Daily Updates

Regular Guest on Money Talks, and one of Michael Campbell’s favorites Jack Crooks of Black Swan Capital is offering Exclusively for readers and listeners of MoneyTalks a very SPECIAL OFFER. When looking at investments or the Economy – “Its all about the price of currencies” – Michael Campbell

In Today’s Currency Currents….

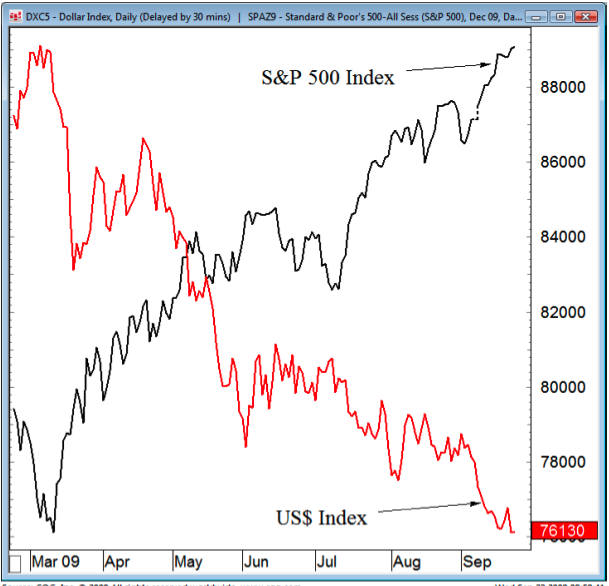

FX Trading – Fed Wednesday. It might be interesting.

Quotable

“Credit expansion is the governments’ foremost tool in their struggle against the market economy. In their hands it is the magic wand designed to conjure away the scarcity of capital goods, to lower the rate of interest or to abolish it altogether, to finance lavish government spending, to expropriate the capitalists, to contrive everlasting booms, and to make everybody prosperous. The final outcome of the credit expansion is general impoverishment.” – Ludwig von Mises

FX Trading – Fed Wednesday. It might be interesting.

Quiet so far this morning in front of the Federal Reserve Bank’s pronouncement on all things monetary due out later this afternoon. We wait to hear how Mr. Bernanke & Co. will decide to save us from ourselves yet again.

One of the questions on the minds of traders everywhere might be: When will Mr. B and Co. decide it’s time to start removing some of the hooch from the punch bowl? We are not sure we will get an answer today, but maybe the Fat Lady of the Fed is warming up. Yesterday, we saw a story indicating as such:

“The Federal Reserve has started talks with bond dealers about withdrawing the unprecedented amount of cash injected into the system the last two years, according to people with knowledge of the discussions,” Bloomberg News reported yesterday.

Of course, as you read further on in the story, the same people with “knowledge of the discussions” say there are no plans to do this anytime soon. I guess the Fed is just getting a brush up from dealers about the arcane process known as reverse purchase agreements—a process used to drain reserves from the system. Heck, the Fed hasn’t drained reserves for so darn long it likely has forgotten how to do it.

Even if Mr. B wants to drain some reserves from the system, most of which are simply sitting un-loaned on banks’ balance sheets anyway, we wonder if Barney Frank will allow it?

But, should the Fed provide some inclination that it’s actually getting ready to act, it might throw some cold water on the idea the dollar is now the carry trade currency of choice, thanks to super low short-term interest rates and US Treasury benign neglect of the dollar. We think there is a lot more to a carry trade currency that meets the eye than just low rates, but we save that view for later today.

We all know there is a wall of momentum, spurred by excess dollar reserves, booting up asset markets here and abroad (whether a bubble or not depends ultimately on a revival of global demand or not). And we all know the “Stimulator of Last Resort’ (US government) is big on the wealth effect i.e. juicing asset markets to try to juice consumer confidence to try to juice global demand, so they seem quite happy with stocks going up.

So if the Fed doesn’t do something to suggests if might mop up something soon, it may be taken as green lighting the seeming US government implicit weak dollar policy as a tool that will continue as long as said dollar falls in an “orderly” matter—bada-bing- bada-boom.

Net, net, this post meeting commentary might actually be interesting.

Jack Crooks

Black Swan Capital LLC

www.blackswantrading.com

Exclusively for readers/listeners/members of MoneyTalks a very SPECIAL OFFER.

Three Full Months of EVERYTHING We Do For Just $99!

Dear MoneyTalks Reader/Listener,

Exclusively for fans of MoneyTalks with Michael Campbell, we’d like to make you an EXCLUSIVE OFFER.

Sign up now to receive 3-months of ALL our advisory trading services and we’ll discount the price by more than 80% – three full months for less than one month’s cost! Plus if you like what you see you’ll continue getting all our trading services at the discounted rate of just $99 per month for as long as you want.

You see, we recently segmented our all-in-one newsletter, Currency Strategist, into four brand new, separate, focused newsletters. As we launch we thought we’d extend an opportunity for you to get in early …

At a very special price.

Everything listed below for 3 months … for just a onetime payment of $99.00.

The value of all these services together is $2,434.00 per year … or about $200 per month. We’re offering you the opportunity to get three full months for just $99.

That’s a difference of over $500.00 for the first three months, and …

With this offer you lock in forever additional savings of more than $100 each and every month off the total value of these services for as long as you remain a member.

As a member you’ll receive…

Currency Currents

Description: Macro view of the global economy and how it may impact currency prices.

Frequency: Daily

Price: Free

Currency Investor

Description: Designed to help investors ride intermediate- and long-term trends in major and select emerging market currencies.

Frequency: Monthly

Recommendations: Exchange Traded Funds (ETFs) [*Analysis and time frames also support multi-currency deposit investors.]

Everyday Price: $149 per year

Currency Options

Description: Designed to provide speculators with trading recommendations covering both the FX options listed on the International Securities Exchange (ISE)and currency futures options listed on the Chicago Mercantile Exchange (CME).

Frequency: Bi-weekly

Average Holding Period: Days or Weeks to months

Recommendations: International Securities Exchange (ISE)-listed FX Options or Chicago Mercantile Exchange (CME)-listed currency futures options

Everyday Price: $595 per year

Emerging Market Currencies

Description: Designed to help traders and speculators exploit short- and intermediate-term trading opportunities in the highly volatile and potentially profitable world of emerging market currencies.

Frequency: Bi-weekly

Average Holding Period: Weeks to months

Recommendations: Spot Forex

Everyday Price: $695 per year

Forex & Currency Futures Description: Designed to help short-term traders, using high leverage, spot trading opportunities among major currency pairs and cross rates.

Frequency: Daily

Average Holding Period: Intraday to several days

Recommendations: Spot Forex and Currency Futures

Everyday Price: $89 per month or $995 per year

[Note: All services include Flash Alerts delivered outside of regular publication dates to enter or exit positions as the market dictates.]

THIS IS WHERE YOU WIN …

As a fan of MoneyTalks, we’re offering you an outstanding deal.

Get three months of all our services for just a onetime payment of $99. That’s a savings of more than 83% on your first three months, and …

You lock in forever an additional savings of over 50% each and every month after that for as long as you remain a member.

Here’s some explanation on the different newsletters you’ll receive …

Our Emerging Market newsletter is geared towards specific emerging market commentary and takes time to evaluate individual countries and themes in depth. We will also recommend a balanced portfolio of currencies to hold as an emerging currency speculator.

In our Currency Options newsletter we are technical-minded, active, and a bit medium-term oriented … occasionally diverging from our longer-term fundamental market views. In addition to that, we incorporate a strict stop-loss guideline in our recommendations, usually around a 50-60% loss threshold, as well as a level at which to take partial profits. We believe this helps reduce the downside and allows for you to be more proactive in grabbing gains when you have them.

In the Forex & Currency Futures newsletter we are active and base most of our trade analysis on short-term technical setups — shooting to grab small open gains when we have them and keeping a skin in the game if we are fortunate to have latched on to a trend. That means you will consistently see recommendations to trade with at least two lots at a time. But remember: the size you trade and amount of leverage must make sense for your own account size and circumstances.

Within the monthly newsletter — Currency Investor — will reside the longer-term trend analysis work and thematic fundamental views incorporating a detailed look at weekly and monthly inter-market relationships between currencies, stocks, bonds and commodities.

Everything you read about above plus access to archives, webinar notifications, audio updates, special reports and more.

We work hard to consistently deliver, what we consider, the best currency trading newsletters available on the market today. We hope you’ll agree.

I urge you, if you were thinking about trading currencies, whether through options, ETFs, futures or Spot FX then don’t wait.

If you want an honest approach and a realistic look at currencies, you’ll have come to the right place.

If for any reason whatsoever you try us out and are unsatisfied with Black Swan’s currency newsletters within the first 30-days of your Membership, we’ll issue a full refund and our thanks for giving us a try.

Take advantage of this 30-day Risk Free offer!

So, if you’re ready to give us a try, Click Here to Sign Up

we’re looking forward to having you onboard with us!

P.S. As a BONUS, subscribe today and receive this 20-page Special Report:

Preparing for a Breakup in the European Monetary System

Most people are worried about the US dollar … and for good reason. These same people tend to see the euro as a real competitor vying for world reserve currency status. Many have been conditioned that way by the financial press. But we believe the risk of breakup in the European Monetary System is building rapidly. We examine the structure of this “artificial fiat currency” and why another downturn in the global economy could mean lights out for the euro. Be prepared.

Even if you decide to cancel, keep the report – it’s yours as a ‘thank you’ for giving us a try!

Even in tough times, which we recognize is on everyone’s mind these days, that’s a very reasonable price for the versatility and money-making potential packed into these newsletters. Of course, at a little over $3 per day you could instead put that money towards you’re morning cup of coffee on the way to work, I guess.

If you want to learn how to implement a solid approach to currency investing … or even if you’re just looking for well-researched trading and investing ideas …

Sincerely,

David Newman

Director of Sales and Marketing

Black Swan Capital

dnewman@blackswantrading.com

Toll-Free 866.846.2672

Futures, Forex and Option trading involves substantial risk, and may not be suitable for everyone. Trading should only be done with true risk capital. Past performance either actual or hypothetical is not indicative of future performance.

Black Swan Capital newsletter services are strictly informational publications and do not provide individual, customized investment advice. The money you allocate to futures or forex should be strictly the money you can afford to risk. Detailed disclaimer can be found at http://www.blackswantrading.com/disclaimer

Step by step, with little fanfare and great complacency, we are witnessing a fundamental, global shift that’s rapidly transforming the investment scene:

The forces of deflation are temporarily receding; and in the meantime, the forces of inflation threaten to roar back with a vengeance.

They are everywhere. They could be overwhelming. They must NOT be ignored …

Inflationary Force #1

Never-Ending, Out-of-Control

U.S. Federal Deficits

As Larry Edelson explained here one week ago:

- Through August, the federal deficit hit $1.38 trillion, or three times last year’s all-time record deficit of $454.8 billion. And in September alone, the administration expects another $200 billion in red ink, bringing the total for the year to $1.58 trillion.

- The U.S. government’s official debt is now at an all-time high of $11.8 trillion, or over $100,000 for each and every household in America.

- Both the administration and its opponents agree that, over the next 10 years, the cumulative federal deficit will be another $9 trillion, driving the burden per household up to $177,000.

- The Federal Reserve is also in hock up to its eyeballs, with more than $2 trillion in liabilities on its balance sheet. That brings the total burden up to $194,000 per household.

- Perhaps worst of all, the government’s unfunded obligations for Social Security, Medicare, and Federal pension payments are also ballooning higher and now stand at an estimated $104 trillion, or $886,000 per household.

- Total burden per household: More than $1 million!

This is, by far, the largest federal deficit in U.S. history — in proportion to household income … in comparison to the nation’s population … or even as a percent of the total economy (other than during major World Wars).

It drives the Fed to print money without restraint. It pumps up demand for scarce goods. And in the months ahead, it’s bound to be the single most powerful pressure point on public policy, financial markets, the U.S. dollar and … inflation.

Inflationary Force #2

New Lows in the U.S. Dollar

Last week, the U.S. dollar sunk to a new, one-year low against a basket of major currencies.

It’s just five points away from its lowest level in history.

And, as Mike Larson detailed this past Friday, the U.S. dollar is now being driven lower by a new, unprecedented factor:

For the first time since 1933, it is now cheaper to borrow dollars than Japanese yen. Indeed, the three-month London Interbank Offered Rate (LIBOR) on the U.S. dollar has slumped to a meager 0.292 percent, while the equivalent rate on the Japanese yen is 0.352 percent.

This means that, instead of using Japanese yen to finance the carry trade — borrowing low-cost money to buy high-yielding investments — international investors will now start using U.S. dollars to finance the carry trade.

It means that, instead of the dollar being a magnet for frightened money, it is becoming precisely the opposite — a source of financing for the risk trade.

Most important, it means that, instead of buying dollars, they have every incentive to borrow dollars and promptly SELL them in order to purchase the higher yielding instruments.

End result: More momentum to the dollar’s decline.

Inflationary Force #3

U.S. Household Wealth

Now Expanding Again

For nearly two years, U.S. households were continually losing wealth. They lost trillions in stocks, bonds, insurance policies, real estate. And these losses, in turn, emerged as a major deflationary force, driving consumer price inflation to zero or lower.

Now, however, in the second quarter of 2009, that trend has reversed.

According to the Fed’s Flow of Funds released just last week, in just the last three months, U.S. households have enjoyed wealth gains of

- $1.1 trillion common and preferred stocks

- $494 billion in mutual funds

- $157 billion in real estate

These gains are still far from enough to recoup the peak asset levels of 2007. But the change in trend is enough to rekindle inflation, and that inflation is likely to take most economists by surprise.

Inflationary Force #4

Exploding U.S. Money Supply

Money pouring into the economy and chasing scarce goods is the classic cause of inflation.

But throughout 2007 and much of 2008, there was no growth whatsoever in U.S. money supply (M1).

During that period, despite the Fed’s efforts to shove interest rates down to practically zero, the total amount of money outstanding remained under $1.4 trillion — another deflationary force.

Now, however, as you can see in this chart provided by www.Shadowstats.com, the outlook has changed dramatically:

Since mid-2008, money supply has exploded beyond $1.65 trillion, with more rapid growth on the way.

Is Deflation Dead?

No. It will return.

But at this juncture, inflation is the primary concern, with far-reaching consequences on how you invest, when and where.

In the days ahead, my team and I will give you step-by-step instructions on how to protect yourself — and profit.

But first, I want to clear up a few basic points. Although we may sometimes disagree on the specific timing and magnitude of particular market moves, we are unanimous in our views about a few fundamental issues:

First, until and unless there is a dramatic change in these inflationary forces, it should be clear that the U.S. dollar’s decline will accelerate in the months ahead.

Second, despite its decline, the U.S. dollar will continue to be a viable, widely traded currency. It will not, as some seem to fear, simply disappear from the face of the earth.

Third, it is both impractical and unreasonable to abandon U.S. Treasury bills and other conservative dollar-denominated investments. They continue to provide U.S. citizens and residents the best safety and liquidity in the world today.

Fourth, the best way to protect yourself from a falling dollar is with contra-dollar investments such as precious metals, natural resources and assets tied to strong foreign currencies.

Stand by for more details in upcoming emails from key members of our team, including myself, Larry Edelson and Mike Larson.

Good luck and God bless!

Martin

Martin D. Weiss, Ph.D., founder and president of Weiss Research, Inc. and a leading advocate for investor safety, is a nationally recognized expert on domestic and international financial markets. With more than 35 years of experience, including many years in Latin America and Asia, Dr. Weiss has helped empower millions of investors to make better financial decisions through his monthly Safe Money and daily Money and Markets.

Dr. Weiss’ keen understanding of foreign markets and the global economy has earned him a reputation for thoughtful, in-depth analysis that investors can rely upon to make informed financial decisions. Regularly called upon by the media for his independent investing guidance, he has been featured in publications nationwide, including The Wall Street Journal, The New York Times, The Chicago Tribune, Investor’s Business Daily, and Forbes, and has also appeared on CNN and CNBC.

Throughout his career, Dr. Weiss has been an advocate for consumers and investors in the insurance, banking and brokerage industries, dedicating his time and resources to provide analysis and data for Congressional testimony, constructive proposals for reforms in the securities industry and legislation for full financial disclosure as well sound accounting and fiscal policy. In November 2004, he launched the Sound Dollar Committee, a nonprofit organization dedicated to building a network of investors seeking to protect the nation’s future by demanding honesty in government accounting, a balanced budget and sound economic policy.

Dr. Weiss is author of The New York Times best-seller, The Ultimate Safe Money Guide, which gave baby boomers a road map to grow their wealth safely. It was listed on the New York Times Business, Wall Street Journal, and BusinessWeek best-seller lists, as well as the Barron’s Roundup for 2002.

Dr. Weiss holds a bachelor’s degree from New York University, a Ph.D. from Columbia University and is fluent in eight European and Asian languages.

A brief excerpt of the lengthy daily internet comment by Richard Russell of Dow theory Letters. One of the best values anywhere in the financial world at only a $300 subscription to get his report daily for a year. HERE to subscribe.

The argument and puzzlement goes on. Are we seeing inflation or deflation? Maybe both. The deflation trend stems from world overproduction. The M-2 money supply, wages and bank credit are contracting, all of which spells deflation. What about bank credit? Is it that the banks just don’t want to lend; they’d rather build up cash reserves? The banks claim otherwise; they say that nobody wants to borrow, which is why they’re not lending.

As for the inflation side of the argument, the inflation is in the huge Fed and Treasury borrowing. Many say (and I’m one of them) that the only way the absurd national debt can be handled is via inflation. Is this what gold is really looking at? So both forces are at work — inflation and deflation. Gold is acting erratically, trying to deal first with one force, then the other.. Meanwhile, the Chinese see the writing on the wall, and they are getting rid of dollars and accumulating gold as fast as they politely can.

In the big picture, I keep referring to American consumers. Can the government lure them into a buying and borrowing mood? I remain sceptical. I think that for the first time since World War II, US consumers have turned thrifty. Even the upper-middle class and the so-called rich are cutting back. The dreaded rumor is that wealthy people have been seen shopping at Target and Wal-mart. Is this the end of the world as we know it? Anybody see Bill Gates and Melinda having dinner at McDonald’s?

The 84 yr. old writes a market comment daily since the internet age began. In recent years, he began strongly advocated buying gold coins in the late 1990’s below $300. His position before the recent crash was cash and gold.

There is little in markets he has not seen. Mr. Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974. He loaded up on bonds in the early 80’s when US Treasuries where yielding 18%.

What Company Would You Buy with $100 Million?

Today, I’d like to play make believe by pretending we’ve just won $100 million with a Powerball ticket.

I only suggest playing the lottery in Fantasy Land, of course. In real life I consider it the world’s most popular voluntary tax. But let’s just say we played, and things went our way.

Our next big question should be how we’re going to invest our windfall.

Oh, you’re worried about taxes? You shouldn’t be. This is Fantasy Land — there are no taxes!

Back to our wonderful dilemma of how to invest the cash.

Sure we could just keep it in cash equivalents. Heck, we should be able to scrape by even if we only make 1 percent a year on our lousy $100 million.

Still that seems rather unfulfilling. So let’s buy a business. I’ll get our new investment banker buddies to line up some candidates for us …

Here Are Three Potential Companies for Us to Invest In!

Company #1. In comes a guy wearing a lab coat. Apparently, he’s an expert in building transistors that will be used in future space shuttles.

All he needs is our money to hire a team of scientists. They’ll spend a couple years developing the product, and hopefully it will earn a patent. Then, once the finished transistor beats out its competition in a government contest, the scientist says we’ll cash out big time when our company’s share price goes to the moon.

Company #2. Our next candidate is dressed in a designer suit. He runs a pretty large chain of clothing stores in the New York metropolitan area. And now he wants to go national with our money.

If the stores catch on, they’ll be bigger than The Gap, he says. Heck, he’s already making pretty good money at his current locations. He just needs funding to scout and acquire new locations and advertise. Also, he wants to fight the existing national chains by setting up some offshore manufacturing facilities. That way we’ll be able to offer clothes at even lower prices.

And, hey, in the best case scenario … The Gap might even just buy the chain if it really catches on!

Company #3. Standing before us is an older man, dressed in a pair of worn khakis and a tattered navy blazer. Turns out that he’s the great-grandson of John Henderson, the creator of Henderson’s World-Famous Chocolates. You know the product … heck, you’ve been eating them since you were a kid.

Apparently, the company is doing just fine by selling its chocolates all over the globe. But the great grandson wants to spend his golden years sailing yachts … NOT thinking about a chocolate empire. So he’ll sell his stake to you at a fair price. The current managers will still run the business, and send your share of the profits every quarter. And as the great grandson points out, Henderson Chocolates hasn’t had a losing year in the last three decades. Even the recession hasn’t really put a big dent in sales.

Now, I Ask You: Which Person Should We Give Our Money To?

Before you answer, let’s review some of the pros and cons of the various businesses …

The transistor opportunity sounds like it could be wildly profitable if everything goes right. We’d be in on the ground floor, and there’s no doubt that a government contract would pay handsomely. Plus, our friends would be really impressed when we tell them we’re funding missions in space!

But I certainly don’t know much about the field. Do you? More importantly, there are a lot of obstacles in the way of success. We’ll probably be waiting a long time to get paid for taking all that risk.

Meanwhile, the clothing business sounds healthy and it’s making money already. Going national could mean nice growth on our initial investment. And there’s the possibility of a buyout down the line.

On the other hand, clothing and fashion are very trend driven, and even the owner says there’s already LOTS of competition in place. Will the stores succeed beyond the New York metro area? And for how long? If the economy slips again, or people suddenly start wearing togas, we might have some serious down years ahead.

As far as the chocolate company … there are clearly some ins and outs of running a large multinational operation that are best left to the executive team. Nor should we expect tremendous growth. But at least we understand the basics of the business as well as the risks.

Even better is the fact that we don’t have to wait for a bunch of milestones to be met or for somebody to come along and buy our shares out from under us.

In fact, this is the kind of cash cow we’d rather just hang onto. Sure, we’ll probably be able to sell at a higher price down the line if we want to … but we’ll also be getting immediate profits sent to us starting RIGHT NOW and probably for as long as we continue holding.

If you’re getting the impression that I like Company #3 the best … you’re right. Heck, what’s not to like?

And here’s the point of our imaginary scenario …

While you probably don’t have $100 million to invest at the moment, you still face these same basic choices when you invest even $1 in the stock market!

Yes, you have far more than three choices when you go out shopping for a stock to buy. There are a tremendous number of businesses in the world … all with varying risk profiles, structures, end markets, and more.

Yet I think it’s fair to lump companies into some basic categories. And that’s what I was trying to do with the three imaginary firms.

Company #1 is like the Nasdaq tech stocks everyone loved so much in the late 1990s — great to brag about, hard to understand for most investors, and very much like playing the lotto unless you do A LOT of research and really understand the firm’s niche. Of course, the profits can be huge.

Company #2 is that so-called “growth” firm that has its greatest years ahead of it, as long as things go according to plan. It’s probably in a cyclical sector … which also means volatile swings. But there’s potential for solid returns if you get the story right.

And Company #3 is what a lot of people dismiss as a boring “value” firm. The kind of company that is going to continue chugging along as it has for decades, spinning off cash, and growing modestly year in and year out. Your friends won’t be impressed, but you stand a very good chance of making money year in and year out.

A bit of an oversimplification? Maybe. I’m not saying it’s simply growth vs. value. I actually think that’s a false dilemma because my favorite companies are BOTH undervalued and growing steadily.

No, the real issue is whether or not you’re buying companies with real, profitable, long-term businesses … companies that are willing to reward you right away with steady income … and companies that are posting sustainable growth without big competitive challenges ahead of them.

I mean, really, why would you risk your hard-earned investment dollars on some fly-by-night company that operates a business you can’t even understand? Especially when you can buy stock in profitable, growing companies you already know and trust.

Right now, with stocks running higher, it’s easy to lose sight of this basic concept. But don’t forget that when you buy a stock, you are literally buying a company. Make sure you understand its business … the risks and rewards … and precisely how you — as an owner — are going to profit (and WHEN).

In the real world you don’t have to just buy one company. So by all means, go ahead and put a little bit of your money into a couple more speculative shares with good prospects as well as some faster-growing companies.

At the same time, I suggest you also make sure the bulk of your stocks will be able to weather the potential economic challenges ahead … and begin paying you non-refundable profits in the form of dividends immediately.

Best wishes,

Nilus

P.S. Just to prove that I “walk the walk” … I AM currently recommending a few more speculative companies along with the steady, conservative firms in my Dividend Superstars newsletter right now. But I still insist that even those aggressive positions pay out dividends right now.

Nilus Mattive, a financial analyst at Weiss Research, is the editor of Dividend Superstars, a monthly publication and is also the editor of the company’s daily e-letter, Money and Markets. Formerly a senior editor of Standard & Poor’s The Outlook, the oldest continuously published investment newsletter in the country, he has written for a number of investment websites, including BusinessWeek and Individual Investor. Mr. Mattive is the author of The Standard & Poor’s Guide for the New Investor (McGraw-Hill, 2004) and has appeared on the popular investment radio show, Traders Nation, to discuss his views on personal finance.

Mr. Mattive graduated cum laude from the University of Scranton.

by: Martin A. Armstrong

Former Chairman of Princeton Economics International, Ltd. and the Foundaton for the Study of Cycles.

Many people assume that because I am against Marxism, that this means I advocate soaking the poor for the benefit of the rich. To really understand the trugh of trends, if you are unvilling to examine the propaganda without the personal bias, you will never see the light of day. This argument between the rich vs the poor, has been so distorted and used to further other goals hidden beneath the surface, we get a lot of heated arugments with no substance. Unfortunately, if you will not examine the facts, then you are allowing those who will manipulated the real core of the people, get away with everything.

Let us examine what has really taken place under Marxism. Putting Russia and China aside, let us look at the Western nations who adopted Marxism under the label of “Socialism” or “Progressive Movements” post 1883.

……read full thesis HERE.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair