Investment/Finances

Michael Campbell interviewed Tim Cestnick, one of Canada’s most respected tax and personal finance experts to get his checklist list of 2011 yearend tax pointers. Tim is the president and CEO of WaterStreet Family Wealth Counsel and author of 101 Tax Secrets for Canadians, Winning The Tax Game, Winning The Estate Planning Game, and The Tax Freedom Zone. He has also authored Winning The Education Savings Game, co-authored Death and Taxes and Your Family’s Money, and is past editor of Tax Tips for Canadians for Dummies.

Where Can I Find €3 Trillion?

When Leverage Comes Back to Haunt You

The German Dilemma

So How Do We Solve the Eurozone Problem?

Where Is the ECB Printing Press?

DC, Cleveland, and New York

Europe remains the focus of markets, and rightly so. But the picture is not as clear as one would like. Different analysts point to different problems – if only this one problem could be solved, then all this would go away, they tend to say. Sadly, it is not one problem but three that must be solved, and none of them is easy. In today’s letter I try and offer a basic primer on the problems facing Europe. My challenge to myself is to do it in a short piece rather than the book-length tome it could easily become. Thus, in the pursuit of brevity, we will not be as in-depth as usual, but I think it helps us to step back a few feet and look at the larger picture before we focus on minutiae.

Where Can I Find €3 Trillion?

First, for the record, the European issue is not a crisis of confidence, as Merkel and Sarkozy, et., keep telling us. It is structural. And until the structural issues are dealt with, the problems will not be solved.

The first problem facing Europe is the glaring sore thumb: there is simply too much sovereign debt in Greece, Ireland, Spain, Italy, Portugal, and Belgium. That is not news. What has yet to be absorbed by the markets is that the cost of bailouts, present and potential, is likely to be in the €3 trillion range, talking an average of the estimates I have seen (with the Boston Consulting Group suggesting €6 trillion). €3 trillion is not pocket change. Indeed, it is a number that is inconceivable in scope.

Greece has been told that they can write off 50% of their debt held by private entities, but not that owed to the IMF, ECB, or other public entities. This means something more like a 20-30% haircut on total debt. Sean Egan suggests that eventually Greece will write off closer to 90%. That is a number that cannot be contemplated in polite European circles, as it is plenty enough to cause a serious banking crisis.

And that is before we get to the rest of the problem children. Portugal will need at least a 40% write-off (probably more!). The Irish are going to walk away from the bank debt they assumed in the banking crisis. While on paper Spain looks like it may survive, in reality it has significant problems in its banking sector. If they move to insure the solvency of their banks, their debts become unmanageable, not to mention that their debt grows each and every month from the rather large deficits they run and seem totally unwilling to try to reduce. The Spanish government deficit is likely to be at least 7% next year, well above their target of 6%. The “semi-autonomous regions” are in deep trouble, and their citizens are leveraged due to excessive real estate exuberance. Unemployment across Spain is 21%, and for the young it is over 40%.

The Spanish government has adopted the rather novel idea that if it doesn’t pay its bills then its deficit will not be as large and therefore they can get closer to meeting their targets. Yields on Spanish debt are about 1% lower than on Italian debt, but give them time.

And then there is Italy. Italy is simply too big to save. Yes, it looks like Berlusconi is leaving, but he is not the real problem. The problem is a 10-year bond yield at 7%, when your debt is 120% of GDP and growing. Italy is likely to be in recession soon, which will only make the problem worse. A drop in GDP while deficits rise means that debt-to-GDP rises faster. That means interest-rate costs are rising faster than (the lack of) growth in the economy. The deficit is a reported 4.6%. By contrast, Germany’s is 4.3%. But the difference is the debt. The market realizes that if you grow debt by 5% a year, it will not be but a few years until Italy is at 150%. There is no retreat without default from such a number, and the markets are saying, “We’ve seen this movie before and the ending is not a happy one. We think we’ll leave at intermission.”

The ONLY reason that Italian yields have dropped below 7% is that the European Central Bank has been buying Italian debt “in size.” Any retreat by the ECB from buying Italian debt and Italian yields shoot to the moon. Italy will need to raise close to €350 this year, including new debt and rollover debt. The higher rates will put even more pressure on the deficit.

Debt, whether it is with an individual, a family, a city, or a country, always has a limit. Debt cannot grow beyond the ability to service the debt. That is the clear lesson of Rogoff and Reinhardt’s epic work, This Time Is Different. When that limit is reached, the debt must be restructured in some way, either with better terms or through some sort of default.

Mediterranean Europe simply borrowed more than it could pay, given the cash flows of the various countries. And now we are at the Endgame. How can one deal with the debt?

The best solution is to figure out how to grow your economy faster than the growth of debt. Over time, debt service becomes a smaller part of the economy. But Southern Europe does not seemingly have that option. Certainly not Greece, Portugal, or Spain; and this week we learned that Italian production was off 4.8%. Europe, even Germany, is slipping into recession.

Germany is in the position of wanting the problem countries to cut their deficits through something called austerity. And living within your means is hardly a novel idea. It makes a great deal of sense. But when you are a country in recession and have to cut back, it only makes the recession worse for a period of time. Asking Greece to cuts its deficit by 4% a year for 4 years to get to something closer to balance means that the Greek economy will shrink by at least 10%, if not more. Tax revenues, never on solid footing, will shrink, making the deficit worse. How do you ask people to willingly enter into a pepression for a rather long time in order to pay back the banks, even if the debts were freely taken on by the government and the money spent on the populace, and even if the haircuts are 50%?

Yes, if Greece leaves the euro that means they will also have a depression. No one will lend them money for at least three years. Their banks will be insolvent, their pension funds destroyed. Their ability to buy needed materials (like oil, medicines, etc.) will be limited to the amount of goods they can produce and sell. Government employees will be forced to leave jobs, as there will be no money to pay them. Those on government pensions will get a fraction of what they were promised. Going back to the drachma will be painful in the extreme. Just as staying in the euro will be painful. Greece has no good choices.

There are those who suggest that Europe is demonstrating the failure of the socialist welfare state. And there is some reason to say that. But I don’t think the socialist welfare state is the cause of the debt crisis. One can have a welfare state without debt, if you are willing to run a sensible budget. Think of the Scandinavian countries.

And you can have countries without much social welfare get into debt problems. There are plenty of examples in history. Amassing large amounts of debt is a national problem that has as much to do with character as anything else. That is true for families or for countries. It is wanting to spend for goods and services today and pay for them in the future.

Debt has its uses. Properly used, it can be of great benefit to societies and families. People can buy homes and tools that can be used for the production of goods, build roads and other infrastructure, etc. But debt cannot be allowed to become the master of the budget or the source for current spending, again whether for families or countries. And Greece and its fellow countries have used debt to fund current spending and now have run up against the inability to borrow more at sustainable levels.

The easy answer is to cut spending. But when you cut back spending, even borrowed spending, it is going to affect GDP. It is something that may have to be done, but it is not without consequence. Ireland, a small country of 4.2 million people, just paid close to €1 billion to service debt that it owes for taking on the debts of its banks that went bankrupt. That is hugely unpopular in Ireland, and it will not be long before the Irish government simply says no. If the current one does not, then there will be a new one that does. Unless the Irish renegotiate their debt, they will be paying on it for decades. Debt that was private debt and paid to European banks (who lent to Irish banks) is now public debt. And it is a punitive and crushing debt.

We can go to each problem country and home in on its own particular situation, and the answer almost always seems to be that the debt must be dealt with in some manner that either directly or indirectly amounts to default. (Even if the Eurozone leaders say that a 50% haircut by a bank is “voluntary.” Yeah, right. European leaders have a different understanding of voluntary than I learned in school.)

But that is the problem. The European Commission is trying to figure out how to find €1 trillion to use to bail out southern Europe and Ireland. They so far cannot, and the market recognizes that fact and that the needs are actually much higher. European leaders cannot (at least publicly) fathom how to find €3 trillion. But whether or not they can “find” another few trillion, that debt will have to be restructured or defaulted. Once you go down that path, as they have with Greece, it is just a matter of time before you have to do the same for Portugal and Ireland; and are Spain and Italy close on their heels?

When Leverage Comes Back to Haunt You

European regulators allowed their banks to leverage up to 450 to 1 on their capital, on the theory that sovereign nations in an enlightened Europe could not default, and therefore no reserves need to be kept for “investing” in government debt. And with those rules, banks borrowed massively and invested it in government debt, making the spread. It was an awesome free profit machine. Until Greece became a road bump. Now it is a nightmare. Even if you only invested 4% of your bank’s assets in Greek debt, if that is more than your capital then you are bankrupt.

Irish banks were foolish and invested in Irish real estate that was in a bubble. They went bankrupt. Spanish banks were even more heavily leveraged to real estate, but have yet to write down their debt. They assume that houses will only lose about 15%, rather than the 50% that the real world is suggesting. And you can get away with that for a time if you own the agencies that rate the real estate debt, as the Spanish banks do. But most of the rest of European banks are going to go bankrupt the old-fashioned, tried-and-true, proven-over-the-centuries way: by buying government debt. Somehow they want to be seen as rational in leveraging up government debt.

As I told the Irish crowd last week, don’t worry about your bank debt; all you have to do is wait a little while. When French and Italian banks (and most of the other banks in Europe) are publicly insolvent and have to go to their respective countries and the ECB for capital, the relatively small amount (by comparison) of Irish bank debt will not even be noticed when you default. I was trying for a little humor, but there is a core of truth in that glib remark.

France cannot afford to bail out its banks. As we have seen this week, they are already in danger of losing their AAA rating, as a false (premature?) press release from S&P suggested. (Someone is in trouble for that one! Seriously, you think S&P is not ready for this? There is reason to believe, I hear, that this was a draft for use later. We’ll see.) France will want the Eurozone to bail out their banks, and that means the ECB. If France gets such a deal, Ireland will certainly demand – and get – one, too.

The German Dilemma

And that brings us to the third problem, which has two parts: (1) the massive trade imbalances in Europe, where Germany and a few others export and the rest of Europe buys, And (2) the fact that German labor is far cheaper on a relative basis than Greek or Portugal labor (or that of most of the rest of the Eurozone). German workers have seen very little rise in their incomes, while Southern Europe labor costs have risen to over 30% higher.

I won’t go into the details (I have written about this before), but there is a basic rule in economics. You can reduce private debt and you can reduce public debt and you can run a trade deficit. But you can only do two of the three at the same time. The total of the three must balance.

Greece runs a massive trade deficit. They are also attempting to reduce their government debt, and private debt (that borrowed by business and consumers) is being forcibly reduced, as the banks are in full retreat.

Greece must therefore endure a large reduction in its labor costs if it wants to reduce its government deficit. Sell that one to the unions. (By the way, Irish public unions took a large reduction, as did pensioners. Different political climate and country.) Germany seemingly wants the rest of Europe to behave like Germans, except that they also want them to continue to buy German products and run trade deficits, while Germany exports its way to prosperity.

In the “old days” of a decade ago, a European country could simply devalue its currency and adjust the relative value of labor that way. But with a fixed currency there is no adjustment mechanism other than reduced pay or large unemployment numbers, which eventually translates into lower wages.

Essentially, the southern part of Europe is on an odd sort of “gold standard,” with the euro being the fixed standard. And the adjustments are painful. There are no easy answers if you stay with the euro. And leaving is its own nightmare.

So How Do We Solve the Eurozone Problem?

Let’s quickly look at options for solving this.

1. The Germans (and the Dutch and Finns, et al.) can simply take their export surplus and taxes and savings and pay for the deficits in the southern zone until such time as they can be brought under control. Or they can bail out all the banks. Not just their own but throughout Europe, as a customer without a banking system cannot buy your products. That seems to be a political non-starter.

2. The problem countries can make the extremely painful adjustments, cut their deficits, and enter into a lengthy pepression. That also seems to be a political non-starter.

3. The Eurozone can forgive enough debt to get the various countries back to a place where they can function, nationalizing the banks that hold the debt, which would lead to a Europe-wide deep recession. Possible if the Eurozone leaders can sell it, but it is a tough sell.

4. A few countries (2? 3? 4?) can leave the Eurozone. If this is not done in an orderly fashion, the chaos will reverberate around the world.

All of the above paths (or some combination of them) mean a banking crisis and chaos and long-term recessions. These are not pretty paths. But the above options assume that the ECB remains true to its Bundesbank core. Which brings us to the next “solution.”

Where is the Eurozone Printing Press?

It is hard for us in the US to understand, but the commitment of European leaders to a united Europe is amazingly strong. They will do whatever they think they must do (and/or can sell to the voters) to maintain the European Union.

As a way to think about it, the US fought its most bloody war over the question of whether or not to remain a union. I think you have to call that commitment. While I am not suggesting that Europe is getting ready to start a civil war, I think it is helpful to remember that commitments to an ideal can drive people into situations that others have a hard time understanding.

Let’s summarize. There is too much debt in many southern countries; and while I have not yet mentioned it, France is not far from having its own crisis if they do not get back into balance. And if they lose their AAA rating, then any EFSF solution is just so much bad paper.

The banks and banking system are effectively insolvent. There are large trade imbalances that make it almost impossible for the weaker Eurozone countries to grow their way out of the problem.

The path of least resistance, and I use that term guardedly, is for the ECB to find its printing press. Perhaps they can borrow one from Bernanke. Yes, I know they are buying sovereign debt now, but they are “sterilizing” it, meaning they sell euro paper to offset the monetary base effects (large oversimplification, I know).

But the money to solve the crisis does not exist. The only way to find it is for the ECB to print money and print in size, enough to lower the value of the euro and make exports cheaper (which gives southern Europe a chance to grow out of its problems). Which is of course something the Germans vehemently oppose, as it goes against their core DNA coding.

But the choice is print or let the euro perish. I see no other realistic solution, aside from massive austerity, willingly accepted by Europeans everywhere, along with the nationalization of their banks, etc., as described above. I think there is even less willingness to endure all that.

It is a hard choice, I know. If you held a gun to my head and asked, “What do you think they will do?” I would have to say, “I think the ECB prints.” But not without a lot of rancor and solemn pledges and maybe a rewriting of the treaty in order to get Germany to go along.

The choice is between a much lower euro or one that is far different from today’s, with a number of countries having left it. There are no good or easy choices.

As a closing aside, a lower euro means lower US and emerging-market exports (Europe is China’s biggest customer!) to Europe and more competition from Europeans in what the rest of the world sells to each other. It will be the beginning of serious trade issues and when coupled with the collapse of the Japanese yen, circa 2013, will usher in currency wars and protectionism. This will be a decade we will be glad to leave in 2020.

DC, Cleveland, and New York

I leave on Sunday for a few days to go to DC to speak at the UBS national wealth management conference. I hope to see my friend Art Cashin there, as well as finally meet Ken Rogoff, for whom I am an admitted groupie. Next weekend I will take a day trip to Cleveland and the Cleveland Clinic for some medical work. Mike Roizen is going to see what he can do to keep this 62-year-old body going for a few more decades. It is getting stiff! Then Thanksgiving, my favorite holiday, followed by a very quick trip to NYC with Tiffani for some business, media, and friends.

I had great fun in Atlanta this week. Hedge Funds Care raised over $100,000 to help abused children, a very worthy cause. Last Monday I was with my daughter Melissa for her 31st birthday dinner. I was sitting across from her, and some of her friends asked where I was going next. “Atlanta,” I said.

“What are you doing there?”

“I am going to speak at a fundraiser for Hedge Funds Care,” was my short answer. They were aghast. “There’s a charity for hedge funds? That’s just wrong!”

I couldn’t resist. I went with it. “Absolutely. Not a lot of people know or care, but a lot of hedge funds went bankrupt in the crisis in 2008. The managers lost their jobs and everything. Think of their kids! They had to leave their private schools, give up their cars and vacations, and lost their credit cards. It has been hard on them. Someone has to help, and we need to take care of our own.” I totally sucked them in. It was fun until Melissa burst out laughing And teased them for being gullible.

Trips in the US somehow don’t seem all that bad any more. Just a few hours on a plane, reading and writing. It is the long international trips that wear and tear the body, I am thinking. Tomorrow I sleep in, trying to catch up.

By the way, be on the lookout for a very special note from me later next week. I am working on a special offer of some of the best business marketing advice I have ever seen (which has sold for tens of thousands of dollars as seminars, papers, books, etc.), and I have arranged for my readers to get it totally free. My little way of trying to help. And now I will hit the send button and relax for the rest of the night. Have a great week!

Your still having fun analyst,

John Mauldin

John@FrontlineThoughts.com

Thoughts From the Frontline is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

To subscribe to John Mauldin’s e-letter, please click here:

http://www.frontlinethoughts.com/subscribe

To change your email address, please click here:

http://www.frontlinethoughts.com/change-address

If you would ALSO like changes applied to the Mauldin Circle e-letter, please include your old and new email address along with a note requesting the change for both e-letters and send your request towave@frontlinethoughts.com.

And the hits just keep on coming, with the Greek government now just one vote away from total collapse.

Italy, storms back to centre stage with a bang.

…..read more HERE

On Monday, the world population hit 7 billion.

The Christian Science Monitor also revealed some scary facts. Like the fact that in the past 60 years, the population jumped by 4.5 billion. Or that in developed countries, 222 million tons of food are wasted every year.

The competition among non-Chinese junior mining companies to successfully mine rare earth elements (REEs) began as a footrace and evolved into a full-on stampede. That race is now unraveling, thanks to slower global economic growth and the sheer number of exploration companies involved in rare earth exploration. We have seen estimates of over 300 companies involved in this global search, and when you factor in the relatively tiny size of the rare earth market (approximately 130,000 tons produced in 2010, according to the U.S. Geological Survey) we still stand by what we’ve said all along—there is room here for a few major players and not much else. We believe the rare earth industry is in the beginning stages of a phase we call “The Great Reset.” We base this theory on four ideas:

- Everything reverts to the mean. This includes rare earth oxide (REO) prices. While we believe we will see a permanently higher price for select REOs, this is not the case for the entire suite of oxides, and prices cannot continue rising indefinitely. The laws of supply and demand have proven this.

- Demand projections for REOs are being re-evaluated downward due to anemic global economic growth prospects. With a tremendous debt overhang in the United States and Europe and evidence of growth slowing in China (the three biggest economies in the world), lower aggregate demand for finished goods that use REOs is a given. We have seen forecasts for REO demand in 2015 that are higher than they are today, and don’t disagree, but the downward revision is indicative of lower demand for most REOs.

- Companies such as Toyota and General Motors are actively researching substitutes for REOs in their products. This type of research has been in progress for some time and we think that these companies would not be spending the R&D dollars if they didn’t want to avoid high REO prices.

- Demand projections for “green” or “clean tech” applications such as hybrid electric vehicles, wind turbines and solar cells are not factoring in whether or not manufacturers of these goods can ensure a steady supply of raw materials (specifically REOs) to meet their production forecasts. The rare earth industry is a customer-driven business in that the customer needs REOs of a highly specific type and purity. If a wind turbine manufacturer can’t procure a specific purity of neodymium oxide, for example, the wind turbine may get built without neodymium, implying demand destruction. We have seen estimates of the use of up to one ton of neodymium needed to produce one megawatt of generating capacity from a wind turbine. China alone has plans to install 100 gigawatts of generating capacity from wind (up from 12 gigawatts in 2009). When you factor in European and American projections for wind power (not to mention other parts of the world), this begs the question of whether or not there is enough neodymium to go around and if there currently is not, will there be enough to satisfy these growth targets in wind generating capacity? We are well aware of the benefits of neodymium-iron-boron magnets in miniaturization and efficiency, but think that if a product can be manufactured economically without REOs, then the manufacturer will choose that path or abstain from building the product at all.

To be clear—we have not “thrown in the towel” on REOs and the important role they play in certain sectors of the economy. What we are saying is that the role will be different from what many in the sector currently suggest. Like many other facets of life, the rare earth sector is Darwinian in nature and will evolve to equilibrate supply and demand. The gratification that comes along with healthy and growing demand for a product (in this case REOs) will be delayed, to the chagrin of investors and rare earth mining company CEOs alike. This “reset” shapes how we think about the rare earth space now and in the future and in deciding how and where to invest. Below is a price chart of the Bloomberg Rare Earth Mineral Resources Index and its one-year performance.

The One Sector Where Supply and Demand Don’t Matter

There is one area of the economy, however, which we think is immune to the vagaries of supply and demand of REOs: the military. While the potential for substitution exists with consumer products, we believe there is no such “wiggle room” when analyzing a country’s defense capabilities. The neodymium-iron-boron magnets we mentioned above are critical in actuators of precision-guided bombs and are designed specifically around these magnets. Actuators are responsible for control of the bomb, and this is just one of several products (lasers and radar being two significant other products) that must use rare earths to function optimally. Without the magnets in the bombs, performance is reduced—implying an inferior product—something nobody should be willing to accept. The U.S. Military is responsible for a small overall percentage of REO demand in the United States, but it is significant nonetheless.

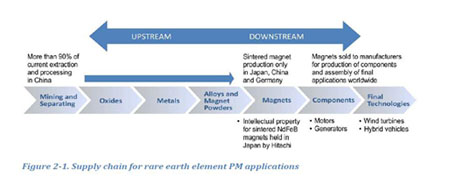

The Rare Earth Supply Chain: The Key to It All

So at this point, we believe two things: first, demand for most REOs will decrease in the near term, and second, that it will be exceedingly difficult for the majority of the junior mining companies involved in rare earth exploration to achieve commercial production of REOs. Despite this, the singular crucial issue that put the rare earth story on the front page of every newspaper around the world in the first place still haunts us—Western dependence on a critical resource from a strategic adversary. While a seemingly endless amount has been written about China’s control of the supply of REEs, what we think is most important (and most often missed by the pundits) is the fact that China also effectively owns the entire mine-to-magnet supply chain. This is the crucial vulnerability. The mining of rare earths is the easy part. It is the resulting steps where intellectual property is created that really matter. In 2010, the United States Government Accountability Office (GAO) was commissioned to deliver a report on the use of rare earth elements in the Department of Defense supply chain. Regarding military capabilities, the report states (Ed. Note: bold text is ours),

“For example, the M1A2 Abrams tank has a reference and navigation system that uses samarium cobalt (SmCo) permanent magnets. The samarium metal used in these magnets comes from China.”

Whether we’re discussing heavy rare earth elements (HREEs) or light rare earth elements (LREEs), a particular concern is the fact that the West is realistically years away from having a supply chain built that can diminish foreign dependence on REOs. Viewed that way, reduced demand for certain REOs could be a blessing in disguise in that it can give Western policymakers more time to formulate a viable strategy, though based on recent behavior in Washington DC (i.e., the debt ceiling debate), we’re not holding our breath. The chart below shows the supply chain for rare earth permanent magnets used in wind turbines and hybrid vehicle motors, among other products. China is responsible for the entire upstream portion of this chain and has designs through mercantilist export policies on owning the entirety of the downstream portion of the chain as well.

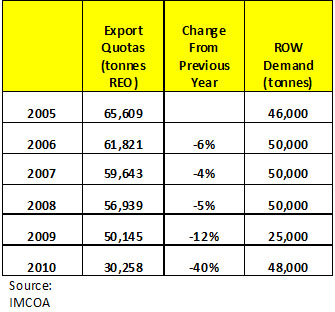

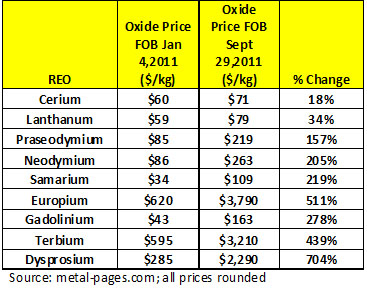

To get a sense of how Chinese export quotas of REOs have decreased in recent years and the resulting increases in prices of REOs, see the charts below:

There are numerous important factors to consider when undertaking due diligence of a mining opportunity (management capability, grade, tonnage, etc.) that we use in the Discovery Investing Ten-Point Factor Model, but we think that there are three keys one must consider initially before looking further at a given rare earth exploration company as an investment.

Despite the fact that we believe the “easy money” has already been made in this sector, we do believe that opportunities for profit exist. Much has been made in recent months of “critical” or “strategic” metals and what constitutes a metal joining this group. We would certainly include rare earths here and, in fact, take this one step further. We consider rare earths to be “political metals.” In the rare earth sector, geopolitics trumps all, and this is the first factor to consider when investing in the junior mining rare earth sector. It should be clear that we have our doubts about permanently increasing demand for REOs. However, due to the significant enhancements REOs provide in military applications, access to a reliable supply of these metals is now on the radar (pardon the pun) of politicians from Brussels, to Ottawa, to Beijing, to Washington DC. In the United States, Sen. Lisa Murkowski (R-Alaska) has been an ardent supporter of rebuilding the U.S. industrial base and supply chain for critical minerals, including rare earths. Rare earth deposits are of strategic significance. A deposit in a safe and stable political jurisdiction is an absolute must.

Second, when comparing rare earth deposits, a decidedly large slant towards HREE mineralization is also a must. After all, the HREEs are truly “rare,” and forecast to be in deficit going forward. In our opinion, investing in a large LREE deposit that promises tens of thousands of tons of REO production per year, when the Chinese dominate this portion of the market and are set to do so going forward, is not a wise move. In the price chart we printed above, dysprosium oxide and terbium oxide (two of the most sought-after HREOs) have increased in price by 704% and 439% respectively, year-to-date. We do not expect continued triple-digit gains in these REO prices, but do believe that deposits with a high percentage of HREEs have potential to outperform going forward.

Finally, while the geopolitics and HREE content are important, without a solid understanding of the metallurgy of a deposit, you could quite literally be investing in moose pasture. This is one of the ultimate differences between rare earths and other metals. Separating 17 metals from each other is an enormously difficult task both technically and financially. This is also a competitive advantage the Chinese have over the West—they have “cracked” the metallurgy of their primary rare earth deposits. While we don’t expect miracles, we do want to see Western rare earth companies making steady progress into understanding the mysteries of the metallurgy. This is one of the biggest risk factors when analyzing a rare earth exploration company.

The Future Is Never Certain, but There Will Always Be a Place for REOs

It appears to be a rather hazy future for the rare earth sector as slow economic growth, potential for substitution, manufacturers potentially misreading demand for their own products that use REOs and price mean reversion all come together to take some of the “froth” out of this market. We think this is a good thing. Regardless, the big picture issues surrounding the need for REOs in various military and clean tech applications are going to keep the industry front and center, but it will evolve much differently than many expect. The Great Reset will ensure that.

Chris Berry, with a lifelong interest in geopolitics and the financial issues that emerge from these relationships, founded House Mountain Partners in 2010. The firm focuses on the evolving geopolitical relationship between emerging and developed economies, the commodity space and junior mining and resource stocks positioned to benefit from this phenomenon. Chris holds an MBA in finance with an international focus from Fordham University, and a BA in international studies from The Virginia Military Institute.

Want to read more exclusive Critical Metals Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators and learn more about critical metals companies, visit our Critical Metals Report page.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair