Daily Updates

“The average duration of a bear market in months is 14-months with the longest modern bear of 1973-74 running almost 24 months. If you’re a bear we are now into 24-months from the peak of October 2007. Clearly the math does not support a current bear environment.”

Dilemma – a noun pronounced [di-lem-uh] meaning a situation requiring a choice between two equally undesirable alternatives. The great stock market advance that began in early March 2009 has set up an investment dilemma for both the bulls and the bears.

Bearish investors assumed the great advance to be a sucker bear market rally and sat in cash alternatives waiting for a major correction – possibly back down to re-test the March 2009 lows. Dilemma, do they capitulate and buy in now and risk a correction or do they sit in cash and wait for a correction that may never materialize?

Bullish investors who enjoyed the advance assume it is a youthful bull market and fear not to remain invested. They also fear that a correction could wipe away much of their March to date returns. Dilemma, do they sell now and try to re-enter at lower prices that may never materialize or do they hold and remain fully invested and risk a correction?

We need to decide, is this a bull market or – is this a bear market? Solve that and we resolve the dilemma. If a bull market the bears should buy in now and the bulls should remain fully invested. If we still have a bear market the bears will stay in cash and await the correction and the bulls will sell and lock in those bear rally profits.

Perhaps some historical data on bull and bear markets will help when we examine the duration of the bull and bear cycle over the past 100 years.

The average duration of a bear market in months is 14-months with the longest modern bear of 1973-74 running almost 24 months. If you’re a bear we are now into 24-months from the peak of October 2007. Clearly the math does not support a current bear environment.

The average duration of a bull market in months is 24-months with the longest modern bull of 1990-1998 spanning 94 months. If you’re a bull we are now only 6-months from the bottom of March 2009 and so the math does not support the end of the current bull.

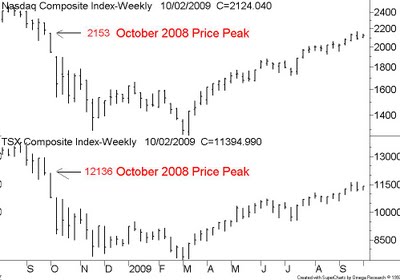

The other issue to support the bull market scenario is the growing number of new 52-week highs in many of the important stock sectors. Yesterday stocks listed on the Nasdaq, the NYSE and the TSX posted over 200 new highs and only 14 new 52-week lows. As we move into October most of the broader indices are approaching new 52-weeks highs with the Nasdaq currently within 2% of the October 2008 peak and the all important Russell 2000 while 15% below the October 2008 peak is above the November 2008 peak

Our chart below looks at the TSX Composite and the Nasdaq October 2008 price targets – if these 52-week targets are overcome, the bears will capitulate and trigger a bullish stampede into equities.

Closing In – 52-week Price Targets on the TSX Comp and the Nasdaq

Bill Carrigan of Gettingtechnical.com

Bill has been writing a weekly business column in the Toronto Star since 1997, and was an early contributor to the former “Report on Business Television”. He has founded the Getting Technical Market Newsletter in December 1998. Bill is also an Instructor for the Canadian Securities Institute. He is also a contributing author of the textbook for the technical analysis course offered by the Canadian Securities Institute (CSI. He is also called upon to provide training to industry professionals on technical analysis at many of Canada’s leading brokerage firms.

Houses bounce too…

Not much happened yesterday. The Dow fell 47 points. The newspapers attributed the reversal to surprisingly low consumer confidence numbers. Apparently, consumers aren’t so sure this crisis is over. As we reported yesterday, they’re saving money…maybe even at an 8% rate.

Oil didn’t move yesterday. Neither did gold.

The Wall Street Journal reported that markets were reacting to “mixed data.”

That is to say, some reports were encouraging. Others were not. It was as if one weather forecaster called for a blizzard and the other for sunny skies and warm temperatures. Investors didn’t know how to dress.

Among the dark clouds was an item on the falloff in tax revenues. States are having a hard time balancing their books, because their tax receipts are declining. The WSJ reports that they are running 17% below last year. Since states cannot print money, they’re forced to make cutbacks – typically reducing hours worked per employee as well as the total number of employees. This is a bad thing, says the report, because it increases unemployment and lowers the wage base, leading to less consumer spending.

Another little cloud appeared yesterday (in addition to the consumer confidence numbers): the vacation timeshare market is collapsing at a record pace.

Well, don’t worry about it. We met a guy who explained the timeshare business to us.

“What you’re selling is a dream. You bring them to the property. You make sure they have a good…

…..Read more HERE.

Since founding Agora Inc. in 1979, Bill Bonner has found success and garnered camaraderie in numerous communities and industries. A man of many talents, his entrepreneurial savvy, unique writings, philanthropic undertakings, and preservationist activities have all been recognized and awarded by some of America’s most respected authorities. Along with Addison Wiggin, his friend and colleague, Bill has written two New York Times best-selling books, Financial Reckoning Day and Empire of Debt. Both works have been critically acclaimed and internationally. With political journalist Lila Rajiva, he wrote his third New York Times best-selling book, Mobs, Messiahs and Markets, which offers concrete advice on how to avoid the public spectacle of modern finance. Since 1999, Bill has been a daily contributor and the driving force behind The Daily.

“few people on or off Wall Street have capitalized on this crisis as deftly as Mr. Buffett. After counseling Washington to rescue the nation’s financial industry and publicly urging Americans to buy stocks as the markets reeled, in he swooped. Mr. Buffett positioned himself to profit from the market mayhem — as well as all those taxpayer-financed bailouts — and thus secure his legacy as one of the greatest investors of all time.” NY Times -Sept.10th 2009

Jim Grant: The Perma-bear Turns Bullish – Sept. 30th/2009

If you’ve never heard of Jim Grant, let me just say this: he makes Ebenezer Scrooge look like a party animal. That’s how pessimistic Grant has been. . . for as long as I can remember.

In the September 19 article titled “From Bear to Bull,” Jim writes:

“The deeper the slump, the zippier the recovery. To quote a dissenter from the forecasting consensus, Michael T. Darda, chief economist of MKM Partners, Greenwich, Conn.: “[T]he most important determinant of the strength of an economy recovery is the depth of the downturn that preceded it. There are no exceptions to this rule, including the 1929-1939 period.”

Growth snapped back following the depressions of 1893-94, 1907-08, 1920-21 and 1929-33. If ugly downturns made for torpid recoveries, as today’s economists suggest, the economic history of this country would have to be rewritten.

Bears and doom-and-gloomers the world over could always count on Grant as their sage on Wall Street.

And while Grant has always been and will continue to be counted on to be a bear, he’s also an astute historian of Wall Street.

In his heart of hearts, Jim wants to be a bear. But even he can’t reject precedent.

And for those bears that are arguing that this time is different. . . let me remind you that that argument has been used in every bull or bear market. During the dot-com mania of the late 1990s, every bull was arguing that technology has made obsolete the business cycle.

Nobody knows if a robust recovery is coming. Even Grant will admit that. But if past economic downturns offer clues for future recoveries, there’s reason for optimism.

Grant writes:

“Our recession, though a mere inconvenience compared to some of the cyclical snows of yesteryear, does bear comparison with the slump of 1981-82. In the worst quarter of that contraction, the first three months of 1982, real GDP shrank at an annual rate of 6.4%, matching the steepest drop of the current recession, which was registered in the first quarter of 2009. Yet the Reagan recovery, starting in the first quarter of 1983, rushed along at quarterly growth rates (expressed as annual rates of change) over the next six quarters of 5.1%, 9.3%, 8.1%, 8.5%, 8.0% and 7.1%. Not until the third quarter of 1984 did real quarterly GDP growth drop below 5%.“

I’ll bet you dollars to donuts that if we go back and read the newspapers of the 1981-82 downturn, the negativity would be as prolific as it is today.

But there is a silver lining in all of this, as Buffett points out: “Buy when people are fearful.”

That’s what I did last December. I bought stocks.

I was a nervous wreck putting cash back into the market. . . but I look like a genius now.

Truth be told, I was just plain lucky.

As Grant concludes. . .

“I promised to be bullish, and I am (for once)-bullish on the prospects for unscripted strength in business activity. So, too, is the Economic Cycle Research Institute, New York, which was founded by the late Geoffrey Moore and can trace its intellectual heritage back to the great business-cycle theorist Wesley C. Mitchell. The institute’s long leading index of the U.S. economy, along with supporting sub-indices, are making 26-year highs and point to the strongest bounce-back since 1983. A second nonconformist, the previously cited Mr. Darda, notes that the last time a recession ravaged the labor market as badly as this one has, the years were 1957-58 -after which, payrolls climbed by a hefty 4.5% in the first year of an ensuing 24-month expansion. Which is not to say, he cautions, that growth this time will match that pace, only that growth is likely to surprise by its strength, not weakness.”

And that is my case, too. The world is positioned for disappointment. But, in economic and financial matters, the world rarely gets what it expects. Pigou had humanity’s number. The “error of pessimism” is born the size of a full-grown man-the size of the average adult economist, for example.

For once in my investment career, I hope Grant is correct.

Party on, Jim!

![]()

Brian Hicks

Subscribe to the FREE Wealth Daily Newsletter HERE.

Maverick investment guru Jim Rogers, who has a pessimistic view on the state of developed economies and what is being done to counter the recession, is not buying into equity and commodity markets at this stage. Rogers attributed the recent run-up in equity markets to the various stimuli packages released around the world. On commodities, Rogers said he owned base metals and — among precious metals — gold but wouldn’t buy those at current levels, given the recent rally in commodities.

The long-term call on the dollar was that it would be “a disaster,” Rogers said, but added that he was positive on the Japanese yen.

Rogers, who last year shifted base from the US to Singapore, said he was long-term positive on Chinese equities. Among other emerging markets (EMs), Rogers said he wouldn’t buy anything in the Russian market, though Brazil, which was a natural resource-rich country, looked better managed now, while the Indian stock market looked expensive due to its recent rally. “Most EMs have been very strong in the past year after the collapse or the fall of 2008, most EMs have gone up a lot. I don’t like to buy anything that has gone up a lot,” he said. “I am very worried about the Western economy, I don’t think that the problems are solved in the West and if you start seeing more problems in the West, it is going to have an effect on most markets around the world as certainly some of the EMs. The EMs, which have a lot of raw materials or commodities, would probably do better than the others but again even they will be affected if we have more problems in the West.”

Here is a verbatim transcript of Jim Rogers’ exclusive interview on CNBC-TV18. Also watch the accompanying video.

Q: It has been a big run for equity markets first and foremost, what have you made of it?

A: The governments around the world are pouring huge amounts of money into the world economy. It has to go somewhere and the easiest, best way for it to go is in the financial markets.

Q: It has also concomitant with a big fall in the dollar and there is a call now for greater weakness in that currency, would you concur?

A: I am not optimistic about the US dollar long-term. In fact, the US dollar long-term is going to be a disaster. However, there are many people in the world right now who are terribly pessimistic about the dollar including me, many people have sold the dollar short, and so it would not surprise me if there were not a big rally. If a rally comes, I plan to sell that rally but I am not selling the dollar down here.

Q: What is your call on the strength that the yen has seen and the kind of a nervousness that most of those export-oriented markets are exhibiting? Where do you see it headed from here?

A: I own the yen so I am very pleased to see the yen going higher. Various things are happening in Tokyo and Japan. They are the second largest creditor nation in the world plus their government has given big incentives for people to bring the yen back into Japan. Billions of yen have been invested outside of Japan and now there is good reason for them to bring it back.

So you have a new government [in Japan], you have incentives to bring the yen back, you have the carry trade unwinding, there are many reasons for the yen to continue to go higher. I own the yen and I hope it does go higher.

Q: What about the base metals, we have seen a lot of volatile moves across most of those base metals, where do you see them headed from here?

A: Base metals have had a huge rally, as you have pointed out. I know I wouldn’t be buying the base metals right now, I do own base metals — I am not selling base metals — but I don’t like to jump on a train, which is moving at a rapid rate. Base metals have gone up a whole lot in the last nine, 10 months. So I am not doing anything except for watching.

Q: You have tracked and watched the Chinese market as well for many years, there is concern on where that market might be headed and why it is lagging the performance of others?

A: I would hardly call it lagging the performance of others. The Chinese market doubled between the fall of last year and August of this year. So it was one of the strongest markets in the world, if not the strongest. It has calmed down in the last month or two but anything that doubles in ten months should slow down and consolidate. Who knows where it is going to go from here but I own Chinese shares, I have not sold any of my Chinese shares because longer-term I am very optimistic about China.

Q: From the emerging and Brazil, Russia, India, China (BRIC) basket, what would be your top pick then right now in terms of markets?

A: I wouldn’t buy any of them. I would never buy the Russian market. The BRIC is some kind of an artificial thing, which some marketing people put together. I would not ever buy the Russian market. I own China. Brazil is a natural resource-based economy and it is being better managed these days and it has been in the past. So Brazil probably has a good future though I don’t own any Brazilian stocks. The Indian stock market has run up a lot in the last year or so. So I don’t think I would buy it either. I am not buying shares anywhere in the world as we speak.

Q: What about gold?

A: I own some gold and I am optimistic about the price of gold but I don’t think I would buy it either. The gold is near its all-time high, I think I would rather buy silver for instance if I had to buy a precious metal. However, I am not buying either at the moment. I certainly would not sell any precious metals — if they go down, I plan to buy more and maybe a lot more.

Q: How is the fund flow situation looking at least for our markets — there is a lot of appetite from foreign investors but in general how is the mood looking across that front?

A: I am not buying any emerging markets (EMs). If I were to buy EMs — I had recently gone to Sri Lanka to look at it as an EM. I have not bought anything there but the Sri Lanka market has been extremely strong in the last year. Most EMs have been very strong in the past year after the collapse or the fall of 2008, most EMs have gone up a lot. I don’t like to buy anything that has gone up a lot. I am very worried about the Western economy, I don’t think that the problems are solved in the West and if you start seeing more problems in the West, it is going to have an effect on most markets around the world as certainly some of the EMs. The EMs, which have a lot of raw materials or commodities would probably do better than the others but again even they will be affected if we have more problems in the West.

Get ready for next month. I always find myself approaching October with a little trepidation. As soon as all those 3rd quarter earnings (or lack thereof) start coming in we could be in for quite a shock. It just seems that surprises of the worst kind show up in the stock market in Octobers past (especially the most recent one).

It doesn’t take much searching for one to start to question the “green shoots” recovery. Over at John William’s web site (www.shadowstats.com) the unemployment numbers are over 20% and climbing. The Baltic dry index certainly does not show a recovery in world wide shipping. Finally the S&P 500 p/e ratios are higher than before the dot com bubble in 1999 (and this in spite of all the stimulus money thrown into the economy).

With all this news what is a boy to do other than head for the bunker with bullets, bullion and beans? Of course I do not think this is TEOTWAWKI. Life will go on and the world will keep spinning. But what to do about this dread in the pit of my stomach as I get nearer and nearer to turning another page on the calendar – to the dreaded investors month of OCTOBER?

Perhaps it is time to take a little defensive action. Nothing as drastic as the 4 – B’s listed above mind you. Here are my simple recommendations:

1. Move up those stop losses. If you do not use stop losses then shame on you. Tighten them up. Maybe as close as 90% to 95% of your stock’s present market value. Sure you might get stopped out on a small dip before a big run up but how many of you are wishing you had done so last October? If the market continues to run up then keep moving the stop loss orders upward. If it drops hard and fast you can thank me later. The market just seems a little toppy to me but what do I know?

2. If you have precious metals in your possession then hold then as a core investment. Right now a 20% to 25% allocation is not too high in my opinion. If you do not have that core investment then now might be the time to buy some and get ready to buy more if there is a short, sharp, quick drop. Decide where you would like to buy in and write it down. Your emotions will get the best of you in a wild ride down. Make a plan and stick to it.

3. Don’t be afraid to lock in profits. If you have a good profit never be afraid to sell a stock and lock it your gains. Maybe sell half and let the other half ride with a stop loss order trailing it closely. Remember that it is not a profit until you sell. Invest for the long term but never marry a position. (You will also need some cash for item #4.)

4. Get ready to buy if the bottom falls out. Look at a few good energy stocks. I like natural gas producers with large reserves. Look at a few mining stocks. There are several good picks out there right now. Maybe even look at a few defense stocks as I smell trade wars on the horizon. See how far they fell last October. Look and see how they recovered. Study their earnings and see what “P” you would be willing to buy at based on their “E” with a realistic P/E ratio. Get those stink bids ready. Remember to have a little speculative investment cash ready to jump in just in case those targets are met. Decide where your buy in price is and write it down. If they are good stocks be bold with a LITTLE speculative capital.

Inflation is already baked into the cake in the long run. The new Japanese prime minister is already talking about making the USA borrow in yen instead of USD. If this ever comes to pass then it will be harder for the USA to inflate their way out of this mess. In the short run deflation is still a possibility and a little cash is prudent. HOWEVER, start building your precious metals positions if you have not already done so. This time is a blessing and will not last forever.

Wishing everyone a very dull October,

Larry LaBorde,

Silver Trading Company

Larry lives in the occupied South with his wife Puddy and sells precious metals at the Silver Trading Company. Larry can be contacted at llabord@aol.com. You can view his web site at www.silvertrading.net.

To order advance copies of Larry’s new book, “Investing Without a Net” just go to his website at www.silvertrading.net and scroll down to the middle of the home page and click on the link.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair