Investment/Finances

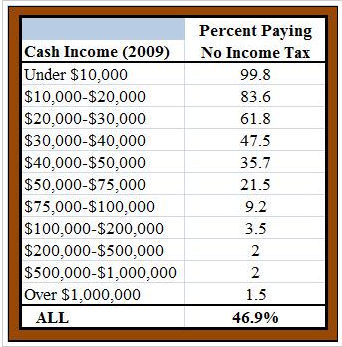

WASHINGTON (AP) — “Tax Day is a dreaded deadline for millions, but for nearly half of U.S. households it’s simply somebody else’s problem. About 47 percent will pay no federal income taxes at all for 2009 (see chart above, data here). Either their incomes were too low, or they qualified for enough credits, deductions and exemptions to eliminate their liability. That’s according to projections by the Tax Policy Center.

In recent years, credits for low- and middle-income families have grown so much that a family of four making as much as $50,000 will owe no federal income tax for 2009, as long as there are two children younger than 17.

Tax cuts enacted in the past decade have been generous to wealthy taxpayers, too, making them a target for President Barack Obama and Democrats in Congress. Less noticed were tax cuts for low- and middle-income families, which were expanded when Obama signed the massive economic recovery package last year. The result is a tax system that exempts almost half the country from paying for programs that benefit everyone, including national defense, public safety, infrastructure and education. It is a system in which the top 10 percent of earners — households making an average of $366,400 in 2006 — paid about 73 percent of the income taxes collected by the federal government.

The bottom 40 percent, on average, make a profit from the federal income tax, meaning they get more money in tax credits than they would otherwise owe in taxes. For those people, the government sends them a payment. “We have 50 percent of people who are getting something for nothing,” said Curtis Dubay, senior tax policy analyst at the Heritage Foundation.”

Mark J. Perry – Carpe Diem

Location:

Washington, D.C., United States

Dr. Mark J. Perry is a professor of economics and finance in the School of Management at the Flint campus of the University of Michigan. Perry holds two graduate degrees in economics (M.A. and Ph.D.) from George Mason University near Washington, D.C. In addition, he holds an MBA degree in finance from the Curtis L. Carlson School of Management at the University of Minnesota. Perry is currently on sabbatical from the University of Michigan and is a visitor at The American Enterprise Institute in Washington, D.C.

View my complete

Every time Easter approaches, I find myself thinking of baskets, eggs and all the other words we investors typically associate with portfolios and diversification.

So I was certainly ready with plenty of holiday-themed metaphors when a friend e-mailed me to say he’d sold his house and wanted advice on what to do with the proceeds.

Of course, the first thing I told him might surprise you: I didn’t say to invest in dividend stocks. Rather, I said his primary goal should be establishing a nice liquid emergency fund.

That begs a good question, of course …

Where the Heck Can You Put

Your Keep-Safe Cash These Days?

It’s no secret that interest rates are pitiful. And as I told my friend, you shouldn’t expect much of a return on your emergency funds. Instead, your main goal is having peace of mind and the wherewithal to survive life’s twists and turns.

For that reason, this account should be considered separate from the uninvested cash in a brokerage account. (That money is best left in a money market fund, either Treasury-only or otherwise at this point.)

Certificates of Deposit (CDs) are clearly the old standby, favored by retirees and conservative investors across the country. That’s because they are readily available and generally very safe — until January 1, 2014 your deposits are insured up to $250,000 at each financial institution ($100,000 thereafter).

The two big problems are: Penalties for early withdrawals and paltry rates right now.

In my opinion, the penalties are enough of a reason to look elsewhere for a liquid savings vehicle. But if you think there’s only a slim chance you’ll need the cash over the life of the CD, they might be okay.

If so, you can find the best current CD rates by using a website like www.bankrate.com. Depending on the term and how much you invest, you should be able to get 3 percent or more. Not bad, but remember that the longer you lock your money up, the greater the chance that interest rates will rise and inflation will outpace your return.

Personally, I would trade higher yields for a greater emphasis on shorter maturities right now.

The first and most important part of any nest egg, is a solid chunk of cash.

Traditional savings and checking accounts are another option. They clearly offer the liquidity you want in an emergency account, but your local bank is probably offering a very poor rate of return right now.

So my suggestion is to start looking nationally using websites like www.checkingfinder.com and www.money-rates.com (for Canadians http://www.bankofcanada.ca/en/rates/). A number of financial institutions are working hard to attract new capital at very favorable rates with high-yield savings accounts and so-called “reward” checking accounts.

Many of the best current rates are now coming from online-only banks (often subsidiaries of household-name brick and mortar franchises). Examples include OnBank (a division of M&T Bank in NY), FNBO Direct (First National Bank of Omaha) and Ally (formerly known as GMAC Bank).

It’s worth noting that these accounts often carry a litany of restrictions and requirements such as receiving statements electronically, making regular direct deposits, using debit cards for purchases, etc. Moreover, many of the attractive rates are only applicable on a certain level of deposits (often $25,000).

Still, if you’re willing to play the game … and even spread your money around at a few institutions … you can certainly earn a much higher return than you might believe possible.

What about bonds? For liquid savings, they would be my least preferred choice because you will not have FDIC insurance and CAN experience capital losses. And I would absolutely insist that you stick only to very short-term bond mutual funds and ETFs.

That said, there are relatively conservative funds that are paying out a percent or two in annual interest.

For example, in Treasuries, the iShares Barclays 1-3 Year Treasury Bond ETF (SHY) yields 1.1 percent and carries an expense ratio of 0.15 percent. Meanwhile, Vanguard’s Short-Term Investment Grade fund (VFSTX), which invests in high-quality corporate bonds, currently yields about 2.3 percent. You can find comparable investments from plenty of other low-cost fund families, too. (For Canadian’s http://www.claymoreinvestments.ca/etf/product-list#INCOMEFIXEDINCOME)

Again, I’m not saying that a yield of 1 percent or 2 percent is much to get excited about. And for the bulk of your investments, especially your retirement funds, I have many ideas that will produce double, triple, and quadruple those numbers.

However, we should all recognize the importance of an ultra-safe, ultra-liquid emergency fund … that is kept in an entirely different basket.

Best wishes,

Nilus

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

Commentary

Banks Want to Hike Dividends

The head of National Bank of Canada says the industry watchdog is standing in the way of higher dividends, making him the first senior banker to speak out against what has become a growing concern for many investors……

….commentary continued below:

Market Summaries

S&P/TSX Composite up 1.6% to 12151 (up 3.4% year-to-date)

Dow Jones Industrial Avg up 0.79% to 10927 (up 4.8% ytd)

Nasdaq Composite up 0.3% to 2403 (up 5.90% ytd)

Oil (West Texas Intermediate) up 4.87 $84.87 (up $5.51 ytd)

Gold (Spot USD/oz) up $12.30 to $1119.80 (up $22.85 ytd)

2009 Personal Income Tax Filing

As you are aware April 30, 2010 is the deadline to file your personal income tax return with the Canada Revenue Agency. In April, we receive a number of requests from both clients and accountants with regards to documents required to complete your return. Please be advised that you should now be in receipt of all pertinent information to file your return. Starting January 1, 2010 you may have received by mail and/or email the following important tax documents:

– 2009 Gain Loss Report

– T5, T3, T5008 and/or T5013

– T4RSP, T4RIF and/or T4A

***Please contact our office prior to April 21, 2010 if you require duplicate copies of any of these documents***

Commentary

Banks Want to Hike Dividends

The head of National Bank of Canada says the industry watchdog is standing in the way of higher dividends, making him the first senior banker to speak out against what has become a growing concern for many investors. Since the financial crisis, the Office of the Superintendent of Financial Institutions (OSFI) has been warning banks and insurance companies not to do anything to jeopardize capital levels, such as boosting or launching major acquisitions until regulators worldwide can agree on a new set of rules for the industry.

But after last year’s near-record bank profits, many investors are growing impatient with OSFI. National Bank CEO Louis Vachon indicated last week that he is willing to increase the bank’s current payout but the regulator needs to be convinced. “From your lips to OSFI’s ears,” he told National Bank’s annual financial-services conference, suggesting shareholders need to start lobbying the regulator. Vachon said he believes the ban on dividend increases could go away as early as this year if the Canadian economy continues to improve and bank loan losses come down. “Maybe it is my hope, more than my view, that the rules for dividends, I think, are going to be looser sooner,” Mr Vachon said.

Julie Dickson, the head of OSFI, has justified the ban by pointing out that if institutions deplete their capital levels now, they could find themselves short when the new regulations come out, resulting in a potential negative impact for shareholders. Most of the attention is focused on the so-called Basel III process which will set guidelines around capital and leverage ratios. However, the US and several European countries are mulling over rules of their own which would also have a major impact. Meanwhile, industry officials are becoming increasingly worried that the process has been taken over by self-interest as regulators and politicians in different jurisdictions use the issue as a way to grab the spotlight.

– Reuters

Soundbites

- The province’s heavy dose of tourism ads throughout the 2010 Winter Olympics and Paralympic Games seem to be paying off. A recent survey found an 11% post-Games increase in the number of US residents who have a positive impression of Vancouver. The provincial ads were run as part of the tourism campaign surrounding the Games. Media coverage in the US also had a significant effect, the study found. “In the case of the Winter Olympics held in Vancouver, there is a clear difference between prior to the Olympics and currently,” said John Nienstedt, president of California-based Competitive Edge Research and Communications, which studies how events impact the image of a host city for a large event. The provincial campaign cost $38.6 million and the Tourism Ministry estimates its ads have been seen almost 1 billion times, through various media avenues.

- The housing and mortgage environment is in for some significant changes beginning with the first rise in mortgage rates in years. Rock-bottom rates are officially in the rear-view mirror after a slew of Canadian banks announced increases to both variable and fixed rate mortgages. In addition, the inclusion of the new lending rules as of April 1st will require first time homebuyers to pass a more stringent set of guidelines before qualifying for a mortgage. Lump in the pending HST, which will make certain purchases more expensive, and a cooling of the housing market could be in the works.

- LinkedIn, the website synonymous with business introductions and professional hook-ups has signed an agreement with Research In Motion Ltd. A day after opening up Canadian offices, LinkedIn announced the new application for Blackberry users that should propel the business networking site into higher traffic volumes based on RIM’s huge subscriber base. This isn’t the first mobile app developed by LinkedIn – the company launched an application for Apple Inc’s iPhone in August, 2008 – but LinkedIn VP Adam Nash said his team tailors each mobile app to take advantage of the specific features of each device.

- The much-anticipated but controversial transformation of the Arctic Ocean into a new oil & gas haven is one step closer to reality with the Obama Administration moving to open that country’s offshore areas – including the Beaufort Sea, subject of a boundary dispute with Canada – to petroleum development. President Obama announced Wednesday plans to end a moratorium on oil-and-gas drilling in almost all US coastal waters, kick-starting what’s expected to be a major push to exploit extensive undersea deposits north of Alaska – part of a total circumpolar resource that geologists believe holds up to one-quarter of the planet’s untapped hydrocarbon reserves. Canada and the US are currently contesting up to 20,000 square km’s of the Beaufort Sea, so this issue could get messy as exploration nears.

Marketwatch – A Look at the Week’s Newsmakers

Royal Bank of Canada (RY) – Barron’s has added CEO Gordon Nixon to its list of the 30 most respected chief executives in the world. Nixon was cited by the influential business weekly for “keeping Canada’s #1 bank thriving” through difficult times. Barron’s publishes the list annually and in order to qualify, CEO’s must have held their position for a minimum of 3 years. The only other Canadian company to qualify was Research In Motion and its co-CEO’s, Jim Balsillie and Mike Lazaridis.

Eacom Timber Corp (ETR) – the Doman family is back. A Richmond-based company run by the former head of Doman Industries Rick Doman, has acquired the forest-products business of Montreal-based Domtar in a deal worth up to $120 million. Eacom Timber Corp, Doman’s TSX Venture Exchange-listed company, said Monday it has agreed to buy Domtar’s forest-products operations for $80 million, plus working capital elements in the $30-40 million range. The company intends to become a major lumber producer after the deal closes, and plans to expand the company’s current client base into Europe and the Middle East. A number of North American producers are looking to capitalize on Russia’s “log export tax” which is now at 25% and is expected to go as high as 80% beginning in 2011, effectively pricing Russia right out of the export business.

Teck Resources Ltd (TCK.B) – Canada’s largest base metals producer has finally regained its investment-grade bond rating after a tumultuous stretch that saw the company staring potential bankruptcy in the face. The yield on Teck’s five-year, 9.75% notes has fallen to 4.51% from 11.2% when they were sold on May 5, according to Trace, the bond-price reporting system of the Financial Industry Regulatory Authority. With the dramatic turnaround, Teck is now yielding less than the overall US corporate bond market at 4.58%, according to Merrill Lynch index data.

“Quote of the Day”

“Look wise, say nothing, and grunt. Speech was given to conceal thought.” – Sir William Osler (1849 – 1919)

This newsletter expresses the opinions of the writers, Marc Latta and Jamie Switzer, and not necessarily those of Raymond James Ltd. (RJL) Statistics and factual data and other information are from sources believed to be reliable but their accuracy cannot be guaranteed. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. It is not meant to provide legal, taxation, or account advice; as each situation is different, please seek advice based on your specific circumstance. RJL and its officers, directors, employees and their families may from time to time invest in the securities discussed in this newsletter. It is intended for distribution only in those jurisdictions where RJL is registered as a dealer in securities. Any distribution or dissemination of this newsletter in any other jurisdiction is strictly prohibited. This newsletter is not intended for nor should it be distributed to any person residing in the USA. Within the last 12 months, Raymond James Ltd. has undertaken an underwriting liability or has provided advice for a fee with respect to the securities of the Royal Bank of Canada. Raymond James Ltd is a member of the Canadian Investor Protection Fund.

JAMIE SWITZER | Raymond James Ltd.

Senior Vice President, Financial Advisor

North Vancouver IAS

PH: 604.981.3355 | FAX: 604.981.3376

jamie.switzer@raymondjames.ca

Dr. Roubini reflects on recent discussions with Chinese policymakers at the China Development Forum, including his suggested response to the flaring U.S.-China currency rift, as well as in-depth discussion of what might happen if the U.S. brands China a “currency manipulator.” Below is his outline of the problem.

In mid-April the U.S. Treasury is expected to publish its biannual report on currency arrangements of other countries. There is a higher probability than ever before that China will be branded a “currency manipulator.” There is no doubt that China is manipulating its currency: After re-pegging to the U.S. dollar in the summer of 2008 and accumulating about US$400 billion dollar a year of additional FX reserves (which now stand, in total, near US$2.4 trillion), there is no doubt, from an economic standpoint, that manipulation is taking place. It looks like a duck and acts like a duck—it is clearly a Peking duck.

But every year, the United States bases the decision of whether to label China a currency manipulator more on politics than on economic facts. Until recently, the likes of Treasury Secretary Tim Geithner and National Economic Council Director Larry Summers could make the argument that a determination of “currency manipulation” for China would cost more in heightened tensions than it would net in trade gains. Such a move could start a trade war and force Chinese officials—who do not ever want to be seen as bowing to foreign pressure—to clam up even further on the currency issue and stubbornly maintain the peg to save face.

This year, several factors have increased the likelihood that China will be branded a currency manipulator. First, the U.S. unemployment rate is at almost 10%, and 17% if you include underemployed and discouraged workers. Second, three quarters of the China trade surplus is with the United States. Third, China re-pegged about 20 months ago and shows no signs of wanting to change its currency policy. Fourth, the political pressure from Congress to get tough on China is at an all-time high: A bipartisan group of 130 representatives have signed a letter arguing that it is time to label China a currency manipulator. Meanwhile, the number of protectionist bills against China in Congress is rising. Fifth, in spite of sharply rising unemployment during the recession, the U.S. refrained from taking sharp protectionist actions. The only clear and explicit case of such protectionism was the case against imports of Chinese tires, a fairly minor trade action given the severity of the U.S. recession. In the U.S. view, China abused this restraint by maintaining the peg and increasing its global trade market share, violating the open-trading system and the WTO regime by not showing flexibility on the currency issue to attempt to rectify the trade imbalances.

The sixth and most important reason China is more likely than ever to get the manipulator stamp: The U.S. administration feels that the policy of keeping quiet on China and engaging its leaders privately has failed. The U.S. grudgingly accepted for a while that China was bound to re-peg in the middle of the economic and financial storm of 2008-09, as it was rapidly losing exports and experiencing a sharp growth slowdown. In fact, had China not pegged, the RMB might have depreciated. But by late 2009, China’s aggressive policy actions had led to a rapid resumption of economic and export growth and rising inflationary pressures that could have been contained in part via currency appreciation. Thus, one would have expected China to start—or at least start signaling—the resumption of slow appreciation of the RMB. Instead, when Barack Obama went to China late last year he was effectively told to take a hike on the currency issue. He was ridiculed by the Chinese for the U.S. fiscal and current account deficits, as well as the accumulation of public and foreign debt. So it was only after months of quiet diplomacy failed to nudge the Chinese to move that the U.S. administration’s patience ran out, and the White House and Congress became publicly vocal on the currency issue.

Things have gotten so bad that even traditional supporters of free trade, and influential thinkers like economist Paul Krugman and fellows at the Peterson Institute for International Economics, are now arguing that it is time to get tough on China with an explicit threat of trade sanctions.

Editor’s Note: The full analysis, “The U.S.-China Currency and Trade Collision Course,” is available exclusively to clients of Roubini Global Economics. For information about becoming an RGE client, visit us at Roubini.com.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair