new categories of buyers to replace these central bank sellers are unlikely to emerge. This changing dynamic between buyers and sellers will tend to lower bond prices, and increase bond yields (which move in the opposite direction as price). Citi estimates that every $500 billion in Emerging Markets FX drawdowns will result in 108 basis points of upward pressure placed on the yields of 10-year U.S. Treasurys (It’s Official: China Confirms It Has Begun Liquidating Treasuries, Warns Washington, Zero Hedge, 8/27/15). This means that if just China were to dump its $1.1 trillion in Treasury holdings, U.S. interest rates would be about 2% higher. Such an increase in rates would present the U.S. economy and U.S. Treasury with the most daunting headwinds that they have seen in years.

The Federal Reserve sets overnight interest rates through its much-watched Fed Funds rate (that has been kept at zero since 2008). But to control rates on the “long end of the curve’ requires the Fed to purchase long-dated debt on the open market, a process known as Quantitative Easing. The buying helps push up bond prices and push down yields. It follows then that a process of large scale selling, by foreign central banks, or other large holders of bonds, should be known as Quantitative Tightening.

Potentially making matters much worse, Janet Yellen has indicated the Fed’s desire to allow its current hoard of Treasurys to mature without rolling them over. The intention is to shrink the Fed’s $4.5 trillion dollar balance sheet back to its pre-crisis level of about $1 trillion. That means, in addition to finding buyers for all those Treasurys being dumped on the market by foreign central banks, the Treasury may also have to find buyers for $3.5 trillion in Treasurys that the Fed intends on not rolling over. The Fed has stated that it hopes to effectuate the drawdown by the end of the decade, which translates into about $700 billion in bonds per year. That’s just under $60 billion per month (or slightly smaller than the $85 billion per month that the Fed had been buying through QE). Given the enormity of central bank selling, and the incredibly low yields offered on U.S. Treasurys, I cannot imagine any private investor willing to step in front of that freight train.

So even as the Fed apparently is preparing to raise rates on the short end of the curve, forces beyond its control will be pushing rates up on the long end of the curve. This will seriously undermine the health of the U.S. economy even while many signs already point to near recession level weakness. Just this week, data was released that showed U.S. factory orders decreasing 14.7% year-over-year, which is the ninth month in a row that orders have declined year-over-year. Historically, this type of result has only occurred either during a recession, or in the lead up to a recession.

The August jobs report issued today, which was supposed to be the most important such report in years, as it would be the final indication as to whether the Fed would finally move in September, provided no relief for the Fed’s quandaries. While the headline rate fell to a near generational low of 5.1%, the actual hiring figures came in at just 173,000 jobs, which was well below even the low end of the consensus forecast. Private sector hiring led the weakness, manufacturing jobs declined, and the labor participation rate remained at the lowest level since 1976. So even while the Fed is indicating that it is still on track for a rate hike, all the conditions that Janet Yellen wanted to see confirmed before an increase are not materializing. This is a recipe for more uncertainty, even while certainty increases overseas that U.S. Treasurys are troubled long term investments.

The arrival of Quantitative Tightening will provide years’ worth of monetary headwinds. Of course the only tool that the Fed will be able to use to combat international QT will be a fresh dose of domestic QE. That means the Fed will not only have to shelve its plan to allow its balance sheet to run down (a plan I never thought remotely feasible from the moment it was announced), but to launch QE4, and watch its balance sheet swell towards $10 trillion. Of course, these monetary crosscurrents should finally be enough to capsize the U.S. dollar.

###

|

Click here to buy Peter Schiff’s best-selling, latest book, “How an Economy Grows and Why It Crashes.” For a more in depth analysis of our financial problems and the inherent dangers they pose for the US economy and US dollar, you need to read Peter Schiff’s 2008 bestseller “The Little Book of Bull Moves in Bear Markets” [buy here] And “Crash Proof 2.0: How to Profit from the Economic Collapse” [buy here] |

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair