Daily Updates

US 10 year Treasury yield still signalling “risk off”

Here is the latest update on the US 10 year Treasury yield, which has served as a useful sentiment barometer over the past many years. So far yields remain in a down trend, suggesting the contraction in risk asset prices is not yet complete and the US dollar and bond markets are still receiving relative safe-haven in flows of global capital.

Click on Banner or HERE for Larger Chart

Interestingly as European leaders continue to meet, to meet, to meet, we note the exact opposite trend in European bonds, where prices are falling and yields are spiking across most sovereign markets. Here is a snap shot of french bond yields relative to german bond yields, France being one of the deemed stronger nations who are being asked to rescue Club-Med (Greece, Spain, Italy, Portugal, Ireland).

About Danielle Park

Portfolio Manager, attorney, finance author and a regular guest on North American media, Danielle Park is the author of the best selling myth-busting book “Juggling Dynamite: An insider’s wisdom on money management, markets and wealth that lasts,” as well as a popular daily financial blog:www.jugglingdynamite.com

Danielle worked as an attorney until 1997 when she was recruited to work for an international securities firm. Becoming a Chartered Financial Analyst (CFA), she now helps to manage millions for more than 200 of North America’s wealthiest families as a Portfolio Manager and analyst at the independent investment counsel firm she co-founded Venable Park Investment Counsel Inc. www.venablepark.com. In recent years Danielle has been writing, speaking and educating industry professionals as well as investors on the risks and realities of investment behaviors.

A member of the internationally recognized CFA Institute, Toronto Society of Financial Analysts, and the Law Society of Upper Canada. Danielle is also an avid health and fitness buff.

Mark your calendar for two historic days that could shake Wall Street to its foundation and change the Western world forever …

The first is Europe’s day of reckoning, postponed to Wednesday, October 26 — just two days from now.

If the leaders of the European Union cannot agree to a master plan that saves Greece from utter ruin … shields Spain and Italy from the contagion of wholesale investor selling … protects France from a fatal downgrade … avoids failure for the world’s largest banks … and persuades German voters NOT to dump its government … all hell will break loose in Europe, as I’ll explain this morning.

The second is America’s day of reckoning on Wednesday, November 23 — just one month from now.

If all members of the “Super Committee” in Congress cannot agree to precisely the same kind of compromises that Democrats and Republicans rejected during the debt ceiling debate … if they cannot find $1.2 trillion in painful deficit cuts … then all hell will break loose for the United States, as I’ll also explain this morning.

These are not isolated, random events. They come after more than a HALF CENTURY of judgment days that our leaders have faced — and failed — each time escalating the crisis to a more dangerous level.

So before I lay out the consequences of what’s likely to happen next, let me walk you through the dramatic days of reckoning that brought us to this climactic phase …

Day of Reckoning #1

The Great Budget Battle of 1959

In the late 1950s, the U.S. federal budget was also going haywire. But like today, Congress was complacent and Wall Street, asleep.

My father, J. Irving Weiss, who was advising some of the nation’s leading businesses at the time, decided to do something about it.

He founded the Sound Dollar Committee.

He chose former President Herbert Hoover as Republican co-chairman, plus presidential adviser Bernard Baruch as Democratic co-chairman.

And he proposed to organize a grassroots movement to fight for a balanced budget.

Hoover was eager to participate. But Baruch told my father that he was tired of fighting the same battle, deciding to support the cause strictly from behind the scenes.

In any case, Dad enlisted others to join, including Leonard Spacek, a fiercely outspoken champion of shareholder rights who became the second managing partner of Arthur Andersen; Leslie R. Groves, who managed the construction of the Pentagon and led the Manhattan Project; and many others.

The Sound Dollar Committee began its campaign by placing a full-page ad in The Wall Street Journal, urging the public to contact their representatives in Congress.

In response, The Chicago Tribune, The Los Angeles Times, and The New York Daily Newsdecided to run their own ads at their own expense. And soon, scores of newspapers and magazines did the same.

Congressmen would walk into their offices on a Monday morning and be struck immediately by the clutter of mailbags.

They’d ask their clerks: “What the heck is this? Where did all this mail come from?”

“They’re protests, sir.”

“Protests against what?”

“They’re coupons demanding a balanced budget — cut out from the newspapers, sir. They’re running big ads against deficits and inflation.”

It was an avalanche! According to a survey by The Chicago Tribune on Capitol Hill, the total response was 12 million postcards, coupons, letters, and telegrams.

All of a sudden, Washington was a “city full of inflation fighters,” wrote Business Week. “Leaders in Congress began the session talking like big spenders; now they are talking about cutting Eisenhower’s budget.”

Senator William Proxmire, who had been steadfastly in favor of the deficit spending, changed his mind and voted for the balanced budget. One congressman after another shifted his vote to support the Eisenhower budget.

And the budget was balanced.

At that pivotal point in time, our leaders in Washington had the unique opportunity to keep the budget balanced — and the dollar strong — for decades to come. They had the chance to promote sustainable, balanced growth in America — and the world — for the rest of the century and beyond.

Unfortunately, they did precisely the opposite.

Eisenhower’s balanced budget was blamed for a brief recession that soon followed. Presidents Kennedy, Johnson, and Nixon unleashed wave after wave of new deficit spending. And the United States never turned back from that wayward path.

“We won the battle,” Dad declared years later. “But we lost the war.”

Day of Reckoning #2

The Nixon Devaluation of 1971

Deficit spending, Johnson’s “Great Society,” and foreign wars were enough to stimulate the U.S. economy until the late 1960s.

Then, suddenly and without warning, the economy ran out of steam, inflation surged, and a worldwide monetary crisis burst onto the scene.

President Nixon could have responded with austerity and restraint — painful in the short term, but promoting economic stability for the future.

Instead, he responded with a series of policy bombshells that had precisely the opposite result.

On August 15, 1971, he took the United States off the gold standard, devalued the dollar, and dismantled the stable structure of foreign exchange based on the Bretton Woods Accord of 1944.

Indeed, if just one event in the postwar 20th century could be selected to mark the dividing line between global stability and instability, it would have to be Nixon’s dollar devaluation of August 15, 1971.

It was that fateful step which helped open the floodgates to a series of other devastating turning points. Here are just some of the most important that come to mind …

Day of Reckoning #3

Arab Oil Embargo of 1973

The world’s largest oil-producing nations, sick and tired of getting paid in sinking U.S. dollars, staged the most dramatic economic rebellion of modern history, declaring a global embargo that quadrupled the price of crude oil almost overnight.

In response, the U.S. Federal Reserve could have chosen to ward off the inevitable inflationary consequences by clamping down on monetary growth and strengthening the dollar.

But instead, the Fed did precisely the opposite.

It added still more fuel to the inflationary fires and created the conditions for a further massive destruction of the dollar throughout most of the 1970s.

Most European nations reluctantly followed Washington’s lead. Global inflation took off. And new, even more dramatic days of reckoning would follow …

Day of Reckoning #4

Mass S&L and Bank Failures

Of the 1970s and Early 1980s

Due mostly to surging inflation and interest rates, thousands of U.S. banks and S&Ls failed.

In response, banking authorities could have compelled the banks to forego risky speculation and beef up their capital.

Instead, they did precisely the opposite. They relaxed capital standards and ultimately flooded the economy with still more cheap dollars, depreciating their value even further.

Europe initially hesitated, but ultimately did the same.

Day of Reckoning #5

The Tech Wreck of 2000

After a wild, speculative run, the Nasdaq crashed, ultimately losing three-quarters of its value and sinking the economy into a dangerous recession.

In response, the U.S. government could have taken steps to discourage another round of wild speculation by letting interest rates find their natural level.

But again, the government did precisely the opposite.

The Fed shoved rates down to 1% … pumped still greater quantities of cheap paper dollars into the economy … and helped create the biggest speculative bubble of all time — this time in housing.

Many countries in Europe did the same, creating housing bubbles in the UK, Ireland, Spain, Italy, Greece, and much of Eastern Europe.

Day of Reckoning #6

The Housing Bust and Great Debt Crisis

Of 2007-08

In the wake of the resulting housing bust — plus the debt crisis and collapse of Lehman Brothers in 2008 — Western governments could have finally faced their day of reckoning with the tough love needed to end this long sequence of crises.

Instead, our leaders did precisely the opposite.

They engineered the greatest bailouts of all time, while Fed Chairman Ben Bernanke broke all prior records for money printing in the United States:

Just consider these facts:

→ Before the Lehman Brothers collapse, it had taken the Fed a total 5,012 days — 13 years and 8 months — to double the U.S. monetary base (the best measure of the Fed’s money printing operations).

→ In contrast, after the Lehman Brothers collapse, it took Bernanke’s Fed only 112 days to do so. In other words, he accelerated the pace of bank reserve expansion by a factor of 45 to 1.

Imagine a crowded interstate highway with a speed limit of 55 miles per hour and with a long tradition of allowing no one to exceed that limit by more than 20 or 25 mph.

Suddenly, a new driver appears on the scene with a jet-powered engine that accelerates to a supersonic speed of 1,350 mph. That’s the same magnitude of change Fed Chairman Bernanke presided over in the days after Lehman went under!

Heck, even in the most extreme circumstances of recent history, the Fed had never pumped in anything close to that much money in such a short period of time.

For example, before the turn of the millennium, the Fed scrambled to provide liquidity to U.S. banks to ward off a feared Y2K catastrophe, bumping up bank reserves from $557 billion on October 6, 1999 to $630 billion by January 12, 2000.

At the time, that sudden increase was considered unprecedented —$73 billion in just three months. In contrast, Mr. Bernanke’s money infusion in the 112 days after the Lehman collapse was fourteen times larger!

Similarly, in the days following the 9/11 terrorist attacks, the Fed rushed to flood the banks with liquid funds, adding $40 billion through Sept. 19, 2011. But Mr. Bernanke’s post-Lehman 112-day flood of money was twenty-five times larger.

His counterparts in the UK, France, Germany, and other major European countries did the same, pumping in massive sums to ward off a financial meltdown and save their largest banks from failure.

Day of Reckoning #7

Sovereign Debt Crisis of 2010-11

The entire rationale of these giant bank bailouts in the U.S. and Europe was to contain the debt crisis — to prevent the contagion of fear from spreading to virtually every private-sector borrower in the Western world.

But it backfired!

By 2010, instead of being contained, the contagion had begun to spread to major PUBLIC-sector borrowers — the very same sovereign governments that had splurged to bail out their banks in the years prior.

The banks were drowning in bad debts. But rather than lifting them from the brink, the sovereign governments themselves were dragged underwater!

And so here we are, my friend, facing the last and most dangerous phase of this 50-year sequence of crises — afflicting not only individual banks and corporations, but ENTIRE countries:

• The first to sink was Greece, as global investors dumped Greek debts in panic.

• Soon after Greece received its first bailout from the European Union and the International Monetary Fund, investors began attacking Ireland and Portugal.

• After Ireland and Portugal were bailed out, the contagion hit Spain and Italy.

• And now, we have France on the chopping block, in danger of losing its triple-A rating.

Here’s the key:

At each step of the way — in both the United States and Europe — government leaders have done nothing to change the cowardly pattern that has prevailed for the past half century.

In the wake of each new crisis, rather than cutting back the size of government — or even just slowing down its growth — they conspired to blow it up even more.

Rather than encouraging prudent saving and disciplined investing, they stimulated unbridled spending and wild speculation.

Rather than truly ending each crisis, they merely set the stage for an even larger one.

And now, after five decades of this wanton behavior, they expect to come up with a new “mother of all bailouts” to end the biggest crisis of all?

History tells us that’s not going to happen. It shows us that, ever since the 1960s, the speculation and bad debts have spread from a few too many … from smaller institutions to the largest in the world … and now, from the largest private-sector borrowers to the world’s largest governments.

Each time, our political leaders helped pass the debts upstream to a larger and higher authority. Each time, they postponed the ultimate day of reckoning.

But now, they’re at the end of the line. There’s simply no entity on the planet big enough to bail them out.

Day of Reckoning #8

This Coming Wednesday,

October 26, 2011

esterday at their summit meeting, Europe’s two most powerful leaders — Angela Merkel of Germany and Nicolas Sarkozy of France — could STILL not come up with a viable rescue plan for Europe.

So they will reconvene 48 hours from now … when they’ve vowed to finally come up with a “total solution.”

But the problem is simply too large to solve.

The PIIGS nations — Portugal, Ireland, Italy, Greece, and Spain — are more than 3.1 trillion euros in debt. France — which, according to Moody’s, is now in danger of suffering a fatal downgrade of its debt — owes another 1.6 trillion. Peripheral nations in Eastern Europe owe still more.

All told, we estimate that Europe’s total at-risk debts are nearly triple the size of Germany’s entire economy.

Any “solutions” only make the problem worse, especially for the two last triple-A countries with any clout — France and Germany. Just consider the dilemma of each …

France: Its megabanks — loaded with bad Greek loans — are on the brink of bankruptcy. But if Sarkozy bails them out with French money, France loses its triple-A credit rating and all hell breaks loose in Europe.

Why? Because Europe’s bailout fund, the European Financial Stability Facility, REQUIRES its donors to maintain a triple-A rating, and France is one of the biggest donors. So if France is disqualified, the entire European bailout scheme falls apart.

Germany: Merkel’s megabanks may not be on the brink of bankruptcy — yet. But Merkel’s public support IS. If she helps bail out French banks, her political career is history … the next German government threatens to bow out of the European Union entirely … and the bailout scheme collapses just the same.

Day of Reckoning #9

November 23, 2011,

Just One Month From Today

In the United States, the sovereign debt crisis has taken another form: Paralysis in Washington, with Democrats and Republicans utterly unable to take decisive steps to control the largest sustained deficits of all time.

They couldn’t cut a real deal during the ugly debt ceiling debate this past summer.

And today, they’re deadlocked on precisely the same issues that torpedoed earlier attempts — Republicans absolutely opposed to any semblance of revenue increases, Democrats equally opposed to any cuts in the social safety net.

Result: Despite some spending cuts that will kick in automatically …

• The nation’s gigantic budget deficits will continue to spiral out of control.

• Moody’s and Fitch are bound to follow S&P’s earlier downgrade of the U.S. government, cutting their own U.S. credit ratings and making the downgrade unanimous among the three major credit rating agencies.

• The U.S. stock market, which plunged after the S&P downgrade, will plunge anew.

• And global credit markets, which witnessed massive disruptions last time, will fall into chaos.

Never Before in the 40 Years Since

I Founded Weiss Research Have

I Seen Anything Like This Singular

Convergence of Forces!

We have major Western democracies on the brink of default for the first time ever.

We have the world’s largest economy — the European Union — coming unglued at the seams.

We have America’s budget deficit far beyond reason or control.

We have the world’s largest banks in de facto bankruptcy, kept alive by little more than fiction — that their bad loans are worth “full value.”

We have European and American political leaders in paralysis.

And we have hundreds of thousands of people pouring out onto the streets in protest.

Yet strangely, despite all this, Wall Street is in dreamland. That can continue for a short while. But whether it does or not, you now have one last opportunity to protect yourself.

Stand by for instructions on precisely how.

Join me on my Facebook page to continue this discussion.

And stay tuned for the NEXT major effort by our Sound Dollar Committee.

Above all, stay safe!

Good luck and God bless!

Martin

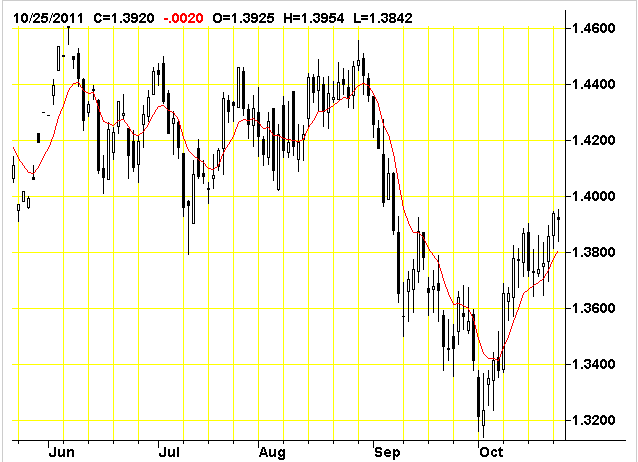

Euro Pacific Capital’s Peter Schiff recommends loading up on your favorite precious metal because the launch in stocks, oil, and even, the euro!, is about to begin.

“You’ve got the euro now at about 1.39, and I think you’ve got a head and shoulders bottom in the euro,” Schiff told King World News yesterday. “Our short-term target for the euro, maybe, by year end, will be up near 1.48.” The implications, suggested from Schiff’s bullish call for the euro, at this critical time are enormous.

Hedge fund manager Eric Sprott’s speech at this week’s Silver Summit turned a room full of nervous precious metals owners into pumped-up silver buyers. Highlights are posted below

- Ten times more silver than gold is produced each year, and the ratio in the earth’s crust is 15:1, so how can the price be 50:1? Expect a return to the historical norm of 15:1, which implies that silver will outperform gold.

- “It’s shocking how undervalued the junior miners are…Gold and silver stocks are growth stocks. They all have a plan to increase production dramatically. Small miners can start a new mine and double in size…The relative value of gold stocks will become apparent with time…The breakout, when it comes, will be very sudden.”

- The demand/supply picture has seen a 380 million ounce per year positive swing — in a 900 million ounce market. Where is the silver coming from?

- The paper silver markets trade a billion ounces a day and the world only produces 900 million in a year. The amount available for settlement of these futures contracts is something like 1.5 million ounces, ludicrously little compared to the amount of paper.

- “On the physical side I’m seeing only buyers.”

- “There are a lot more people who can afford a one-ounce silver coin than an ounce of gold.”

- Gold will be a reserve currency and silver will also play a role.

- “We tried to buy 15 million ounces of silver and had to wait three months — and some of the silver we got was manufactured after we ordered. So there’s not a lot of silver sitting on shelves waiting for people to buy it.”

- “Somewhere along the line some manufacturer will say ‘I can’t get the silver I want’ and the jig’s up.”

- People will prefer gold and silver to having money in a bank where there’s tremendous counterparty risk. Three months ago Dexia was considered to be the best capitalized European bank and now they’ve been nationalized.

- “You go to some of the biggest names who own gold and ask them about silver and a lot of them haven’t even looked at it.”

- Central banks are selling gold surreptitiously.

-

Eric Sprott of Sprott Asset Management back to Financial Sense Newshour for a wide-ranging interview on precious metals. Eric sees the gold to silver ratio eventually contracting, with silver to outperform gold.

Eric has accumulated 35 years of experience in the investment industry. After earning his designation as a chartered accountant, Eric entered the investment industry as a research analyst at Merrill Lynch. In 1981, he founded Sprott Securities (now called Cormark Securities Inc.), which today is one of Canada’s largest independently owned securities firms. After establishing Sprott Asset Management Inc. in December 2001 as a separate entity, Eric divested his entire ownership of Sprott Securities to its employees.

What we are witnessing in the European Crisis is the demise of the welfare state in the form that its in, says Jack Crooks of Black Swan Trading, one of the most respected currency analysts in North America. “It’s a global debt problem and it’s a severe debt problem in the euro zone”. The problem is huge given the Eurozone has 427% debt to GDP while the Bank for International Settlements says anything over 260% is a major drag on growth.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair