Daily Updates

Quotable

![]() “The Belief that man is outfitted with an immortal soul, differing altogether from the engines which operate the lower animals, is ridiculously unjust to them. The difference between the smartest dog and the stupidest man—say a Tennessee Holy Roller—is really very small, and the difference between the decentest dog and the worst man is all in favor of the dog.” – H.L. Mencken

“The Belief that man is outfitted with an immortal soul, differing altogether from the engines which operate the lower animals, is ridiculously unjust to them. The difference between the smartest dog and the stupidest man—say a Tennessee Holy Roller—is really very small, and the difference between the decentest dog and the worst man is all in favor of the dog.” – H.L. Mencken

![]() FX Trading – Starting to Heat Up South of the Border

FX Trading – Starting to Heat Up South of the Border

Yesterday, Mexican industrial production slid by 7.3% year-over-year in August, worse than the expected 6.2% decline and the previous drop of 6.5%. And in a sign that companies aren’t yet ready to apply capital in this economy, gross fixed investment plunged by more than 14% in July when estimates were calling for a drop of 11-12%.

Friday, Mexico’s central bank wraps up a meeting on monetary policy. They’re expected to sit tight with rates at 4.5%. What’s on their minds?

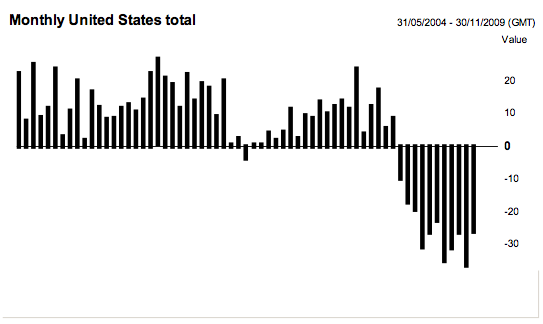

First, the continued poor economic data isn’t sitting well. Keep in mind 80% of their exports are sent to the United States. And while there may be signs of recovery in the US, America is expected to lag the rest of the world and the US consumer is still retrenching. The most recent monthly data shows Mexican imports to the US down nearly 30% year-over-year.

Mexican exports to the US, year-over-year percent change

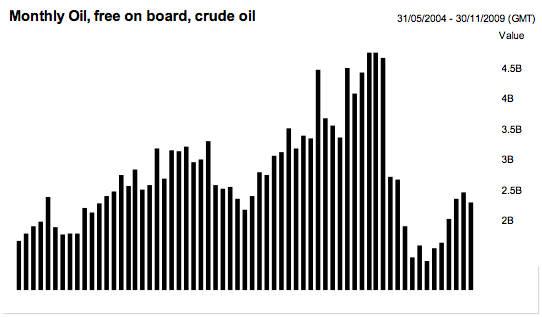

On top of that, crude oil revenues are down. And it’s no secret that Mexico makes a living on production and distribution of crude. Relatively low prices and lackluster demand is an awfully discouraging combo. Mexican government, like many governments around the world, is left scurrying around to compensate for lost revenues.

Mexican exports of crude oil

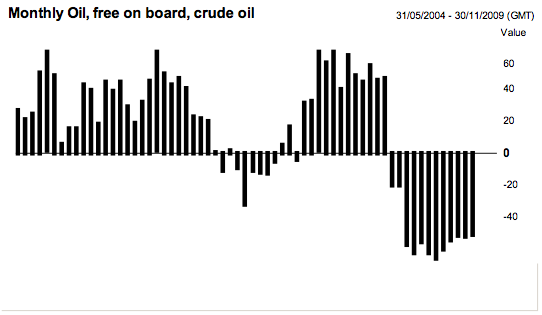

Mexican exports of crude oil, year-over-year percent change

Money sent back into Mexico from Mexicans working in the US or abroad continue to show notable year-over-year declines.

It’s obvious looking at these charts that there’s been a major setback to Mexico’s economy in the wake of global credit crisis.

That is why there are important reforms being weighed by Mexico’s politicians. The lower house is currently chewing on a proposal that would institute a new 2% sales tax

on pretty much everything. Time is winding down but it is expected some alternate proposals based instead on spending cuts will surface before next week’s deadline to make a decision and pass it on to the Senate.

Are these proposals, if any make it through, going to save Mexico’s economy? It’s not likely. But what is being hoped for is that taking some type of action can postpone potentially worse conditions long enough for the global economy and business as usual to get back on its feet.

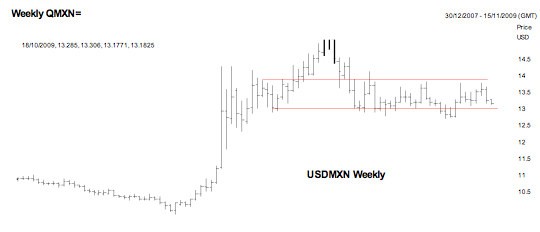

As for the peso, at least it hasn’t been the self-proclaimed “hindrance on the economy” as rising currencies of other nations have become. Nope – the Mexican peso has been pretty much stuck trading sideways for the last couple months, rising and falling from support and resistance.

It’s nearing support again. And if it’s judged on its fundamental backdrop then the likely move for USDMXN is for the peso to weaken and this pair to bounce back up towards resistance.

But, if the US dollar falls into crisis-mode (or is at least viewed that way by traders) then the peso could find default strength and this pair could blow through support fairly easily. If it does, and the anti-dollar move is sustained then the pent-up momentum in USDMXN could send the pair lower in a hurry.

John Ross Crooks III

Black Swan Capital LLC

Ed Note: Jack Crooks will be speaking at the:

The Money Talks All Star Trading Super Summit

Saturday, October 24, 2009 -The Sheraton Vancouver Wall Centre

Click HERE for the Speaker Lineup and to REGISTER if you want to take advantage of this Event.

Click on the Banner for a Black Swan Special offer.

Register HERE for the FREE Daily Currency Currents Newsletter.

Black Swan Capital is an independent minded currency advisory firm established to provide subscription-based services to help retail and institutional clients consistently attain above average profits trading and investing in both forex and currency futures markets. We tell our Members when to enter and exit and why. HERE for more information.

Our commitment is to deliver well researched trading recommendations that our clients understand and can efficiently execute through their brokers. We outline the reasons to enter a trade and define the risk. But our Members must understand there is a substantial risk of loss trading in forex (off-exchange retail foreign currency) and currency futures markets.

Register HERE for the FREE Daily Currency Currents Newsletter.As a subscriber to Currency Currents you stay tuned-in to our current global-macro view and our analysis of key investment themes driving currency prices. Nothing is off limits to us in this free-wheeling look at the markets. Some days you’ll receive ramblings on trading psychology, while other days we may take an academic approach in explaining esoteric economic issues. Ultimately we have one goal in mind: to help you get a handle on the key investment themes driving global capital flow. Because if you know where the money is going, it increases the probability that yourposition in the market will be a profitable one.

Businesses are still laying off employees, those still employed are working more hours for less pay, home foreclosures remain near record levels, consumer credit is still plunging, and defaults on commercial real estate are increasing. However, the stock market has gained 53% from spring lows, Wall Street banks are reporting record again and oil prices have more than doubled since last fall. What’s going on? How can Wall Street enjoy a strong recovery while the rest of America suffers? Will commodity markets followWall Street or Main Street?

Since last summer, we have held a negative view on most commodity markets. We believed recoveries on both WallStreet and Main Street were required before the majority of commodity markets could enjoy a demand resurgence strong enough to support sustained bull markets. However, the Continuous Commodity Index reached a new thirteen month high this week and gold pushed into record territory. Is it possible commodity markets could experience major bull moves while the world’s two largest economies (Japan and the US) remain mired in stagnation and/or recession? To help answer this question, we must compare the current recession to past recessions. In all recessions since the Thirties, the Federal Reserve was the primary culprit. When inflation threatened to destabilize the economy, the Federal Reserve raised interest rates and restricted credit to curb demand, which cooled economic expansion. When inflation subsided, they reduced interest rates and made credit easy again. Economic growth always returned following Fed easing. However, this is a recession of a different kind.

A brief excerpt of the lengthy daily internet comment by Richard Russell of Dow theory Letters. One of the best values anywhere in the financial world at only a $300 subscription to get his report daily for a year. HERE to subscribe.

“I wouldn’t want to be a member of the Federal Reserve Board of Governors these days. It’s been over a year since the Lehman Brothers collapse (Sept 15, 2008), yet despite all the unprecedented actions taken by the Fed in the interim (bailing out banks, slashing short-term interest rates to 0%, and printing over a trillion dollars in new money), the US economy appears to be on extremely shaky ground.” From Fred Hickey’s great High-Tech Strategist.

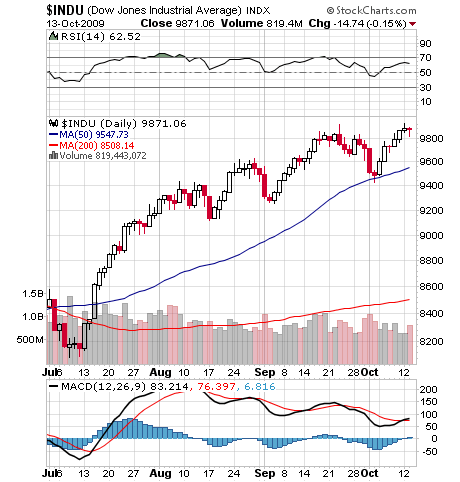

Below I show two charts.The first is the D-J Industrial Average, which closed last Friday at a new recovery high of 9864.94. The second chart shows the D-J Transportation Average which failed by a wide margin to confirm the Industrials.

Ed Note: Charts to close of business 10/13/09

For the benefit of my many new subscribers, I want to explain the rationale of confirmations. The Industrial Average reflects the manufacturing capabilities of the nation. The Transportation Average reflects the sales and shipping capabilities of the nation.

If you manufacture, but you are not selling or shipping your products, that’s an obvious negative. If you’re selling and taking orders to ship products that are not being manufactured fast enough or in large enough quantities, that’s a clear negative. When manufacturing is going well and the products are being sold and shipped, that’s a healthy combination. All of which explains why when both the Industrial and Transportation Averages are rising to new highs together, the situation is both healthy and bullish.

Those are the fundamentals. Technically, and this has been time-tested, when one or the other Average breaks to new highs or new lows for the move, and the breakout is not confirmed by the other Average, it is usual for the prevailing direction of the market to be halted or reversed.

To bring it all to the present, we now have Industrials at a new high for the move, but the Transports have failed to rise above their comparable high of 4015.16. Transports closed last Friday at 3875.32, which was 140 points below their prior peak of 4015.16. As a rule, the closer together (in time) a confirmation occurs, the more authoritative. The longer it takes for a confirmation, the less important the final confirmation.

The 84 yr. old writes a market comment daily since the internet age began. In recent years, he began strongly advocated buying gold coins in the late 1990’s below $300. His position before the recent crash was cash and gold.

There is little in markets he has not seen. Mr. Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late-’50s through the ’90s. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974. He loaded up on bonds in the early 80’s when US Treasuries where yielding 18%.

As we all know, these are treacherous times for investors. The US stock market has lost over 40% of its value. Commodities, currencies, bonds, have all seen unprecedented volatility. The dollar, against all reason, has rallied, and many foreign securities markets have declined substantially.

Investors have begun to fear that there is no shelter from the storm.

I believe that opportunity is in abundance. My investment philosophy, and that of my firm, Euro Pacific Capital, is based on a number of strongly held, core beliefs:

…..read more HERE.

Market Buzz

While Friday’s session ended down, Canada’s main stock index rose sharply on the week, powered by four consecutive days of triple digit gains as firm commodity prices and what was trumpeted as new signs of a global economic recovery helped fuel a broad rally led by key energy players.

Once again, it does appear the rally has gotten ahead of itself particularly in reference to a report published this past Friday by Gluskin Sheff’s well regarded economist, David Rosenberg.

Rosenberg has done a little number crunching on the market “recovery” and concluded that on an operating basis, the trailing P/E multiple on the S&P 500 has expanded a massive 10 points from the March lows to stand at 27.6x. His research suggests, historically when the economy is taking the turn away from contraction towards expansion, which indeed was the case in Q3, the trailing P/E multiple is 15x or half what it is today.

It is interesting to note that the last time the multiple was this high was back in March 2002. Over the next several months, the S&P 500 proceeded to lose just under 35 per cent of its value. Yes, the macro environment today differs from that in 2002 as both interest rates and inflation remains lower. But overall, the rising multiples should not be ignored.

So, what should one do in this environment? Continue to look for companies with low multiples relative to their growth prospects. In fact, this past week our long-time clients were rewarded with a huge jump in the shares in one company from our Small-Cap Universe (www.keystocks.com) that has long possessed solid fundamentals.

The company, China Agritech, Inc. (CAGC:NASDAQ), a China-based manufacturer and distributor of liquid and granular organic compound fertilizer, saw its shares jump over 40 per cent on Friday after it announced it was increasing its annual net revenue and net income guidance for the year ended December 31, 2009.

The company is now expecting net revenue for the year 2009 to be as high as $70 million versus the previous guidance of over $60 million. The revised guidance for net income is approximately $12.5 million compared with the previous net income guidance of $9.5 million. Diluted earnings per share are now expected to approximate $1.88, based on the current average number of diluted shares outstanding. The new guidance represents almost a 55 per cent increase for net revenues and around a 45 per cent rise for net income over the year 2008 results.

Of note, I will be speaking at a Calgary Small-Cap Conference (www.smallcapconference.ca) this coming Thursday, October 15th, at 6:00pm at the Coast Plaza Hotel & Conference Centre and encourage our clients or other interested parties to register online and attend.

Looniversity – Paper Profits – Unrealized Gains & Losses

An unrealized loss occurs when a stock decreases after an investor buys it, but he or she has yet to sell it. If a large loss remains unrealized, the investor is often hoping the company’s fortunes will turn around and the stocks worth will increase past the price at which it was purchased. If the stock rose back above the original price, then the investor would have an unrealized gain for the time he or she still holds onto the stock.

For example, say you buy shares in ABC Company at $10 per share and then shortly afterwards, the stock’s price plummets to $3 per share, but you do not sell. At this point, you have an unrealized loss on this stock of $7 per share. Let’s say the company’s fortunes then shift and the share price soars to $18. Since you have still not sold the stock, you’d now have an unrealized gain of $8 per share.

Gains or losses are said to be “realized” when a stock is sold. This is especially important from a tax perspective as, in general, capital gains are taxed only when they are realized. Unrealized gains and losses are also commonly known as “paper” profits or a loss, which implies that the gain/loss is only real “on paper.”

Put it to Us?

Q. I recently placed an order through my discount broker and she asked whether or not my order was an “all or none” or “any part” order. I told her it was a “regular order” and we proceeded. Fill me in on what she was referring to.

– Anne Urchuck; Calgary, Alberta

A. Good question, Anne. An “all or none order” is one under which the trader is restricted to executing the total number of shares specified on the order at one time or none at all. For example, if your order is to purchase 1000 shares of Company XYZ at $1.00 and there are only 500 shares available at $1.00, you will not get a partial fill (500 shares). Many investors use this order to prevent the acceptance of partial fills and avoid paying multiple commissions on separate fills days.

An “any part order” is the opposite of an all or none order. Under this order, you agree to accept as much stock as can be obtained up to the full amount of your order.

KeyStone -Why Subscribe?

- First coverage on high growth, profitable stocks, trading at low prices

- Independent and updated BUY/SELL/HOLD Stock Reports

- Unsurpassed 9-year track record of uncovering great small caps with strong fundamentals

- About Keystone Financial HERE – Go HERE to subscribe

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair