April ushered in both broader evidence of recovery in parts of the Western

economy, and a series of both ecological and economic “events” that are

quite worrisome. It’s unlikely any of the April events (including, we fervently

hope, sovereign debt) would be, in and of itself, shattering. What each does

is to impact the psychology under which markets are operating and hence

how they perform. The cumulative impact of these events after a strong

uptick means sell buttons are being pushed, and should be signaling profits

taking by you. How much is the question.

The notion of an event impacting markets hard isn’t news. In the last decade

both the 9-11 destruction of New York’s twin towers and the flooding of New

Orleans by Hurricane Katrina made the list. The Black Swan by Nassim Taleb

that became popular after the Credit Crunch meltdown emphasized the

concept. We would emphasis, however, that a 9-11, Katrina and the Credit

Crunch are different birds.

The 9-11 attacks were a calculated attempt to disrupt western commerce.

They worked because, like any high impact terrorist act, they were a

surprise. The timing deepened a recession that was ready to get underway

and broadened the bear market the Tech bubble ushered in. They have cost

$trillions in added security cost and 10s of thousands of lives to war in a

broad protracted aftermath. 9-11 earned the Black Swan Event moniker.

Katrina was an event to be expected though also impossible to time. Most of

the region picked up and carried on as it had after similar weather borne

destruction. Human suffering was largely immediate. The impact to New

Orleans was exceptional. It hasn’t really recovered from its failed levee

system after five years. One immediate impact was to underscore resource

scarcity for oil, plus zinc and other metals for which the city acts a

warehousing/transport hub. That helped set up crazy oil prices, but the event

had little broader impact The Credit Crunch was/is an event that fit

perfectly into the financial model Taleb uses in his (now) popular short fund.

That would seem to make the Crunch an obvious Black Swan Event. It was,

however, another difficult-to-time event like Katrina rather than a true

surprise like 9-11. Many could see the bubbles forming and warned about

them. The timing of the Crunch will be a marker for the economic turning

point from western to eastern centers. Right now it feels like that marker is

being called.

Since it got underway over two and a half years ago, the credit crunch seems

less like a black swan and more like a slow motion train wreck. That is especially true of late. The crisis gripping parts of Europe has been brewing

for months. Like drivers who realize too late they won’t make a corner,

markets are reacting to seemingly implacable forces they can’t seem to

avoid.

There are several worries that relate specifically to the metals sector.

China’s moves to slow the pace of growth appear to be working. That’s good

in the long run if it allows China to avoid its own bubble. The obvious

downside is this could mean a near term slackening of demand that is

showing up in metal prices.

The second is the Australian government’s plan to boost taxes on the “excess

profits” of mining firms. To the obvious impact on companies working in Oz

is added the realization that other jurisdictions could make similar moves.

This is a topic we have touched on in the past and is certainly no black swan

for us.

Its no secret to resource sector participants that others think deposits

magically appear without thought or effort on the part of mining companies.

Many governments see resource extraction as some sort of “free lunch”.

When the sector has periods of high profits they must, by definition, be

“excessive” and fair game for revenue hungry governments.

Obviously this raises the bar that determines what is economically viable by

increasing the average cost base for commodities. Part of the reason cheap

oil is over is a revenue sharing structure that sets a high base price for

anything coming out of the well. Following a similar model in the mining

business will simply help ensure metal prices stay high.

The big worries right now of course are European. Most of these have been

visible for a while but had been “normalized” through the last year of market

recovery. Most of the EU did not deal with anything but emergency debt

issues and let longer term problems fester in denial. However, they have

built one on top of an another until its impossible to ignore the pile’s

abnormality.

To wit:

The sovereign debt of Greece has been labeled junk and is now yielding at

the same level charged by mass mailing credit cards. Portugal’s debt rating

is now slipping away, and Spain is looking increasingly shaky. The €110

billion bail out for Greece with EU/IMF funding is large. Yet Greek workers

are tossing rocks in protest. What they would toss if Germany’s parliament

refuses to ratify its portion we don’t know.

Frustration is understandable, but the reaction of the Greek populace borders

on delusional. The nastier the backlash, the less likely it is that bond buyers

will believe Greece is willing to take the necessary steps. Without some faith

in the bond pits, interest rates in Greece will stay at levels that all but guarantee a debt spiral even with a bailout in place.

Many Club Med citizens are remembering the “good old days” when they

could devalue their way out of spending crises and print the money to pay

back old debts. If reason doesn’t prevail, the core countries in the EU may

have to cover some bank debts directly and give rioters their wish by cutting

them out of the EMU. Definitely one of those “be careful what you wish for”

scenarios that we really hope does not come to pass.

An Icelandic volcano shut down most European air traffic for five days and is

increasing its activity again as this is written. This volcano can spew for

months at time, and has often signaled its bigger neighbor is about to

awaken. The disruptions to air traffic going forward aren’t likely to be as

severe, but it will make travel planning tougher and more expensive to deal

with. Just another headache for Euroland.

A South Korean warship mysteriously sinks, and evidence increasingly points

to a North Korean torpedo as the cause. Since North Korea is mum on the

subject, the best case would seem to be that a lower ranking nutcase was

responsible rather than the “Dear Leader”.

A presumably lone nutcase who fortunately had limited skills plants a bomb

in Times Square. It didn’t explode and is not likely to damage the city’s

image. One wonders if it was actually heading for Wall St and just happened

to begin sputtering in mid Main St. We take a little comfort from that thought

since we’ll be speaking at a conference across the street next week.

A BP oil well in the Gulf of Mexico blows out and is seriously leaking. So far,

damage to the Gulf seems to be relatively limited, but few immediate

solutions are at hand. The impact on further such oil production will at a

minimum be higher capital costs to ensure problems of this sort can be dealt

with more quickly. Washington only recently opened up a number of offshore

areas to new drilling. An ill wind blowing the wrong way could ensure these

areas get closed again.

A writ has been filed against Goldman Sachs and a young VP. It alleges that

a synthetic CDO was filled by the worst possible mortgage crap with the aid

of a client who intended to short it. Regardless of whether this is judged

illegal or not, the ethics at work is going to cause further questioning of how

financial markets function. Goldman is the big dog on Wall St. Most of its

clients didn’t seem too concerned about its proprietary trading as long as the

gains were there. This case could give a lot of those clients second thoughts.

Reformers will now have a freer hand to do their work and those voting

against financial reform bills will have to explain why, even if the bills are

silly. Whether new legislation will actually help is another question.

Most events like those above can be dealt with individually without terribly

serious market disruptions. The potential of sovereign default will always shake things up since banking gets hurt which can lead to severe domino

effects. Greece’s debt is large enough to matter internationally, but only

just. It’s concern for southern Europe as a whole that is the real issue in this

case. The ability of a country to escape a debt spiral is directly correlated to

the interest rate the market demands for its debt. Even if the PIIGS enforce

credible spending cuts they can still be trapped in a spiral if lending costs

don’t settle down. There is no way we know of to legislate this since its

basically about trust.

Financial cotangents are mostly about lost confidence. Despite large gains

for some assets since the Crunch, confidence hadn’t really returned at large

enough scale to deal with a pile this size right now. Most of the European

banking sector has made much less serious efforts to write off and

recapitalize than banks in the US. That may now be forced on them. If

recent bond yields and share prices for southern European banks are any

guide, the equity injections will be public again rather than private.

Markets reflect the common consciousness. That isn’t a philosophical

musing, but merely a fact. If this pile gets any larger markets will continue

to retreat. We try to regularly remind that profits taking should be an on

going part of dealing with what are generally high risk stories. Hopefully you

have taken note.

The $6 Billion?

Now that base metal prices are in decline, the next question is more obvious.

How much is enough? The continuing puzzle of what size of copper inventory

markets can handle comes down to that. LME stockpiles have dropped by

well over 15% since late February, as have the much smaller Comex stocks.

In Shanghai the copper stockpiles have grown by almost 30 Kt in the past

month, which offsets about half the LME declines. All of the SHFE metal

stocks are growing right now, and stockpiles of other mineral goods are flat

lining. Shanghai’s stocks continue to auger the global price picture.

The decline in western stocks may indicate a reluctance to sell metal when it

appears western economies are mending. Added availability in China could

relate to fresh indications the Yuan is finally going to be allowed to rise as

much as it is efforts to slow growth starting to take root. For now, holding

Yuan is a Dollar hedge if it is going to rise.

Regardless, copper’s price has become unstuck from its $3.50 per pound

($7700 per tonne) waypoint. Both prices and stockpiles are in decline, as we

had expected would happen at some point. It’s too soon to call this a trend

since the last 50 cents or so of gain looked like froth that needed blowing off.

We do think the “new-normal” can now establish itself.

The listed copper stockpiles are currently valued at about US $5.5 billion,

down from about $6.2 billion a week ago. A decade ago when stockpiles held about 50% more metal than today they were valued well below $2 billion

(about 65 cents per pound) in the midst of a bear market. That is the

seeming disconnect we have been concerned about. But then, these days a

billion here or there is chump change.

The copper stockpiles are valued at about seven or eight days of trading in

Freeport McMoran. It’s not unusual to hedge producer shares by going into

futures market for the metal. Futures pricing on the LME for copper rises,

slightly, out to the 15 month slot. That on its own could be holding the spot

price up.

It’s also true that smelters are having a tough time contracting as much

concentrate as they’d like. As we’ve noted before the overbuilding of

smelters in China has caused an upstream capacity glut, and smelters have

cut charges to the bone to ensure they can maintain supply. Asian smelters

often supply other units in the same conglomerate. That makes the issue of

supply maintenance a critical concern that could also bring more long buyers

to the futures market.

None of this means the copper price is going to move back up. If sentiment

shifts towards a short circuiting of the western recovery, or the Asian boom,

copper would continue to pull back with everything else.

Copper producers are trading at levels established before copper’s last up

leg. Either the possibility of a broader down turn had still been weighing on

them, or market ratios are changing. Though we think the former is most

likely, this is the wrong time to be concerned on which is the more

important. For the time being we continue to be more focused on warehouse

changes than on price for all the base metals. That and Mediterranean bond

prices.

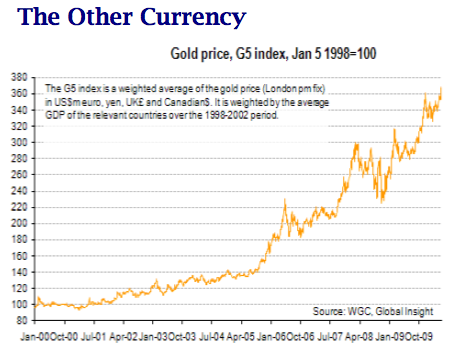

The chart on this page shows the gold price over the last decade measured against a basket of five currencies (the Canadian and US Dollars, UK Pounds, Euros and Yen. It’s a good indication of how strong the recent move has been when you stop thinking in dollars.

Gold has not seen new all time highs in $CAD or $US and yet the chart above

shows a clear upward breakout. The chart for Euros or pounds is much more

impressive and gold has been moving up against all currencies.

All of this is another way of saying gold is trading like a currency which

means its trading on its own against all currencies. There have been a

number of recent sessions where gold had strong upward moves in the face

of falling stock markets and a surging dollar. This is quite different from the

pattern two years ago when gold was falling 30% as markets panicked and

the Dollar surged. Currency trades never happen isolation; you are always

selling one currency to buy another. In the past month we think much of the

new money entering the gold market is coming out of the Euro which has

been crashing hard.

This is different from straight “fear buying” and has the potential to be more

long lasting and fundamental in its aspect. Those that have expected gold to

falter whenever the markets showed some strength lately have been

disappointed.

Gold’s trading pattern has changed several times in the past few years and it

can certainly change again. Nonetheless, the market now seems set up for a

challenge of last year’s all time high which bodes well for gold stocks.

Ω

To view Eric Coffin’s latest video interview on Industry Watch with Al Korelin, please go HERE [April 12, 2010]

Gain access to potential gains of hundreds or even thousands of percent! HRA initiated

coverage on 8 new companies in 2009. So far, the average gain on those companies is

over 250%! For more information about HRA Advisories, please visit:

www.hraadvisories.com