Daily Updates

It appears gold mania is spreading, and if this press release by the US Mint is any indication, it has hit the broad population. As a result, the administration is taking prompt “corrective” steps:

“The United States Mint will not offer the following products in 2009: the one-ounce American Eagle Silver Proof Coin; the one-ounce American Eagle Silver Uncirculated Coin; the American Eagle Gold Proof Coins (all weights, as well as the four-coin set); the one-ounce American Eagle Gold Uncirculated Coin; the United States Mint Annual Uncirculated Dollar Coin SetTM, which also includes a one-ounce American Eagle Silver Uncirculated Coin; and the American Eagle Platinum Bullion Coins (all weights).

Because of unprecedented demand for American Eagle Gold and Silver Bullion Coins, the United States Mint suspended production of 2009 proof and uncirculated versions of these coins. All available 22-karat gold and silver bullion blanks are being allocated to the American Eagle Gold and American Eagle Silver Bullion Coin Programs, as mandated by Public Law 99-185 and Public Law 99-61, respectively. Both laws direct the agency to produce these coins in quantities sufficient to meet public demand. The proof and uncirculated versions of the American Eagle Gold and Silver Proof Coins are not mandated by law.”

The Mint does promise to promptly reevaluate the supply/demand curve for gold and to allow the public to avoid having to keep its holding in the dollar:

The United States Mint is working diligently with current and potential blank suppliers to increase the supply of bullion coin blanks, so it can offer to the public the proof and uncirculated versions of American Eagle silver, gold, and platinum coins in 2010.

….more HERE by Tyler Durden

Also….

THE DYNAMICS OF THE GOLD & SILVER MARKETS?….EXPLOSIVE!

by Adrian Douglas

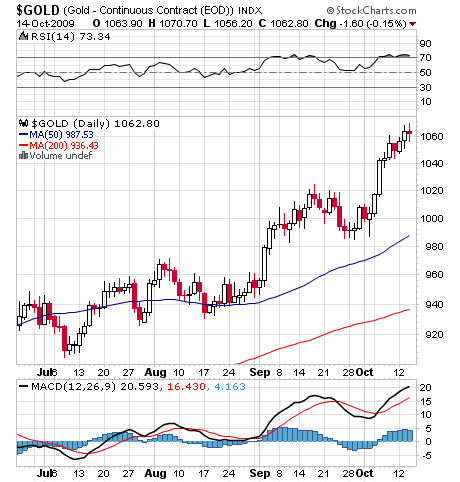

This week gold closed above $1000/oz for the fourth consecutive week and made another all time weekly high close. But the top-callers have come out in their droves declaring that gold is in a bubble that is about to burst, and because the recession has been declared as over there is no reason to hold such a safe-haven asset. All that is nonsense and I will explain why. The dynamics unfolding in the gold and silver markets are nothing short of explosive.

The dynamics are different for gold and silver so I will start by discussing gold.

Gold is a unique substance. It is about the only thing on the planet that is bought and stored and never consumed. Almost all the gold ever mined in history still exists above ground. The purpose of gold is to act as a store of wealth. This singularity of gold makes it susceptible to a scam that was first perpetrated by the goldsmiths in the 16th century. The goldsmiths realized that customers would buy gold and leave it for safe keeping in their vault. This meant that they could show the same gold bar to many customers and sell the same gold bar many times over. This was the early form of the concept of fractional reserve banking where banks only retain 10% of the money on deposit gambling that no more than 10% of the money will ever be called upon to be paid out.

This basic scam is at the center of modern gold market manipulation. Paper substitutes for gold are sold instead of real gold through derivatives, futures, pooled accounts, ETF’s, gold certificates etc. I estimate that each actual physical ounce of gold has been effectively sold 20 times over or more. To be able to maintain this Ponzi scheme some real gold is required because some investors or jewelers demand real gold. For the scam to be sustained there must always be plentiful physical gold for those who want it. This physical supply has been met from mine supply and central bank leasing and selling. The market is in effect a giant inverted pyramid with a huge paper gold market being supported above a small amount of physical gold at the tip of the inverted pyramid. The scam can continue until there are indications of a shortage of physical gold. If the twenty or so claimants of each oz of real gold demand their gold then there is the potential for a squeeze like has never been seen before in history.

To lend support to the idea that all the gold in the world has been sold several times over I cite the case of Morgan Stanley who were sued in 2005 for selling non-existent precious metals to their customers. They even had the audacity to charge storage fees! They settled the class action suit out of court but no criminal charges were ever filed against them. If Morgan Stanley was doing this you can bet that it is the tip of the iceberg. As further evidence just look at the monster OTC derivatives market. Standing at approximately $1,000 trillion it is multiples of the liquidated value of all the assets in the world and all currency in the world. Clearly derivatives must be selling some sort of claims to assets that can not be fulfilled because there are not enough underlying assets.

The price discovery of gold has been almost exclusively achieved through the shuffling of paper gold promises between investors and bullion banks on the COMEX with very little real gold ever changing hands. The situation is changing. Some big entities are now demanding physical gold. These entities are almost certainly countries not individuals, such as China, Russia, India, Venezuela, Iran the Gulf States to name but a few. This demand for real gold, instead of paper substitutes, is putting a strain on the gold market. Paul Walker, CEO of GFMS, recently said the price of gold was going up because of “large lumpy transactions in a market with a degree of illiquidity”. Roughly translated this means that there are large demands for physical metal which the market is struggling to meet. That is a Cartel apologist’s limp wristed reference to the explosive dynamics that I am defining!

The supply that feeds the bottom of the inverted pyramid to support the gold price suppression via a paper market is drying up. Mine supply has been declining for almost a decade and this year central banks became net buyers of gold for the first time in 20 years. The stress in the physical market is starting to show to those who are paying attention. For example, the London PM Fix is coming in at historic highs day after day, the contango in the futures market has contracted dramatically, the US mint is routinely suspending production due to shortages of metal. But most importantly we are seeing astute investors display a growing preference for real bullion. A couple of months ago Greenlight Capital, the large hedge fund, switched $500 million of investment in GLD to physical gold bullion. The supposed gold holding of GLD has not grown to a record high despite a record high gold price. Apparently Germany has requested that its sovereign gold held by the NY Federal Reserve Bank be returned to Germany. Hong Kong has requested the same of the Bank of England that stores its sovereign gold. Robert Fisk, a respected journalist for the UK’s Independent newspaper, reported this week that the Arab oil producing states, Japan, Russia and China have been holding secret talks to replace the dollar as the international reserve currency and as an accounting unit for trade. He reports that the basket of currencies they propose instead of the dollar would include gold! If gold is going to regain its monetary role then you can understand why those in the know want actual physical bullion. There are some very real and significant signs that a run on the bank of the Gold Cartel for physical gold is commencing.

Meanwhile most investors and analysts are focused only on the net short position of the Commercial traders on the COMEX which has reached an historically high level, and has in the past signaled the onset of a major correction. However, such market observers are only watching a side-show of the main event. The main event is all about a growing tightness in supplies of gold in the physical market. I don’t think the Commercial net short position of 800 tonnes is that important; what is important is that the world’s stockpile of 140,000 tonnes may have been sold several times over. In all likelihood half of the supposed 30,000 tonnes of Central Bank stockpiles have been sold at least 20 times over. The gold short position could well be 300,000 tonnes (15,000 times 20) against a total world inventory of only 140,000 tonnes, much of which is not available to the market. Could you think of a more bullish scenario? If you think that such business practices could not be tolerated I can hold up the example of the airlines who regularly and knowingly oversell the seats on their flights expecting that not all passengers will show up. Bullion bankers oversell their inventory of gold knowing that only 10% of the customers will ever ask for it, just as the goldsmiths did.

One can not discuss the gold market in isolation as it is linked to the dollar and Treasury debt. The major impetus behind the suppression of the gold market was to maintain a strong dollar despite massive over-issuance of the currency. This has allowed the US to live beyond its means because the rest of the world accepts the home-made funny money as payment for goods and services! Lawrence Summers, in a study he made when he was a Professor of Economics at Harvard titled ‘Gibson’s Paradox and the Gold Standard” showed that in a free market gold and real interest rates move inversely to each other. However, since 1995 the US has had low gold prices and low interest rates. In the absence of a Gold Standard this could only have been achieved by surreptitiously fixing the gold price through market manipulation. This was the essence of the “strong dollar policy” of Robert Rubin, the mechanism of which was never explained to the public.

The dynamics of the silver market are different. About 90% of physical silver production is used for industrial applications. Only 10% is purchased for investment. Clearly paper substitutes for silver can not be used in industrial processes. The investment market is suppressed by paper silver substitutes as described above with respect to the gold market. It is this market, specifically the COMEX futures exchange, which controls the price of silver. The very low price of silver over the last 30 years has encouraged large holders of silver to dishoard it. After all, who wants to pay costly storage fees for something that is of low and declining value and very bulky to store? This dishoarding has filled the gap between silver production and industrial demand which runs at over 200 million ozs annually. Much of the investment demand has been met with paper substitutes and scams that are variations on the one that was perpetrated by Morgan Stanley described above. Because of the suppression of the price of silver it has been uneconomic to recycle most industrially used silver, with the exception of that used in the photographic process. This has meant that most industrially used silver finds its way into land fills. All the existing above ground silver is now less than 1 billion ozs. Considering that just SLV ETF alone claims to have over 250 million ozs of silver it is reasonable to estimate that investors have been sold something of the order of 5 billion ozs of silver. But how much is supported by real physical silver? If the same oz of silver has been sold 20 times over, as per my estimate in gold, then only 250 million ozs of investment silver bullion exist. This means that 4.75 Billion ozs of silver could potentially be demanded in a market where only 1 billion ozs of stock pile exists and mining supply is already oversubscribed to the tune of 200 million ozs annually. One can probably add to this picture that investors who can not easily find physical gold will come looking to buy physical silver. What is even more bullish is that the industrial users will not sit idly by watching a manic silver grab. They will join in the fray because they can not remain in business unless they have silver inventory. They will try to stockpile at a time of acute shortage.

The dynamics of the gold and silver markets are bullish beyond anyone’s wildest dreams. This is no longer about whether the commercials will knock down the price by selling more contracts short. This is about a lot of market participants who have been content in the past to hold precious metal paper substitutes who now increasingly will want to own real bullion. This has been happening slowly but will gather pace like a rolling snow ball. Because in the last 30 years most investors have trusted the brokers, dealers and bullion banks to actually have the metals that have been sold there has been no “run on the bank”. This is now changing. Many indications point to significant supply stress building.

Why are the entities that hold the largest short positions on the planet custodians of the bullion depositories for the largest ETF’s? That’s like putting a sex offender in charge of the Children’s Day Care Center or Bernie Madoff in charge of your company pension fund! The argument against holding physical bullion yourself has always been the risk it might get stolen while in your possession. However, the risk of holding bullion substitutes might be that it has already been stolen or never existed!

The precious metals market is now akin to a game of musical chairs with perhaps only one chair for every 20 players. It might be prudent to follow in the footsteps of Germany, Hong Kong, China and Greenlight Capital and get your chair BEFORE the music stops.

If the physical markets for precious metals lock up due to shortages then the short squeeze will be of epic proportions; it will be something to tell your grand children about. Needless to say it will be a better story for your grandchildren if you are on the right side of the trade!

Adrian Douglas

October 9, 2009

www.marketforceanalysis.com

Adrian Douglas was born in 1957 in England. He graduated from Cambridge University in 1980 in Natural Sciences. He worked for 20 years in the Oil & Gas Industry with Schlumberger where he reached senior management positions in Marketing and Sales. Adrian established a highly successful consultancy business specializing in pricing and marketing called InnovoMark -Innovative Marketing- www.innovomark.com. He developed unique methodologies related to pricing and marketing which have been incorporated into proprietary training programs.

The study of commercial enterprise pricing led to a deep interest into the market pricing mechanisms of financial assets. As a result Adrian developed a unique algorithm and methodology for analyzing financial futures markets, and in particular identifying appropriate entry and exit points. The technique has been named “Market Force AnalysisTM” (MFATM) and a patent is pending. The market calls that Adrian has made using his proprietary MFATM have attracted much attention. In particular, John Embry of Sprott Asset Management, spoke very favorably of the technique on ROBTV on Canadian Television.

Adrian has made almost a daily contribution to the website www.lemetropolecafe.com commenting on precious metals and the financial markets in general. Many of his specialized articles that have been published at www.lemetropolecafe.com can be found in the “published articles’ section.

This brief comment from the Legendary Trader Dennis Gartman. For subscription information for the 5 page plus Daily Gartman Letter L.C. contact – Tel: 757 238 9346 Fax: 757 238 9546 or E-mail:dennis@thegartmanletter.com HERE to subscribe at his website.

As for gold, we remain long of gold in Sterling terms, in EUR terms and in US dollar terms. As we have long said, the great bull markets in gold are currency agnostic; that is, the great bull markets in gold see gold rise in terms of any and all currencies. This is one such bull market. Investors around the world are increasingly disdainful of currencies and are increasingly enamoured of gold, and why not?

Government… especially intrusive, left-of-centre government… always puts into place policies that diminish the value of their currencies, thus increasing the “value” of gold. We are not Gold Bugs here at TGL, but we are sufficiently dismayed by government actions… especially those of the Obama Administration… to accept the thesis most often promoted by the Bugs that “Gold is a store of value.” IT is that, and really very little more, but for now, that is sufficient to keep us long.

Click HERE for larger image of long term chart from 1982 below:

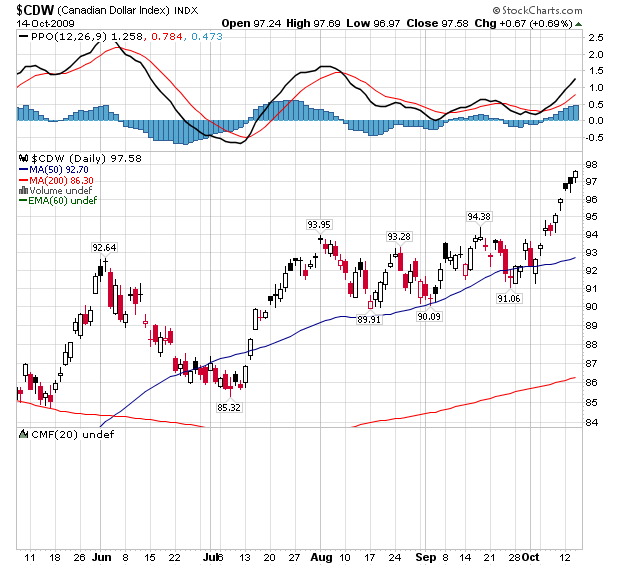

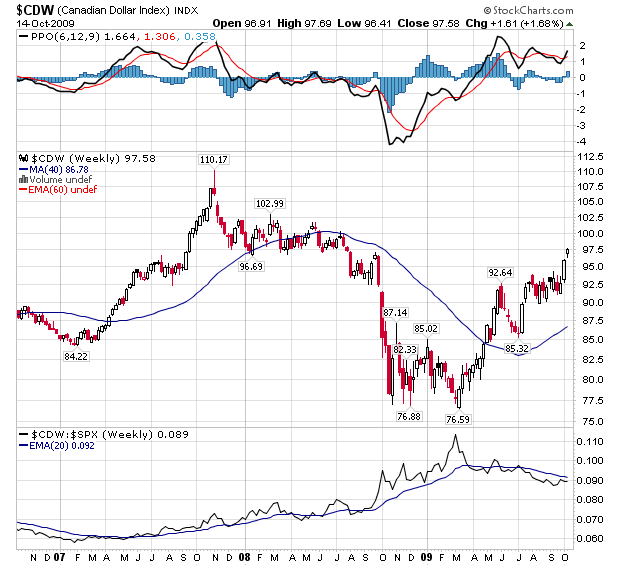

Canadian Dollar – Moving even further one, the Canadian dollar continues to soar relative to the US dollar… along with the Aussie and the “Kiwi” dollars. Landing here in Toronto last evening and finally catching a bit of the news, we listened as Prime Minister Stephen Harper said, regarding his currency, that he does in fact agree with the Bank of Canada’s recent assessment that a “too rapid” rise in the country’s currency is a risk.” What is important here is that he said “a too rapid rise.” He did not say that a quiet, sustained rise shall put the country at risk, but instead simply argued that volatility and sharp, severe bouts of strength can. Mr. Harper further said that while some of the recent strength in the Canadian dollar reflects the reality of an economy that is strengthening, “obviously, the value of the Canadian dollar is a risk to recovery” if it is too rapid. He said:

I don’t think it’s a risk to choking off the recovery, but if it goes up too rapidly it does have difficult effects on our economy…. The governor of the Bank of Canada has been clear that a too rapid rise in the dollar is a risk to our recovery.

From Friday’s analysis on Canadian Dollar:

The Canadian dollar soared higher Friday and it remains firmer this morning despite the fact that Canada’s markets are all closed for Thanksgiving Day there. Over the years we’ve learned the very hardest of ways that when Canada’s markets are closed the C$ can have, and often does have, a rather erratic trading conditions. We cannot and will not be surprised to see the usually docile C$ trade in a much wider range today. But then again we shall not be surprised to see the C$ trade very quietly and within a very narrow range either. Forewarned is forearmed. However, what is important to note that Friday’s strength was properly predicated upon decidedly positive economic news there as the unemployment rate fell from 8.7% to 8.4% and as Canada’s correlative to our non-farm payrolls actually showed an increase of 30,600 jobs added in September. Bay Street had been looking for a net loss of jobs, so this figure caught everyone off, sending the C$ sharply higher as the market began to talk about the fact that the BOC might begin to raise rates, following Australia’s lead, sooner rather than later. Recall, however, that the Bank said that its intention is to keep rates at the short end steady through mid-’10, and until we hear otherwise from the Bank’s leaders, we’ll “go” with what they’ve said in the past. Even so, this was an impressive statistic, and although it is not perfectly correlative, given that the US’ population is approximately 9.1 x’s that of Canada’s, this is the rough equivalent of US non-farm payrolls having rise 278,600 in the same month, when indeed US non-farm payrolls fell 263,000! Canadian’s may wail and gnash their teeth at the prospects of “par” between the US and Canadian dollars, but the harsh reality is that things are going better economically in the “Great White North” than they are in the Great Moribund South, with the Canadian dollar the beneficiary.

We have been bullish of the C$ for some rather long while, and we remain bullish of it this morning. The fact that the C$/US$ rate fell downward through 1.05 on Friday and is putting 1.04 to test this morning simply confirms our long held thesis that “par” is but a matter of time, and far beyond “par” only a matter longer:

Ed Note: Dennis Gartman will be speaking at the:

The Money Talks All Star Trading Super Summit

Saturday, October 24, 2009 -The Sheraton Vancouver Wall Centre

Click HERE for the Speaker Lineup and to REGISTER if you want to take advantage of this Event.

Mr. Gartman has been in the markets since August of 1974, upon finishing his graduate work from the North Carolina State University. He was an economist for Cotton, Inc. in the early 1970’s analyzing cotton supply/demand in the US textile industry. From there he went to NCNB in Charlotte, N. Carolina where he traded foreign exchange and money market instruments. In 1977, Mr. Gartman became the Chief Financial Futures Analyst for A.G. Becker & Company in Chicago, Illinois. Mr. Gartman was an independent member of the Chicago Board of Trade until 1985, trading in treasury bond, treasury note and GNMA futures contracts. In 1985, Mr. Gartman moved to Virginia to run the futures brokerage operation for the Virginia National Bank, and in 1987 Mr. Gartman began producing The Gartman Letter on a full time basis and continues to do so to this day.

Mr. Gartman has lectured on capital market creation to central banks and finance ministries around the world, and has taught classes for the Federal Reserve Bank’s School for Bank Examiners on derivatives since the early 1990’s. Mr. Gartman makes speeches on global economic and political concerns around the world.

Ed Note: Below is a small excerpt from Mark Leibovit’s Daily VR Trader. The VR Gold Letter is published WEEKLY

We’re Approaching The Important 50% Retracement Level At Dow 10,300+ – Caveat Emptor!

Michael Campbell will be hosting and I will be presenting at the ‘All-Star Trading Super Summit’ on Saturday, October 24, at the Sheraton Wall Centre in Vancouver, British Columbia. Below is his formal invitation. Vancouver is always fun and I get all the salmon I can eat. Hope to see you there. Sign up today!

Precious metals ended yesterday mixed, even though the Dollar fell, as traders exited their “safety” holdings, including Treasuries, the Dollar, and gold. Gold was down 1.40 to 1062.70 after hitting a new record high of 1071.80 yesterday morning. Silver was up 0.10 to 17.88 after setting a recovery high of 18.13. Platinum was up 3 to 1359 and set a new high of 1371. Palladium was up 1 to 327.

I am overall still very bullish, but I was looking for a move in Gold to find resistance (if not a temporary top) near the 1080 level. If we go through there, 1120-1130 is the next benchmark.

From Yahoo.com:

“Famed investor Jim Rogers is “quite sure gold will go over $2000 per ounce during this bull market.” Still, “I wouldn’t buy gold today,” Rogers says. “I think I’ll make more money in other commodities, which are cheaper,” as discussed in more detail here.“

Marks Comment From Tues Oct. 13th

Gold futures held by speculators reached a record high in the most recent week as prices climbed to an all-time high above $1,060 an ounce, raising worries that a possible switch in positions could lead to a slump in gold prices. On the Comex division of the New York Mercantile Exchange, net long, or buying, positions held by speculators rose to 239,668 contracts in the week ended Oct. 6, according to the market regulator, the Commodity Futures Trading Commission. That’s up 6.7% from a month ago and nearly doubled the level at the end of last year, when gold was trading below $900 an ounce. The CFTC’s weekly Commitments of Traders report, released late Friday, also showed that speculative net long positions accounted for 50% of open interest, or the amount of total contracts outstanding. Speculative net long positions topped 50% for the first time ever in mid-September, when gold prices rose to an 18-month high above $1,000. The percentage has since stayed around 50%.

The weekly VR Gold Letter focuses on Gold and Gold shares. The letter is available to Platinum subscribers for only an additional $50 per month and to Silver subscribers for only $70 per month. Email me at mark.vrtrader@gmail.com.

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

The VR Gold Letter is available to Platinum subscribers for only an additional $20 per month, while for Silver subscribers the price is only an additional $70.00 per month. Prices are going up very shortl, so act now! Separately, the VR Gold Letter retails for $1500 a year! The VR Gold Letter is published WEEKLY. It is 10 to 16 pages jam-packed with commentary and charts. Please call or email us right away. Tel: 928-282-1275. Email: mark.vrtrader@gmail.com .

Marks VRTrader Silver Newletter covers Stock, TSE Stocks, Bonds, Gold, Base Metals, Uranium, Oil and the US Dollar.

More kudos – Mark Leibovit was named the #1 Intermediate Market Timer for the 10 year period ending in 2007; the #1 Intermediate Market Timer for the 3 year period ending in 2007; the #1 Intermediate Market Timer for the 8 year period ending in 2007; and the #8 Intermediate Market Timer for the 5 year period ending in 2007. NO OTHER ANALYST SURVEYED APPEARED IN ALL FOUR CATEGORIES FOR INTERMEDIATE MARKET TIMING AS PUBLISHED IN TIMER DIGEST JANUARY 28, 2008!

For a trial Subscription of The VR Silver Newsletter covering Stocks, Bonds, Gold, US Dollar, Oil CLICK HERE

Click on image or HERE to watch a 2:17 minute video interview on Yahoo Finance.

Famed investor Jim Rogers is “quite sure gold will go over $2000 per ounce during this bull market.”

Rogers’ confidence gold will continue to rally stems from a view the U.S. dollar is on its way to losing status as the world’s reserve currency.

“Is it going to happen? Yes,” Rogers says. “I don’t like saying it [and] I’m extremely worried about it but we have to deal with the facts. America is not getting better [and] the dollar is going to be replaced just like pound sterling [was].”

Rogers didn’t offer a timetable, and it’s likely gold would exceed $2000 per ounce if the dollar were to lose its reserve status.

Still, “I wouldn’t buy gold today,” Rogers says. “I think I’ll make more money in other commodities, which are cheaper,” as discussed in more detail here.

Among many others, Rogers is “worried about the fact the U.S. government is printing huge amounts, spending gigantic amounts of money it doesn’t have,” the investor and author says. “People are very worried [and] skeptical about paper money [and] looking for places to protect themselves. The best way is to buy real assets. [That] has always protected one during currency turmoil, and it will again.”

I wasn’t at my friend, Jim Grant’s, famed conference in New York. But I gather Bill Fleckenstein was. Bill notes that John Paulsen, the nation’s most successful trader (he made over two billion last year being short housing) spoke about gold (and I note that Paulsen has a huge position in gold shares). Said John Paulsen, “What I”m looking at is not where gold is going to be tomorrow, one week from now, one month from now, three months from now. What I’m looking is where is gold going to be vis-a-vis the dollar one year from now, three years from now, five years from now. And I think, with a high probability, at each of these points, gold will be higher than it is relative to the dollar today. That probability increases the further out you go. So when I look at what the risk is, the risk to me is far more in staying in dollars than it is staying in gold at this point.”

For more from Richard Russell please see the following:

Hope Is Not A Strategy & A Madman During A Hurricane

THE TWO WAYS TO VIEW THE CURRENT RALLY

Richard Russell is better than fine wine. His thoughts, as always, are excellent. Investors interested in his daily missives would be wise to investigate his website:

There are two ways to view the stock market’s advance from the March lows. One way is to assume that the stock market, despite an awful lot of negative news, is discounting better times ahead. This is the usual way of viewing a steady stock market advance, and it is undoubtedly the way most bulls are thinking.

The other way to view the advance from the March low is that this is the normal and expected recovery following a semi-crash in the stock market. I consider the 2007 to 2009 collapse a semi-crash. The automatic recovery following a crash is the single surest action in the market. Normally following a crash, the market will recoup one-third to two-thirds of the territory lost during the crash. The Dow would have to advance to the 10300 area to recover just half its 2007 to 2009 loses.

Meanwhile, we are facing an extraordinary situation in US finances. Wall Street, or I should say, the Federal Reserve, has bailed out Wall Street banks and entities that were considered “too big to fail.” The actual and potential costs of the financial bailout put US taxpayers on the hook for $17.8 trillion (that’s trillion), which is more than the entire annual gross domestic product of the US.

In 1990 the 20 largest companies in the nation controlled 12% of US financial assets. Today the 20 largest companies control more than 70% of US financial assets. Many of these include corporations that have been deemed “to big to fail.” The Russell comment is “if they’re too big to fail, then they’re too big to exist.” In a true capitalist (not socialist) economy, if you fail you fail and you’re bankrupt. You just haven’t made the “grade.” If any business is so reckless and so ignorant of risk that it goes broke, then damn it — let it go under. And let its CEO and board be accountable. But that’s hardly what’s happening in the US today.

While the run of Americans are struggling with their economic lives, the big bankers are back “in business as usual,” paying out billions of dollars in bonuses and making profits on the backs of the taxpayers who bailed out these incompetents. And ironically, these same blundering bankers are now throwing road blocks in front of meaningful regulatory reform.

Even worse, the Congressional Budget Office estimates that the 2009 budget deficit will be almost $1.4 trillion, which is about 10% of GDP. As of September, 2009, the interest on the national debt was $383 billion or more than one billion dollars for every day of the year! By 2010 the national debt will be $20 trillion, and the US will be borrowing to pay just the interest on its out-of-control debt.

I prefer to keep it simple and basic. I look at the whole picture from a Dow Theory standpoint. A basic principle of Dow Theory is that the primary trend of the market and the economy cannot be manipulated. The primary trend, one way or another, will run its course to conclusion, despite the wishes or efforts of any government or congress or president or central bank.

In their effort to halt or reverse the primary bear trend, Bernanke and Geithner have virtually bankrupted the US. Their frantic efforts to “pump up” the US economy with an ocean of Fed-created junk money and zero interest rates have failed to inspire America’s consumers to go back to their high-spending ways. For the retail stores and chains, the “back-to-school” session has been a dud. Leading retail experts are already warning of a “slow to disastrous Christmas season.” The age of thrift has descended on America. And all the wild Fed and Treasury spending has only served to frighten US consumers into (can you believe?) saving.

Now the fright has moved into anger. Americans see that the Wall Street banks and Goldman have been saved. But what about the man on the street? Politicians respond to only two things — money and votes, and the pols are currently quaking at the thought of the next elections.

As far as Bernanke is concerned, there is only one path to follow — keep doing what you’ve been doing. More liquidity, keep the rate at zero, continue blabbing about “green shoots,” issue more propaganda about “the economy improving.”

Ironically, the talk has now turned to an “exit strategy” for the Fed’s program. This would mean raising interest rates and cutting back on government spending. Bernanke knows that at this point reversing the Fed’s stance would be disastrous. It could throw the nation into a deep recession or depression.

The exploding deficits and skyrocketing debt of the US are not lost in real money — gold. As the world’s central banks create new currencies in order to stem any rise in the dollar, all fiat currencies weaken. It now requires an increasing amount of junk currencies to buy an ounce of gold. Thus, against the time-honored standard, gold, fiat monies around the world are losing value or purchasing power. When it takes more of a currency to purchase a hamburger or a bicycle or an ounce of gold, you’re talking about inflation.

![]()

The author of The Pragmatic Capitalist is the founder and CEO of an investment partnership. Prior to establishing his own business, TPC was a Merrill Lynch Financial Advisor. TPC is a Georgetown University alumnus, growing up in the DC area and now living in Southern California.

The Pragmatic Capitalist is a jack of all trades. Rather than focus on one facet of the U.S. equity markets, the goal is to assess and address global capital markets as a whole – with the understanding that all markets are intertwined and being an “expert” in one segment of the market without a vast knowledge of the others is futile.

The saying “common sense is very uncommon” has never been more applicable than it is to modern markets. TPC attempts to approach markets with sound reasoning and as little emotion as possible. A capitalist through and through, but always pragmatic…

Research

TPC uses a top down investment approach. The research and market methodology is based on cognitive science and the theory of chaos. Through the understanding of market psychology you can derive that markets are non-linear dynamical systems which are susceptible to inefficiencies. Markets are inefficient in short time periods due to their chaotic nature (a symptom of human psychological irrationality). This creates opportunity.

Based on this methodology we employ risk management structures that account for the possibility of short-term inefficiencies and random occurrences within large and liquid systems. Although there are short-term opportunities in markets, risk management is the overriding factor in achieving high absolute returns. Black swans cannot be predicted, but they can be avoided by employing proper risk management. This analytical, quantitative and systematic approach helps us in achieving our goal of high absolute returns.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair