Market Opinion

Please check out our website at:

http://www.raymondjames.ca/jamieswitzer

If you would like to receive our “Weekly Wrap”, please click HERE to subscribe.

Market Summaries

S&P/TSX Composite up 2.23% to 11927 (up 1.53% year-to-date)

S&P/TSX Venture Composite up 1.92% to 1488 (up 0.06% ytd)

Dow Jones Industrial Avg up 2.34% to 10450 (up 0.24% ytd)

Nasdaq Composite up 2.90% to 2309 (up 1.80% ytd)

Oil (West Texas Intermediate) up $4.48 to $78.26 (down $1.10 ytd)

Gold (Spot USD/oz) up $31.60 to $1258.30 (up $161.35 ytd)

Commentary – What is the price of Gold telling us?

Gold closed at an all time high of $1256.50 USD per oz on Friday, surpassing its previous record of $1254.80, set on June 8th. The yellow metal has climbed more than 15% this year, outperforming equities and bonds. Although, Gold could be headed for a cyclical correction in the coming weeks, its current strength suggests that interest is very strong as investors continue to lose confidence in fiat currencies.

With gold trading at all-time highs, one would think that precious metals stocks as represented by indices such as XGD in Canada and GDX in the US have also soared to new highs; peculiarly this is not the case. In fact, they are still trading approximately 7% below their respective all-time highs, a level reached over 3 years ago when Gold was trading around $850 per ounce. This is significant because under normal conditions stock prices lead commodity prices higher. Negative divergences such as this are worth watching due to the fact that it can signal future weakness in the broader equity markets. This also holds true for other sectors, such as copper which has been notably weak since the beginning of May.

The combination of Europe’s fiscal woes and dimming prospects for the US economy has prompted investors to step up and purchase bullion as an alternative asset. On Friday, reports showed US jobless claims rose unexpectedly and manufacturing in the Philadelphia region missed analyst forecasts. Meanwhile, Governments in many of the developed nations, including the U.S., are struggling to meet demands to spend more to boost their respective economies’ while cutting ballooning deficits.

People are looking at the euro as a wake-up call and they are becoming somewhat skeptical of a US recovery. If sovereign debt risks continue to grow then investors will continue to clamour into gold. Should the U.S. Federal Reserve be forced to keep interest rates at a record low in order to try and stimulate the economy, some analysts believe that gold may reach $1400 this year and rise as high as $1600 in 2011.

We have been long term bulls on gold bullion. However, given the divergence between the price of bullion and that of the major stock producers, we recommend clients continue to trade the precious metals sector according to seasonality swings and company specific opportunities.

Soundbites

- It was only a matter of time before the US government took a look at the resource potential in Afghanistan. A recent study by the United States Geoligical Survey found a bounty of valuable minerals in much larger quantities than earlier anticipated. The total value potential of the minerals – including lithium, iron, gold, niobium, mercury, and cobalt – is estimated at $1 trillion USD, with one of the team members saying that may be conservative. President Hamid Karzai said in January, before the latest data, that he hoped the rumoured deposits could help one of the world’s most impoverished countries become one of the richest.

- The much-anticipated dividend cut by BP was announced Wednesday and while it’s prudent given the uncertain future for the much-maligned energy giant, it’s going to take a toll on British investors. At last count, one in seven British pensioners owns BP stock and relies on its once-hefty payout for income. BP said it will probably be Christmas before it entertains the notion of re-implementing the distributions. I’m sure BP shareholders are cursing CEO Tony Hayward, who London’s Daily Telegraph recently reported sold a third of his BP shares only one month before the Deepwater Horizon rig fell to the ocean bottom.

- According to one veteran of the energy patch, we could be in for a wave of consolidation as 2010 plays out. Grant Fagerheim, an oil & gas entrepreneur of 25-years says we are in for a major shakeup, predicting four of every ten companies will not be around this time next year. In a Q&A in Thursday’s National Post, Fagerheim attributes his belief to income trusts having to switch back to corporations and bigger players in search of growth. He mentions Cenovus, EnCana, Talisman, and Canadian Natural Resources as seniors that will be active in merger activity, as well as NAL Oil & Gas Trust and Bonavista Energy Trust as trusts who will be looking to pick off some of the weaker players in the trust conversion space.

- Vancouver-based mining mogul Frank Giustra, Mexican billionaire Carlos Slim, and former US President Bill Clinton have launched a $20 million USD relief fund to help create jobs in earthquake-ravaged Haiti. The fund is targeting small to medium-sized enterprises which are having difficulty securing financing. A 7.0 earthquake ripped through Haiti in January, killing 300,000 and injuring countless others. The damage to buildings was extensive and has left many businesses inoperable making this donation that much more important. Giustra told The Province that the goal for these funds is the same as the principle behind the Clinton Giustra Sustainable Growth Initiative, which was launched three years ago to stimulate economic growth in impoverished countries. “What we’re looking to do is provide capital in a fashion that is more like providing the fishing rod instead of the fish,” Giustra said from Port-au-Prince

Marketwatch – A Look at the Week’s Newsmakers

Churchill Corp (CUQ) – shares of Churchill shot up almost 6% in Tuesday’s session after investors learned that rival Aecon Group has made a $51.2 million equity investment in the Calgary-based firm. The purchase gives Aecon a 15% ownership stake in Churchill which has just completed its own purchase of Seacliff Construction Corp, for $390 million. Churchill is now a well-diversified leader in electrical, data communications and heavy construction, nicely-equipped to take on the challenges of working in western Canada.

BP Plc (BP) – with BP shares plummeting and recently announced dividend suspension, many Brits are panicking. It’s estimated that 40% of all British households own BP shares and have grown accustomed to living off the robust income stream. British Prime Minister David Cameron put out a plea Wednesday afternoon to once again support the company and its shares, stating, “BP is an important company for people’s pensions, employs a lot of people, and it pays lots of tax.” This is just another layer of stress for Britain’s new government which is already facing a troubled economy and rising unemployment. BP shares have dropped more than 50% this year, seriously influencing the savings of individuals and performance of many of Britain’s pension funds.

Quadra FNX Mining Ltd (QUX) – the newly formed combination of Quadra Mining and FNX has hit its first speed bump with a much-ballyhooed partnership with a major Chinese player falling apart last week. The deal, which was announced in March, would have provided Quadra FNX with the needed financing to complete the final phases of the Sierra Gorda copper mine in Chile. After reviewing the proposed agreement, it appears State Grid International Development wanted to wait for all necessary permits to be in place before committing any capital and with Quadra FNX having designs on production by 2013, this simply wasn’t feasible. While talks are said to be ongoing, Quadra FNX CEO Paul Blythe made it clear his company is looking at other options.

“Quote of the Day

“An economist is an expert who will know tomorrow why the things he predicted yesterday didn’t happen today.” Laurence J. Peter (1919 – 1988)

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

MARC LATTA | Raymond James Ltd.

Senior Vice President, Financial Advisor

PH:604-981-3366 | FAX: 604.981.3376

marc.latta@raymondjames.ca

Suite 480, 171 West Esplanade

North Vancouver, British Columbia

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

Please check out our website at:

http://www.raymondjames.ca/jamieswitzer

If you would like to receive our “Weekly Wrap”, please click HERE to subscribe.

Market Summaries as of May 14th/2010

S&P/TSX Composite up 2.80% to 12015 (up 2.30% year-to-date)

S&P/TSX Venture Composite up 2.84% to 1593 (up 9.74% ytd)

Dow Jones Industrial Avg up 2.30% to 10620 (up 1.80% ytd)

Nasdaq Composite up 3.60% to 2347 (up 3.40% ytd)

Oil (West Texas Intermediate) down $3.50 to $71.61 (down $7.75 ytd)

Gold (Spot USD/oz) up $24.55 to $1232.95 (up $136.00 ytd)

Keep Playing Defense

Markets continue to be extremely volatile and last week’s series of swings is probably indicative of how the spring and possible summer will treat investors. Making forecasts beyond the next few weeks seems foolish based on the ever-changing landscape we are facing.

With Greece looking like it could act as the lynch-pin for many more European-based calamities, we are proceeding with caution and not rushing to “buy on the dips.” Gold continues to look strong in this uncertain environment and many utility and consumer staple stocks are weathering this recent round of selling remarkably well. On the “buy side” we have our eye on a few high-yielding utility names, while we may continue to sell broad-based equities as our “stops” continue to be breached to the downside. The addition of the iPath S&P 500 VIX Short Term Futures Index (VXX-US) a few weeks back has worked out very well in the short term but we would be sellers if this market gives any clear “rally” indicators. If this air of uncertainty remains, the VXX tool will provide investors with a great short-term trade opportunity if bought into index rallies.

With a steady diet of negative news, investors seem to be leaving commodities and rotating into more defensive options. Oil is down more than $14 USD a barrel over the past month and more than $10 in the past two weeks. This type of selling pressure is indicative of how the majority of the commodity sector is currently reacting.

In the short to medium term, stay focused on equities that are reacting well in this market volatility and try to avoid chasing the bottom on some of your favourite commodity names of the past year. It may be a while before they find traction again and the peace of mind of owning boring, high-yielding defensive names may be a comforting one.

Soundbites

- BC Hydro has turned to the sporting world to find the man who will lead them into the next decade. Highly regarded former Vancouver Canucks senior exec and deputy CEO of VANOC David Cobb has been named Hydro’s new president and CEO after a lengthy search. Former CEO Bob Elton was shuffled out after a rocky 6-year tenure which now sees the Crown corp taking a risk bringing on Cobb who has a stellar background, but no experience in the electricity sector. Cobb will get thrown into his role head-first, with numerous initiatives to tackle including an aggressive energy conservation target, implementation of the new Clean Energy Act, and overseeing the multi-billion-dollar Site C hydroelectric project – all lightning rods for criticism.

- Our country’s realtors, already under fire from Canada’s competition watchdog, are now facing a new obstacle that could ultimately lead to lower fees. iBidBroker.com has been launched in Toronto by 29-year old entrepreneur and former SmartCentres Inc employee Ajay Jain. The unveiling of the website comes at a time when the Competition Bureau is battling with the Canadian Real Estate Association (CREA) over access to the Multiple Listing Service (MLS) system, which controls about 90% of residential real estate transactions in Canada. Jain, who worked previously in land acquisitions at SmartCentres Inc, has invested $100,000 to $150,000 in his startup, claims his goal is not to lower commissions, but that may end up being the result. “The general concept is, if agents compete, the homeowner is going to win,” he said. Royal LePage CEO Phil Soper is quick to point out that similar websites are already established in the US. LePage recently released a survey that found 86% of its agents worry that deregulation in the industry would erode standards of service.

- In an age where silver-haired men of distinction seem to be running all facets of financial senior management, Britain has turned to 38-year old whiz kid George Osborne to manage what may be the country’s most precarious financial environment in decades. Combine that with the country’s first coalition government since 1945 and you have an intriguing scenario that will keep market-watchers glued to the headlines for a long time to come. Britain is trying to pull itself out of its worst recession since the Second World War, which sees unemployment at a 16-year high and a ballooning deficit that currently stands at 11% of GDP. At 38, Osborne is Britain’s youngest Chancellor the Exchequer (Finance Minister) in more than 100 years.

Marketwatch – A Look at the Week’s Newsmakers

Cardiome Pharmaceuticals Corp (COM) – shares climbed in soft markets after the Vancouver-based bio-tech posted solid Q1 earnings of $15.5 million USD (26 cents per share), compared with losses of $9.2 million just a year earlier. Revenues flew to $23 million (from only $200,000) in the quarter on the momentum of Cardiome’s licensing deal with Merck for its flagship drug, Vernakalant, which focuses on irregular heartbeats.

Crescent Point Energy Corp (CPG) – announced Wednesday it has agreed to pay $1.1 billion to buy the 79% of privately-held Shelter Bay Energy Inc it doesn’t already own. The move boosts its exposure in the prolific Bakken oil field and establishes it as one of the region’s dominant producers. The Shelter Bay operations are extremely familiar to Crescent Point, having created the company in 2008 to avoid federal government restrictions on the growth of trusts. The most recent US Geological Survey estimates Bakken could contain as many as 5.5 billion barrels of oil.

Seacliff Construction Corp (SDC) – shares shot higher in today’s miserable session after the construction company announced that rival Churchill Corp has agreed to pay $390 million, or $17.14 per share for the company. This was a significant jump for the stock, which closed at $14.55 on Friday and represents a 23% premium to the shares’ 20-day average price. The business combination is highly-accretive to Churchill and creates a formidable entity on the general contracting side as well as a strong oilsands player in many facets.

“Quote of the Day

“The things that will destroy America are prosperity-at-any-price, peace-at-any-price, safety-first instead of duty-first, the love of soft living, and the get-rich-quick theory of life” – Teddy Roosevelt.

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

MARC LATTA | Raymond James Ltd.

Senior Vice President, Financial Advisor

PH:604-981-3366 | FAX: 604.981.3376

marc.latta@raymondjames.ca

Suite 480, 171 West Esplanade

North Vancouver, British Columbia

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

Today’s chart provides some long-term perspective in regards to the gold market. As today’s chart illustrates, gold has been in a strong bull market since 2001. The pace of that upward trend increased beginning in mid-2005. Following the financial crisis of late 2008, gold surged once again. While gold made another record high today, it still trades significantly below resistance (red line) of its upward sloping trend channel. In the end, with gold currently trading near $1,250 per ounce, gold has more than quadrupled in price during its nine-year bull market.

How do I get my free Chart of the Day?

Simply enter and submit your email address HERE (we won’t share it with anyone) and you will receive one free chart per week and instantly receive the latest free Chart of the Day.

Today, Chris Mayer, editor of the Capital & Crisis newsletter, offers an update on a notably bullish case for uranium.

VRTrader Platinum Uranium comment by Mark Leibovit – June 14, 2010

Spot: $40.75 UNCHANGED. Bull market high in the cash market was $138.00.

The June Uranium Futures closed at $40.75. Uranium futures recent his a new bear market low of 40.00. June 13, 2007 hosted the bull market high of 154.95. Major support lies well under the market at $36.00.

The spot price of uranium quadrupled from 2004 to 2007. When it hit $138/lb, uranium became a certified bubble, which has now burst.

Cameco Corporation (NYSE:CCJ) — The Bull Case for Uranium

06/18/10 Stockholm, Sweden – Cameco Corporation (NYSE:CCJ) is a Canada-based exploration, development, mining and refining company focused on uranium, the silvery-white metal used for feedstock in nuclear reactors. Cameco is also the world’s largest publicly-traded uranium producer.

Today, Chris Mayer, editor of the Capital & Crisis newsletter, offers an update on a notably bullish case for uranium. From Mayer’s research update:

“First, we are most interested in supply, as any investor in a natural resource should be. We like commodities hard to produce more of when demand rises. That implies that prices will rise quickly. And investors will make a lot of money.

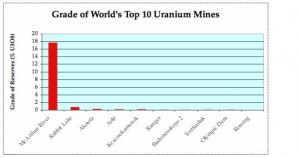

“Uranium fits the bill. Most of the stuff — nearly 60% of it — comes from only 10 mines. Cameco’s MacArthur River mine alone is 15% of the world’s production. For comparison, Forest points out that the top 10 mines in the gold sector produce 19% of the world’s supply. In copper, the top 10 make up 30%. Uranium is a top-heavy field.

“But within that top-heavy field are mega disparities. Mines have grades, which basically tell you how much ore you have to process to get a given quantity of uranium. A high-grade mine means you have to process less. A low-grade mine means you have to munch through more rock to get the same amount of uranium.

“Well, Cameco’s MacArthur mine is the world’s highest-grade mine — and it isn’t even close. Take a look at the next chart, from Dave Forest’s piece titled “Why Uranium Will Make Someone Rich” at Oilprice.com:

“As Forest comments: ‘Top producer McArthur River grades a towering 17.7%. After this, the world’s other top mines barely show up! McArthur is 2,360% richer than No. 2 Rabbit Lake. And a staggering 59,000% higher than the No. 10 mine, Rossing.’

“Rabbit Lake, by the way, is also a Cameco mine. Again, other mining sectors show a smoother curve as you move from left to right. But uranium is quirky.

“So what does this mean? Grades affect costs. High-grade mines are usually low-cost mines. What this means for the uranium industry is the cost curve is extremely steep. That is, as it tries to produce more uranium, the costs of the incremental uranium shoot up rapidly.

“The bull case for uranium is right here in this chart:

On the vertical axis are uranium supply costs and on the horizontal axis is demand. The low-cost mines are in the $10-15 a pound range and all in Saskatchewan. Olympic Dam is highlighted because it is the exception. It is a BHP mine in Australia that produces copper and gold as well. These other metals lower the cost of extracting uranium, but it is not a pure uranium mine.

“As demand moves higher, you can see how the cost rapidly shoots up. In fact, the World Nuclear Association says that 2010 demand will come at 81,000 pounds. That puts us against the right-hand part of the curve.

“It’s true that some uranium will come from existing stockpiles and recycled uranium. But the stockpiles are dwindling and recycled uranium is still a tiny piece of the pie. All this is to say that the pressure on the uranium price will be high. It must move higher to induce these marginal mines to produce.”

Further, Mayer points out that it’s trading for only nine times next year’s cash flow, has a strong balance sheet, no net debt, and over $1 billion in cash. To learn his specific actionable recommendation on Cameco you have to visit the Agora Financial research page and sign up for Capital & Crisis.

Also, remember that Chris Mayer will be speaking at the Agora Financial Investment Symposium in Vancouver. You can register for the July event here.

Best,

Rocky Vega,

The Daily Reckoning

About Rocky Vega

Rocky Vega is a regular contributor to The Daily Reckoning. Previously, he was founding publisher of UrbanTurf and RFID Update, which he operated from Brazil, Chile, and Puerto Rico, and associate publisher of FierceFinance. He specialized in direct marketing at MBI, facilitated MIT Sloan School of Management programs, and has been featured on CBS. Vega graduated with honors from Harvard University, where he was on the board of Let’s Go Publications and directed business programs involving McKinsey, Goldman Sachs, and Harvard Business School faculty. He is also enrolled at the Stockholm School of Economics.

[Nothing in this post should be considered personalized investment advice. Agora Financial employees do not receive any type of compensation from companies covered. Investment decisions should be made in consultation with a financial advisor and only after reviewing relevant financial statements.]

“Europe, like America, is “not crater-ing,” and is not going to change the shape of the US recovery, he said.”

On the global economy, Welch thinks economic pundits such as Nouriel Roubini, nicknamed “Dr. Doom,” are too negative, and the idea that business is bad these days is wrong. On Tuesday, Roubini told CNBC that the risk of a double-dip recession is growing, especially in the euro zone, where restructuring Greece’s debt is inevitable.

Europe, like America, is “not crater-ing,” and is not going to change the shape of the US recovery, he said.

However, he said there is a mismatch of economic and political sensibilities between European nations, which makes operating a common currency extremely tough, according to Welch.

He welcomed the decline in the currency, which has been overvalued for a while. “The euro could go below a buck,” Welch predicted.

…..read more of what Jack Welch former Chairman of GE has to say about BP HERE

Please check out our website at:

http://www.raymondjames.ca/jamieswitzer

If you would like to receive our “Weekly Wrap”, please click HERE to subscribe.

Market Summaries

S&P/TSX Composite up 0.80% to 11667 (down 0.70% year-to-date)

S&P/TSX Venture Composite down 0.27% to 1460 (up 1.86% ytd)

Dow Jones Industrial Avg up 2.80% to 10211 (down 2.10% ytd)

Nasdaq Composite up 1.10% 2244 (down 1.10% ytd)

Oil (West Texas Intermediate) up $2.27 to $73.78 (down $5.58 ytd)

Gold (Spot USD/oz) up $6.80 to $1226.70 (up $129.75 ytd)

Weekly Wrap – edition #357

Lack of Fixed Income Options a Bank-Driven Myth

The media routinely mentions the low-interest rate environment we are in and the lack of safe, solid options for investors looking for yield. This is very true for the purchaser of GIC’s and Canada Savings Bonds; the rates are paltry. But we have become conditioned to peer at the latest posted rate at your neighbourhood bank and accept the big bold numbers on the signage as “what’s available in the current marketplace.” A 1.50%, one-year rate is hardly attractive and when it’s outside of an RRSP or RRIF and subjected to taxes and inflation, what are we left with at the end of the day? If you are willing to open your mind to alternatives, the fixed income arena is much larger than you’re probably aware.

How does a preferred share from Royal Bank yielding 5.71% sound? A 4.18% yield from a laddered 1-5 year government bond ETF? Or a convertible debenture from Trinidad Drilling with a coupon rate of 7.75% and just over two years left to maturity? We have been using options like these to bolster our portfolios over the past 12-18 months. You have to be wary of those investments which are susceptible to rising interest rates, but many will stand up given the right maturity or interest rate provision.

It’s imperative that you don’t take on a tonne of risk just to squeeze out a few more basis points in a fixed income portfolio. This is a component of your investments that should be void of large price swings and risk should be measured. Leave your equity portfolio as the avenue for risk as the upside potential on a bond or preferred share “win” is fairly minimal in most cases. Having said that, moving a few notches higher on the risk chain and away from the GIC world can provide a big increase in yield.

After coming out of the recent credit crisis and watching iconic names such as Lehman Bros and Merrill Lynch implode, we can never “say never” again in our industry – anything is possible. We can however, make educated decisions on which companies would survive if we were to experience another economic downturn? Take a company like Royal Bank. Even at the depths of last year’s catastrophic events, the viability of Royal was rarely questioned and looking back, the firm, along with the entire Canadian banking sector, has come out of that stretch in very good shape. In 2009, with low interest rates and a fragile credit environment, investment bankers were forced to get creative in order to raise money. As a result, a number of preferred share issues were unveiled at attractive interest rates, reasonable terms to maturity and interest rate provisions that gave the purchaser a degree of comfort that the price of the shares wouldn’t get compromised if interest rates were to rise. These issues possess a 5-year interest rate reset clause which gives the issuer the option to call the shares and return the cash to the shareholders, or renew the interest rate at a coupon rate a predetermined amount higher than the 5-year Government of Canada bond yield at that time. This gives the investor a very attractive coupon rate (5 to 6.5%), a reasonable term to maturity (5 years), and protection from interest rates becoming more attractive throughout the life of the investment (5-year interest rate provision).

The Royal option is just one example and the options available are much too long-winded for the purpose of this piece. The goal here is to encourage you to look beyond the bank window for ways to expand your portfolio and refuse the notion that your high quality options end there.

Soundbites

- Canadian banking heavyweights led the charge to defeat the proposed “global bank tax” at last week’s G20 meetings in Montreal. Minister of Finance Jim Flaherty and Bank of Canada governor Mark Carney each addressed the influential audience with similar messages that the any form of global bank tax should be set aside in favour of a renewed focus on bank balance sheets and capital requirements. Flaherty was clearly the most aggressive, stating “quite frankly, we ought to look at accelerating the financial reforms. Uncertainty is the enemy here and banks, and other financial institutions need to know as soon as reasonably possible what the quality and quantity of capital standards are going to be and what the cap on leverage is going to be.”

- The annual “Top 100” list has been unveiled by the Vancouver Sun with mining exec’s once again leading the way, accounting for more than 60% of the entire list. Miners dominated the top 10 with only two non-miners occupying positions (Cannacord CEO Paul Reynolds #4 & Telus head Darren Entwistle at #6). Ivanhoe Mines’ CEO John Macken was #1 with 2009 compensation of nearly $10 million followed by Ivanhoe founder Robert Friedland at $8.51 million and Goldcorp CEO Charles Jeannes at $7.89 million. While these numbers may seem exorbitant, they pale in comparison to Canada’s highest paid executive for 2009. Barrick Gold Corp chief Aaron Regent earned $24.2 million, drawing the ire of shareholders who attempted to have the pay package reduced.

- Sprott’s Peter Hodson makes some excellent points over the weekend in his FP column, titled “Good intentions, bad results.” In so many cases, the near term, knee-jerk reaction to turmoil pleases the masses only to pave a path of future pain. He references a number of recent situations including the manner in which the Lehman Bros fiasco was unwound, ultimately accelerating the credit crisis. And how about the Fed’s 0% interest rate policy which leaves you wondering how those on fixed income’s can be expected to “stimulate” the economy with interest rates on their investments at or near all-time lows? And finally, the spill in the Gulf and subsequent moratorium’s on drilling bring into question where this lack of exploration could leave us five or ten years out when we are already predicting a supply squeeze as things stand? All interesting discussions surrounding the “law of unintended consequences” as Peter puts it…

Marketwatch – A Look at the Week’s Newsmakers

Apple Inc (APPL) – founder Steve Jobs unveiled the company’s new iPhone 4 on Monday to a pumped audience despite the leak of a prototype a few months back. Speaking at the Worldwide Developer Conference in San Francisco, Jobs said,” a lot of you have already seen this,” poking fun at the incident that saw one of Jobs’ senior staff leave a prototype in a bar, only to be later sold to tech blog Gizmodo. Jobs then went on to quip, “believe me, you ain’t really seen it.” The new device has a glass front and antennas built into its stainless steel body. The 4G has 100 new features beyond what the 3G had to offer, and comes 23% thinner than its predecessor making it the thinnest and most advanced smartphone on the planet.

BP Plc (BP) – sick of the BP story yet? Despite the mountainous obstacles the company is facing, it is rumoured to be a takeover target of a number of significant players in the energy game. Shell and Exxon Mobil are two of the names being tossed around as possible suitors for the beleaguered firm. With nearly 50% of BP’s market evaporating since the beginning of the fiasco in the Gulf, the shares are now in bargain territory and are attractive even with an unknown cleanup and legal bill lying in wait. Industry pundits say one scenario would see the assets of BP bought and a company subsequently spun-off that would deal solely with future litigation and cleanup obligations. While speculation increases on BP’s future, one thing that’s in jeopardy is the annual dividend which now yields over 10%. Slashing or even halting the payout would shore up a once pristine balance sheet that is now facing penalties and clean-up costs that’s certain to be in the ten’s of billions.

Uranium One Inc (UUU) – Russian state-controlled miner ARMZ continues to build towards becoming one of the world’s top uranium producers after announcing it has become the controlling shareholder of Vancouver-based Uranium One. The deal, announced Wednesday, will see ARMZ take control of a minimum of 51% of the company, creating an instantly strong international uranium player. Prior to the deal, ARMZ ranked fifth in production and Uranium One, eighth, behind the “Big 3” of Rio Tinto, Cameco Corp, and Kazatomprom.

“Quote of the Day

Give a man a fish, and you’ll feed him for a day. Teach a man to fish, and he’ll buy a funny hat. Talk to a hungry man about fish, and you’re a consultant.” – Scott Adams (1957 – ), Dogbert; Dilbert cartoons

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

MARC LATTA | Raymond James Ltd.

Senior Vice President, Financial Advisor

PH:604-981-3366 | FAX: 604.981.3376

marc.latta@raymondjames.ca

Suite 480, 171 West Esplanade

North Vancouver, British Columbia

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

Please check out our website at:

http://www.raymondjames.ca/jamieswitzer

If you would like to receive our “Weekly Wrap”, please click HERE to subscribe.

Market Summaries as of May 14th/2010

S&P/TSX Composite up 2.80% to 12015 (up 2.30% year-to-date)

S&P/TSX Venture Composite up 2.84% to 1593 (up 9.74% ytd)

Dow Jones Industrial Avg up 2.30% to 10620 (up 1.80% ytd)

Nasdaq Composite up 3.60% to 2347 (up 3.40% ytd)

Oil (West Texas Intermediate) down $3.50 to $71.61 (down $7.75 ytd)

Gold (Spot USD/oz) up $24.55 to $1232.95 (up $136.00 ytd)

Keep Playing Defense

Markets continue to be extremely volatile and last week’s series of swings is probably indicative of how the spring and possible summer will treat investors. Making forecasts beyond the next few weeks seems foolish based on the ever-changing landscape we are facing.

With Greece looking like it could act as the lynch-pin for many more European-based calamities, we are proceeding with caution and not rushing to “buy on the dips.” Gold continues to look strong in this uncertain environment and many utility and consumer staple stocks are weathering this recent round of selling remarkably well. On the “buy side” we have our eye on a few high-yielding utility names, while we may continue to sell broad-based equities as our “stops” continue to be breached to the downside. The addition of the iPath S&P 500 VIX Short Term Futures Index (VXX-US) a few weeks back has worked out very well in the short term but we would be sellers if this market gives any clear “rally” indicators. If this air of uncertainty remains, the VXX tool will provide investors with a great short-term trade opportunity if bought into index rallies.

With a steady diet of negative news, investors seem to be leaving commodities and rotating into more defensive options. Oil is down more than $14 USD a barrel over the past month and more than $10 in the past two weeks. This type of selling pressure is indicative of how the majority of the commodity sector is currently reacting.

In the short to medium term, stay focused on equities that are reacting well in this market volatility and try to avoid chasing the bottom on some of your favourite commodity names of the past year. It may be a while before they find traction again and the peace of mind of owning boring, high-yielding defensive names may be a comforting one.

Soundbites

- BC Hydro has turned to the sporting world to find the man who will lead them into the next decade. Highly regarded former Vancouver Canucks senior exec and deputy CEO of VANOC David Cobb has been named Hydro’s new president and CEO after a lengthy search. Former CEO Bob Elton was shuffled out after a rocky 6-year tenure which now sees the Crown corp taking a risk bringing on Cobb who has a stellar background, but no experience in the electricity sector. Cobb will get thrown into his role head-first, with numerous initiatives to tackle including an aggressive energy conservation target, implementation of the new Clean Energy Act, and overseeing the multi-billion-dollar Site C hydroelectric project – all lightning rods for criticism.

- Our country’s realtors, already under fire from Canada’s competition watchdog, are now facing a new obstacle that could ultimately lead to lower fees. iBidBroker.com has been launched in Toronto by 29-year old entrepreneur and former SmartCentres Inc employee Ajay Jain. The unveiling of the website comes at a time when the Competition Bureau is battling with the Canadian Real Estate Association (CREA) over access to the Multiple Listing Service (MLS) system, which controls about 90% of residential real estate transactions in Canada. Jain, who worked previously in land acquisitions at SmartCentres Inc, has invested $100,000 to $150,000 in his startup, claims his goal is not to lower commissions, but that may end up being the result. “The general concept is, if agents compete, the homeowner is going to win,” he said. Royal LePage CEO Phil Soper is quick to point out that similar websites are already established in the US. LePage recently released a survey that found 86% of its agents worry that deregulation in the industry would erode standards of service.

- In an age where silver-haired men of distinction seem to be running all facets of financial senior management, Britain has turned to 38-year old whiz kid George Osborne to manage what may be the country’s most precarious financial environment in decades. Combine that with the country’s first coalition government since 1945 and you have an intriguing scenario that will keep market-watchers glued to the headlines for a long time to come. Britain is trying to pull itself out of its worst recession since the Second World War, which sees unemployment at a 16-year high and a ballooning deficit that currently stands at 11% of GDP. At 38, Osborne is Britain’s youngest Chancellor the Exchequer (Finance Minister) in more than 100 years.

Marketwatch – A Look at the Week’s Newsmakers

Cardiome Pharmaceuticals Corp (COM) – shares climbed in soft markets after the Vancouver-based bio-tech posted solid Q1 earnings of $15.5 million USD (26 cents per share), compared with losses of $9.2 million just a year earlier. Revenues flew to $23 million (from only $200,000) in the quarter on the momentum of Cardiome’s licensing deal with Merck for its flagship drug, Vernakalant, which focuses on irregular heartbeats.

Crescent Point Energy Corp (CPG) – announced Wednesday it has agreed to pay $1.1 billion to buy the 79% of privately-held Shelter Bay Energy Inc it doesn’t already own. The move boosts its exposure in the prolific Bakken oil field and establishes it as one of the region’s dominant producers. The Shelter Bay operations are extremely familiar to Crescent Point, having created the company in 2008 to avoid federal government restrictions on the growth of trusts. The most recent US Geological Survey estimates Bakken could contain as many as 5.5 billion barrels of oil.

Seacliff Construction Corp (SDC) – shares shot higher in today’s miserable session after the construction company announced that rival Churchill Corp has agreed to pay $390 million, or $17.14 per share for the company. This was a significant jump for the stock, which closed at $14.55 on Friday and represents a 23% premium to the shares’ 20-day average price. The business combination is highly-accretive to Churchill and creates a formidable entity on the general contracting side as well as a strong oilsands player in many facets.

“Quote of the Day

“The things that will destroy America are prosperity-at-any-price, peace-at-any-price, safety-first instead of duty-first, the love of soft living, and the get-rich-quick theory of life” – Teddy Roosevelt.

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

MARC LATTA | Raymond James Ltd.

Senior Vice President, Financial Advisor

PH:604-981-3366 | FAX: 604.981.3376

marc.latta@raymondjames.ca

Suite 480, 171 West Esplanade

North Vancouver, British Columbia

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair