Market Opinion

April ushered in both broader evidence of recovery in parts of the Western

economy, and a series of both ecological and economic “events” that are

quite worrisome. It’s unlikely any of the April events (including, we fervently

hope, sovereign debt) would be, in and of itself, shattering. What each does

is to impact the psychology under which markets are operating and hence

how they perform. The cumulative impact of these events after a strong

uptick means sell buttons are being pushed, and should be signaling profits

taking by you. How much is the question.

The notion of an event impacting markets hard isn’t news. In the last decade

both the 9-11 destruction of New York’s twin towers and the flooding of New

Orleans by Hurricane Katrina made the list. The Black Swan by Nassim Taleb

that became popular after the Credit Crunch meltdown emphasized the

concept. We would emphasis, however, that a 9-11, Katrina and the Credit

Crunch are different birds.

The 9-11 attacks were a calculated attempt to disrupt western commerce.

They worked because, like any high impact terrorist act, they were a

surprise. The timing deepened a recession that was ready to get underway

and broadened the bear market the Tech bubble ushered in. They have cost

$trillions in added security cost and 10s of thousands of lives to war in a

broad protracted aftermath. 9-11 earned the Black Swan Event moniker.

Katrina was an event to be expected though also impossible to time. Most of

the region picked up and carried on as it had after similar weather borne

destruction. Human suffering was largely immediate. The impact to New

Orleans was exceptional. It hasn’t really recovered from its failed levee

system after five years. One immediate impact was to underscore resource

scarcity for oil, plus zinc and other metals for which the city acts a

warehousing/transport hub. That helped set up crazy oil prices, but the event

had little broader impact The Credit Crunch was/is an event that fit

perfectly into the financial model Taleb uses in his (now) popular short fund.

That would seem to make the Crunch an obvious Black Swan Event. It was,

however, another difficult-to-time event like Katrina rather than a true

surprise like 9-11. Many could see the bubbles forming and warned about

them. The timing of the Crunch will be a marker for the economic turning

point from western to eastern centers. Right now it feels like that marker is

being called.

Since it got underway over two and a half years ago, the credit crunch seems

less like a black swan and more like a slow motion train wreck. That is especially true of late. The crisis gripping parts of Europe has been brewing

for months. Like drivers who realize too late they won’t make a corner,

markets are reacting to seemingly implacable forces they can’t seem to

avoid.

There are several worries that relate specifically to the metals sector.

China’s moves to slow the pace of growth appear to be working. That’s good

in the long run if it allows China to avoid its own bubble. The obvious

downside is this could mean a near term slackening of demand that is

showing up in metal prices.

The second is the Australian government’s plan to boost taxes on the “excess

profits” of mining firms. To the obvious impact on companies working in Oz

is added the realization that other jurisdictions could make similar moves.

This is a topic we have touched on in the past and is certainly no black swan

for us.

Its no secret to resource sector participants that others think deposits

magically appear without thought or effort on the part of mining companies.

Many governments see resource extraction as some sort of “free lunch”.

When the sector has periods of high profits they must, by definition, be

“excessive” and fair game for revenue hungry governments.

Obviously this raises the bar that determines what is economically viable by

increasing the average cost base for commodities. Part of the reason cheap

oil is over is a revenue sharing structure that sets a high base price for

anything coming out of the well. Following a similar model in the mining

business will simply help ensure metal prices stay high.

The big worries right now of course are European. Most of these have been

visible for a while but had been “normalized” through the last year of market

recovery. Most of the EU did not deal with anything but emergency debt

issues and let longer term problems fester in denial. However, they have

built one on top of an another until its impossible to ignore the pile’s

abnormality.

To wit:

The sovereign debt of Greece has been labeled junk and is now yielding at

the same level charged by mass mailing credit cards. Portugal’s debt rating

is now slipping away, and Spain is looking increasingly shaky. The €110

billion bail out for Greece with EU/IMF funding is large. Yet Greek workers

are tossing rocks in protest. What they would toss if Germany’s parliament

refuses to ratify its portion we don’t know.

Frustration is understandable, but the reaction of the Greek populace borders

on delusional. The nastier the backlash, the less likely it is that bond buyers

will believe Greece is willing to take the necessary steps. Without some faith

in the bond pits, interest rates in Greece will stay at levels that all but guarantee a debt spiral even with a bailout in place.

Many Club Med citizens are remembering the “good old days” when they

could devalue their way out of spending crises and print the money to pay

back old debts. If reason doesn’t prevail, the core countries in the EU may

have to cover some bank debts directly and give rioters their wish by cutting

them out of the EMU. Definitely one of those “be careful what you wish for”

scenarios that we really hope does not come to pass.

An Icelandic volcano shut down most European air traffic for five days and is

increasing its activity again as this is written. This volcano can spew for

months at time, and has often signaled its bigger neighbor is about to

awaken. The disruptions to air traffic going forward aren’t likely to be as

severe, but it will make travel planning tougher and more expensive to deal

with. Just another headache for Euroland.

A South Korean warship mysteriously sinks, and evidence increasingly points

to a North Korean torpedo as the cause. Since North Korea is mum on the

subject, the best case would seem to be that a lower ranking nutcase was

responsible rather than the “Dear Leader”.

A presumably lone nutcase who fortunately had limited skills plants a bomb

in Times Square. It didn’t explode and is not likely to damage the city’s

image. One wonders if it was actually heading for Wall St and just happened

to begin sputtering in mid Main St. We take a little comfort from that thought

since we’ll be speaking at a conference across the street next week.

A BP oil well in the Gulf of Mexico blows out and is seriously leaking. So far,

damage to the Gulf seems to be relatively limited, but few immediate

solutions are at hand. The impact on further such oil production will at a

minimum be higher capital costs to ensure problems of this sort can be dealt

with more quickly. Washington only recently opened up a number of offshore

areas to new drilling. An ill wind blowing the wrong way could ensure these

areas get closed again.

A writ has been filed against Goldman Sachs and a young VP. It alleges that

a synthetic CDO was filled by the worst possible mortgage crap with the aid

of a client who intended to short it. Regardless of whether this is judged

illegal or not, the ethics at work is going to cause further questioning of how

financial markets function. Goldman is the big dog on Wall St. Most of its

clients didn’t seem too concerned about its proprietary trading as long as the

gains were there. This case could give a lot of those clients second thoughts.

Reformers will now have a freer hand to do their work and those voting

against financial reform bills will have to explain why, even if the bills are

silly. Whether new legislation will actually help is another question.

Most events like those above can be dealt with individually without terribly

serious market disruptions. The potential of sovereign default will always shake things up since banking gets hurt which can lead to severe domino

effects. Greece’s debt is large enough to matter internationally, but only

just. It’s concern for southern Europe as a whole that is the real issue in this

case. The ability of a country to escape a debt spiral is directly correlated to

the interest rate the market demands for its debt. Even if the PIIGS enforce

credible spending cuts they can still be trapped in a spiral if lending costs

don’t settle down. There is no way we know of to legislate this since its

basically about trust.

Financial cotangents are mostly about lost confidence. Despite large gains

for some assets since the Crunch, confidence hadn’t really returned at large

enough scale to deal with a pile this size right now. Most of the European

banking sector has made much less serious efforts to write off and

recapitalize than banks in the US. That may now be forced on them. If

recent bond yields and share prices for southern European banks are any

guide, the equity injections will be public again rather than private.

Markets reflect the common consciousness. That isn’t a philosophical

musing, but merely a fact. If this pile gets any larger markets will continue

to retreat. We try to regularly remind that profits taking should be an on

going part of dealing with what are generally high risk stories. Hopefully you

have taken note.

The $6 Billion?

Now that base metal prices are in decline, the next question is more obvious.

How much is enough? The continuing puzzle of what size of copper inventory

markets can handle comes down to that. LME stockpiles have dropped by

well over 15% since late February, as have the much smaller Comex stocks.

In Shanghai the copper stockpiles have grown by almost 30 Kt in the past

month, which offsets about half the LME declines. All of the SHFE metal

stocks are growing right now, and stockpiles of other mineral goods are flat

lining. Shanghai’s stocks continue to auger the global price picture.

The decline in western stocks may indicate a reluctance to sell metal when it

appears western economies are mending. Added availability in China could

relate to fresh indications the Yuan is finally going to be allowed to rise as

much as it is efforts to slow growth starting to take root. For now, holding

Yuan is a Dollar hedge if it is going to rise.

Regardless, copper’s price has become unstuck from its $3.50 per pound

($7700 per tonne) waypoint. Both prices and stockpiles are in decline, as we

had expected would happen at some point. It’s too soon to call this a trend

since the last 50 cents or so of gain looked like froth that needed blowing off.

We do think the “new-normal” can now establish itself.

The listed copper stockpiles are currently valued at about US $5.5 billion,

down from about $6.2 billion a week ago. A decade ago when stockpiles held about 50% more metal than today they were valued well below $2 billion

(about 65 cents per pound) in the midst of a bear market. That is the

seeming disconnect we have been concerned about. But then, these days a

billion here or there is chump change.

The copper stockpiles are valued at about seven or eight days of trading in

Freeport McMoran. It’s not unusual to hedge producer shares by going into

futures market for the metal. Futures pricing on the LME for copper rises,

slightly, out to the 15 month slot. That on its own could be holding the spot

price up.

It’s also true that smelters are having a tough time contracting as much

concentrate as they’d like. As we’ve noted before the overbuilding of

smelters in China has caused an upstream capacity glut, and smelters have

cut charges to the bone to ensure they can maintain supply. Asian smelters

often supply other units in the same conglomerate. That makes the issue of

supply maintenance a critical concern that could also bring more long buyers

to the futures market.

None of this means the copper price is going to move back up. If sentiment

shifts towards a short circuiting of the western recovery, or the Asian boom,

copper would continue to pull back with everything else.

Copper producers are trading at levels established before copper’s last up

leg. Either the possibility of a broader down turn had still been weighing on

them, or market ratios are changing. Though we think the former is most

likely, this is the wrong time to be concerned on which is the more

important. For the time being we continue to be more focused on warehouse

changes than on price for all the base metals. That and Mediterranean bond

prices.

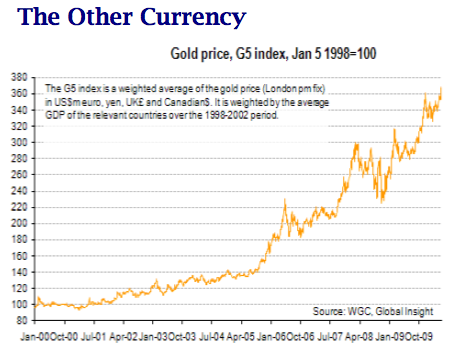

The chart on this page shows the gold price over the last decade measured against a basket of five currencies (the Canadian and US Dollars, UK Pounds, Euros and Yen. It’s a good indication of how strong the recent move has been when you stop thinking in dollars.

Gold has not seen new all time highs in $CAD or $US and yet the chart above

shows a clear upward breakout. The chart for Euros or pounds is much more

impressive and gold has been moving up against all currencies.

All of this is another way of saying gold is trading like a currency which

means its trading on its own against all currencies. There have been a

number of recent sessions where gold had strong upward moves in the face

of falling stock markets and a surging dollar. This is quite different from the

pattern two years ago when gold was falling 30% as markets panicked and

the Dollar surged. Currency trades never happen isolation; you are always

selling one currency to buy another. In the past month we think much of the

new money entering the gold market is coming out of the Euro which has

been crashing hard.

This is different from straight “fear buying” and has the potential to be more

long lasting and fundamental in its aspect. Those that have expected gold to

falter whenever the markets showed some strength lately have been

disappointed.

Gold’s trading pattern has changed several times in the past few years and it

can certainly change again. Nonetheless, the market now seems set up for a

challenge of last year’s all time high which bodes well for gold stocks.

Ω

To view Eric Coffin’s latest video interview on Industry Watch with Al Korelin, please go HERE [April 12, 2010]

Gain access to potential gains of hundreds or even thousands of percent! HRA initiated

coverage on 8 new companies in 2009. So far, the average gain on those companies is

over 250%! For more information about HRA Advisories, please visit:

www.hraadvisories.com

Rumors of the imminent collapse of the eurozone continue to swirl despite the Europeans’ best efforts to hold the currency union together…..

Germany, Greece and Exiting the Eurozone

by Marko Papic, Robert Reinfrank and Peter Zeihan

Rumors of the imminent collapse of the eurozone continue to swirl despite the Europeans’ best efforts to hold the currency union together. Some accounts in the financial world have even suggested that Germany’s frustration with the crisis could cause Berlin to quit the eurozone – as soon as this past weekend, according to some – while at the most recent gathering of European leaders French President Nicolas Sarkozy apparently threatened to bolt the bloc if Berlin did not help Greece. Meanwhile, many in Germany – including Chancellor Angela Merkel herself at one point – have called for the creation of a mechanism by which Greece – or the eurozone’s other over-indebted, uncompetitive economies – could be kicked out of the eurozone in the future should they not mend their “irresponsible” spending habits.

Rumors, hints, threats, suggestions and information “from well-placed sources” all seem to point to the hot topic in Europe at the moment, namely, the reconstitution of the eurozone whether by a German exit or a Greek expulsion. We turn to this topic with the question of whether such an option even exists.

The Geography of the European Monetary Union

As we consider the future of the euro, it is important to remember that the economic underpinnings of paper money are not nearly as important as the political underpinnings. Paper currencies in use throughout the world today hold no value without the underlying political decision to make them the legal tender of commercial activity. This means a government must be willing and capable enough to enforce the currency as a legal form of debt settlement, and refusal to accept paper currency is, within limitations, punishable by law.

The trouble with the euro is that it attempts to overlay a monetary dynamic on a geography that does not necessarily lend itself to a single economic or political “space.” The eurozone has a single central bank, the European Central Bank (ECB), and therefore has only one monetary policy, regardless of whether one is located in Northern or Southern Europe. Herein lies the fundamental geographic problem of the euro.

Europe is the second-smallest continent on the planet but has the second-largest number of states packed into its territory. This is not a coincidence. Europe’s multitude of peninsulas, large islands and mountain chains create the geographic conditions that often allow even the weakest political authority to persist. Thus, the Montenegrins have held out against the Ottomans, just as the Irish have against the English.

Despite this patchwork of political authorities, the Continent’s plentiful navigable rivers, large bays and serrated coastlines enable the easy movement of goods and ideas across Europe. This encourages the accumulation of capital due to the low costs of transport while simultaneously encouraging the rapid spread of technological advances, which has allowed the various European states to become astonishingly rich: Five of the top 10 world economies hail from the Continent despite their relatively small populations.

Europe’s network of rivers and seas are not integrated via a single dominant river or sea network, however, meaning capital generation occurs in small, sequestered economic centers. To this day, and despite significant political and economic integration, there is no European New York. In Europe’s case, the Danube has Vienna, the Po has Milan, the Baltic Sea has Stockholm, the Rhineland has both Amsterdam and Frankfurt and the Thames has London. This system of multiple capital centers is then overlaid on Europe’s states, which jealously guard control over their capital and, by extension, their banking systems.

Despite a multitude of different centers of economic – and by extension, political – power, some states, due to geography, are unable to access any capital centers of their own. Much of the Club Med states are geographically disadvantaged. Aside from the Po Valley of northern Italy – and to an extent the Rhone – southern Europe lacks a single river useful for commerce. Consequently, Northern Europe is more urban, industrial and technocratic while Southern Europe tends to be more rural, agricultural and capital-poor.

Introducing the Euro

Given the barrage of economic volatility and challenges the eurozone has confronted in recent quarters and the challenges presented by housing such divergent geography and history under one monetary roof, it is easy to forget why the eurozone was originally formed.

The Cold War made the European Union possible. For centuries, Europe was home to feuding empires and states. After World War II, it became the home of devastated peoples whose security was the responsibility of the United States. Through the Bretton Woods agreement, the United States crafted an economic grouping that regenerated Western Europe’s economic fortunes under a security rubric that Washington firmly controlled. Freed of security competition, the Europeans not only were free to pursue economic growth, they also enjoyed nearly unlimited access to the American market to fuel that growth. Economic integration within Europe to maximize these opportunities made perfect sense. The United States encouraged the economic and political integration because it gave a political underpinning to a security alliance it imposed on Europe, i.e., NATO. Thus, the European Economic Community – the predecessor to today’s European Union – was born.

When the United States abandoned the gold standard in 1971 (for reasons largely unconnected to things European), Washington essentially abrogated the Bretton Woods currency pegs that went with it. One result was a European panic. Floating currencies raised the inevitability of currency competition among the European states, the exact sort of competition that contributed to the Great Depression 40 years earlier. Almost immediately, the need to limit that competition sharpened, first with currency coordination efforts still concentrating on the U.S. dollar and then from 1979 on with efforts focused on the deutschmark. The specter of a unified Germany in 1989 further invigorated economic integration. The euro was in large part an attempt to give Berlin the necessary incentives so that it would not depart the EU project.

But to get Berlin on board with the idea of sharing its currency with the rest of Europe, the eurozone was modeled after the Bundesbank and its deutschmark. To join the eurozone, a country must abide by rigorous “convergence criteria” designed to synchronize the economy of the acceding country with Germany’s economy. The criteria include a budget deficit of less than 3 percent of gross domestic product (GDP); government debt levels of less than 60 percent of GDP; annual inflation no higher than 1.5 percentage points above the average of the lowest three members’ annual inflation; and a two-year trial period during which the acceding country’s national currency must float within a plus-or-minus 15 percent currency band against the euro.

As cracks have begun to show in both the political and economic support for the eurozone, however, it is clear that the convergence criteria failed to overcome divergent geography and history. Greece’s violations of the Growth and Stability Pact are clearly the most egregious, but essentially all eurozone members – including France and Germany, which helped draft the rules – have contravened the rules from the very beginning.

Mechanics of a Euro Exit

The EU treaties as presently constituted contractually obligate every EU member state – except Denmark and the United Kingdom, which negotiated opt-outs – to become a eurozone member state at some point. Forcible expulsion or self-imposed exit is technically illegal, or at best would require the approval of all 27 member states (never mind the question about why a troubled eurozone member would approve its own expulsion). Even if it could be managed, surely there are current and soon-to-be eurozone members that would be wary of establishing such a precedent, especially when their fiscal situation could soon be similar to Athens’ situation.

One creative option making the rounds would allow the European Union to technically expel members without breaking the treaties. It would involve setting up a new European Union without the offending state (say, Greece) and establishing within the new institutions a new eurozone as well. Such manipulations would not necessarily destroy the existing European Union; its major members would “simply” recreate the institutions without the member they do not much care for.

Though creative, the proposed solution it is still rife with problems. In such a reduced eurozone, Germany would hold undisputed power, something the rest of Europe might not exactly embrace. If France and the Benelux countries reconstituted the eurozone with Berlin, Germany’s economy would go from constituting 26.8 percent of eurozone version 1.0’s overall output to 45.6 percent of eurozone version 2.0’s overall output. Even states that would be expressly excluded would be able to get in a devastating parting shot: The southern European economies could simply default on any debt held by entities within the countries of the new eurozone.

With these political issues and complications in mind, we turn to the two scenarios of eurozone reconstitution that have garnered the most attention in the media.

Scenario 1: Germany Reinstitutes the Deutschmark

The option of leaving the eurozone for Germany boils down to the potential liabilities that Berlin would be on the hook for if Portugal, Spain, Italy and Ireland followed Greece down the default path. As Germany prepares itself to vote on its 123 billion euro contribution to the 750 billion euro financial aid mechanism for the eurozone – which sits on top of the 23 billion euros it already approved for Athens alone – the question of whether “it is all worth it” must be on top of every German policymaker’s mind.

This is especially the case as political opposition to the bailout mounts among German voters and Merkel’s coalition partners and political allies. In the latest polls, 47 percent of Germans favor adopting the deutschmark. Furthermore, Merkel’s governing coalition lost a crucial state-level election May 9 in a sign of mounting dissatisfaction with her Christian Democratic Union and its coalition ally, the Free Democratic Party. Even though the governing coalition managed to push through the Greek bailout, there are now serious doubts that Merkel will be able to do the same with the eurozone-wide mechanism May 21.

Germany would therefore not be leaving the eurozone to save its economy or extricate itself from its own debts, but rather to avoid the financial burden of supporting the Club Med economies and their ability to service their 3 trillion euro mountain of debt. At some point, Germany may decide to cut its losses – potentially as much as 500 billion euros, which is the approximate exposure of German banks to Club Med debt – and decide that further bailouts are just throwing money into a bottomless pit. Furthermore, while Germany could always simply rely on the ECB to break all of its rules and begin the policy of purchasing the debt of troubled eurozone governments with newly created money (“quantitative easing”), that in itself would also constitute a bailout. The rest of the eurozone, including Germany, would be paying for it through the weakening of the euro.

Were this moment to dawn on Germany it would have to mean that the situation had deteriorated significantly. As STRATFOR has recently argued, the eurozone provides Germany with considerable economic benefits. Its neighbors are unable to undercut German exports with currency depreciation, and German exports have in turn gained in terms of overall eurozone exports on both the global and eurozone markets. Since euro adoption, unit labor costs in Club Med have increased relative to Germany’s by approximately 25 percent, further entrenching Germany’s competitive edge.

Before Germany could again use the deutschmark, Germany would first have to reinstate its central bank (the Bundesbank), withdraw its reserves from the ECB, print its own currency and then re-denominate the country’s assets and liabilities in deutschmarks. While it would not necessarily be a smooth or easy process, Germany could reintroduce its national currency with far more ease than other eurozone members could.

The deutschmark had a well-established reputation for being a store of value, as the renowned Bundesbank directed Germany’s monetary policy. If Germany were to reintroduce its national currency, it is highly unlikely that Europeans would believe that Germany had forgotten how to run a central bank – Germany’s institutional memory would return quickly, re-establishing the credibility of both the Bundesbank and, by extension, the deutschmark.

As Germany would be replacing a weaker and weakening currency with a stronger and more stable one, if market participants did not simply welcome the exchange, they would be substantially less resistant to the change than what could be expected in other eurozone countries. Germany would therefore not necessarily have to resort to militant crackdowns on capital flows to halt capital trying to escape conversion.

Germany would probably also be able to re-denominate all its debts in the deutschmark via bond swaps. Market participants would accept this exchange because they would probably have far more faith in a deutschmark backed by Germany than in a euro backed by the remaining eurozone member states.

Reinstituting the deutschmark would still be an imperfect process, however, and there would likely be some collateral damage, particularly to Germany’s financial sector. German banks own much of the debt issued by Club Med, which would likely default on repayment in the event Germany parted with the euro. If it reached the point that Germany was going to break with the eurozone, those losses would likely pale in comparison to the costs – be they economic or political – of remaining within the eurozone and financially supporting its continued existence.

Scenario 2: Greece Leaves the Euro

If Athens were able to control its monetary policy, it would ostensibly be able to “solve” the two major problems currently plaguing the Greek economy.

First, Athens could ease its financing problems substantially. The Greek central bank could print money and purchase government debt, bypassing the credit markets. Second, reintroducing its currency would allow Athens to then devalue it, which would stimulate external demand for Greek exports and spur economic growth. This would obviate the need to undergo painful “internal devaluation” via austerity measures that the Greeks have been forced to impose as a condition for their bailout by the International Monetary Fund (IMF) and the EU.

If Athens were to reinstitute its national currency with the goal of being able to control monetary policy, however, the government would first have to get its national currency circulating (a necessary condition for devaluation).

The first practical problem is that no one is going to want this new currency, principally because it would be clear that the government would only be reintroducing it to devalue it. Unlike during the Eurozone accession process – where participation was motivated by the actual and perceived benefits of adopting a strong/stable currency and receiving lower interest rates, new funds and the ability to transact in many more places – “de-euroizing” offers no such incentives for market participants:

- The drachma would not be a store of value, given that the objective in reintroducing it is to reduce its value.

- The drachma would likely only be accepted within Greece, and even there it would not be accepted everywhere – a condition likely to persist for some time.

- Reinstituting the drachma unilaterally would likely see Greece cast out of the eurozone, and therefore also the European Union as per rules explained above.

The government would essentially be asking investors and its own population to sign a social contract that the government clearly intends to abrogate in the future, if not immediately once it is able to. Therefore, the only way to get the currency circulating would be by force.

The goal would not be to convert every euro-denominated asset into drachmas but rather to get a sufficiently large chunk of the assets so that the government could jumpstart the drachma’s circulation. To be done effectively, the government would want to minimize the amount of money that could escape conversion by either being withdrawn or transferred into asset classes easy to conceal from discovery and appropriation. This would require capital controls and shutting down banks and likely also physical force to prevent even more chaos on the streets of Athens than seen at present. Once the money was locked down, the government would then forcibly convert banks’ holdings by literally replacing banks’ holdings with a similar amount in the national currency. Greeks could then only withdraw their funds in newly issued drachmas that the government gave the banks to service those requests. At the same time, all government spending/payments would be made in the national currency, boosting circulation. The government also would have to show willingness to prosecute anyone using euros on the black market, lest the newly instituted drachma become completely worthless.

Since nobody save the government would want to do this, at the first hint that the government would be moving in this direction, the first thing the Greeks will want to do is withdraw all funds from any institution where their wealth would be at risk. Similarly, the first thing that investors would do – and remember that Greece is as capital-poor as Germany is capital-rich – is cut all exposure. This would require that the forcible conversion be coordinated and definitive, and most important, it would need to be as unexpected as possible.

Realistically, the only way to make this transition without completely unhinging the Greek economy and shredding Greece’s social fabric would be to coordinate with organizations that could provide assistance and oversight. If the IMF, ECB or eurozone member states were to coordinate the transition period and perhaps provide some backing for the national currency’s value during that transition period, the chances of a less-than-completely-disruptive transition would increase.

It is difficult to imagine circumstances under which such support would not dwarf the 110 billion euro bailout already on the table. For if Europe’s populations are so resistant to the Greek bailout now, what would they think about their governments assuming even more risk by propping up a former eurozone country’s entire financial system so that the country could escape its debt responsibilities to the rest of the eurozone?

The European Dilemma

Europe therefore finds itself being tied in a Gordian knot. On one hand, the Continent’s geography presents a number of incongruities that cannot be overcome without a Herculean (and politically unpalatable) effort on the part of Southern Europe and (equally unpopular) accommodation on the part of Northern Europe. On the other hand, the cost of exit from the eurozone – particularly at a time of global financial calamity, when the move would be in danger of precipitating an even greater crisis – is daunting to say the least.

The resulting conundrum is one in which reconstitution of the eurozone may make sense at some point down the line. But the interlinked web of economic, political, legal and institutional relationships makes this nearly impossible. The cost of exit is prohibitively high, regardless of whether it makes sense.

John F. Mauldin

johnmauldin@investorsinsight.com

1 in every 10 American homeowners missed a mortgage payment in Q1 (a record)

1 in 6 Americans are either unemployed or underemployed Over 4 in 10 unemployed Americans have been out of work for at least six months.

1 in 4 Americans with a mortgage have negative equity in their homes.

1 in 10 Americans believe their income will rise in the next six months.

1 in 5 Americans see business conditions improving in the next six months.

1 in 50 Americans plan to buy a home in the next six months.

1 in 8 Americans believe that current government policy is actually helping the economy.

1 in 10 American small businesses have a job opening.

1 in 10 American’s credit card usage is being written off (a record).

There are 5 unemployed workers competing for every job opening (hence

downward pressure on wage growth).

Outside of these, it’s all good. Lagged impact of gargantuan fiscal stimulus (the longevity of which is now being challenged with Greece the proverbial canary in the coal mine) and inventory-led production gains (the longevity of which is now being challenged by the fact that real final sales since the recession technically ended is running at a pace that is two-thirds weaker than what is “normal” coming out of a “downturn”).

In today’s issue of Breakfast with Dave

Full Report HERE – Summary HERE

• While you were sleeping: European bourses are in the red, and so are Asian equity markets; bonds are on an even keel

• Credit crunch in Europe: The NYT runs with a story on how credit growth is drying up in the Euro area just as it started to in the United States two years ago

• Walmart and the consumer: CFO Thomas Schoewe on the tapes saying “more than ever our customers are living paycheck to paycheck.”

• Investor sentiment still positive … and that’s a negative!

• Shiller P/E ratio pointing to a big correction in the U.S. equity market

• Deflation is evident in the labour market … just ask any graduate

• The U.S. Federal Reserve not even thinking about raising rates until 2012

• More troubling housing data out of the U.S.: mortgage delinquencies continue to rise

Please check out our website at:

http://www.raymondjames.ca/jamieswitzer

If you would like to receive our “Weekly Wrap”, please click HERE to subscribe.

Market Summaries as of May 14th/2010

S&P/TSX Composite up 2.80% to 12015 (up 2.30% year-to-date)

S&P/TSX Venture Composite up 2.84% to 1593 (up 9.74% ytd)

Dow Jones Industrial Avg up 2.30% to 10620 (up 1.80% ytd)

Nasdaq Composite up 3.60% to 2347 (up 3.40% ytd)

Oil (West Texas Intermediate) down $3.50 to $71.61 (down $7.75 ytd)

Gold (Spot USD/oz) up $24.55 to $1232.95 (up $136.00 ytd)

Keep Playing Defense

Markets continue to be extremely volatile and last week’s series of swings is probably indicative of how the spring and possible summer will treat investors. Making forecasts beyond the next few weeks seems foolish based on the ever-changing landscape we are facing.

With Greece looking like it could act as the lynch-pin for many more European-based calamities, we are proceeding with caution and not rushing to “buy on the dips.” Gold continues to look strong in this uncertain environment and many utility and consumer staple stocks are weathering this recent round of selling remarkably well. On the “buy side” we have our eye on a few high-yielding utility names, while we may continue to sell broad-based equities as our “stops” continue to be breached to the downside. The addition of the iPath S&P 500 VIX Short Term Futures Index (VXX-US) a few weeks back has worked out very well in the short term but we would be sellers if this market gives any clear “rally” indicators. If this air of uncertainty remains, the VXX tool will provide investors with a great short-term trade opportunity if bought into index rallies.

With a steady diet of negative news, investors seem to be leaving commodities and rotating into more defensive options. Oil is down more than $14 USD a barrel over the past month and more than $10 in the past two weeks. This type of selling pressure is indicative of how the majority of the commodity sector is currently reacting.

In the short to medium term, stay focused on equities that are reacting well in this market volatility and try to avoid chasing the bottom on some of your favourite commodity names of the past year. It may be a while before they find traction again and the peace of mind of owning boring, high-yielding defensive names may be a comforting one.

Soundbites

- BC Hydro has turned to the sporting world to find the man who will lead them into the next decade. Highly regarded former Vancouver Canucks senior exec and deputy CEO of VANOC David Cobb has been named Hydro’s new president and CEO after a lengthy search. Former CEO Bob Elton was shuffled out after a rocky 6-year tenure which now sees the Crown corp taking a risk bringing on Cobb who has a stellar background, but no experience in the electricity sector. Cobb will get thrown into his role head-first, with numerous initiatives to tackle including an aggressive energy conservation target, implementation of the new Clean Energy Act, and overseeing the multi-billion-dollar Site C hydroelectric project – all lightning rods for criticism.

- Our country’s realtors, already under fire from Canada’s competition watchdog, are now facing a new obstacle that could ultimately lead to lower fees. iBidBroker.com has been launched in Toronto by 29-year old entrepreneur and former SmartCentres Inc employee Ajay Jain. The unveiling of the website comes at a time when the Competition Bureau is battling with the Canadian Real Estate Association (CREA) over access to the Multiple Listing Service (MLS) system, which controls about 90% of residential real estate transactions in Canada. Jain, who worked previously in land acquisitions at SmartCentres Inc, has invested $100,000 to $150,000 in his startup, claims his goal is not to lower commissions, but that may end up being the result. “The general concept is, if agents compete, the homeowner is going to win,” he said. Royal LePage CEO Phil Soper is quick to point out that similar websites are already established in the US. LePage recently released a survey that found 86% of its agents worry that deregulation in the industry would erode standards of service.

- In an age where silver-haired men of distinction seem to be running all facets of financial senior management, Britain has turned to 38-year old whiz kid George Osborne to manage what may be the country’s most precarious financial environment in decades. Combine that with the country’s first coalition government since 1945 and you have an intriguing scenario that will keep market-watchers glued to the headlines for a long time to come. Britain is trying to pull itself out of its worst recession since the Second World War, which sees unemployment at a 16-year high and a ballooning deficit that currently stands at 11% of GDP. At 38, Osborne is Britain’s youngest Chancellor the Exchequer (Finance Minister) in more than 100 years.

Marketwatch – A Look at the Week’s Newsmakers

Cardiome Pharmaceuticals Corp (COM) – shares climbed in soft markets after the Vancouver-based bio-tech posted solid Q1 earnings of $15.5 million USD (26 cents per share), compared with losses of $9.2 million just a year earlier. Revenues flew to $23 million (from only $200,000) in the quarter on the momentum of Cardiome’s licensing deal with Merck for its flagship drug, Vernakalant, which focuses on irregular heartbeats.

Crescent Point Energy Corp (CPG) – announced Wednesday it has agreed to pay $1.1 billion to buy the 79% of privately-held Shelter Bay Energy Inc it doesn’t already own. The move boosts its exposure in the prolific Bakken oil field and establishes it as one of the region’s dominant producers. The Shelter Bay operations are extremely familiar to Crescent Point, having created the company in 2008 to avoid federal government restrictions on the growth of trusts. The most recent US Geological Survey estimates Bakken could contain as many as 5.5 billion barrels of oil.

Seacliff Construction Corp (SDC) – shares shot higher in today’s miserable session after the construction company announced that rival Churchill Corp has agreed to pay $390 million, or $17.14 per share for the company. This was a significant jump for the stock, which closed at $14.55 on Friday and represents a 23% premium to the shares’ 20-day average price. The business combination is highly-accretive to Churchill and creates a formidable entity on the general contracting side as well as a strong oilsands player in many facets.

“Quote of the Day

“The things that will destroy America are prosperity-at-any-price, peace-at-any-price, safety-first instead of duty-first, the love of soft living, and the get-rich-quick theory of life” – Teddy Roosevelt.

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

MARC LATTA | Raymond James Ltd.

Senior Vice President, Financial Advisor

PH:604-981-3366 | FAX: 604.981.3376

marc.latta@raymondjames.ca

Suite 480, 171 West Esplanade

North Vancouver, British Columbia

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

From: Jamie Switzer [mailto:Jamie.SWITZER@raymondjames.ca]

Sent: Tuesday May 18, 2010 8:57:51 AM PDT

Subject: *** Portfolio Recommendation – Buy Duke Energy Corp

Action: Buy Duke Energy Corp (DUK-US)

Current Price: $17.00 USD

Dividend Yield: 5.62%

As we have mentioned numerous times of late, our focus in the short to medium term will be on defensive, high-yielding stocks that are “acting well” in the current environment. The opportunity to pick up a Citigroup in the US or Canadian bank will arise but we think the markets will continue to experience headwinds in the short term as this European crisis plays out. Talk of disbanding the Euro currency is the latest story making the rounds as some of the healthier nations search for ways to remove themselves from lesser-lights.

Duke Energy has performed remarkably well through a number of recent market conditions and has become the consummate “defensive play.” Duke provides electric and gas services to nearly 4 million homes throughout the US and prides itself on affordable, reliable, and clean products. It produces 35,000 megawatts of electric generating capacity in the Carolina’s and Midwest, and natural gas distribution services in Ohio and Kentucky. Duke has $57 billion USD in total assets, employs almost 19,000 people, and posted operating revenues of $12.7 billion in 2009.

Shares of Duke are attractive not only from a dividend and growth perspective, but also on valuation, with a forward looking p/e (price to earnings) ratio of only 13.25. We feel this is the ideal type of equity holding to add to our portfolios in this time of uncertainty and one that will “pay you while you wait” for a better investing environment.

Please contact us by phone to discuss this recommendation and how it fits with your overall investment strategy.

Marc & Jamie

WEEKLY WRAP: If you would like to receive our “Weekly Wrap”, please click HERE to subscribe.

Please check out our website at:

http://www.raymondjames.ca/jamieswitzer

This recommendation may not be suitable for all individuals. As each situation is different, please arrange to contact us to discuss and determine the suitability of this security to your own individual circumstances. This message is only to be read by the addressee and is not for public distribution. The sender is not responsible for distribution of this message beyond the addressee intended. All information in this message is confidential to the addressee and should be treated as such. Raymond James Ltd. is a member CIPF. This expresses the opinions of the authors, Marc Latta and Jamie Switzer, and not necessarily reflects those of Raymond James.

Please check out our website at:

http://www.raymondjames.ca/jamieswitzer

If you would like to receive our “Weekly Wrap”, please click HERE to subscribe.

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

MARC LATTA | Raymond James Ltd.

Senior Vice President, Financial Advisor

PH:604-981-3366 | FAX: 604.981.3376

marc.latta@raymondjames.ca

Suite 480, 171 West Esplanade

North Vancouver, British Columbia

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair